News

22 Jun 2022 - It's time to take advantage of share price falls

|

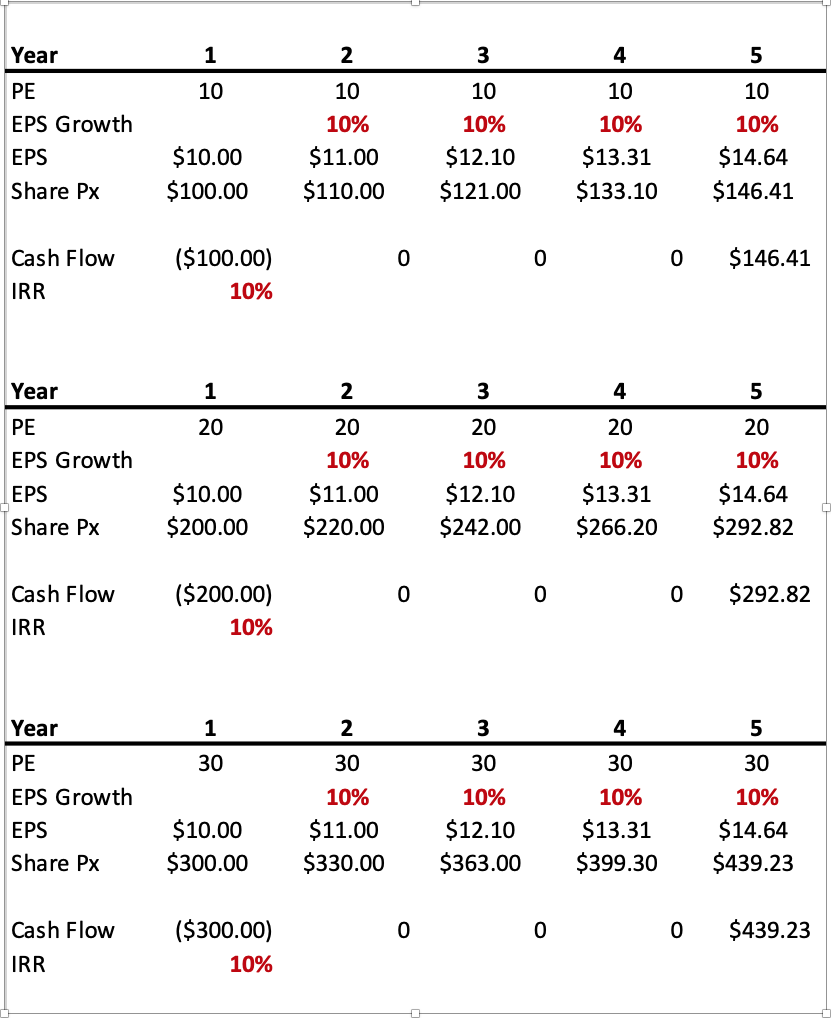

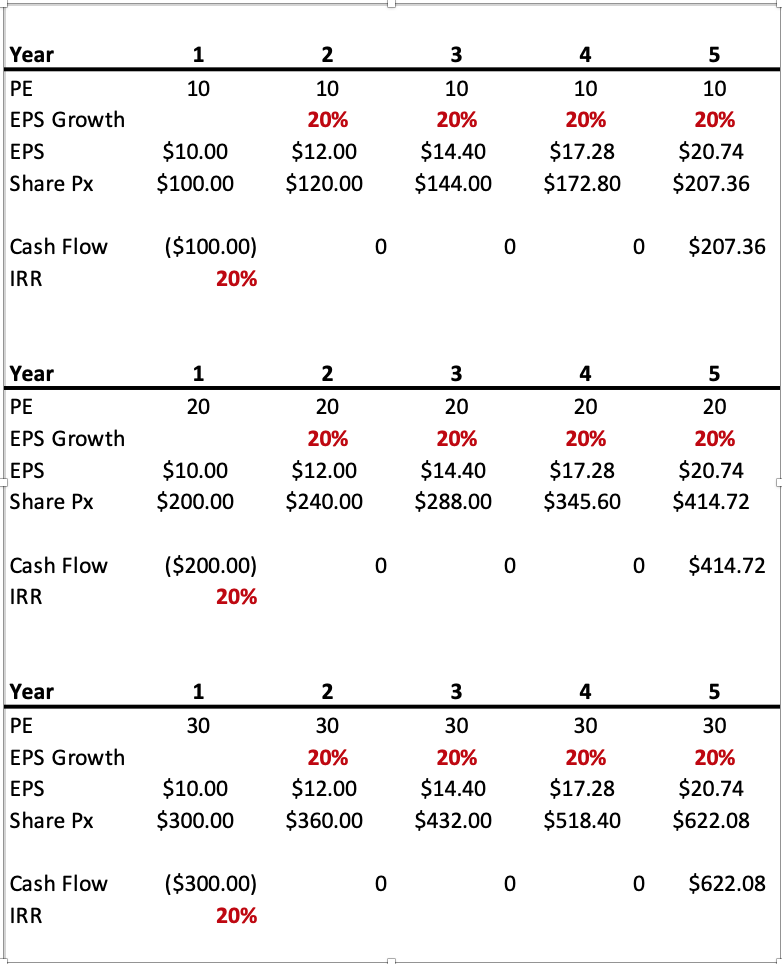

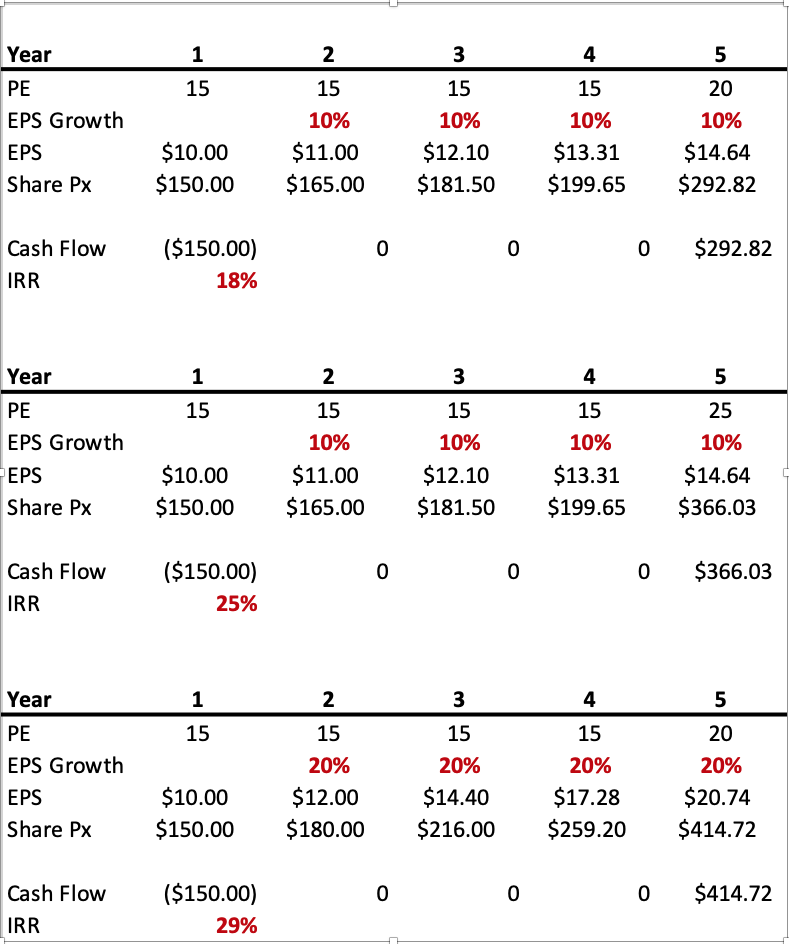

It's time to take advantage of share price falls Montgomery Investment Management May 2022 The price-to-earnings ratios of many quality businesses have fallen sharply over the last six months. In many cases, the falls were justified. Now that valuations have dropped, I believe investors have a far better chance of making attractive returns. The proviso, of course, is that you buy businesses that grow their earnings. Celebrating the recent fall in share prices might be a step too far, but investors who plan to be net buyers of equities should be at least a little excited about the recent declines. The ASX 200 decline year-to-date of just 3.4 per cent masks the more serious declines of even the highest quality companies. Indeed, 112 of the biggest 200 companies listed on the ASX are below their price at the beginning of the year. And the average decline is 17.7 per cent. The median decliner is down 15.4 per cent. Zip is off 76 per cent year-to-date, Pointsbet is down 60 per cent, Kogan is 47 per cent lower, Boral is 43 per cent below its price at the beginning of the year, and even high-quality company, Reece, is 38 per cent weaker. Meanwhile, other high-quality companies such as REA Group, Wesfarmers, ARB Corporation, Credit Corp and Super Retail Group are off between 15 and 25 per cent in less than 16 weeks. Of course all of this is happening because inflation is surprising to the upside, scaring many investors as well as central bankers. And in response the central bankers are reversing the massive stimulus that was foisted on markets and economies in response to COVID-19. The punch bowl that drove massive asset inflation during the pandemic is being taken away. It really is as simple as that. The US Federal Reserve will put its balance sheet on a new course, reducing its size by up to a trillion US dollars per year. So there's no debating; we are in the midst of a correction. There is however a silver lining. PE ratios have compressed materially over the course of the last six months. Now that they are lower, investors have a better chance of making attractive returns, provided they buy businesses that can grow earnings. Let me explain with a few simple tables. Table 1. Internal rates of return equal earnings growth when PEs remain constant. Table 1 demonstrates the investor's return, from buying and selling a share at the same PE multiple, matches the rate of earnings growth. In all three examples the earnings growth is 10 per cent per annum. It matters not whether the stock was purchased at 10, 20 or 30 times earnings; the investor's internal return will match the earnings growth rate provided the shares are sold at the same PE multiple that was paid for them. Table 2. Internal rates of return equal earnings growth when PEs remain constant Table 2 simply reinforces the earlier point. On this occasion the EPS growth rate is 20 per cent in all cases and irrespective of the PE the investor's return matches the EPS growth rate provided the shares and purchased and sold on the same PE. China's economic woes, the invasion of Ukraine, supply chain disruptions and the possibility of recessions and stagflation have all offered reasons for investors to sell stocks to the extent PE's have compressed materially. As I mentioned earlier however it doesn't matter what the contemporaneous catalysts are, throughout history whenever rates go up or inflation accelerates, PE have compressed - without exception. Now that PEs have compressed, investors must find businesses whose earnings will grow. Warren Buffett once observed: "Your goal as an investor should be simply to purchase, at a rational price, a part interest in an easily understood business whose earnings are virtually certain to be materially higher, five, ten, and twenty years from now." Compressed PEs may offer that "rational" price. PE ratios can of course fall further and any escalation of tensions between Western allies and China or Russia would certainly do that. Investors would have to simply ride through what we all hope would be a temporary interruption to the peace the western world has mostly enjoyed since the fall of the Berlin Wall. To protect oneself from the idiosyncratic risk of PE contraction, it is important that not only does the company's earnings grow, but they grow at a rate that meets or exceeds market expectations. If growth is expected to be 20 per cent and comes in at 18 per cent, the PE may contract further, offsetting the benefits accrued to investors from the earnings growth. Table 3. A bonus from PEs bouncing. Assuming global peace