News

29 Jun 2022 - Thinking about industrial (and Qantas and Netflix)

28 Jun 2022 - 4D podcast: explaining the country review process

|

4D podcast: explaining the country review process 4D Infrastructure June 2022 Bennelong's Dave Whitby speaks with Greg Goodsell, 4D's Global Equity Strategist, about 4D's unique country review process - an integral part of the business's investment process - and its impact on the portfolio.

For more detail on our country review process, you can read our Global Matters article: Why country risk matters |

|

Funds operated by this manager: 4D Global Infrastructure Fund, 4D Emerging Markets Infrastructure FundThe content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. |

28 Jun 2022 - EM Demographics - will ageing break a 40-year trend?

|

EM Demographics - will ageing break a 40-year trend? abrdn June 2022 Populations in many emerging markets (EMs) are set to age rapidly, with countries facing challenges should they 'get old' before they 'get rich'. Whether economies age gracefully will reflect a complex combination of growth trajectories, the real interest rate environment and policy choices. Demographics affect not just the outlook for economic growth - with population size (and hence labour force) a key building block of the economy - but they also have implications for savers and borrowers (households, firms and governments) via an influence on interest rates. Indeed, while growth is a major influence on the EM investment landscape (stronger economic and corporate earnings growth lift equities), interest rates on debt determine the price of a range of other assets too. Lower rates raise the value of firms' revenue generation and vice versa. It is therefore important to form a view on how demographics will affect both growth and interest rates. Emerging market demographics 'in focus' - implications for equilibrium real interest rates is the second of three research papers that seek to examine the nature and consequences of demographic change in major emerging markets. This second paper hones in on the impact that demographic trends may have on real equilibrium interest rates - a crucial, but unobservable, economic variable. Government bond yields - falling since the 1980sTaking a step back from the current market volatility and concerns about high inflation, government bond yields in developed and emerging markets have been in long-term decline since the 1980s. Sliding developed market and EM yields over this period partly reflect success in bringing down inflation, but they also reflect falling real — inflation adjusted - yields. A large body of academic literature points to an underlying downward trend in equilibrium real interest rates (r*, pronounced 'r star') as the reason. Many papers have concluded that secular trends - including demographics - explain much of the fall in real yields, with the global financial system potentially creating a global phenomenon as markets link savings and investment across borders. This raises a crucial question for investors: if demographic trends are turning, will interest rates be pushed higher? R* as theoryThe equilibrium interest rate is a hard-to-measure theoretical concept. It's closely related to economic growth and is also the interest rate that balances an economy's supply of savings with the demand for investment. Some commentators have concluded that demographics will push up r* as shrinking pools of labour reduce the supply of savings. However, demographics operate via two channels which can work in opposite directions: fewer workers may reduce the number of savers, but they also push down on potential economic growth and therefore investment. R* gazingOur research suggests that over the next five years, demographic composition will typically push up on r* - primarily due to rising dependency ratios as the number of non-workers outpaces workers. But shrinking labour forces are almost always exerting greater downwards pressure. Moreover, other factors influencing potential growth are likely to push equilibrium interest rates in different directions across EMs. On a net basis, roughly half of major EMs may see equilibrium rates pushed down by these forces, while half may see them rise. Over a longer time horizon - say 30 years - the impact of shifting demographic composition potentially creates more meaningful upwards pressure. But even then the outlook varies. For example, China faces a well-known demographic challenge as the result of its now scrapped 'One Child' policy. But even here, falling long-term growth will likely offset the impact on the balance of savings and investments from an ageing society. Demographics aren't destiny for growth, interest ratesDemographics are just one (albeit very important) influence on interest rates over the longer term. The Covid-19-shock, income inequality and technological change are all important drivers too, along with policy choices. Demographics are just one (albeit very important) influence on interest rates over the longer term Indeed, the fracturing of EM-developed market real yields - which had moved in near lockstep until 2013 - implies that domestic policy choices may have become increasingly important. Ageing by itself won't drive interest rates higher, compounding the Covid-19 shock. While demographic trends are becoming more adverse as populations age, the impact on real equilibrium rates continues to be offset in many countries by downwards pressure from slower growth in working-age populations. Additionally, the balance of risks from economic scarring, inequality and technology gives further weight to our research which suggests that few economies will suffer major upwards pressure on r*. Author: Robert Gilhooly, Senior Emerging Markets Research Economist |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund , Aberdeen Standard Life Absolute Return Global Bond Strategies Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund |

27 Jun 2022 - Managers Insights | Collins St Asset Management

|

|

||

|

Damen Purcell, COO of Australian Fund Monitors, speaks with Rob Hay, Head of Distribution & Investor Relations at Collins St Asset Management. The Collins St Value Fund has a track record of 6 years and 4 months and has outperformed the ASX 200 Total Return Index since inception in February 2016, providing investors with an annualised return of 17.87% compared with the index's return of 10.3% over the same period.

|

27 Jun 2022 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

|||||||||||||||||

| DigitalX Fund | |||||||||||||||||

|

|||||||||||||||||

|

DigitalX Bitcoin Fund |

|||||||||||||||||

|

|||||||||||||||||

|

Balmoral Digital Assets Fund |

|||||||||||||||||

|

|||||||||||||||||

|

|

|||||||||||||||||

| PURE Resources Fund | |||||||||||||||||

|

|||||||||||||||||

| View Profile | |||||||||||||||||

|

Want to see more funds? |

|||||||||||||||||

|

Subscribe for full access to these funds and over 650 others |

27 Jun 2022 - 10k Words

|

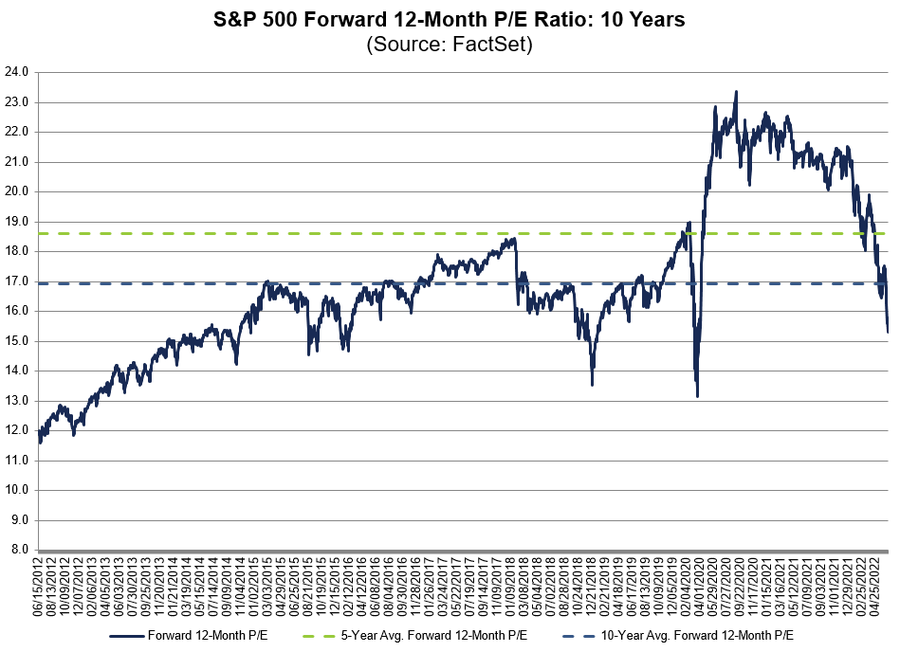

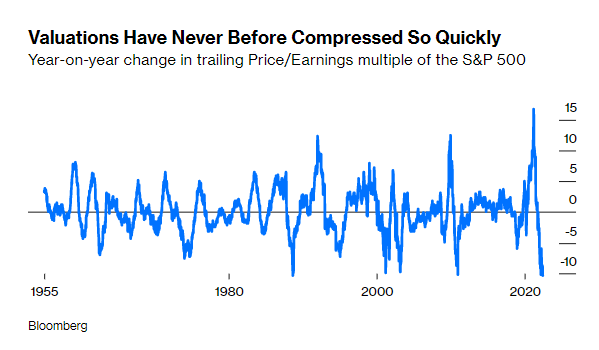

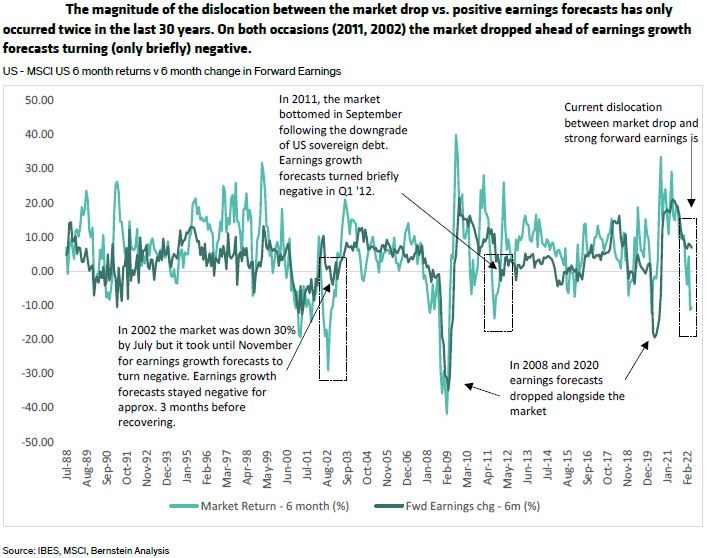

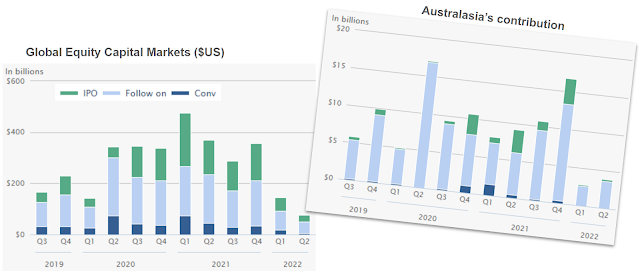

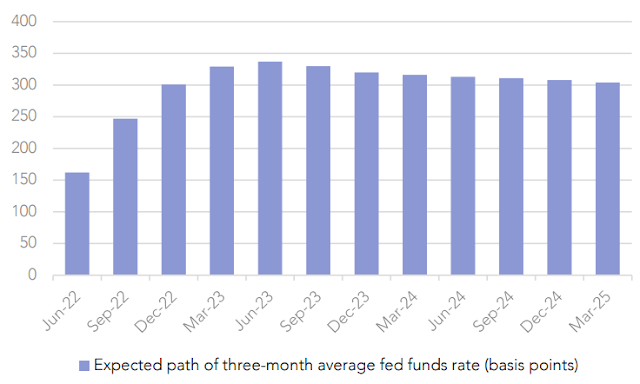

