News

6 Oct 2022 - Why on earth would Experiences thrive with all the gloom around today?

|

Why on earth would Experiences thrive with all the gloom around today? Insync Fund Managers September 2022 Put simply-Pent-up demand. Pre-Covid expenditure on experiences had been consistently growing ahead of GDP and its sub-segment, travel, was one of the fastest growing. Most megatrends within Insync's portfolio tend to have low sensitivity to economic cycles but the one sub-segment that suffered temporarily was travel. The extent of the fall in travel was unprecedented. Worldwide a staggering 1 billion fewer international arrivals in 2020 than in 2019. This compares with the 4% decline recorded during the 2009 global economic crisis (GFC).

There has been a lack of visibility on how leisure travel was going to emerge after governments implemented onerous travel restrictions. This was compounded by the shift to working from home with online meetings reducing the need for face-to-face meetings. What we do know is that humans desire to travel is hardwired into all of our DNAs. As travel restrictions have started to ease consumers appear to be making up for lost time. Airlines in the US last month reported domestic flight bookings surpassing pre-pandemic levels! US travellers spent $6.6 billion on flights in February, 6% higher than February 2019. Airlines for America, a leading US industry advocacy group noted that travellers have been eager to book tickets as COVID restrictions lifted. This provides a good indicator for the rest of the world. Our families and friends are all planning new adventures and reunions too. Interestingly, rising jet fuel prices, which have put upward pressure on ticket prices, has so far not deterred travellers who are willing to spend more. Emirates recently added a fuel surcharge and saw booking rise! A number of surveys are painting similar stories. TripAdvisor, found that 45% of Americans are planning to travel this March and April, including 68% of Gen Z travellers. This number will climb higher as the summer season rapidly approaches, as 68% of all American adults will vacation this summer (The Vacationer). No wonder hotels around the United States are nearing or have already surpassed pre-pandemic occupancy. Just try finding a decent, moderately priced hotel room in Sydney, as two of our team have recently experienced. The megatrend of Experiences is accelerating. Finding the right businesses benefitting from the trend is equally important for the consistent earnings growth we seek. It's why Cruise lines, airlines and hotels, whilst obvious picks, don't meet the quality criteria we insist upon.

Recently we reinvested into Booking Holdings after the over-blown pull back in its share price and the Covid event subsiding. It generates prodigious amounts of cash because of their scale and superior margins versus its competitors. As well as delivering a commanding competitive position they also help it in protecting against inflation. Bookings recently overtook Marriott, the largest hotel group, in gross volume booked in 2012, and today stands 70% bigger. Companies with superior business models and balance sheets tend to come through a crisis strengthening their competitive position. Booking Holdings is a prime example. The structural reduction in business travel has made hotels reliant upon OTAs once again to fill-up their rooms. This has been evidenced by recent data showing strong market share gains, in excess of pre-COVID levels. Second is the shutdown of Google's "Book on Google" product, removing the biggest perennial risk to the OTA investment case. The fact that the most powerful online search engine is shutting down this service is testament to the powerful position that Booking Holdings occupy.

Long term, travel looks set to continue to grow ahead of GDP as populations age, emerging market middle classes expand, and discretionary spend shifts more from "things" to "experiences.". Booking Holdings will be a major beneficiary compounding earnings for many years with its share price likely to follow the consistent growth in earnings. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

5 Oct 2022 - Around the world in 200 Meetings, Jonas Palmqvist: Medical Technology

|

Around the world in 200 Meetings, Jonas Palmqvist: Medical Technology Alphinity Investment Management October 2022 Jonas Palmqvist shares his highlights from his recent trips to the US, the key trends and themes within the healthcare sector and the future trends to look out for in medical technology. Speakers: Jonas Palmqvist, Portfolio Manager & Elfreda Jonker, Client Portfolio Manager This information is for adviser & wholesale investors only. |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Sustainable Share Fund Disclaimer |