is maintained, investors have another benefit from investing after PE compression. Inflation will eventually peak and interest rates will eventually stop being raised. At that point PE ratios may start to expand again. Table 3 reveals the bonus in terms of internal rates of returns earned by investors from a jump in PE ratios at the time of sale. In the first example, shares are purchased on a PE of 15 and earnings grow by 10 per cent per annum. If the PE stayed at 15 at the time of sale, the investor would earn 10 per cent per annum. But in this example, in the final year, the PE jumps to 20 times. The result is an 18 per cent per annum return. PE compression and stock market falls may just be the rational price investors in equities and managed funds have been waiting for. Author: Roger Montgomery, Chairman and Chief Investment Officer Funds operated by this manager: Montgomery (Private) Fund, Montgomery Small Companies Fund, The Montgomery Fund |

21 Jun 2022 - Megatrends drive sustainable growth

|

Megatrends drive sustainable growth Insync Fund Managers May 2022 Megatrends enable us to locate the sustainable outsized market growth opportunity stock hunting-grounds (as well as help us avoid those that will dwindle). They are the 'fuel' to quality company's sustainable growth earnings. We are presently in the midst of one of the most disruptive innovation cycles in technological history. Thus, we resist the temptation of concerning ourselves with near term timing based 'market rotations' and changes in 'sentiment'. These distractions will otherwise prevent us from generating outsized returns in the years ahead. PWC consulting estimates that global GDP will be up to 14% higher in 2030 as a result of the accelerating development and take-up of AI. The equivalent of an additional $15.7 trillion USD.

Internet of people v Internet of Things Our lives are already being impacted. In the past 5 years alone, almost all aspects of how we work and how we live - from retail to manufacturing to healthcare - have become increasingly digitised. The internet and mobile technologies drove the first wave of digital, known as the 'Internet of People'. Analysis carried out by PwC's AI specialists anticipate that the data generated from the Internet of Things (IoT) will outstrip the data generated by the Internet of People many times over. This is already resulting in standardisation, which naturally leads to task automation and the automatic personalisation of products and services - setting off the next wave of digital progress. AI exploits digitised data from people and things to automate and assist in what we do today, how we make decisions and how we find new ways of doing things that we've not imagined before.

From one of the all-time ice hockey greats this very apt thought describes the way Insync frames its investment thinking. Despite the market's sentiment shift on the rotation trade, Insync's focus is on where the world is moving to. Data continues to show an acceleration in spending on pets, the rollout of 5G, health & wellness, and digital transformation Major corporates expect elevated growth in technology to both accelerate and persist for the foreseeable future (according to a Morgan Stanley survey), in areas such as cloud computing, digital transformation and artificial intelligence. CIO intentions indicate that they expect to increase IT spend as a percentage of revenue over the next three years than they did pre-pandemic. The percentage of CIOs planning to increase spend versus those planning to decrease spend is known as the up-to-down ratio. It rose to 9.0, nearly 6x the pre-pandemic 2019 average. The best way to invest in a megatrend isn't always the obvious way!

Semiconductors are driving the digital transformation of the world. Covid19 has had a profound impact on so many industries but one of the key areas everyone has started to care about are silicon chips. This became abundantly clear when new car purchases were dramatically delayed because of chip supply chain shortages. Semiconductor chip usefulness has gone further than any other technology in connecting the world. The companies that produce them enables us to do pretty much everything, from the smartphones in our pockets to the vast datacentres powering the internet, from electric scooters and cars to hypersonic aircraft, and pacemakers to weather-predicting supercomputers. Their manufacturing requires a high level of specialist technological know-how as it is a highly expensive, complex and a long process. It typically takes 3 months and 700 different steps to cover a silicon wafer with intricate etchings forming billions of transistors (microscopic switches that control electric currents and allow the chip to perform tasks).

