News

18 Jul 2022 - Compelling Opportunity for Investors: Improving Convexity, Yet Benign Default Risk

|

Compelling Opportunity for Investors: Improving Convexity, Yet Benign Default Risk (Adviser & Wholesale Investors Only) Ares Australia Management 28 June 2022 What is Convexity & Why Is It Important? When credit instruments sell off, market participants will often talk about convexity being back. So, what is it?

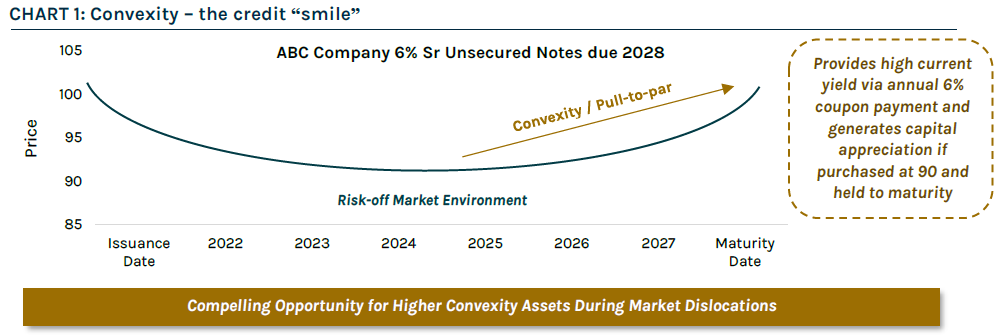

During a risk-off environment, the price of a credit instrument typically drops below its nominal value (also referred to as "face" or "par" value) due to perceived increased default risk. As illustrated by the example in Chart 1 below, there is a compelling investment opportunity when a bond trades at a discount to its nominal value - assuming the bond does not default, a bond's price will benefit from a natural "pull" to the nominal value as it approaches maturity. This movement is referred to as "pull-to-par". Typically, bonds and loans that trade at a discount have positive convexity, offering investors enhanced yield and capital appreciation potential without taking excess risk.

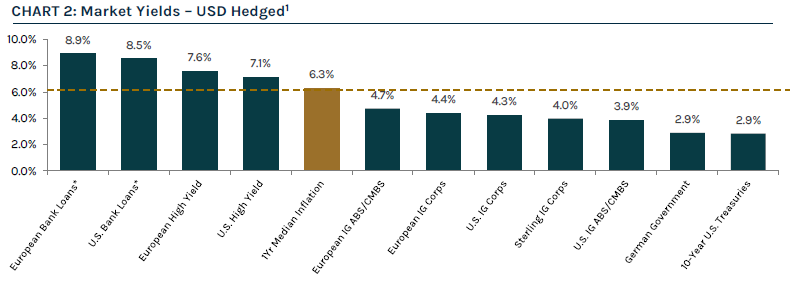

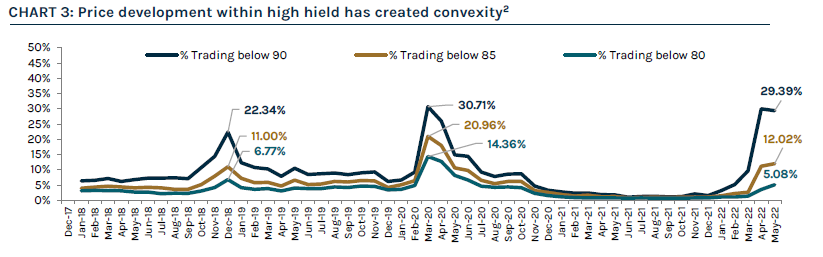

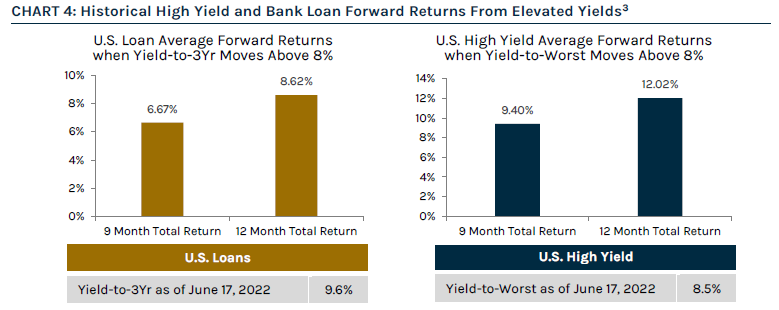

Market Opportunity - Convexity & Higher Yields Calendar year 2022 has presented significant turmoil for global financial markets amid a risk-off environment and sustained macro uncertainty. Global inflationary pressures continue to persist, including the ongoing war in Ukraine, slowing growth, higher energy prices and supply-chain disruptions. Central banks face substantial challenges as they look to combat elevated inflation with interest rate hikes, but without triggering a recession. Against the backdrop of wider spreads and the sell-off in rates over the past few months, fixed income yields have reset to higher levels, presenting an attractive opportunity for yield-focused investors. Global leveraged credit assets are providing a meaningful pickup in real yields when compared to traditional fixed income markets, as illustrated in Chart 2. Higher yields and a decline in asset prices have introduced greater upside convexity in leveraged credit This combination of higher yields and cheaper prices in an environment where bouts of volatility have become shorter and more frequent, is presenting alpha generating opportunities for active managers. History suggests investing in periods of dislocation, when yields reach current levels, provides attractive forward returns in the high yield bond and bank loan markets.