4 Oct 2022 - Which Emerging Markets look good? Hint: look for tourists

|

Which Emerging Markets look good? Hint: look for tourists Pendal September 2022 |

|

WHEN investing in Emerging Markets, consider going where the tourists go. That's the message from Paul Wimborne, who co-manages Pendal's Global Emerging Markets Opportunities Fund. For Paul and his EM team, investing starts at country-level - which means a lot of time spent sifting through national data before deciding where to invest. One of the best indicators of the health of a country is its tourism levels, he says. A strong tourism sector creates jobs, boosts local economies, adds to government revenue and foreign exchange earnings, as well as improving the cultural exchange between countries. It signals opportunities for investors in emerging markets. This is borne out by comparing the tourism sectors in Mexico, one of the better performing emerging economies, and Thailand, says Wimborne. Both countries rely on tourism and facing similar challenges - reduced capacity among airlines, airport chaos as operations ramp up again, and rising oil prices. But there is pent-up demand internally and externally, post-Covid lockdowns. The outlook for the two countries is very different. "The best tourism news is coming out of Latin America, and particularly Mexico," Wimborne says. "Passenger traffic is already back to pre-COVID levels in Mexico. That not really a surprise when you consider that tourism in Mexico depends on the United States consumer. "In the US, consumer confidence is pretty good along with employment conditions. Extrapolating the tourism sector, Mexico is the bright light within emerging markets." In contrast, many Asian economies, reliant on China, are struggling to re-emerge from the COVID pandemic. "If you take Thailand, there were just over 3 million visitors in June 2019, before the pandemic. Pre-COVD tourism contributed about ten per cent of GDP. In June this year, there were just 800,000 overseas tourists," Wimborne says. "The missing tourists are mostly from China and other Asian countries. That's because many Asian countries, including China, are trying to minimise the effects of COVID, and are following zero-COVID strategies. Outbound tourism from China is essentially zero." There are emerging economies between Mexico and Thailand whose tourism markets fall in the middle. "In Turkey, visitor numbers are just below the record level set in 2019. In Dubai, numbers are at 85 per cent of pre-COVID levels," Wimborne says. There is a geographic trend in the health of emerging economies' tourism markets. "As you move east from Latin America through the middle east, and then into Asia, tourism markets worsen. In essence, Chinese tourists are the key lagging factor in international tourism recovery. "Countries like the Philippines, Malaysia and particularly Thailand because of its reliance on tourism, are going to lag emerging markets in other regions. It's going to take longer for some countries in Asia to recover, than in other parts of the world." Author: Paul Wimborne, Senior Portfolio Manager and Co-Manager |

|

Funds operated by this manager: Pendal Focus Australian Share Fund, Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Regnan Global Equity Impact Solutions Fund - Class R, Regnan Credit Impact Trust Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

30 Sep 2022 - Times like these - investing in sustainable growth companies makes sense

|

Times like these - investing in sustainable growth companies makes sense Insync Fund Managers August 2022 For the best part of 10 years, we've enjoyed the tranquil waters of low and stable inflation and even lower interest rates. That's all changing.

Many companies will struggle in this new world, however there is a small group who will thrive. And they have one thing in common: sustainable compounding earnings growth. It's never been more important for investors. We anticipate markets are already shifting focus after a recent wild swing backwards impacting all, deserved or not, to the prospect of Goldilocks economic conditions (not too hot nor too cold). The evolving economic backdrop is accelerating the business performances of the type of stocks that we hold at Insync; specific companies backed by our megatrends. Whether it's demographic shifts, digitisation or even pet humanisation; its megatrends like these providing the tailwinds for their growth, irrespective of the economy. And, it's why we remain fully invested despite market swings and the often touted fears by commentators. Investing in the highest quality stocks benefitting from megatrends delivers strong earnings growth over a full economic cycle. This is because of the duration of the megatrends being far longer than mere themes. Recent portfolio examples include Home Depot (see below) and Walt Disney (whom recently increased ticket prices by 7% with zero impact on demand). Our holdings possess high gross margins and strong pricing power, providing strength in both high and more normalised inflation environments. Our portfolio is well positioned as a result for continued delivery of the 5 year aim of both funds, as stock prices over the longer term follow consistent earnings growth.

Home Depot (a supersized bunnings) benefits from the 'Household Formation' Megatrend, fuelled by the all-important 'Demographics' Super Driver. Understanding changing demographics across all ages and segments globally is very important in identifying the winning companies of the future. One example is the escalation in the 47 year old age cohort in the United States over the next 8 years (see graph below).