Semiconductor chips lay at the heart of the exponential transition that we're going to experience in computing over the next 5-15 years. More than we have ever witnessed before, and it will continue to grow exponentially. For example, AI applications process vast volumes of data-about 80 Exabytes pa today. This is projected to increase to 845 Exabytes by 2025. One Exabyte = One quintillion bytes = one thousand quadrillion bytes. Truly eye-watering numbers. Insync's investments in the most profitable semiconductor companies enable investors to participate in 3 of the 16 enduring megatrends: video gaming, workplace automation and enterprise digitisation. Their earnings growth will continue to compound at high rates with the resulting share price growth following. This is a consistent feature of the 29 companies in the portfolio. Patience will reward. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

20 Jun 2022 - Winning by not losing

|

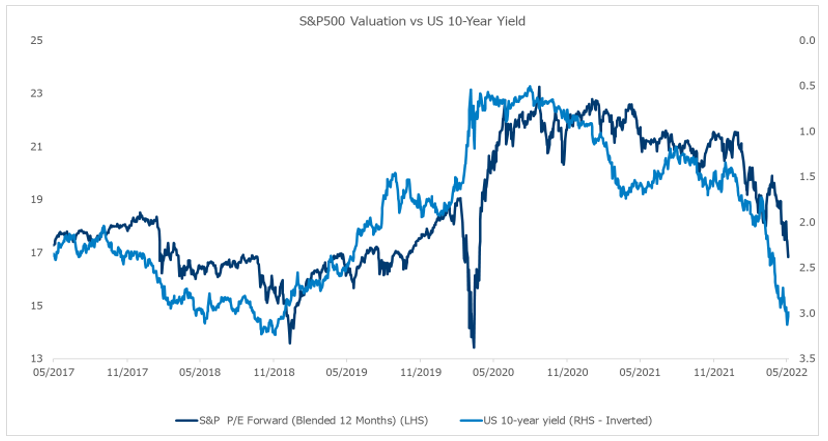

Winning by not losing Alphinity Investment Management May 2022 Investing in global equity markets has felt like playing a game of dodgeball over the last two years. Around every corner investors have been faced with a new surprise to navigate. Just as in dodgeball, where players run for cover to avoid the sting of those dreaded balls, equity investors have flocked to the safety of defensive stocks in 2022. Year to date defensives have outperformed value, growth and cyclical stocks, doing what they are supposed to do in uncertain times: offer equity investors a shield against the onslaught of valuation pressures, slowing earnings growth and increased uncertainty. As we continue to brace ourselves for ongoing volatility in equity markets, we prefer to maintain exposure to selective stocks with defensive characteristics - those that are winning by not losing. Deutsche Boerse and Merck & Co are two such examples. The big de-rating might not be overGlobal equity markets have de-rated since the recent peak in September 2020, with a sharper deceleration in 2022 driven by rising inflation fears as reflected in higher 10-year bond yields. In fact, most major market indices are now trading below their pre-Covid valuation levels. The derating has been particularly evident in the more expensive parts of the market, such as Technology stocks. For example, the Nasdaq Composite Index has fallen by -25% so far this year, with most of this occurring through forward PE multiples contracting from ~32 to ~23x currently. In comparison, the S&P 500 has fallen 16% and contracted from ~22x to ~17x over the same time frame. All major equity markets have derated sharply YTD to below pre-Covid levels

Source: Bloomberg, 10 May 2022 Despite this overall market de-rating, most major indices are still trading in line or above their 20-year averages and remain relatively high when considering the sharp rise in 10-year yields (see chart below). The Russia Ukraine War has also recently pushed commodity prices to new highs, raising inflation risks and potentially placing further pressure on market valuations. Valuations may be at more risk as bond yields continue to surge

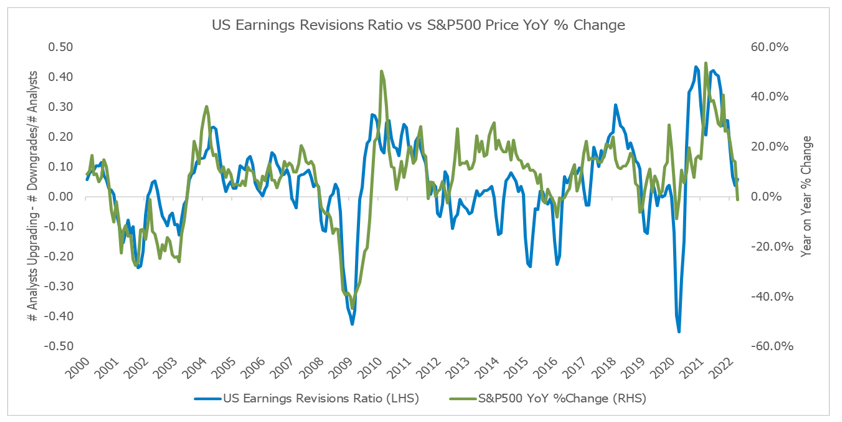

Source: Bloomberg, 10 May 2022 Investors' fears are shifting from inflation to growthUS GDP has surged past prior cycle peaks but is now decelerating sharply. Similarly, while 1Q22 earnings were modestly ahead of expectations on average, management commentary and guidance about the outlook has been increasingly cautious, prompting analysts to downgrade earnings forecasts for both '22 and '23. In fact, earnings revisions breath has been declining since August 2021 and has recently moved outright negative. Given the wide range of headwinds companies currently face, which include cost pressures, supply chain constraints, inventory build ups and potentially weaker demand from higher prices and lower global growth, it's likely that earnings revisions will remain negative for the foreseeable future. This has historically been associated with weak overall market performance (see below). Earnings Revisions and Price are highly correlated