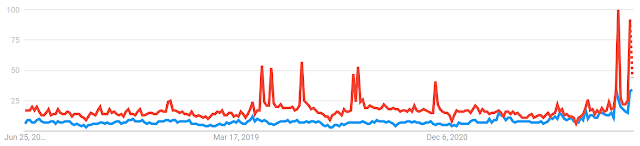

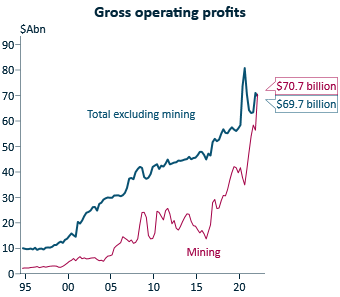

10k Words Equitable Investors June 2022 Price-to-Earnings multiples have been crunched in the calendar year to-date, as FactSet and strategist Christophe Barraud chart - but that begs the question posed by Sanford Bernstein - does this imply earnings expectations will be cut? Global equity capital markets volumes have dropped more than market indices, Equitable Investors highlights, while there are plenty of companies in need of fresh cash. Below-trend economic growth and above-trend inflation is the widely held consensus view of the economic backdrop from the Bank of America global fund manager survey. Off the back of that, the market is expecting the Fed cash rate to settle at ~3%, Wilsons calculates. Back in Australia, ANZ-Roy Morgan Consumer Confidence is strikingly low amid all the talk of inflation and interest rates - search terms that have surged on Google Trends. IFM highlights that Australian mining profits have for the first time exceeded profits in all other non-finance sectors combined.

S&P 500 Forward PE over 10 years Source: FactSet

S&P 500 trailing PE since 1955 Source: Bloomberg, @C_Barraud

Are earnings forecasts about to be downgraded?