The acceleration in the age 47 cohort coincides with the median average age of all home buyers, pushing up construction demand. Additionally a housing supply deficit in the US as high as 3.8m homes exists. On the renovation front, seniors are increasingly reluctant to move into aged care centres, and the increased 'working from home' trend further fuels demand. These are long duration strong tailwinds. Short term interest rate rises, and other macro factors are unlikely to alter this powerful megatrend. Home Depot is a big winner of all this. Think of it as a massive Bunnings network with almost 2,000 stores! They serve both trade and DIY markets, dominating the US building supply industry and run by a highly competent management team. Despite rising interest rates their recent strong results are testament to both the strength of the company and the power of the megatrend. Home Depot delivers very high returns on invested capital with an expected 10-15% p.a. compound annual earnings growth in the years ahead. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

29 Sep 2022 - Sector Spotlight: SGH

|

Sector Spotlight: SGH Airlie Funds Management July 2022 |

|

Hear from Joe Wright as he provides a backdrop on Seven Group; a diversified investment business operating mining and industrials companies including WesTrac, Coates and Boral. Speaker: Joe Wright, Equities Analyst Funds operated by this manager: Important Information: Units in the fund(s) referred to herein are issued by Magellan Asset Management Limited (ABN 31 120 593 946, AFS Licence No. 304 301) trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks.. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