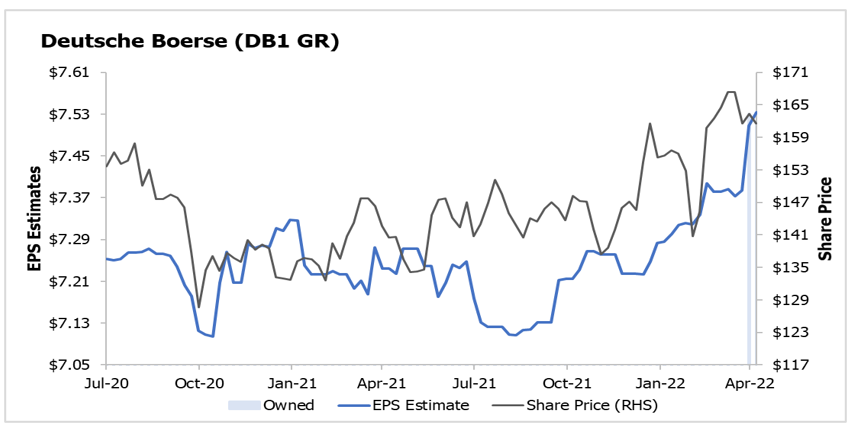

Source: Alphinity, Bloomberg, 3 May 2022 Earnings leadership has taken another step to being more defensiveAt a sector level, we have however seen a sharp contrast with the classic defensive sectors, such as Utilities and Consumer Staples outperforming the overall market year to date, driven by a superior ratings performance as well as better earnings revisions versus their cyclical peers and the broader market (excluding the Energy and Materials). Defensives have a strong track record of outperforming during slowing growth/recessionary periods, a relative safe-haven within periods of market stress. With a broad range of defensives already reflecting these benefits in relatively high valuations, active investors need to remain nimble and look for new opportunities. Some of these might not be seen as typical defensive plays, such as Merck & Co referred to below, but they offer defensive characteristics that should bode well in a volatile environment. One such defensive earnings leader is Deutsche Boerse. Just as in a dodgeball game, there are certain times in the market cycle when it is not always about running the fastest, but also about finding the best places to hide. Deutsche Boerse- Leading stock exchange enjoying multiple cyclical & structural tailwindsDeutsche Boerse (DB1) is a high-quality owner of various key pieces of financial market infrastructure in Europe across pre-trading, trading & clearing and post-trading. These assets include Institutional Shareholder Services (ISS), Eurex (leading European financial derivative exchange), EEX (a commodities trading & clearing exchange), Xetra (cash equities) and Clearstream (a leading European settlement & custody provider). These businesses all tend to command dominant or leading market positions within their segments, and as such enjoy significant barriers to entry and high margins. These diversified businesses generate resilient mid-cycle digit % secular growth, which we expect to be further boosted by various cyclical tailwinds, including both higher interest rates and higher interest rate volatility, as well as further targeted M&A. Consequently, we expect the company to exceed management's net income growth target of 10% (CAGR) for FY19-23E. With positive earnings revisions and a relatively undemanding valuation multiple (current forward PE of ~21x), we continue to see more upside for DB1 in the current environment. Deutsche Boerse - More defensive Earnings supported by several cyclical and structural factors

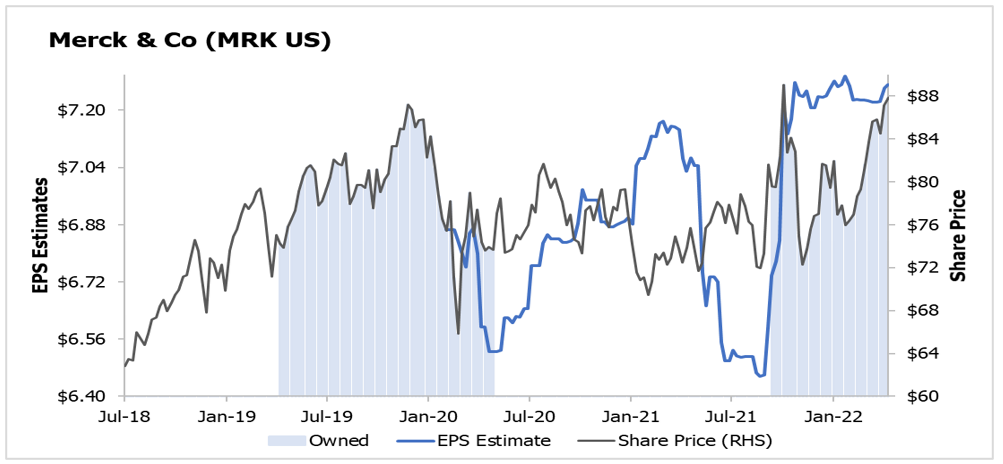

Source: Bloomberg, 10 May 2022 Merck & Co- A high quality defensive with flagship growth products & consistent earningsMerck & Co (MRK) is a global pharmaceutical company that delivers health solutions through its prescription medicines, vaccines, biologic therapies, animal health and consumer care products. MRK recently reported an impressive 1Q22 result with both revenue and earnings beating consensus expectations and the company raising 2022 guidance for both despite an expected FX headwind, driven by strength across the portfolio. Despite the relative outperformance and re-rating from 10x to 12x YTD, we maintain our position in this flagship defensive at this juncture with two main drivers for our investment case: 1) Product growth of the existing portfolio: Both the flagship growth products Keytruda (the largest selling drug in the world, innovative immuno-oncology, 30% of group revenues) and Gardasil vaccine (blockbuster vaccine against papilloma virus/cervical cancer, ~9% of group revenues) continue to grow ahead of expectations with their high quality Animal Health business (the third largest in the world) enjoying above market growth rates. 2) Business development: Management continue to look for new M&A opportunities to expand the business, underpinned by a strong balance sheet, with gearing at only ~2x EBITDA. Earnings growth underpinned by a portfolio of strong flagship products

Source: Bloomberg, 10 May 2022 Author: Elfreda Jonker, Client Portfolio Manager This information is for adviser & wholesale investors only |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Sustainable Share Fund |

17 Jun 2022 - Fears about green inflation overblown

|

Fears about green inflation overblown abrdn 07 June 2022 Fears that the global transition to a low-carbon economy will drive inflation over the long term are overblown, with the tightening of monetary policy set to have far greater implications for portfolios. Some observers point to the energy transition as inherently inflationary, with companies compelled to invest less in fossil-fuel energy at a time when the costs for renewable energy remain elevated. The market has labelled this green inflation - the contribution that environmental policies have on the cost of delivering goods and services that is passed on via supply chains to consumer prices. In truth, there are a variety of regulations and policies that can influence inflation. The international push-back against globalisation - for example, the continued imposition of trade tariffs - is one of the forces putting upward pressure on prices. While the pandemic has highlighted the fragility of global supply chains and logistical networks, Russia's invasion of Ukraine has extended inflationary drivers by delaying the recovery process and amplifying commodity price pressures as the war restricts access to energy, metals and grains. However, the reason that the US has an inflation problem is not due to climate policies, but because its economy was overstimulated as it emerged from Covid-19. The US retained accommodative monetary and fiscal policies for too long, and now its labour market is running red hot. A multi-year commodity boom in areas of renewable energy that require specialist components - such a rare earth metals - is possible owing to high demand and limited supply. But overall, we don't see green inflation as a meaningful contributor to rising consumer prices over the long term. Climate policies tend to operate over decades, meaning they're a structural driver of relative prices. However, at an aggregate level, consumers will only ever experience sustained high inflation if major central banks allow that to happen. Even if we were to see sustained commodity price increases, we would not expect headline inflation to remain above central bank targets for extended periods. We urge investors to look beyond the short term and think about the likely disinflationary consequences of prolonged global policy-tightening in the pipeline. We urge investors to think about the likely disinflationary consequences of prolonged global policy-tightening in the pipeline. What we're seeing now is central banks reacting to excess inflation, and we expect them to prioritise anchoring inflation over growth. We don't think we'll be debating green inflation in two years' time, rather the consequences of a US recession that came sooner than expected. Really, the narrative around green inflation is being driven by what's happening in the West. On the whole, inflation is far lower across Asia Pacific, where climate policy is at a much earlier stage of implementation and there aren't the same constraints on the fossil fuel sector. Moreover, delays in the reopening of Asian economies post Covid-19 has led to more subdued activity levels. Asia's growing importanceOne key question for investors to consider is the role that Asia Pacific will play in the technological innovation required to effect the global energy transition, and whether that will be disinflationary. From a macroeconomic perspective, policy initiatives by governments and central banks in Asia Pacific have been more prudent, with less willingness to prop up markets artificially. The region has far lower debt levels, fewer constraints on governments and strong state capacity to act. There's tremendous capital available to Asian governments and companies to effect the energy transition. We believe Asian companies will play an increasingly prominent role in investor portfolios. There can be no energy transition without Asia, where industrial pollution has forced governments to act. Heavy investment has brought the cost of technology down sharply over the past decade. Solar power became cheaper than coal-fired energy by 2015 in India, enabling it to invest in renewable energy quite aggressively. We think the technological innovation we are seeing at Asian companies to solve real world problems should be better reflected in portfolios. Some of these companies are working hard to bring down the cost of green hydrogen. Nowhere is this more relevant than China's highly polluting manufacturing sector, which needs to embrace new energies to clean up entire supply chains. China wants to do for green hydrogen what it has already done for solar technology and some wind turbine technologies. We're optimistic, since it will only take progress in countries such as India and China to have a marked impact on correcting some problems the planet is facing. Ultimately, we want to see the power of capitalism and innovation turned towards the global energy transition. But wealthier nations need to live up to their commitments to assist poorer countries so that they don't routinely get left behind. While China will continue to play a critical role in bringing down the costs of technology, this will take time and poorer countries will need support in the interim. Of course, asset managers have parameters on what they can and can't invest in. Poor countries often have low credit ratings, governance problems or capital markets not fully formed. We must find a way to mobilise capital to benefit these countries; it's part of the equation that needs solving. In the near term, some solutions will appear inflationary. Electric vehicles, for example, are more expensive than those with internal combustion engines. Yet electric vehicles is where we see relative prices falling the most - and that's true of a wide range of renewable technologies, such as solar PV. But forces that appear inflationary today can be disinflationary in future. There will also come a time when commodity prices fall, and as a big commodity importer Asia would be a major beneficiary. What's incumbent on asset managers when promoting sustainable investments is to communicate that it's a long-term decision. Commodity and fossil-fuel-intensive businesses are doing well because production costs have risen more slowly than prices, which is good for earnings and valuations. Conversely, valuations among renewables became expensive at times last year because many of the businesses are growth firms, so as the interest-rate structure increased, the discount rate applied to their earnings also increased - leading to significant underperformance. What it underlines is that investors are likely to experience plenty of variance along the way. Even if you're confident that central banks will get on top of this problem eventually, strategies that seek to manage inflation and volatility will be appealing from a portfolio perspective over the near term.