Global Equity Capital Markets ($US)

No, ASX-listed cash burners with 12m or less cash at last reported burn-rate

Source: Equitable Investors

"Stagflation" is the most popular economic backdrop expectation

Source: BofA Global Fund Manager Survey (June 2022)

Expected path of Federal Reserve cash rate Source: Refinitiv, Wilsons

ANZ-Roy Morgan Consumer Confidence

Australian web searches for "inflation" (blue line) and "interest rates" (red line) Source: Google Trends, Equitable Investors

Australian Gross Operating Profits Source: ABS, IFM June Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Nothing in this blog constitutes investment advice - or advice in any other field. Neither the information, commentary or any opinion contained in this blog constitutes a solicitation or offer by Equitable Investors Pty Ltd (Equitable Investors) or its affiliates to buy or sell any securities or other financial instruments. Nor shall any such security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. The content of this blog should not be relied upon in making investment decisions.Any decisions based on information contained on this blog are the sole responsibility of the visitor. In exchange for using this blog, the visitor agree to indemnify Equitable Investors and hold Equitable Investors, its officers, directors, employees, affiliates, agents, licensors and suppliers harmless against any and all claims, losses, liability, costs and expenses (including but not limited to legal fees) arising from your use of this blog, from your violation of these Terms or from any decisions that the visitor makes based on such information. This blog is for information purposes only and is not intended to be relied upon as a forecast, research or investment advice. The information on this blog does not constitute a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Although this material is based upon information that Equitable Investors considers reliable and endeavours to keep current, Equitable Investors does not assure that this material is accurate, current or complete, and it should not be relied upon as such. Any opinions expressed on this blog may change as subsequent conditions vary. Equitable Investors does not warrant, either expressly or implied, the accuracy or completeness of the information, text, graphics, links or other items contained on this blog and does not warrant that the functions contained in this blog will be uninterrupted or error-free, that defects will be corrected, or that the blog will be free of viruses or other harmful components.Equitable Investors expressly disclaims all liability for errors and omissions in the materials on this blog and for the use or interpretation by others of information contained on the blog |

Source: Sanford Bernstein

Source: Sanford Bernstein

27 Jun 2022 - Consolidation and rising tail risks

24 Jun 2022 - RBA ignores weaker real economy and hikes

|

RBA ignores weaker real economy and hikes Yarra Capital Management 08 June 2022 A 50 basis point hike by the Reserve Bank of Australia (RBA) was clearly a surprise for financial markets. The RBA's rationale for increasing interest rates was that inflation is higher than expected. This is despite the fact that the CPI data was printed ahead of the May decision (i.e. the inflation surprise is not "new" news) and despite the RBA's acknowledgement that the prime reason for high inflation is due to supply shortages rather than excess demand. The RBA nevertheless decided to go against its own guidance that 25bps hikes could be expected going forward as part of their self-selected 'business as usual' strategy, instead delivering a 50bp hike. Indeed, the economic data since the May decision can be best described as limited and the tone of the data clearly missed to the downside, rather than exceeded expectations. Business confidence eased, consumer confidence was sharply lower, the wage price index missed expectations to the downside, employment was 25k weaker than expected, building approvals was 4.4% weaker than expected and home loans written were 6% below expectations. Only the GDP data slightly beat expectations (0.8%qoq v 0.7% expected). The only other data that the RBA likely could have looked at was the monthly Inflation Gauge data that did come in relatively strong at the start of the week. Again, however, the reason for the strength was supply side issues in petrol, energy, food and rent. It is also relevant to note that the accuracy of this survey can be questionable. The RBA's inability to read the (financial market) room was again on full display. While only slightly more surveyed economists expected 25bps than a larger move, only 3 of the 29 surveyed expected a 50bp hike. The ASX200 fell 0.6% and 3-year bond yields spiked 12bps as a consequence of yet again opaque and arguably misleading communication. Arguably, this is clearly an attempt of catch-up by a central bank that has been caught out by failing to detect the inflation threat early enough and now, in an effort to make greater inroads into the negative real cash rate settings, has chosen to surprise financial markets. There is likely an element of using the cover of larger hikes from the US, BoC and RBNZ to hike by a greater increment in June. However, in choosing this action the RBA has opened the door to implementing further 50bp hikes in coming months. It is indeed possible that inflation prints high in Q2, and the RBA mechanically follows with a 50bp hike in August. For households and firms this inconsistency in terms of communication, data flow and action likely adds a layer of confusion into financial markets at a time when forward looking and consistent guidance is needed. The RBA has indicated that it sees further hikes necessary stating it "expect[s] to take further steps in the process of normalising monetary conditions in Australia over the months ahead". However, if "the size and timing of future interest rate increases will be guided by the incoming data and the Board's assessment of the outlook for inflation and the labour market" then it would be useful if they were consistent in that interpretation of that data and their decision on the cash rate. From our perspective it was a coin toss between a 25bp or 40bp hike. However, rates markets are now left with little choice but to embed hikes in excess of 25bps per meeting for the next few months while the RBA moves to set local rates sharply higher in an effort to contain global supply led inflation pressures. In the rush to catch up to other central banks, however, we need to be conscious that the monetary transmission mechanism works very differently in Australia. The tightening in financial conditions in the US has been a function of all key forces moving in the same direction (wider corporate bond spreads, higher bond yields, higher USD, weaker US equities and Fed hikes). In Australia, however, movements in the RBA cash rate and the A$ have much greater impacts. Australia's financial conditions have now tightened materially post the RBA's decision (refer chart). Should the RBA hike rates by a further 100bps over the coming months, Australia's financial conditions will likely move closer to the current level in the US. However, given Australia is currently already a high carry currency, the risk is now firmly skewed to a materially higher A$ in coming months. The impact of this would likely be to further tighten Australian financial conditions and act as a material headwind for the interest rate sectors of housing and consumer discretionary. |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