29 Sep 2022 - Are we there yet? (Whitepaper)

28 Sep 2022 - 10k Words

|

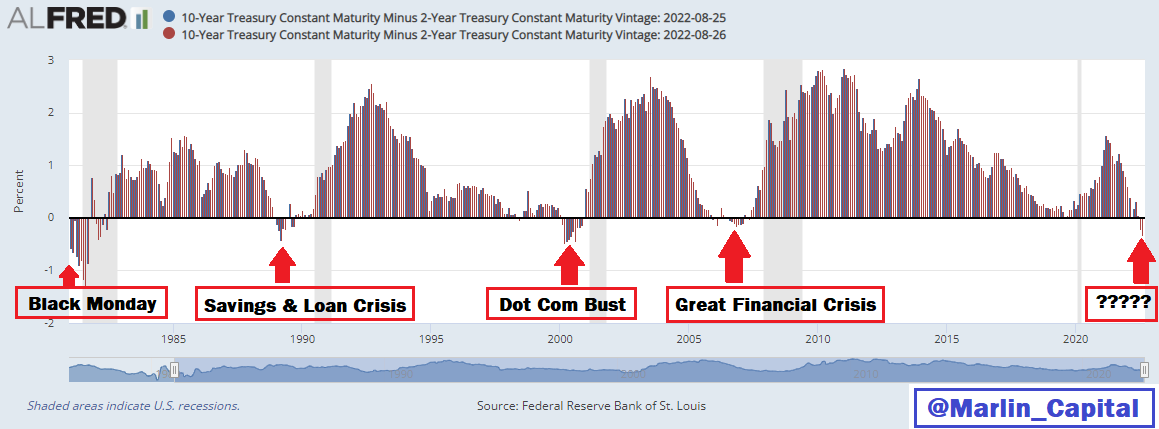

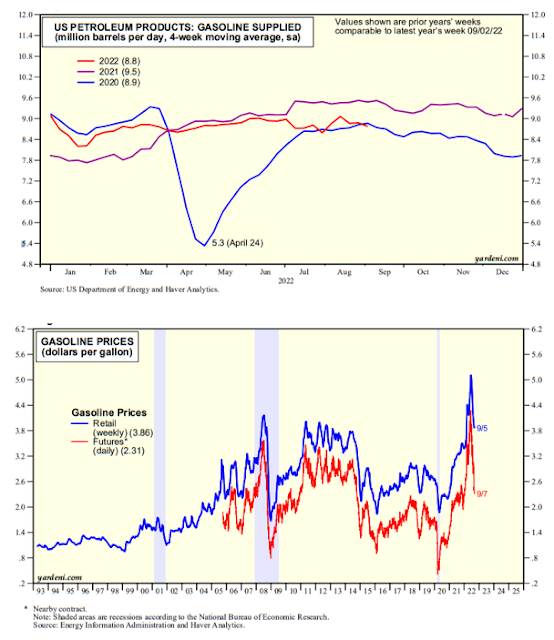

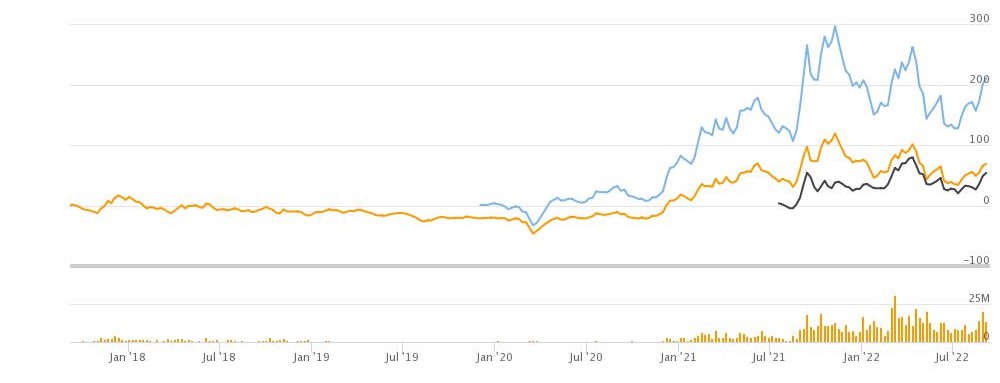

10k Words Equitable Investors September 2022 Earnings season on the ASX has come to a close with a historically low number of downgrades on the FY22 numbers, as tracked by Wilsons, but more downgrades than upgrades to EPS and dividend guidance for FY23, based on Evans & Partners' numbers. The one year return on Bloomberg's benchmark for the bond market is down 19% over the past 12 months. While the Australian yield curve is sloping upwards, the US yield curve is currently inverted. An inverted yield curve has historically led to some type of "break" in the system, @Marlin_Capital warns. But the inflation data is potentially turning - Yardeni highlights plunging US gasoline prices. Given the European situation, nuclear power and uranium are seeing a revival of sorts, at least with Japan revisiting its stance. Uranium equities have been advancing and the Washington Post ran a Blooomberg piece highlighting the unsavoury sources of current uranium supply. Taking a look at equities, Bespoke's optimistic take on the June half-year's poor showing is that such a poor first six months is typically followed by 12 months of 20%+ returns for the S&P 500. We thought it was interesting how closely the Grayscale Ethereum Trust has traded in comparison with the ARK Innovation ETF - a speculative cryptocurrency vehicle alongside a high growth tech investment vehicle. And potentially adding some colour to that is Visual Capitalist's charting of the demise of long-term investing. Aggregate ASX earnings downgrades announced over course of 12 month reporrting cycle

Source: Wilsons Net guidance upgrades for FY23f for the S&P/ASX 200

Source: Evans & Partners Bloomberg Global-Aggregate Total Return Index Value Unhedged USD

Source: RBA Australian and US yield curves

Source: worldgovernmentbonds.com An inverted yield curve has historically led to some type of "break" in the system Source: @Marlin_Capital, Federal Reserve of St Louis US gasoline priced have plummeted as consumption is reduced relative to a year earlier Source: Yardeni Research North American uranium ETFs on the rise (URA, URNM, U.U)

Source: TIKR, Equitable Investors Authoritarian nations dominate the world's uranium production

S&P 500 has been up at least 22% in the year following prior 20%+ two-quarter drops

Source: Bespoke Grayscale Ethereum Trust (orange) and ARK Innovation (green) moving together

Source: TIKR, Equitable Investors The average holding period of shares on the NYSE has fallen to new lows