Author: Jeremy Lawson, Chief Economist, abrdn Research Institute |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund , Aberdeen Standard Life Absolute Return Global Bond Strategies Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund |

17 Jun 2022 - The Rate Debate - Episode 28

|

The Rate Debate - Episode 28 Yarra Capital Management 04 May 2022 Has the RBA hit panic mode? With rates on the rise, higher inflation and wages below expectation, has Australia's central bank panicked by hiking rates by 50bps, the largest monthly move in over 20 years? The RBA's charter is to ensure the economic prosperity and welfare of the Australian people, which increasingly appears to be being overlooked in favour of an inflation target that isn't easily achievable without causing recession. |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

16 Jun 2022 - Why it's all about Earnings Growth

|

Why it's all about Earnings Growth Insync Fund Managers May 2022 Why it's all about Earnings Growth Companies that sustainably grow their earnings at high rates over the long term are called Compounders. Investing in a portfolio of Compounders is an ideal way to generate wealth for longer-term oriented investors that tend to also beat market averages with less risk. This chart shows the tight correlation between returns of the S&P 500 (orange line) and earnings growth (blue line) since 1926. NB: Grey bars are US recessions

Insync's focus is on investing in the most profitable businesses with long runways of growth resulting in a portfolio full of Compounders. Inflation & interest rate impacts By focusing on identifying businesses benefitting from megatrends with sustainable earnings growth, means we do not need to concern ourselves with market timing, economic growth forecasts, inflation, or the future of interest rates. Throughout the last 100 years we've experienced periods of high economic growth, recessions, different inflation and interest rate settings, wars, pandemics, crisis and on it goes, but the one thing that has remained consistent... Over the long term, share prices follow the growth in their earnings. Media and many market 'experts' continue to be concerned about the risk of a sustained period of higher inflation. They worry over a short-term 'rotation' from quality growth stocks of the type Insync seek to own to value stocks. The latter in many cases is simply taken as equating to lowly rated companies and reopening stocks, such as airlines, energy, and transport. There are 3 problems with this view that can trap investors:

In sharp contrast good businesses remain strong at this stage of the cycle. They continue delivering the earnings growth that propel share prices over the long term. This is what makes their share price progress both sustainable and well founded. High margins and superior pricing power from Insync's portfolio of 29 highly profitable companies across 18 global Megatrends offers "the holy grail" of inflation-busting companies. Pricing power, sound debt management and margin control allow great companies to handle inflation and interest rates well. LVMH and Microsoft (featured in October update) are portfolio examples that recently increased prices of their products with no impact on their sales growth. Profitability + Revenue Growth Short term, investors typically fret over interest rate rises and all growth stocks suffer initially, as they adopt an indiscriminate machine-gun approach to selling. Over time however, the more profitable businesses with strong revenue growth start to reassert their upward trajectory in their share prices, as investors appreciate their long-term consistent earnings power. Stocks with "quality growth" attributes, such as high returns on capital, strong balance sheets, and consistent earnings growth, have typically outperformed in past situations similar to what we face today (Mid-2014 through early 2016 and from 2017 through mid-2019. Source- Goldman Sachs).

This is in sharp contrast to stocks with strong revenue growth projections that also have negative margins or low current profitability. They are highly sensitive to changes in interest rates (These stocks propelled the short-term returns of many of the Growth funds in 2021). Many of them lack profit and cash flow, which doesn't give you much downside protection if they don't deliver. Many rely on the constant supply of new capital to fund their operations. These types of companies have very long durations because their present values are driven primarily by expectations of positive cash flows at a distant point in the future. We call this HOPE. As the saying goes; we don't rely on hope as a sound strategy. Stocks with valuations entirely dependent on future growth in the distant future are vulnerable to a dramatic drop in price if rates rise sharply or revenue growth expectations are reduced. This chart (performance of the Goldman Sachs Non-Profitable Tech Basket) shows the downside risk to this sector of unprofitable high revenue growth companies. The index has fallen by close to 40% from its peak in February 2021. The index consists of non-profitable US listed companies in innovative industries.

Unsurprisingly, popular "new era" stocks held by high growth managers have also suffered a similar fate with examples noted below.

Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

15 Jun 2022 - Manager Insights | Magellan Asset Management

|

|

|

|

Damen Purcell, COO of FundMonitors.com, speaks with Chris Wheldon, Portfolio Manager at Magellan Asset Management. The Magellan High Conviction Fund has a track record of 8 years and 8 months. On a calendar year basis, the fund has only experienced a negative annual return once since its inception and has provided positive returns 88% of the time, contributing to an up-capture ratio for returns since inception of 83.03%.

|

15 Jun 2022 - Why "making dirty cleaner" is key to 2030

|

Why "making dirty cleaner" is key to 2030 Yarra Capital Management May 2022

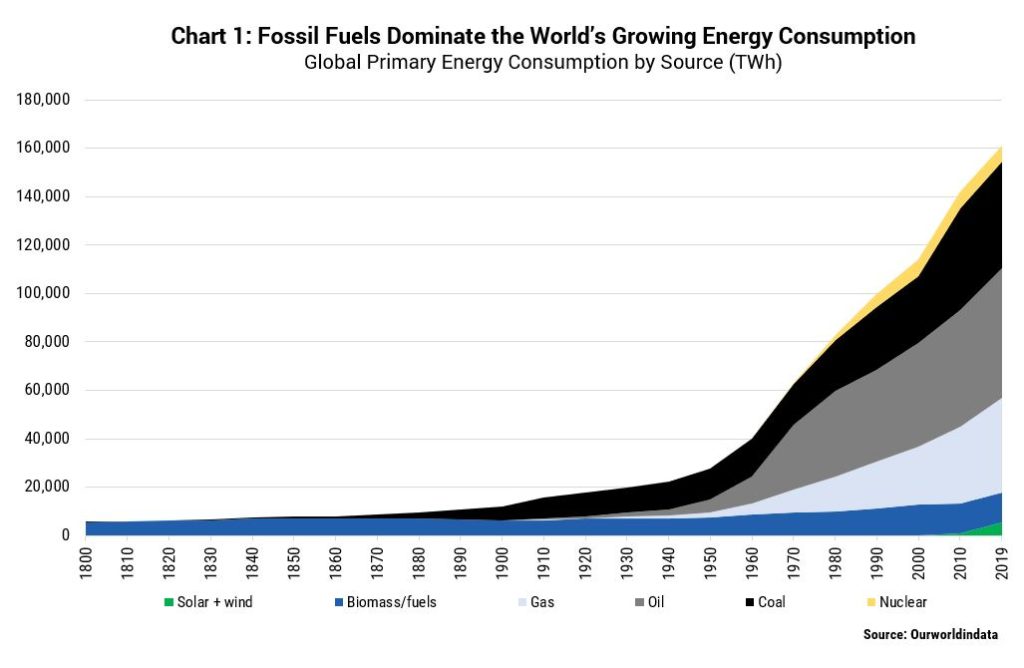

As Australia resets to a more ambitious 2030 emissions target under a new Labor government, it's time we address the largest opportunity on our pathway to net zero emissions: "making dirty cleaner". David Gilmour, Portfolio Analyst and ESG Specialist, details why. As Australia resets to a more ambitious 2030 emissions target under a new Labor government, it's time we address the largest opportunity on our pathway to net zero emissions: "making dirty cleaner". For too long, sustainability investment has centred on future facing industries, like renewables, and blatantly ignored the dirtiest industries. The focus has been on the cure to emissions, with no consideration to prevention. Divestment has been the weapon of choice. The Ukraine-Russia war has been a wake-up call. Fossil fuels, despite Western efforts to curb supply, are necessary for energy security when global trade is dividing into geopolitical blocks. What's more, they continue to dominate the world's growing demand for energy (Chart 1). To break their nexus with economic growth - and simultaneously transition without widening wealth inequality - we need to solve the demand side for both industry and the consumer. And that requires investor support and engagement.

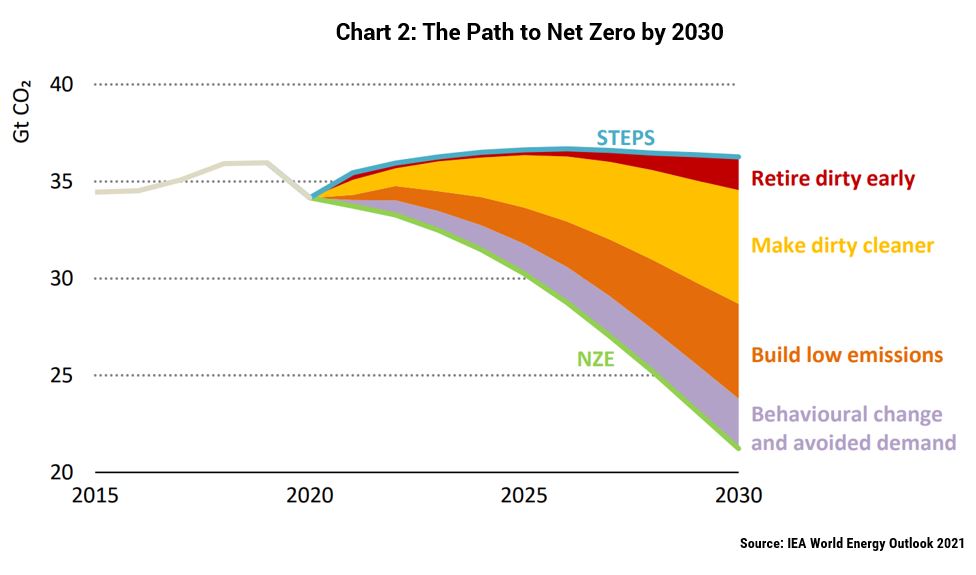

According to the International Energy Agency (IEA), we cannot simply divide energy investments into "clean" and "dirty". In fact, the largest part of emissions reductions under its net zero scenario - the same one purists cite when arguing to cease new fossil fuel production - comes from a middle ground of "transition" investments (Chart 2). Examples include project enhancements to reduce methane leakage, efficiency or flexibility measures in industrial processes, coal-to-gas switching (e.g. new gas boilers), refurbishments of power plants to support co-firing with low emissions fuels, and gas-fired plants that enable higher renewables penetration.

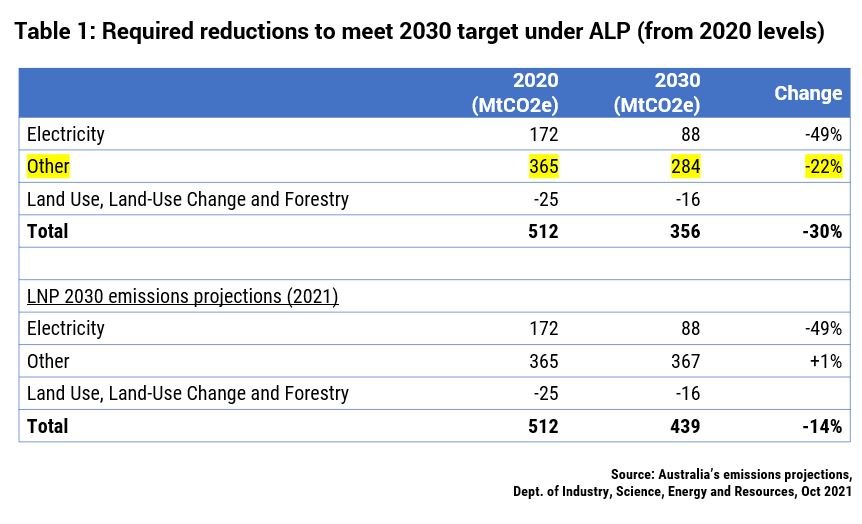

Within Goldman Sachs' latest forecast for a 37% fall in US emissions by 2030[1] (below the Biden Administration's target 50-52% reduction), energy efficiency is the first of three themes driving emissions lower over the short term. Outside Utilities, GS forecasts the biggest reductions to come from Oil & Gas Producers, Diversified Metals & Mining and Aluminium[2] - sectors where ownership by ESG focused investors is limited. Domestically it's a similar story. Like the US, Australia's electricity sector only accounts for around 30% of total emissions. Labor's new target for a 43% reduction on emissions to 2030 (based on 2005 levels) will require substantive efforts from Industry and Transport since, as we discussed last year, the Electricity sector is already stretched to its limit with a forecast 49% reduction by 2030 from today's levels. When you dig into the numbers, Labor's target equates to -30% on 2020 emissions levels, from 512MT today to 356Mt in 2030. This compares to the Coalition's projection for 439MT by 2030 (-14%) (Table 1). If we assume no further emissions reductions in the electricity sector under Labor, then it needs a -22% reduction in emissions from the "Other" sources, versus the Coalition's former forecast for +1%.