23 Jun 2022 - Winning the war on talent

|

Winning the war on talent Claremont Global May 2022 As global fund managers, one of the most important areas of focus for many of the companies we research is around talent acquisition and retention. This issue goes beyond not just ensuring the brightest minds remain on the books but also extends towards becoming an employer of choice in an increasingly competitive market. This is made all the more difficult due to the growing expectations laid down or justly expected by a labour pool that is, as we stand today, heavily in demand. As a result, it is becoming more and more intrinsic to a company's position within their respected industry to ensure their organisation is, in fact, an attractive proposition for any prospective candidate. A winning talent management strategy therefore should be viewed as a robust advantage, that may prove to be just as critical to the company's long-term success as the competitive moat around the business itself. Employee retention - an 'old school' metric or one to cast a sharp eye over?One metric that can get often overlooked is that of the retention rates of company staff. Whether it relates to a technology business, a retailer, or a consulting firm, the cost of replacing any given employee is greatly underappreciated. According to estimates out of the Work Institute's 2017 Report, the replacement cost for an employer averages roughly 33% of an employee's annual salary for their exit. A company we believe is industry standard when it comes to placing a stringent focus on retaining its talent and expertise is the paintings and coatings business, Sherwin-Williams (SHW-US), which operate close to 5,000 stores around the US. While providing competitive compensation and benefits for its staff, the company prides itself on the discipline of its execution and is known to train staff "like the military". Store managers usually start as graduates but are often treated as business owners. This may sound like a talent strategy from a bygone era, however, this tried-and-tested method from a 155-year-old company creates an exceptionally low staff turnover of 7-8%, or 5-6% for store managers and sales reps. We begin to appreciate how impressive this number is when measured against the US Bureau of Labour Statistics' annual turnover figures across both retail and wholesale channels. Annual US employee turnover by sales channel

Source: US Bureau of Labour Statistics This incredibly low churn creates real loyalty from the company's professional customers, who take comfort in the fact that the staff member they are dealing with on a daily basis is, in fact, an expert in what they sell. "The managers of the big brands have a very clear responsibility. It's attracting and keeping talented people in order to sustain and build the trustworthiness of that brand. There is no clearer objective in the economy. Your economic success depends on expanding and building your economies of trustworthiness." - Robert Reich The company also pushes the notion of upward mobility (everyone knows the CEO started in the stores), providing a tangible path to move into management positions, and areas of increased responsibility, if they remain at the business over the long term. The growing importance of scaleThe aptly termed "war on talent" could not currently be any more evident than in the technology and digital industries. The sheer pace at which the world has evolved in partnership with an accelerated digital transition through the pandemic has pushed demand for top-quality personnel to an extreme level. One of the key dynamics we have noticed is the unmatched strength at which the large technology firms are able to exert when looking to attract talent out of a thinning top-end labour market. These larger technology players are able to offer potential candidates extremely competitive pay and benefits packages, heavy investment in training and strong career progression opportunities ― in addition to offering a meaningful company mission and purpose that may strike a chord with those looking to make a tangible difference in how we live our everyday lives. As we can see in the chart below, many of Sherwin-Williams' competing players are struggling to compete for top-end talent due to the likes of the "hyper-scalers" sucking up this talent at unprecedented rates. The company's older and arguably less-savvy competitors are suffering "brain drain" if desired work experiences, compensation and benefits, or career progression opportunities are not fulfilled. US software engineer and software developer hires