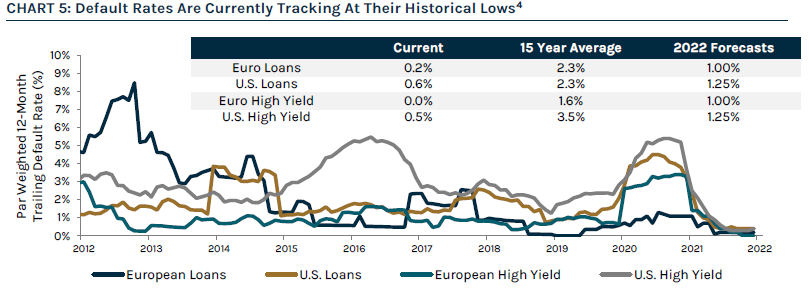

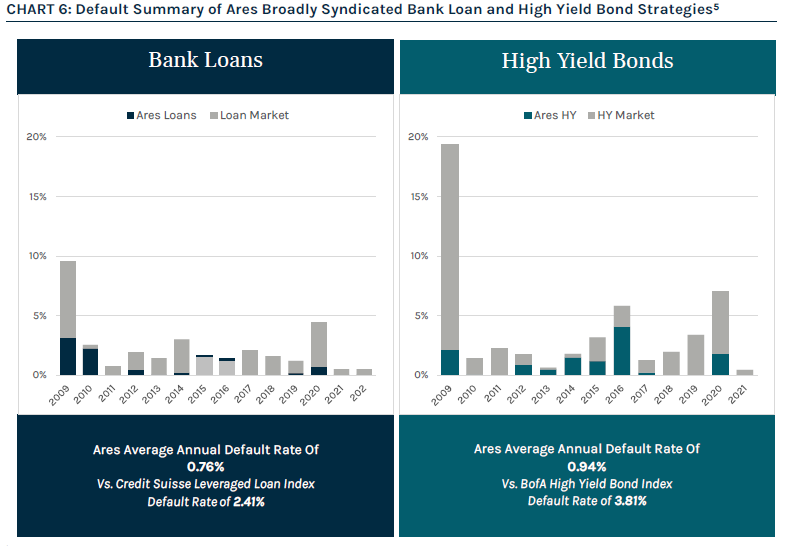

Market Outlook Looking forward, we expect volatility to persist with the potential for asset coverage leakage and an uneven recovery across markets. We believe credit spreads are currently at levels that represent attractive entry points, but tail risks have increased, and we anticipate elevated credit dispersion as well as rising idiosyncratic credit events driven by a host of conflicting themes. We believe Ares is well positioned to provide superior credit selection and vigilant risk management in today's volatile market due to our disciplined investment process that focuses on capital preservation, predicated on bottom-up fundamental research with the goal of minimizing default risk by identifying and avoiding marginal quality credit. This core tenet of Ares' investment philosophy has resulted in significantly lower defaults in its bank loan and high yield bond strategies, particularly in periods of dislocation. In summary, as investors are faced with rising rates and elevated inflation, many may struggle to determine how best to position their credit exposure in an effort to maximize yield and mitigate risk. At Ares, our differentiated approach to capitalizing on the best risk-adjusted return opportunities across the investable universe is rooted in the scale and integration of our Global Liquid and Alternative Credit strategies, which allows us to fully leverage extensive research and origination capabilities, proprietary technologies and longstanding relationships. Written By Teiki Benveniste, Head of Ares Australia Management |

|

Funds operated by this manager: Ares Diversified Credit Fund, Ares Global Credit Income Fund |

15 Jul 2022 - Mind the gap - Hedging tails to provide liquidity in times of stress

|

Mind the gap - Hedging tails to provide liquidity in times of stress (Adviser & wholesale investors only) CIP Asset Management July 2022 Including tail hedging in a portfolio can have the following benefits:

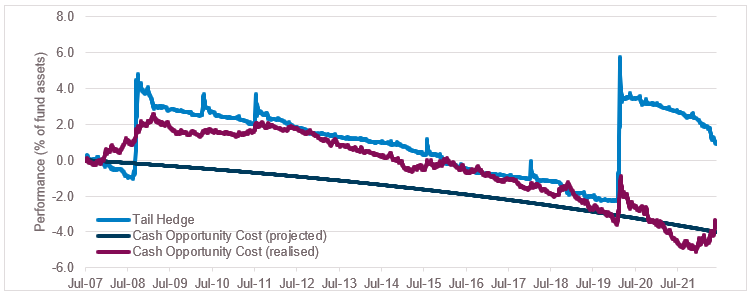

Point 3 may be of particular interest to Australian super funds where, for example, FX hedges can incur large mark-to-market losses during times of market stress. For example, the latest Quarterly Superannuation Statistics published by APRA (March 2022) show the industry currently has $322bn of FX hedges. During the financial crisis AUD dropped 37.6%, which would have led to FX hedge losses of -$121bn based on current exposures at a time the overall portfolio was down -26% (-$577bn in today's terms), and a COVID scenario would result in FX losses of around -$58bn at a time overall assets were down -$466bn. Investors use a variety of approaches to try and mitigate losses in their portfolios, including diversification, market timing, and explicit hedging. While we agree all three approaches have a place in managing portfolios, hedging is by far the most reliable way to mitigate losses during times of market stress. It (almost) goes without saying that even investors who successfully add long-term alpha for their clients via market timing cannot always predict market drawdowns, and one only needs to look at recent market moves to see the pitfalls of relying too heavily on diversification (eg simultaneous sell-off in equities and fixed income with ACWI -18.9% and Global Agg -14.5% YTD on a total return basis). Because it is reliable, hedging can be an important tool in building resilient long-term portfolios. However, that reliability comes at a cost, and because true market stress events are few and far between, we often find that the costs of hedging are more visible to investors than the benefits. Since most investors are not particularly concerned by small drawdowns, the cost of hedging can be reduced by focusing only on larger, less-frequent drawdowns. Specifically, tail hedging allows investors to hedge against only the most extreme outcomes that can inflict long-lasting damage on even the most diversified portfolios. It's worth reiterating that because tail hedging, by design, is only expected to 'work' in the most extreme circumstances, investors can expect to see (modest) losses in tail hedges far more frequently than they will see gains. However, it is the timing and magnitude of the gains that is important. A robust tail hedging program will provide investors with large gains when other parts of the portfolio are experiencing very large drawdowns. And that knowledge may also allow investors to adopt a barbell approach and take higher risk, and earn higher returns, elsewhere in the portfolio. One final point: to be reliable, a tail hedge needs to be "always on" since the whole point of hedging is that we can't always predict a drawdown. In this regard, systematic option strategies can be particularly useful. In addition to the FX exposures outlined previously, an additional liquidity drain may come in the form of capital calls on private equity commitments. The super industry currently has approximately $106bn exposure to private equity. Some basic assumptions (1) lead to a rough estimate of $11bn liquidity required in a crisis year. Further liquidity needs might reasonably be expected to arise from such things as capital raising (eg rights issues) from portfolio companies, investment opportunities in real estate, infrastructure etc arising from market and/or funding stress. The main point is that super funds can expect to have high liquidity obligations that are required (or desired) to be met during times of market turmoil, on our calculations as much as 6% of fund assets, and possibly much more. A super fund could budget for this by setting aside some amount to be held in low risk, highly liquid instruments such as cash, ready to be deployed in times of stress. However, such an approach has an opportunity cost because the return on cash is much lower than the return on the rest of the portfolio. Using the past 15y years as a rough guide, a cash investment would have returned 2.6%p.a. vs approximately 5%p.a. for a typical balanced super portfolio. The last 10y would have been an even larger difference (1.5% vs 8%). The chart below shows the performance of a systematic tail hedge strategy(2) (light blue line) compared to the realised opportunity cost of holding an additional 6% of fund assets in cash (purple line) and the projected constant opportunity cost of holding cash (dark blue line).

Figure 1: Tail hedge strategy vs opportunity cost of holding cash. The chart shows the long-term performance impact of running a tail hedge strategy can be substantially less than holding additional cash in the portfolio. The mark-to-market of the tail hedging program would need to be met over time, but the chart shows that the realised negative performance during "normal" periods is no more than the drag on performance from holding excess cash, and during stress periods the tail hedging realises large gains which can be used to meet any liquidity requirements. For the specific objective of providing liquidity during a crisis, we find an effective tail hedging program to be a more efficient approach despite the perceived "cost" of hedging. 1 10y fund life, 5y investment phase with capital called evenly, investment realisations of zero in a market crisis. 2 The example strategy is a SPX 3m 1×4 20d/5d put spread rolled monthly. |

|

Funds operated by this manager: |

14 Jul 2022 - Be an investor not a speculator

|

Be an investor not a speculator Claremont Global June 2022 The current market sell-off has many market participants running for cover and waiting till the "uncertainty clears." Issues concerning the market are well-known - central bank tightening, high inflation, the Ukraine conflict, supply chain shortages and increasing concerns of a recession in 2023. And in current markets, I am reminded of the timeless words of Benjamin Graham (the father of security analysis and Warren Buffet's mentor) who made the clear distinction between investment and speculation. In his seminal work "The Intelligent Investor" on the very first page he makes the following observation:

Defining an adequate returnWhen reading this quote the key word is adequate. Note that Graham makes no mention of market timing or predicting a bottom - a practice much loved by sell-side strategists. So what is considered an adequate return? Over the 100 years to December the S&P 500 has given an annual return of 8% p.a. Equity returns are simply a function of:

The S&P 500 path to adequateLet's break down these constituents: Earnings growth: looking at 2007 as our starting base (i.e. peak of that cycle) and using consensus earnings in FY22 - earnings per share (EPS) growth was on average close to 6 per cent per annum over the 15-year period. We think this number is a reasonable proxy of our long-term estimate for future earnings growth. Dividends: the current dividend yield is 1.6 per cent. PE expansion/compression: this is the hardest to forecast and requires an accurate forecast of future investor psychology and interest rates. Over the last 15 years the market multiple has averaged 16 times and the current multiple is 17.4x. Assuming a reversion to 16x over 10 years would detract 0.8% p.a. from an investor's return.

Source: FactSet If we add these three constituents together it leads to a return of 6.8% per cent - somewhat short of the long-term equity return of 8 per cent. And while this may not be quite "adequate", it is still a reasonable return compared to what's currently on offer in a savings account - although hopefully news here is improving and central bankers will offer some comfort to hard-pressed pensioners! This assumes one invests in the market through an index fund, where for the purposes of this article I have ignored passive fees. And as an active manager trying to beat the market - we have always targeted a long-term return of 8-12 per cent per annum. This is why last year we were cautioning clients that we expected future returns to be at the bottom end of our targeted range, given the elevated valuation of the market. However, the recent market sell-off has us feeling far more constructive and on the front foot with clients. Let's now look at this by breaking down into the same three constituents. The Claremont path to adequateEarnings growth: we believe our companies could deliver earnings growth over the long term in the low double digits. Dividends: the current yield on the fund roughly equates to our active manager fees. PE expansion/compression: our fund holdings now trade 1 per cent below their 10-year average and 13 per cent below the five-year average. We would argue that it is not unreasonable to expect PE multiples to have a neutral impact on future returns over the long-term. So, if we put this all together - we are much more confident of hitting the right side of that 8-12 per cent per annum equation than we were a few months ago. We know we have little ability to call the bottom, however at current prices we believe we have a reasonable probability of achieving an adequate return. The art of patienceTo conclude with Ben Graham and one of my favourite quotes on market fluctuations in Chapter 8 of the Intelligent Investor:

The sell-off this year has already seen us add two companies to the portfolio - companies we have been following for years while we waited patiently for an entry point. And now with 13 names in the portfolio and a cap of 15 - we have room for two more. Whilst no one likes a falling share market, it opens up a wider opportunity set for us and the ability to acquire truly great businesses at prices that ensure a fair risk-adjusted return. We intend to do just that. Author: Bob Desmond, CFA, Head of Claremont Global & Portfolio Manager Funds operated by this manager: |

13 Jul 2022 - Meta & the battle for digital advertising supremacy

|

Meta & the battle for digital advertising supremacy Antipodes Partners Limited June 2022 Antipodes has owned Meta (previously Facebook) since the end of 2018 and despite the recent volatility in which many sold out of the company, it remains one of our top 20 holdings. We think that even though competition for eyeballs is increasing, and will continue to increase, the digital advertising pie is growing, and Meta can continue to dominate advertising revenue over our investment horizon. Further we believe there are opportunities to increase the monetisation rate of core Facebook and Instagram. In this new podcast episode, Alison Savas is joined by Ben Legg, one of the world's leading authorities on the digital advertising industry. Ben is a former Google COO, and now helps global brands advertise on social networks. Some key points covered include:

|

|

Funds operated by this manager: Antipodes Asia Fund, Antipodes Global Fund, Antipodes Global Fund - Long Only (Class I) |

13 Jul 2022 - Super-sized rate hikes, super-sized credit risk, super-size problems. Follow the dominoes.

|

Super-sized rate hikes, super-sized credit risk, super-size problems. Follow the dominoes. Jamieson Coote Bonds June 2022

The change of policy in 2022 has set off a series of dominoes for asset markets. Government Bonds were first to fall in quarter one, with other assets also following aggressively into quarter two. Listed assets are marked to market instantly (which can often be unpleasant) whilst illiquid or private markets can hold previous asset valuation marks as there is no observable price where price discovery could occur. It is worth considering what those realisable values might be if higher quality or liquid public assets are already -10, -20, -30%? Is a credit crisis about to erupt?The dominoes of change are quickly bringing attention to credit default as it stands to reason that refinancing outstanding lowly rated corporate debt will become increasingly problematic. The Australian Government was borrowing 10-year money at 1.05% in August last year, these rates have now moved to over 4.05% today. If the Government has to pay over 4% when it used to pay a bit above 1%, then spare a thought for corporate borrowers who might have borrowed at super low rates and are now asked to refinance at Government Yield of 4% plus some large credit spread component. How long will the markets have confidence in these lowly rated corporates to refinance at such punitive interest rate levels? The danger here is that they cannot ROLL those existing borrowings forward. That means there is no further credit extended and they need to REPAY the initial borrowing amount as well. That is exactly how a credit crisis erupts.

This is the policy pivot we have written about for some time and has marked a turning point in asset performance. But how does a Central Bank do that here with inflation globally between 5 and 8 %? Central Bankers are now rapidly raising rates as fighting inflation has taken absolute priority over saving corporate zombies from bankruptcy, generating material stress in the credit complex as many investors flee the asset class. Credit risk has been spectacularly dormant as the broad decline in long term Government Bond yields since the 1980's, plus support from Central Banks, has fostered a "begin" environment for the assets class, slingshot by the massive support of flows and investor sponsorship in the ''search for yield'', under the financial repression of low interest rates. That sponsorship and flow looks likely to have ended with rates markets having a stunning sell off this year, leading most asset markets to weak performance. Many public credit assets have also underperformed - primarily from their inherent fixed income duration, rather than the material recalibration of credit (spread) risk.

The US Fed moved to 1.75% this week and suggested its next move is either 0.50% or 0.75% hike to 2.25 or 2.50% in July to continue the fight against inflation by killing demand in the economy. The forces corporate credit markets are now facingSo, the next complex issue facing markets will likely revolve around credit default and the stunning rebirth of credit risk in the corporate credit fixed income space. Credit is a high specialised market which is little understood by most investors. Credit quality, as measured by ratings agencies, ranges from the highly converted (but low yielding) AAA rated issuers, all the way through to lower CCC rated issuers classified as having substantial risk of default (known in markets as 'junk'). Due to the inherent credit risk in these lower rated securities, yields are far higher to entice investors to take on the risk of default.

Any such support for the market looks very difficult to achieve this time as Central Bankers are now rapidly raising rates to fight inflation. Would you lend money to a buy now pay later platform or a growth company with no sustainable earnings to meet debt repayments in the current environment? Thankfully for Australian investors we have very few names like this, but our corporate credit does move its sympathy with global markets which are full of such names. Rate hikes strike in an uncertain worldWith materially higher rates now priced by Government Bond markets, the economy is expected to slow rapidly as rate hikes bite, hitting the public, lowering confidence and curtailing discretionary spending. Liquidity and asset quality will become important considerations for portfolios looking to benefit from steep discounts in many quality assets. We do not expect that rates will fall back to anything like the emergency levels we have seen post pandemic, so it feels like the re-birth of credit and default risk could be with us for some time yet as we move to a structurally higher rate environment than in recent years. It is important to acknowledge that the playbook in the last few episodes of a corporate credit seizure (Central Bank rate cuts and Quantitative Easing) will not work under a higher inflation and unstable geopolitical environment. That pivot of policy simply isn't available if inflation remains above Central Bank mandate levels as we would expect for the balance of 2022 due to the global energy shock. |

|

Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged), CC Jamieson Coote Bonds Global Bond Fund (Class B - Unhedged) |

12 Jul 2022 - Australian Secure Capital Fund - Market Update

|

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund June 2022 Aggregated property values across the country on a monthly basis have slowed marginally, (-0.80%). The highest performer this month was Adelaide (+1.30%), followed closely by Perth (+0.40%). Australia's property price increases experienced over the last 18 months are now well and truly past their peak rate of growth. Interestingly however unit prices are holding their value better than houses across capital cities with regional property still remaining in positive growth. The market is quickly becoming a buyers market with aggregate home sales nationally through the June quarter now 15.9% lower than a year ago. However, with housing conditions cooling, the flow of new listings to the market is slowing which along with a strong labour market should help support prices Rental markets around the country also remain extremely tight with rents and residential property yields now rising at a faster rate than housing values also providing a buffer for property investors. Ultimately however it will be interest rates which will have the largest impact on the path of housing markets.

The weighted average clearance rate across the country is lower than last year at 59.8% compared to 2021's 75.4% clearance rate (-15.60%) Other cities across the board also achieved rates marginally lower than last year, with the exception of Brisbane. Brisbane increased by +5.90% compared to the previous year, with Canberra being dropping in comparison (-29.70%) Source: CoreLogic Source: CoreLogic Quick Insights Lowered Rates & Politicised Policy A new study by the Melbourne Institute has revealed that government support programs contributed very little to the health of the housing market during the pandemic. Instead, it was the RBAs low cash rate that boosted the purchases. Buyers took advantage of relatively low servicing costs and interest rates. Housing programs typically assisted only the few who applied early. The War Room Tony Lombardo, CEO of Lendlease; Janice Lee, PwC Australia Partner; Susan Lloyd-Hurwitz, CEO of Mirvac; and Tarun Gupta, CEO of Stockland, some of the nation's most senior property leaders came together earlier this month to discuss the ongoing housing crisis. The conclusion drawn in the Channel Nine boardroom was that government policies stimulating demand can only do so much. Ultimately, it is the lack of investment in property infrastructure and overly tight zoning policies that continue to stoke unaffordability. Sydney's Stamp Duties The NSW Coalition Government announced this month its new revisions to the stamp duty. The system would allow home buyers to opt-out of paying stamp duty in favour of a $400 and 0.3% annual land tax. Some were quick to note how this might increase housing prices as the money usually spent on stamp duty would instead go into an auction bid. However, as lenders take the cost of annual tax into their loan serviceability criteria, the impact of this legislation may become negligible. Funds operated by this manager: ASCF High Yield Fund, ASCF Premium Capital Fund, ASCF Select Income Fund |

12 Jul 2022 - Earnings risk is being contemplated by markets

|

Earnings risk is being contemplated by markets QVG Capital Management June 2022 Inflation driving higher rates and earnings risk (given recession fears), combined with tax-loss selling and flows out of equities, to deliver a horror month for the Small Ords. The benchmark fell -13.1% for June delivered the second worst monthly return since the GFC. The Aussie 10-year bond rate started the month at 3.34% and finished it at 3.66% but not before touching a high of 4.25% intra-month. The US 10-year Treasury Bond interest rate showed a similar pattern, starting the month with a 2.83% yield and finishing it at 3.06% via a 3.48% high. The moves lower in global and domestic equities are starting to price these higher rates. The new fear gripping markets is earnings risk. Depending on who you read, the average US recession sees -13% to -17% earnings cuts (the GFC was a lot worse). It is this earnings risk that is now being contemplated by markets. We have managed money in rising and falling rate environments and know which we prefer! In the past, rising rate environments have been gradual enough so that the earnings growth of our portfolio has compensated for multiple compression from higher rates. The unique feature of this market is not the magnitude but the speed of the move in rates which has led to the fastest compression of valuations ever as shown here: Valuations have never before compressed so quickly Year-on-year change in trailing Price/Earnings multiple of the S&P 500

The chart above shows we have been sailing into the wind, but it won't always be this way. Given the next leg of this bear market is likely to be a focus on earnings not multiples, we have been positioning the portfolio towards companies we believe have greater earnings certainty. This ought to mitigate the impact on the portfolio of a recessionary or slowing growth environment should it occur. Funds operated by this manager: |

11 Jul 2022 - ASML: a once in a lifetime buying opportunity

|

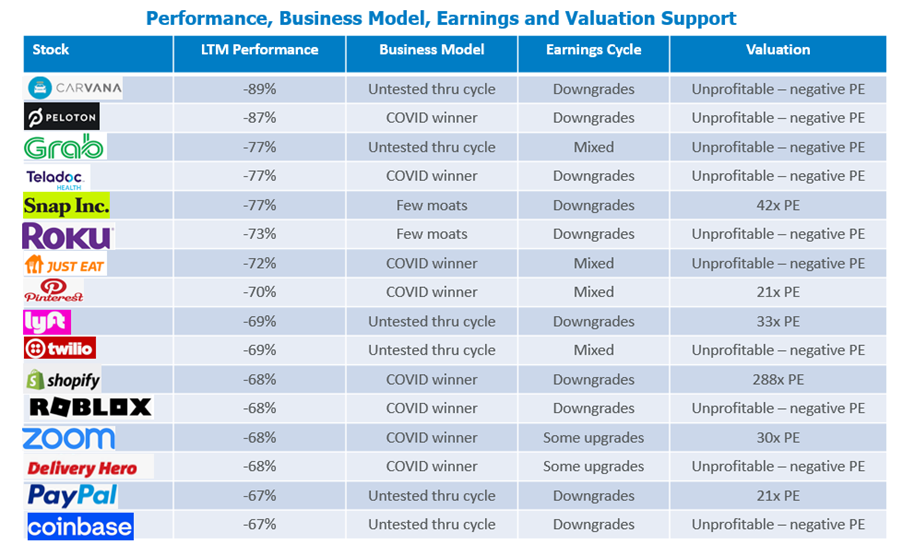

ASML: a once in a lifetime buying opportunity Alphinity Investment Management June 2022 There are 3 important criteria for identifying a once in a generation buying opportunity: 1) confidence that the business model will still be viable in a generation; 2) confidence that the stock has moved out of an earnings downgrade cycle into an earnings upgrade cycle; and 3) valuation support that signals a true buying opportunity, not an opportunity to catch a falling knife. Global equity markets have pulled back sharply in 2022 and it may be tempting to view some previously high-flying stocks as once in a generation buying opportunities. However, caution is needed because many of the worst preforming stocks year to date do not meet the 3 criteria outlined above. The following table shows stocks in the MSCI World Index that are down 65% or more in the last 12 months. Arguably, the vast majority of these do not meet the first criteria of a durable business model that will definitely be around for generations to come. In addition, most of these stocks are not in an earnings upgrade cycle, nor do they have strong valuation support even at these levels. Caveat emptor for these types of stocks

Source: Bloomberg, 31 May 2022, Alphinity Unlike the stocks in the table above, ASML is a high-quality stock that has corrected over 30% from its late 2021 high and meets the criteria of a durable business model, earnings upgrades and valuation support. A Business Model with Staying PowerASML is definitely going to be around in a generation as evidence by the fact that the stock listed in 1995 and has seen a few cycles already. ASML's enviable market share of around 70% provides confidence that there are deep moats around the business that can outlast periods of strong competition or disruption. Looking forward, ASML management likes to talk about the 3 main drivers of their stock being structural (AI, Internet of Things, 5G, Electric Vehicles, etc), cyclical (semi shortages and ongoing semi supply chain disruptions) and geopolitical (reshoring of semi capacity to the US and potentially Europe to reduce the risks associated with China/Taiwan). The combination of these 3 drivers is very powerful and supports a strong long term business case for ASML. Earnings Upgrade CycleASML's 1Q22 result came out slightly ahead while guidance for the FY22 maintained top line growth of ~20% and strong gross margins of ~52%. The bigger earnings story from the recent Capital Markets Day was a substantial upgrade to capacity targets for FY25 based on very strong demand. The potential upgrades here are significant - in the order of +50% revenue potential over the medium term. Valuation SupportASML is currently trading on a PE of less than 30x versus almost 50x PE at the end of FY21. This valuation is now below its 5 year average PE and represents an attractive PEG ratio of just over 1x. Furthermore, ASML's net cash balance sheet, 65% ROE and strong Free-Cash-Flow yield provide confidence in downside support for the stock. As shown in the table below, ASML's valuation support is in sharp contrast to many of the unprofitable or barely profitable tech stocks with no valuation support even at these levels. If markets continue to trend down, then many of the stocks that have been crushed in the last 12 months can continue to fall further. ConclusionStick with high quality stocks with durable business models, earnings leadership and valuation support. In this context, ASML looks very attractive. Happy hunting for once in a generation buying opportunities! This information is for adviser & wholesale investors only |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Sustainable Share Fund Disclaimer |

8 Jul 2022 - Rate Hike Volatility: Winter Comes in June for Crypto

|

Rate Hike Volatility: Winter Comes in June for Crypto Laureola Advisors 22 June 2022 The S&P 500 was flat in May but at the time of writing is down 5.8% in June and -22.9% ytd. Most financial assets are down negative double digits ytd: Nasdaq -31%, 10-year US Treasuries -15%, and Bitcoin -56%. The growing volatility and uncertainty in the financial markets globally is being driven in large part by the overdue and somewhat chaotic reaction of Central Banks to persistent inflation. The US Fed hiked rates by 75 bps in June - the largest hike in 27 years. The 10-year US real yields soared 150 bps in 60 days and most other bond markets suffered - the Australian 10-year yield rose 57 bps in 2 days. The persistent inflation, made worse by supply chain problems from lockdowns in China and war in the Ukraine, is starting to bite consumer spending and reduce economic growth around the world. In Europe, the 80% rise in the price of natural gas is one problem; the 50% reduction in deliveries by Russia is a worse problem. Europe may not be able to buy all the gas they need for next winter at any price. Investors fearing more volatility may want to raise cash to be "safe". But if cash buys 8% fewer goods and services next year compared to this year, too much cash may not be safe. A well-managed Life Settlements strategy can contribute to investors' portfolios in these turbulent times: it will be non-correlated with the equity and bond market turmoil, and it offers a return that has a strong probability of keeping up with inflation. PORTFOLIO CONSTRUCTION: THE ROLE OF LIFE SETTLEMENTS - The Role of the Laureola Fund in Portfolios of Private Clients and Family Offices Last month we discussed the role of LS in institutional portfolios showing that, mathematically, a small allocation to LS could both reduce portfolio volatility (risk) and increase returns over most 5-year periods because of its diversification characteristics, even if single digits returns are assumed. But there are other definitions of investment risk sometimes used by Private Clients and Family Offices. Some are simple and straightforward, but still very useful in analysis - maybe even more useful. Many strategies that promise diversification in bull markets fail to deliver the needed diversification in bear markets. But the Laureola Fund does. The Fund has outperformed all asset classes (except for commodities) ytd in 2022 including hedge funds as measured by the Barclay HF index (-5.7% ytd). The Fund has delivered positive returns in 7 of the 10 worst months for the S&P since inception, and in 2 of the 3 months when both had negative returns the negative return of the Fund was insignificant. The Fund has helped investors keep up with inflation delivering 6.7% net over the past 3 years. For once the theory and the practice align: The Laureola Fund can make a positive contribution to investors' portfolios in turbulent times no matter what analysis is used. Funds operated by this manager: |

8 Jul 2022 - Why are insurance stocks undervalued?

|

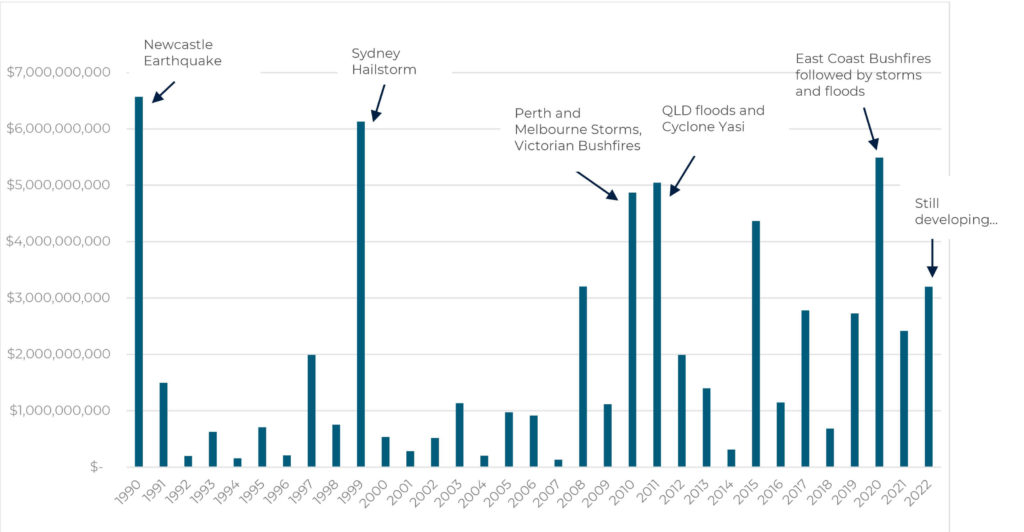

Why are insurance stocks undervalued? Tyndall Asset Management June 2022 There are a number of unique characteristics that make the insurance sector attractive in the current environment, including some company-specific factors which have led to valuation-based investment opportunities. Valuing the insurance sector Valuing insurance companies remains difficult due to the potential mismatch of estimated claims verses actual claims paid which may take years to finalise. Large catastrophes can take several years to be resolved—such as the New Zealand earthquakes—and injury claims can be stuck in the legal process for a long time. As a result, errors in claim loss forecasts can impact a company over many years. As investors, we look at a combined ratio calculation to measure the profitability of insurance companies, which is the sum of operating expenses and claim losses divided by premium revenue. A ratio below 100% indicates profitable insurance underwriting. Chart 1. Insured losses by Financial Years (in constant $2017)

Source: Insurance Council of Australia The chart is a reminder that disasters happen, and that risk is why people buy insurance to protect them from the impact of a disaster. A well-run insurance company prices risk appropriately. Insurance companies have accepted that there is an impact on the size and frequency of claims as a result of climate change, and premiums have increased to reflect this. What makes insurance companies attractive in the current market climate? The current market environment is characterised by rising interest rates, energy price spikes and higher inflation. This has led to a softening in economic growth and growing fears of recession. Stagflation or recession will negatively impact profit margins and valuations for companies. One of the things that makes the insurance sector unique is that premiums are billed and collected up-front, delivering in a premium float before claims are paid. The float is usually large and is invested to generate additional returns on top of an underwriting margin. Typically, this large premium float is invested in a mixture of cash and bonds, and possibly a small proportion in shares and other assets. Insurance companies aim to make an insurance margin which includes a return on the float that is akin to a leveraged investment return, since the return is earned on the premium float. The insurance sector is one of a handful that benefits from higher interest rates, with a 1% increase in rates equating to 10-20% earnings upside. The insurance Industry structure in Australia is attractive, operating as a functional oligopoly with the two major domestic insurers—QBE and IAG—taking approximately 70% market share. What makes the structure of insurance companies different? The business service provided by insurance companies is the pricing and pooling of risk. It does not require an inventory of raw materials or finished goods, freight costs, or energy consumption. Premiums are typically a function of asset value and rise with the insured value. The rate of return on insurance floats improves as interest rates rise, which is the opposite outcome experienced by most companies. Inflation can flow into claims costs, though insurers do generally mitigate this by adjusting premium prices upwards. Furthermore, insurers would face similar pressure and typically be less likely to compete in an inflationary environment. Why are the insurance stocks undervalued? The recent increase in the frequency of disasters and associated claims has weighed on investor sentiment, with concerns that estimated losses and exposure protection limits would be exceeded. To date, the measures in place have provided adequate protection. In addition to claim frequency, a series of operating missteps have dented investor confidence. Most notably, QBE, IAG, as to a lesser extent Suncorp, were forced to raise provisions for Business Interruption claims relating to COVID-19 and to manage costs associated with insurance policy documents incorrectly referencing the Quarantine Act 1908 (rather than Biosecurity Act 2015). IAG was disproportionately impacted by this and had to raise equity. Litigation has so far favoured the insurers, which may lead to the future release of surplus provisions for claims. Investor confidence in IAG waned further after the company suffered humiliating make-goods as a result of failing to apply group policy discounts and payroll errors. Accusations that IAG retained risk to the Greensill financial collapse proved unfounded, with the company clarifying that the business division that had this exposure had been sold and the risk transferred to the purchaser. What are the signs that things are improving? Consistent with IAG and Suncorp's February results commentary concerning premium rate increases, QBE released a performance update in early May which confirmed a healthy 22% growth in constant currency gross insurance premium revenue. QBE indicated that after the increase in risk rates and a 9% reallocation into riskier assets, the expected running yield on the investment portfolio has almost tripled to an exit rate of ~2%. The operating missteps of IAG and QBE have rattled investor confidence. Suncorp has fared better following its focus on cost reductions and dividends, and this has been rewarded by the market through share price gains. We expect a recovery in market valuation and dividend payments from both IAG and QBE as: (i) the cost impact of remediation fades; and (ii) the industry-wide improvements in premium pricing are earned and higher running yields on the premium float are delivered. The valuation, dividend profile, and sensitivity to rates, inflation, and the risk of stagflation leave IAG, QBE, and Suncorp well placed to outperform. And with high dividend payouts expected to persist, the Tyndall Australian Share Income Fund remains happily overweight the sector. Author: Michael Maughan, Portfolio Manager, Tyndall Australian Share Income Fund Funds operated by this manager: Tyndall Australian Share Concentrated Fund, Tyndall Australian Share Income Fund, Tyndall Australian Share Wholesale Fund Important information: This material was prepared and is issued by Yarra Capital Management Limited (formerly Nikko AM Limited) ABN 99 003 376 252 AFSL No: 237563 (YCML). The information contained in this material is of a general nature only and does not constitute personal advice, nor does it constitute an offer of any financial product. It does not take into account the objectives, financial situation or needs of any individual. For this reason, you should, before acting on this material, consider the appropriateness of the material, having regard to your objectives, financial situation, and needs. The information in this material has been prepared from what is considered to be reliable information, but the accuracy and integrity of the information is not guaranteed. Figures, charts, opinions and other data, including statistics, in this material are current as at the date of publication, unless stated otherwise. The graphs and figures contained in this material include either past or backdated data, and make no promise of future investment returns. Past performance is not an indicator of future performance. Any economic or market forecasts are not guaranteed. Any references to particular securities or sectors are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities or sectors and no warranty or guarantee is provided. |