The new Federal government has also committed to strengthening the existing Safeguard Mechanism (SGM) to support its national target. Currently, Australia's largest emitting facilities (>100,000 tonnes per annum) have to purchase credits (ACCUs) when their emissions rise above generously set baselines. We support Labor's proposal to reduce these baselines over time which, if enacted, will drive greater energy efficiency and lowest-cost abatement solutions. Investors must also play an important role. We believe strongly in company engagement over exclusion; the former can lead to outperformance, while the latter shifts ownership to parts of the market with less oversight and deprives companies of capital when they need it most. That's why we are shareholders in high emitters such as Alumina (AWC), a company with a harder pathway to net zero but has the capability to benefit from the transition. AWC is already among the lowest emitters among major alumina producers, is pursuing early-stage technologies and is a clear beneficiary of green capex given the expected growth in demand for aluminium (39% demand growth to 2030[3]). We are also overweight Worley (WOR), which is well positioned to capture higher structural demand from energy transition work over and above its traditional work for the oil & gas industry. Once we solve the demand side, we expect supply from the oil & gas industry will take care of itself as customers evaporate. Until then Australian gas producers enjoy a privileged position. They are low sovereign risk for European countries weaning themselves off Russian gas, and will contribute significantly to lowering emissions in Asia as coal-to-gas switching takes place. Early this year we established a position in Woodside Petroleum (WPL), a company which predominantly produces gas and has a new strategy to invest $US5bn in new energy opportunities by 2030. Our focus remains on working with management to strengthen its 2030 interim target and lower its reliance on offsets. As ever, we continue to test the resolve of Australian companies to reduce their exposure to climate change risks and whether they are pursuing the right opportunities in the transition. Importantly, we have no intention of sidelining companies that provide critical products, especially when cleaning up their operations will cause the largest reductions in global emissions to a low carbon future. |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund [1] Source: Goldman Sachs: The path to lower US emissions, and what can drive impact, May 2022.