Source: BainAura talent platform, Bain For context, while many companies were furloughing staff amid the pandemic's economic fallout, Microsoft (MSFT-US) saw its employee base rise 18,000 or 11%, with Alphabet's (GOOGLE-US) base also rising net 16,000 employees or 13%. This has developed into a seriously large competitive advantage for the large technology firms and, as current shareholders of both companies, provides us with comfort that they will be able to continually drive innovation and product development with the pools of talent they have in their corner. "What's most impressive is that your team (Google) has built the world's first self-replicating talent machine. You've created a system that not only hires remarkable people, but also scales with the company and gets better with every generation." - Paul Otellini, Former President and CEO, Intel An alternative strategyThis system of managing and curating talent extends beyond simply retaining existing personnel and hiring new staff. The strategy of careful, diligent M&A to bring in experts that not only have the skills to drive sustained innovation and product development but actually want to work for the broader organisation, is one that cannot be overlooked. We see this dynamic present itself in areas such as medical and analytical instruments, where it can be more efficient to bring in a team of scientists or technicians through bolt-on acquisitions into the umbrella organisation, rather than invest in years of internal R&D and training in order to develop specific products or technologies. We have been most impressed by this method of talent management through another one of our portfolio holdings, Agilent Technologies (A-US). Their large team of highly skilled field scientists is one of the most underappreciated assets of their business and the retention of this talent is critically important to the sustainability of their business model. This was shown over the course of the pandemic when they did not move to reduce staff, nor did they cut base pay or hours, as a response to the temporary disruptions across the business. According to Agilent's CEO Mike McMullen, this has led to attrition rates that sit at much lower levels than peers in the market. However, a key piece in the evolution of their team of scientists is the onboarding of R&D teams through focused acquisitions of appropriate target companies, subsequently integrating them into the larger Agilent ecosystem. This can be witnessed through one of their most recent acquisitions in BioTek, a leading cell analysis business, of which then-owners, the Alpert family, sought to sell their company to Agilent as they appreciated the prevailing culture and long-term synergies across their respective R&D teams. "The cultural alignment, the consistency and commitment to the same sort of core values really do matter." - Mike McMullen, Agilent CEO, Goldman Sachs Healthcare Conference, Jan-21 Agilent's stringent focus on an engineering-led culture allows them to present themselves as an attractive suitor to smaller, niche businesses with bands of top-end scientists and experts in their fields that do not necessarily want to be swept into a corporate behemoth. This enables them to not only bolster the talent pool across the organisation but retain them over the long term, which will, in turn, materialise into tangible value creation for shareholders through sustained innovation and product development. Intrinsic to longevityTalent management can no longer be dismissed as simply an HR problem. It is becoming so critical in today's world that if a company mismanages its workforce, a loss of competitive advantage and profitability will present itself as the most likely outcome. The subsequent costs of recruiting, training, loss of expertise, potentially fractured relationships with customers, wage inflation, and cultural tearing all need to be placed in heavy consideration when curating a talent management strategy. We ensure that the businesses we invest in and research at Claremont Global have sound strategies in place to manage their pool of talent, ensuring that they not only retain the best people but also attract top-flight talent in the market to drive sustained innovation and product development well into the future. Authors and consultants, Rob Silzer & Ben Dowell, capture this phenomenon perfectly: "Talent management is more than just a competitive advantage; it is a fundamental requirement for business success." - Silzer & Dowell, Strategy-Driven Talent Management: A Leadership Imperative. Author: Luke Davrain, CFA, Investment Analyst Funds operated by this manager: |

22 Jun 2022 - It's time to hedge - the bear is here

|

It's time to hedge - the bear is here Watermark Funds Management June 2022 REVIEW The Australian share market saw a significant contraction in May with the All-Ordinaries Index down 3.0%, its worst month since January. The sell-off was once again led by Technology stocks with the sector down 8.7%. The Real Estate sector also performed poorly, down 8.9%, led by concerns of more aggressive interest rate tightening and associated impacts on demand. After a soft April, the Materials sector resumed its outperformance in May, aided by expectations of more stimulus in China. In terms of factor leadership, value resumed its leadership over growth. The value factor has now outperformed growth by 20% over the last 6 months. MARKET OUTLOOK The secular bull market that ended for Australian shares last August emerged from the financial crisis and was a product of successive waves of liquidity led asset reflation, as central banks pushed real interest rates lower and lower and asset values higher and higher (Fig1). Figure 1: Successive waves of asset inflation

Source: Bloomberg, S&P 500 Chart Asset inflation, of course, created excess demand, leaving product and labour markets acutely tight. Unemployment in Australia is now at its lowest in 40 years and with little immigration, the services sector is scrambling to find workers. Fair Work Commission awarded a 5.2% increase in the minimum wage, well above expectations. This policy led bonanza for asset owners was a consequence of systemic deflation. No one has a complete explanation for the root cause of this deflation which you can see clearly in the value of bonds which have pushed higher for decades (long term interest rates have been falling). The first phase took place in the 1980's with back-to-back global recessions that killed the inflation of that era. Then in the early 1990's with the collapse of the Soviet Union we had a rapid expansion of western democracies, a deepening of capital markets and the globalisation of trade. This spread of the neo-liberal 'rules based' order (capitalism) was deflationary allowing interest rates to fall and debt balances to accumulate. The spoils of this period where not spread evenly however, laying the seeds of its demise. Asset owners captured all the gains while labour's share of GDP has fallen sharply. We now have the first generation of citizens in the west who are worse off than their parents in real terms. The emergence of popularism and de-globalisation were the first phase of its descent. A new cold war between the East and West has manifested the next phase. With this reversal in these deflationary forces, the good times of ample liquidity and asset reflation have passed. Even before the health crisis, we were approaching the limits of these policies in driving asset values higher as bond yields in many western countries were already negative. On a hold to maturity basis, investors were guaranteed a loss, which of course is nonsensical. Then with the health crisis, policy makers doubled down on these same policies. The excess demand created from emergency stimulus and the associated supply chain disruptions have unleashed inflation which will be with us for years to come. Investors need to ask two important questions: Are the deflationary forces that persisted for so long still around or has their demise contributed to the inflation we are seeing today? Secondly, what has caused this inflation, is it established or transitory? How these inflationary pressures play out will determine the duration of this bear market. If the inflation hangs around for years to come as expected then we are in a secular bear, if it is transitory and the deflationary forces resume/return then potentially shares can make new highs in the years ahead. We are still early in this bear market. Until inflation moderates and central banks back away from hiking rates further, shares will move lower in the medium term. In the short term at least, share markets globally are oversold and sentiment is extremely bearish. In the weeks and potentially months ahead, we should see a decent bear market rally which investors should sell into as the big drawdown is still ahead in the second half of the year. Australian shares have proven remarkably resilient through this first phase of the drawdown given our economy's exposure to commodities which are the driving force behind the inflation we are seeing. In simple terms, the Australian economy is a good inflation hedge. The 'quarry and farm' may once again avoid another global recession. As we get into the 3rd quarter of the year however, around the US mid-term elections, western economies will be slowing quickly and the 'street' will be slashing profit estimates, pushing shares lower. This becomes a pivotal moment for investors as the policy response will determine the next move for shares. If the inflation data improves as everyone expects, Central Banks may 'pause' on any further policy tightening. Under this scenario economies slow but avoid recession and shares can stage a significant rally early into next year. However, an early pause only ensures inflation lingers for longer, leaving us with 'stagflation'. Alternately, Central Banks look to overshoot in tightening financial conditions further to kill inflation, only to push western economies into recession. Under this scenario shares obviously fall further into the first half of next year. The policy response as the economy slows, asset values fall, and inflation moderates will determine which path the market follows. Either way the medium-term outcome is much the same, shares will be lower. The emerging data is less than encouraging, with the May CPI report showing further deterioration, Central Banks are once again losing credibility as they were guiding to a moderation in the data. It seems they still have a lot more to do evident in the FOMC decision to increase the target interest rate by a full 75bpts (3 hikes in 1), which is unprecedented. With the broader offshore indexes down more than 20% we are now officially in a bear market for shares with investors seemingly still pricing in a soft-landing scenario (green line below in Fig 2). They have never tightened once shares have fallen into a bear market before (down >20%), a further demonstration of just how far behind the curve they find themselves. Given inflation has never been tamed once it gets above 5% without a recession, a recession more than likely beckons and we move lower (the red line in Fig 2). Figure 2: Market drawdowns with and without recessions

Source: Stifel While we have seen some contraction in valuations (P/E's) already as financial conditions have tightened, we are yet to see any move lower in profit expectations. With the demand shock from the COVID stimulus, many public companies are over earning, profits have moved well above trend. In a garden variety recession earnings typically fall by a least one third Fig 3 below. Figure 3: S&P 500 Profit (EPS) drawdowns from prior peaks

Source: Stifel If we are in a stagflation environment of lower growth and persistent inflation, then valuations may well move to the lower end of the historic range (P/E's are low during periods of inflation) which along with lower earnings leaves us with a share market that still has a long way to fall. SECTORS IN REVIEW The Consumer sector delivered a flat result for the month, with gains in supermarket shorts, offsetting losses in some consumer growth stocks. Our long position in the Fuel Marketers has been gaining momentum as fuel security becomes an increasing issue for Western Governments. Ampol (ALD) and Viva Energy (VEA) refining assets, historically loathed by the market, are now generating super returns and driving upgrades for both companies. This sector is under-owned and offers defensive exposure at a cheap multiple. As mentioned in the April monthly, the Agriculture sector is building as fertile ground for short ideas. Share prices have risen aggressively given the confluence of a strong domestic grain harvest, and sky-high soft commodity prices driven by supply-chain dislocation. We know however, as with all highly cyclical industries, that conditions are ever changing, and we should be careful extrapolating at either the top or the bottom of the cycle. Using a 'normal season' as the basis for valuation, earnings multiples look extreme. We see several catalysts, including the successful negotiation of a humanitarian export corridor in the Black Sea to correct over-inflated soft commodity prices. Financials had a flat month in terms of attribution. Our shorts in the Banks delivered returns, as we saw the beginning of a major sell off across the sector. Banks had held up well for most of the broader market volatility of 2022. This changed when investors came to appreciate the consequences of faster than expected rate rises. We have been highlighting for some time the nexus between bank returns and the property market. Offsetting these profits was weakness in our long position Macquarie Group (MQG), we continue to see good earnings prospects for Macquarie in the short term amidst the energy market volatility. Commodities trading remains a key driver of results. Technology delivered some modest positive returns. Largely from our short portfolio. The sector continues to be the most sensitive to higher than expected inflation outcomes. Which are then leading to higher interest rates expectation. Selling across the sector has been indiscriminate. The Building Material companies continue to come under considerable pressure as it has become clearer that interest rates will be moving a lot higher. This is the case not just for the local Builders but the US based ones as well James Hardie (JHX) and Reliance Worldwide Corporation (RWC). As manufacturing businesses these companies are also very exposed to escalating fuel and energy costs. In Media, cyclical business like Nine Entertainment (NEC) and Seven West Media (SWM) have come under considerable pressure on fears of a fall in advertising spending. NEC shares are starting to look attractive with a full recession now factored in. Contractors: We expect the resources sector to hold together relatively well even as growth slows elsewhere. Monadelphous (MND) an important contractor in energy and iron ore operating in WA should perform well in the years ahead, especially as energy investments picks up. The iron ore hubs are so large and established now, having doubled in size over the last 15 years, spending in this sector will remain elevated for years to come. As a defensive sector, Healthcare has held up relatively well in a difficult market, it's probably time to take profits here. Resources: The lithium sector has fallen hard following some negative research pieces suggesting the market is over supplied in the medium term as Chinese production ramps up. We have a balanced portfolio of attractively prices emerging producers/explores and a short portfolio of expensive explorers in preproduction. Producers of bulk commodities have held up very well in recent weeks, it's time to take profits in some of the iron ore miners in particular. The iron ore prices is still above $150/t and looks vulnerable here. Funds operated by this manager: Watermark Absolute Return Fund, Watermark Australian Leaders Fund, Watermark Market Neutral Fund Ltd (LIC) |