Source: Visual Capitalist September Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Nothing in this blog constitutes investment advice - or advice in any other field. Neither the information, commentary or any opinion contained in this blog constitutes a solicitation or offer by Equitable Investors Pty Ltd (Equitable Investors) or its affiliates to buy or sell any securities or other financial instruments. Nor shall any such security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. The content of this blog should not be relied upon in making investment decisions. Any decisions based on information contained on this blog are the sole responsibility of the visitor. In exchange for using this blog, the visitor agree to indemnify Equitable Investors and hold Equitable Investors, its officers, directors, employees, affiliates, agents, licensors and suppliers harmless against any and all claims, losses, liability, costs and expenses (including but not limited to legal fees) arising from your use of this blog, from your violation of these Terms or from any decisions that the visitor makes based on such information. This blog is for information purposes only and is not intended to be relied upon as a forecast, research or investment advice. The information on this blog does not constitute a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Although this material is based upon information that Equitable Investors considers reliable and endeavours to keep current, Equitable Investors does not assure that this material is accurate, current or complete, and it should not be relied upon as such. Any opinions expressed on this blog may change as subsequent conditions vary. Equitable Investors does not warrant, either expressly or implied, the accuracy or completeness of the information, text, graphics, links or other items contained on this blog and does not warrant that the functions contained in this blog will be uninterrupted or error-free, that defects will be corrected, or that the blog will be free of viruses or other harmful components. Equitable Investors expressly disclaims all liability for errors and omissions in the materials on this blog and for the use or interpretation by others of information contained on the blog |

.png)

27 Sep 2022 - Webinar Replay: Catalyst Fund

|

L1 Capital Webinar Replay: Catalyst Fund L1 Capital September 2022 WEBINAR REPLAY | L1 Capital Catalyst Fund | September 15, 2022

Speaker: James Hawkins, Partner & Head of L1 Capital's Catalyst Fund Time Stamps: • 0.44 Fund overview • 2.50 Reflections from the first year • 4.49 Activist market observations • 13.17 Questions from investors |

|

Funds operated by this manager: L1 Capital Long Short Fund (Monthly Class), L1 Capital International Fund, L1 Capital Long Short Fund (Daily Class), L1 Long Short Fund Limited (ASX: LSF), L1 Capital Catalyst Fund, L1 Capital Global Opportunities Fund |

27 Sep 2022 - Investment Perspectives: Why rising interest rates aren't working (yet)

26 Sep 2022 - Look beyond market noise to unlock China's growth

|

Look beyond market noise to unlock China's growth abrdn August 2022 Market sentiment on China has become especially fragile of late amid fears over near-term growth. However, we see reasons to be positive and urge investors to think longer term and ignore market noise. Hot topics among our investment teams include zero-Covid policy, US-China tensions, monetary and fiscal easing, the weak economic backdrop, a beleaguered property sector and regulatory oversight. China's economy contracted 2.6% in the second quarter this year on the back of Covid-19 lockdowns and a real estate sector under severe liquidity stress due to continued government deleveraging. Of course, these headwinds will likely trigger further monetary and fiscal policy easing, which will support China's economy. Chiefly we expect infrastructure spending and modest interest rate cuts. In the absence of strong stimuli, we're anticipating a gradual turnaround. Our Research Institute is forecasting year-on-year GDP growth of about 3% in 2022 - below market consensus of close to 4%. We see authorities have levers to stabilise the property sector, and growing policy support reaffirms Beijing's commitment. Reportedly they're considering a rescue fund to deliver unfinished residential projects. While it may be insufficient to shore up buyers' confidence, it's a step in the right direction. Further, we expect policymakers to dilute or discard their zero-Covid strategy over time, most likely after the Party's 20th National Congress this year. So we see lockdown effects on growth dissipating. Similarly we see regulatory pressures easing. At a recent Politburo meeting we noted support for expanding China's universe of digital platforms and standardising supervision. Stable regulation will help to improve investor confidence and could drive multiple re-ratings for e-commerce companies. Clearly, geopolitical risk is hard to predict and we expect heightened US-China tensions to last for some time. But we view such tensions as periodic and part of an evolving geopolitical landscape. Our base case is that Beijing will not engage in direct military conflict with Taiwan in the near term. We think cooler heads will prevail in recognition of the heavy cost to economies and global stability. We believe imposing sanctions on Taiwan would be contrary to Beijing's own economic interests, while more military drills around the Taiwan Strait risk disrupting global supply chains and logistics. So what might investors expect? Here we outline our investment teams' China views. Equity teamIt's early for China's economy to show strong signs of recovery on the back of easing measures. So we expect equity markets to remain rangebound in the near term. But we're constructive on the outlook as stimulus measures start to work their way through the system in the second half of 2022. "We're constructive on the outlook as stimulus measures start to work their way through the system in the second half." Companies have started reporting their first-half results, with investors now more focused on analysing fundamentals to understand their underlying strengths and weaknesses. Given our focus on high-quality stocks, we're optimistic about the earnings resilience of our holdings. Valuations also look attractive. The MSCI China A Onshore Index's 12-month forward price-earnings ratio is 11.6x - comfortably below 15.4x for MSCI World and against a five-year average of 12.6x.1 China aims to reduce real estate's contribution to GDP growth due to the sector's high leverage. We have positioned our equity portfolios around the following five themes that we think will enjoy state support and are deemed critical to give China a competitive edge in its economic rivalry with the US: Aspiration: rising affluence leading to fast growth in premium consumption; Fixed income teamWith inflation not an issue, we expect stronger fiscal policy-easing this year and further rate cuts over the next 12 months. However, we suspect growth in infrastructure investment might disappoint after a strong first half. Momentum in the property sector is too weak for it to recover this year. Property sales have fallen sharply and will likely stay low amid impaired consumer confidence. However, we think state-owned enterprises (SOEs) in the sector with continued access to funding are well-placed to outperform. Additionally, with the rollout of more co-ordinated government support, we see potential for stabilisation among large, well-established privately owned enterprise (POE) developers. More generally, Chinese SOEs have enjoyed healthy demand in recent months and we expect them to retain strong government support, although we remain cautious about valuations. We think onshore SOE spreads will remain tight in coming months. We have been trimming core SOE positions over rich valuations relative to Asian and global peers. For the same reason we underweight Chinese financials in the offshore market, especially big banks. We also see supportive liquidity conditions for Local Government Financing Vehicles (LGFVs) in the near term, albeit amid growing concerns about the ability of local governments to support them. Offshore China portfolio positioning:

Onshore China bond positioning:

Multi-Asset teamThe world is a highly unusual place today, with this economic cycle different for three reasons: policymakers are seeking to avoid stimulating the economy via the property sector; strict Covid containment measures continue to dampen consumption; and major central banks are tightening policy aggressively to fight inflation, leading to slower global growth. Whereas in China, where inflation is not an issue, economic growth is in the early stages of recovery after authorities started easing policy this year. Government bond yields are near historic lows, so not outright cheap. But equity risk premia and offshore credit spreads remain attractive. As a result, although Chinese growth is likely to see sequential improvement in the second half of this year, the strength of the recovery will be weaker than in previous cycles. Monetary policy is likely to remain loose, with credit growth driven more by government than the property sector. As policymakers seek to balance short-term growth with long-term structural reform goals, we remain long China onshore equity and China duration; cautious on China credit; and we recommend hedging currency risk when investing in China. In a normal cycle, an early recovery phase is the time to invest in Chinese equity. However, in this cycle we think the recovery will be highly uneven and asset allocators need to pay close attention to potential tail-risk from Covid lockdowns and the property sector. Active stock selection is key. In a normal cycle, as growth recovery takes hold, the bulk of government bond outperformance should be behind us. However, in this cycle the weak recovery suggests China's central bank is likely to keep liquidity conditions loose, meaning bond yields will remain lower for longer. In a normal cycle, credit should rally with equities. However, in this cycle we are not confident that policymakers will backstop troubled property developers, which means high-yield credit will remain distressed. Of course, that does not preclude interesting opportunities in investment grade credit. For currencies, we think CNY can stay resilient on a trade-weighted basis, but weakening external demand and a hawkish US Federal Reserve will put downward pressure on CNY against USD. For global investors, hedging CNY risk is not a bad idea as hedging costs are at their lowest for five years.

Author: Nicholas Yeo, Head Of China Equities; |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund , Aberdeen Standard Life Absolute Return Global Bond Strategies Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund 1 Bloomberg, 26 August 2022 |