|

14 Jun 2022 - Record high inflation could trigger a fresh eurozone financial crisis

|

Record high inflation could trigger a fresh eurozone financial crisis Magellan Asset Management May 2022 Italy's 66th post-war government collapsed in January 2021 when Prime Minister Giuseppe Conte was forced to resign after former premier Matteo Renzi removed his minor Italia Viva party from the ruling coalition. President Sergio Mattarella encouraged the parties to revive the alliance so he could avoid calling a snap general election during a pandemic. But the talks went nowhere. As concerns grew that any election might usher right-wing populists into power, Mattarella pulled off a masterstroke. In early February, Mattarella unexpectedly contacted Mario Draghi; yes, 'Super Mario' who saved the euro in 2012 with his 'whatever it takes' comment. Mattarella asked the chief of the European Central Bank from 2011 to 2019 to begin talks to form a 'national unity' government. Within days, Draghi had won a parliamentary majority to become Italy's 29th prime minister since 1946 and its fourth unelected (or 'technocratic') premier since 1993.[1] Investors were pleased. On February 13 when Draghi assumed office, 'lo spread' - the yield at which Italian 10-year government bonds trade over their German equivalents, a number that is judged the bellwether of EU economic and political risks - had narrowed to a five-year low of just under 100 basis points. Draghi's government retains the confidence of investors yet lo spread has widened to 200 basis points (as the German 10-year bond topped 1% for the first time since 2015).[2] What malfunction occurred that widened the gap towards the 300 basis-point level that is seen by many as the tripwire for a crisis? None that was Draghi's fault. The culprit, like elsewhere in the world, is inflation. Eurozone inflation has climbed to its highest since the euro was created in 1999. Consumer prices surged 8.1% in the 12 months to May due to the ECB's promiscuous monetary policy, mammoth fiscal support during the pandemic, rising energy prices due to the switch to renewables, and supply blockages created by pandemic disruptions. The way Russia's war on Ukraine has boosted energy, commodity and food prices is likely to keep eurozone inflation elevated. The ECB has one objective; to maintain price instability, which is interpreted as keeping inflation below 2%. The central bank modelled on the inflation-hating Deutsche Bundesbank has little choice but to tighten monetary policy when inflation is nearly four times its target. Since 2016, the ECB's key rate has stood at 0%, while the overnight deposit rate has been negative since 2014 (and at a record minus 0.5% since 2019).[3] When the pandemic struck, the ECB added to various asset-buying programs[4] that gained heft when the bank first undertook quantitative easing in 2015. Over the past seven years, the central bank has purchased 3.9 trillion euros of eurozone assets, including 723 billion of Italian public debt, an amount equal to nearly 40% of Italy's GDP.[5] Given the record inflation, talk is mounting the ECB in July will raise rates for the first time since 2011, in what would be the first step towards boosting the key rate to a 'neutral' level of about 1.5% next year. The central bank is curtailing, and intends to end, its asset purchases.[6] Many central banks are raising key rates to tame inflation. For most countries, the main threat is the resultant slowing in economic growth boosts the jobless rate, perhaps to worrying levels if economies slump into recession. The ramifications of tighter monetary policy for the 19-member eurozone are wider and more concerning for three reasons. The first is the ECB is poised to stop acting as the buyer of last resort for its almost-bankrupt 'Club Med' members such as Italy, where gross government debt stood at 151% of GDP at the end of 2021.[7] No financier of government deficits (as some see it) for indebted sovereigns, especially Italy, will likely trigger a bond sell-off that puts the finances of debt-heavy governments on an unsustainable footing. Rising yields might restart the 'doom loop' that triggered the collapses of Greece, Ireland and Spain from 2010, whereby national bank bond holdings held as capital reserves plunge in value and the national government and commercial lenders become entwined in a downward spiral. The ECB would be exposed as lacking any credible way to quell such a government-bank suicide bind short of resuming the asset-buying that fuels the inflation it seeks to kill. The second way tighter ECB monetary policy is troubling is that the resultant economic downturn will remind indebted euro-users that they have no independent monetary policy to help their economies, nor a bespoke currency they can endlessly print to meet debt repayments, or devalue to export their way out of trouble. The only macro tool domestic policymakers possess is fiscal policy. The problem is many indebted governments are already running large fiscal deficits - Rome's shortfall over 2021 stood at 7.2% of GDP[8] and is forecast to be 6.0% in 2022[9] - and their debt loads mean these dearths can't be widened or prolonged. As talk mounts that indebted countries should quit the euro to reinstall the other macro tools, populist Italian politicians are bound to rekindle plans for a parallel currency as the least traumatic way for Italy to readopt the lira. The third means by which higher inflation is poisonous for the eurozone is that it creates a fissure between the area's creditor and debtor nations that would make it harder to find durable solutions for the euro. Inflation-phobic but inflation-ridden Germany and other creditors such as Finland and the Netherlands will squabble with France (government debt at 113% of GDP), Greece (193%), Italy, Portugal (127%) and Spain (118%) over how far the ECB should go to rein in inflation. The leaders of the creditor countries will be under domestic political pressure to ensure the ECB smothers inflation. They will battle with debtor leaders over how the ECB might support tottering governments and wobbly national banks sitting atop troubled economies. In line with this hawk-dove split, the Netherlands central bank chief Klaas Knot in July became the first ECB policy-board member to call for the bank to raise its key rate by 50 basis points to tackle inflation.[10] To maintain its inflation-fighting credentials, the ECB must raise interest rates enough to tame inflation, even if that stance crushes economic growth. The core concern of such tight monetary policy is that it will expose how the euro's flawed structure - that it is a currency union without the necessary political, fiscal or banking unions - has become explosive due to the large debts of southern eurozone governments. To be sure, policymakers are likely to once again thrash out some last-minute fudge that defers a denouement on the euro's fate. But temporary solutions are only, well, temporary and the euro needs a durable resolution. The indebted south could win the political tussle such that the ECB never makes a serious attempt to tame inflation. Due to generous pandemic support, creditor nations have higher government debt-to-GDP ratios - Germany's is 69%, the Netherland's 52%. They thus might tolerate faster inflation as it improves their debt ratios if their economies hold up. But that path might only delay tighter monetary policy and subsequent detonations. The war in Ukraine might undermine eurozone economic growth enough to quell inflation without the ECB doing much. The cost of servicing public debt, while rising, is still historically low, which reduces the likelihood of missed debt payments and a crisis. Eurozone governments are restarting efforts to create a proper banking union, which would mean common bank rules and eurozone, rather than national support for troubled banks.[11] But creditor nations don't want to be part of a mutual deposit insurance scheme if that means subsidising Italian banks holding Rome's debt. Nor do debtor governments want to join a banking union that could restrict their banks buying their bonds to support them. Lo spread is well short of the post-euro record 556 basis points it reached in 2011 during the first eurozone crisis that was triggered by the current-account imbalances among members.[12] But Rome's debt was only 120% of GDP then, and that gap narrowed only due to ECB support that is now waning because the problem today is inflation, not skewed trade and investment flows. Germany's economic slump and dislike of inflation will ensure Berlin pressures the ECB to prioritise inflation. Lo spread could widen enough to threaten a flawed currency union, especially if member countries are squabbling over solutions. While Draghi the central banker could bluff investors, Draghi the politician has no similar obvious masterstroke. Of note too is that Draghi's prime ministership will likely end when Italy holds a general election next year in Europe's spring that is likely to usher right-wing eurosceptics into power. To all the world's problem, be prepared to add elevated doubt about the euro's long-term future. The currency swap In 1948, Chris Howland was a 20-year British private who was the most popular radio DJ in northern Germany. On the night of June 17, two British military policemen appeared at the radio station in Hamburg where Howland worked. They made Howland sit up all night before allowing him at 6.30 am to open a sealed envelope and read the content on air. The news? The military government of Britain, France and the US from June 20 would introduce a new currency. Every German would receive 40 new Deutsche marks, which had been printed in the US and shipped in wooden crates stamped 'Doorknobs', in exchange for 60 Reichsmarks. Any other swastika-emblazoned Reichsmarks people held were made worthless come June 21.[13] A 'currency reform' of some sort was expected. But still. It's estimated that 95% of Reichsmarks were destroyed without replacement and savers were left with only 6.5% of their assets. The instantaneous currency switch and savings savaging were at the heart of measures under the Marshall Plan designed to revive Germany's economy at a time when millions of Germans were starving, inflation was rife, the currency untrusted and bartering prevalent. The steps, which in the absence of Russian knowledge sparked the Berlin Blockade,[14] worked. The economic revival in the French, UK and US zones that became West Germany was credited with helping Germany adopt a new constitution in 1949 known as the Basic Law. The currency changeover on top of the rampant post-war inflation and the hyperinflation of the early 1920s left a legacy. Germans adopted a mentality that the value of the Deutsche mark must be protected above all. This job was given to the Bundesbank when it was established in 1957 as the world's first and only central bank still to be granted independence under its country's constitution (whereas other central banks are granted 'independence' through acts of parliament or the goodwill of the executive).[15] Come 1993, Germany's Constitutional Court confirmed that under the Basic Law the Bundestag (parliament) only had the authority to ratify the Maastricht Treaty that created the euro if the European monetary union was in Germany's interest. The test? "The future European currency must be and remain as stable as the Deutsche mark," the court decreed.[16] Thus the ECB ended up with the same primary objective as the Bundesbank; namely, to maintain price stability. In Germany, the ECB's loose monetary setting and the inflation unleashed are seen as a betrayal. To the German public, tabloid media and even the German 'father of the euro' Otmar Issing, the ECB is modelled more on Italy's economic mismanagement pre-euro (when Rome's main policy response was to devalue the lira). Issing, the ECB's first chief economist, said the ECB has "lived in a fantasy" that downplayed the danger of inflation and thus the bank "has contributed massively to this trap in which it is now caught".[17] The ECB lax stance has wiped out returns on German savings, which is seen as income foregone to subsidise lazy southern Europeans.[18] High inflation stings Germans because few invest in equities or other 'growth' assets that might act as a hedge against inflation. Most German savings head to small regional savings and co-operative banks that offer low deposit rates. The German public is unlikely to feel more generous towards the indebted south if interruptions to energy and other imports from Russia send the German economy into recession.[19] But, as pessimism grows about global prospects, the economic outlook of inflation-tolerant and Russian-gas-dependent Italy is dimming too. Although Italy's economy is supported by consumer savings built up during lockdowns and 192 billion euros from the EU's 750-billion-euro Covid recovery fund, higher energy prices and other tremors from the Ukraine war could slow growth enough to send the country into recession.[20] Many fret about the trouble to be ignited when the ECB halts its asset buying, given how precarious are Rome's finances - the country has the largest budget deficit in the eurozone and the worst public debt ratio after Greece (193%).[21] In case of any crisis centred on Italy, policymakers have options such as loans from the EU rescue fund and linked ECB bond purchases of struggling members. But such aid would require approval from Germany's Bundestag and other creditor-nation parliaments. Another option is the one revealed when Draghi and French President Emmanuel Macron signed a joint letter last December that implicitly called for the transfer of all eurozone government debt since 2007 to a debt-management agency. But Germany and many other euro members would oppose such subterfuge.[22] It's probable that sometime soon the talents of Draghi the unelected politician and other policymakers will be tested. Lo spread will reveal what bond investors think. What's unlikely in any upcoming crisis, however, is any solution that cements the euro's future. By Michael Collins, Investment Specialist |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund [1] In 1993, Bank of Italy Governor Carlo Azeglio Ciampi was drafted as prime minister. At the height of the sovereign debt crisis in 2011, Mario Monti, who'd spent a decade at the European Commission, was appointed PM. In 2018, rival populist parties tapped Conte, a law professor at a university in Florence, to be PM. A list of Italian prime ministers can be found at: wikipedia.org/wiki/List_of_prime_ministers_of_Italy[2] The gravest scare for investors during Draghi's time as prime minister occurred in January this year when Italy's parliament failed to elect a new president in seven ballots held over a week and Draghi was touted as the next head of state (and seemed interested in the role). But that would have once again meant a snap general election that might have jetted right-wing populist parties into power. That outcome was avoided when MPs re-elected Mattarella even though the 80-year-old had rejected a second term. Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. A copy of the relevant PDS relating to a Magellan financial product or service may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to be implemented and its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |