News

24 Jan 2023 - 10k Words

|

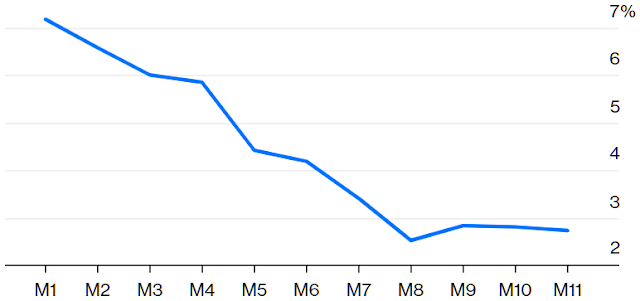

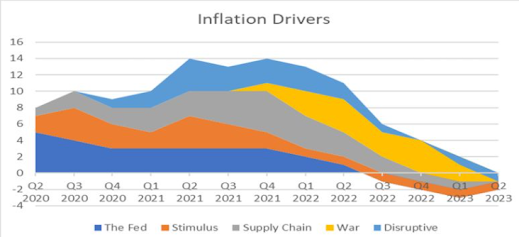

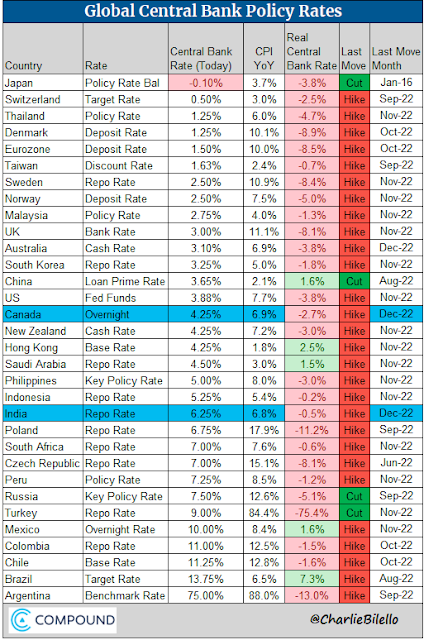

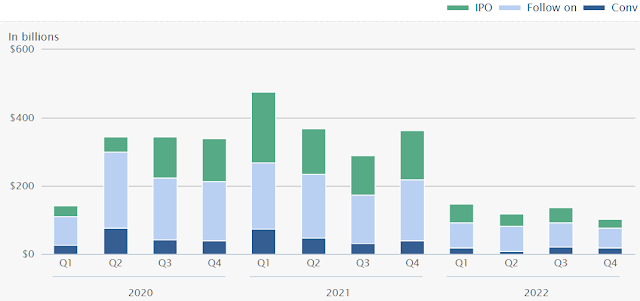

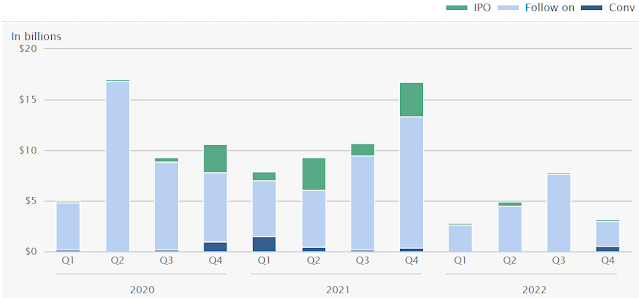

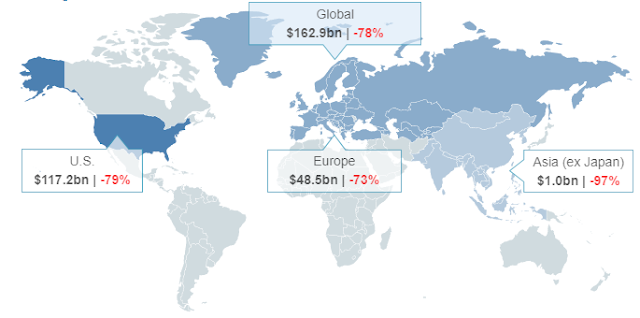

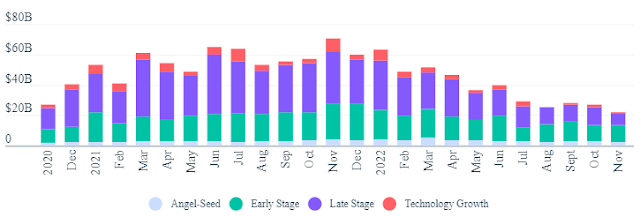

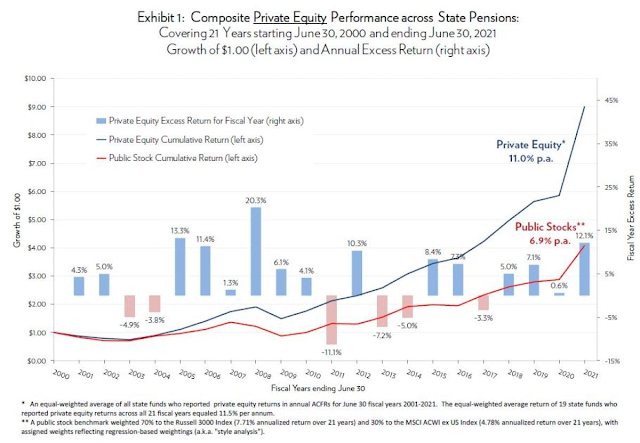

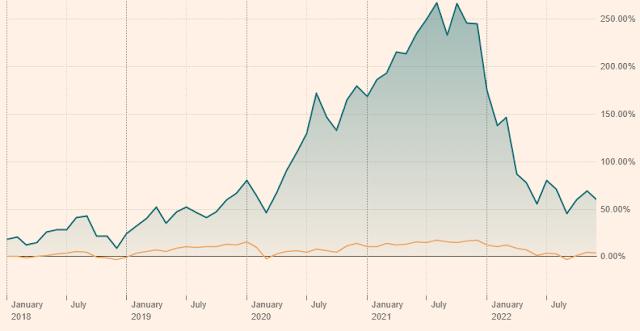

10k Words Equitable Investors December 2022 December's chart are largely lifted from an Equitable Investors slide deck. We can't really avoid taking a look at inflation and interest rates - so that is where we start with charts from Bloomberg showing the expectation for a sharp inflation correction in the US in 2023 (and a view on why based on Academy Securities' view of inflation drivers). Central bank policy rates remain, in the main, below inflation rates, as @charliebilello tabulates. CY2022 is almost gone and we can look back at capital markets and see sharp declines in the availability of funding - global equity capital raising volumes down 65% and Australasian down 54% year-on-year, using dealogic data. High yield debt issuance plunged even further. Crunchbase reckons that in global venture capital markets, seed funding dropped by a third, early stage halved and late stage is down by 80% compared to November 2021. Finally, Cliffwater shows us how private equity has outperformed since 2000 (in a period that coincides with historically low interest rates) and Refinitiv's Venture Capital Index gives us an idea of how alternative assets may have faired in 2022 if they were priced daily. Implied inflation (starts Dec 9) Source: Bloomberg Inflation Drivers (estimated) Source: Bloomberg, Academy Securities Global Central Bank Policy Rates (as of Dec 8, 2022) Source: Compound/@charliebilello Global Equity Capital Market Volumes ($USb)

Source: WSJ, Dealogic Australian Equity Capital Market Volumes ($USb) Source: WSJ, Dealogic High Yield Debt Capital Markets Source: WSJ, Dealogic Global Venture Capital Funding Source: Crunchbase Composite Private Equity Performance (US State Pensions) Source: Cliffwater Refinitiv Venture Capital Index Over 5 Years Source: FT December Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Nothing in this blog constitutes investment advice - or advice in any other field. Neither the information, commentary or any opinion contained in this blog constitutes a solicitation or offer by Equitable Investors Pty Ltd (Equitable Investors) or its affiliates to buy or sell any securities or other financial instruments. Nor shall any such security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. The content of this blog should not be relied upon in making investment decisions. Any decisions based on information contained on this blog are the sole responsibility of the visitor. In exchange for using this blog, the visitor agree to indemnify Equitable Investors and hold Equitable Investors, its officers, directors, employees, affiliates, agents, licensors and suppliers harmless against any and all claims, losses, liability, costs and expenses (including but not limited to legal fees) arising from your use of this blog, from your violation of these Terms or from any decisions that the visitor makes based on such information. This blog is for information purposes only and is not intended to be relied upon as a forecast, research or investment advice. The information on this blog does not constitute a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Although this material is based upon information that Equitable Investors considers reliable and endeavours to keep current, Equitable Investors does not assure that this material is accurate, current or complete, and it should not be relied upon as such. Any opinions expressed on this blog may change as subsequent conditions vary. Equitable Investors does not warrant, either expressly or implied, the accuracy or completeness of the information, text, graphics, links or other items contained on this blog and does not warrant that the functions contained in this blog will be uninterrupted or error-free, that defects will be corrected, or that the blog will be free of viruses or other harmful components. Equitable Investors expressly disclaims all liability for errors and omissions in the materials on this blog and for the use or interpretation by others of information contained on the blog |

23 Jan 2023 - Outlook Snapshot

|

Outlook Snapshot Cyan Investment Management December 2022 |

|

As a broad statement, it feels as if the market is in somewhat of a holding pattern. Even the central banks seem uncertain about the economic outlook. For example, in June last year, the governor of the US Fed, Jerome Powell, explained ''I think we now understand better how little we understand about inflation''. Further, RBA stated that interest rates would stay low until 2024. It has subsequently increased rates by 300 basis points (bp) with the most recent rise of 25bp taking the cash rate to 3.1%. The tightening of monetary policy has been swift and aggressive, which has thrown equities markets into a spin. As stated in our September monthly report: "We believe the most-likely first positive catalyst for a stock market recovery will be a line of sight as to when the interest rate hike cycle will end. Most central banks in developed economies are rapidly and aggressively raising rates. Stock markets hate this. We don't know if this monetary policy strategy will curb inflation as hoped, but an end to this cycle could provide a clear positive catalyst for a shift in sentiment for equities." The market is currently consumed by this issue and economists seem to be at the centre of every discussion. Gareth Aird, Commonwealth Bank's head of Australian economics, had previously forecast the RBA's rate hike in early December would be the last but he has updated his predictions after the RBA signalled more rate rises. He stated, "The tweak in forward guidance was not as material as we anticipated and as a result, we shift our risk case to our base case....We now expect one further 25 basis point rate hike in February 2023 for a peak in the cash rate of 3.35 per cent". Chief Economist at AMP Shane Oliver believes the cash rate has now "peaked" -- with a high risk of one final 0.25 per cent hike to 3.35 per cent in February. By end 2023 or early 2024 he expects the RBA to start cutting rates. However, that value doesn't get released in a straight line, and we are in the middle of one of those frustrating periods at the moment. But the market is forward looking, so investors waiting for genuine clarity around the economy may well find that the market has already moved ahead of them this year. |

|

Funds operated by this manager: Cyan C3G Fund |

20 Jan 2023 - Three Ways to Profit in 2023

|

Three Ways to Profit in 2023 Wealthlander Active Investment Specialist November 2022

A year ago, we communicated that inflation and geopolitical risks would dominate 2022. Early in 2022, we predicted the recession would strike within 18 to 24 months. We now expect that the outlook for 2023 will be dominated by the following economic drivers: US and global recession, volatile inflation outcomes, and continuing geopolitical risks. This provides tremendous challenges to traditional equity and property-centric portfolios and great opportunities for unconstrained active management. Let us explore three ways we expect to benefit from this outlook to position and profit in 2023. (1) Precious Metals and Other Commodities Geopolitical risks remain extreme, and war is a highly profitable business for some instrumental people and entities, with the Pentagon again being unable to pass an audit. The war in Ukraine is at risk of escalation and is no closer to being resolved. The Middle East remains a risk, and China and Taiwan remain unresolved. Politically the world appears to be fracturing both regionally and ideologically, and many important countries are now openly flouting US hegemony and working on deepening and developing their own trading and financial relationships. Precious metals was our favoured asset class for 2022 (and one of its top performers) and remains a must to own given the political and economic environment. Gold could easily reach new highs in 2023, offering diversification and some reasonable prospect of substantial gains. As part of a diversified portfolio, we also perceive opportunities in oil, uranium, speciality metals and food. (2) Active Management, Hedging and Shorting Even bonds may provide opportunities. Convertible bonds currently appear attractive as equity substitutes and offer better downside protection. Government bonds with duration have two-sided risks albeit they may still suffer under structural inflation, capital withdrawals or central banks unexpectedly holding their nerve and keeping policy tight for longer. Nonetheless, they will likely provide tactical opportunities to own small weightings. Liquid alternatives and trading strategies appear attractive for their low market sensitivity and their ability to protect capital. These include long/short approaches, relative value opportunities, contrarian trading, carbon trading and event-driven strategies. These strategies don't rely upon favourable equity markets to do well and provide a cash alternative, offering better capital preservation in weak markets. It is not necessary to lock up money for 7-10 years in illiquid alternatives to get the benefits of diversification, as liquid strategies provide attractive opportunities while so many stocks remain overvalued.. Investors in large commercial property managers like Blackstone are finding out that favourable published returns are not available to them when they want to redeem. Investors in some large Australian super funds could also potentially suffer similar issues, particularly if economic and financial market conditions further deteriorate. Stock picking will likely offer good opportunities into 2023, both long and short and even among some very large market leaders. Tesla looks to be the gift that keeps on giving on the short side, with the reality of strong competition, insider sales and lower growth in a recession bringing the company's valuation back down to earth. (We have successfully shorted Tesla more than once in 2022 and will likely do so again). Numerous still highly priced growth stocks are likely to disappoint further and will provide good hedging opportunities during market weakness in the early part of 2023. Companies like Zoom still fall into this category. Numerous "high promise" but currently unprofitable companies have had a disastrous 2022 whilst diluting shareholder equity by issuing large share and option incentives to management. Many large quality companies and household names where investors are hiding also appear overvalued; companies like McDonalds and Coca-Cola are trading at greater than 30 times earnings with modest growth and consumer sensitivity. Blackrock provides an opportunity to short passive management. Many commercial property stocks will likely be strong shorting opportunities, given the sector's disastrous outlook. Later in 2023, there may be significant opportunities on the long side in small caps and selective growth companies to play a recovery. On the long side, selective resource stocks still offer good longer-term opportunities, but many managers need to be avoided in the space due to demonstrably poor risk management and track records. If 2022 has proven anything at all about many money managers, it is that too many are like passive funds and rely upon rising markets, offering little risk management or capital preservation on the downside. Poor downside risk management can reveal who to avoid and switch away from! (3) Genuine Diversification and Differentiation We expect that markets will remain challenged in early 2023 as economic mismanagement, increased corruption and malfeasance, geopolitical, valuation, and volatile inflation and interest rate pressures continue haunting broad market outlooks. This will again prove highly challenging for passive management, which must wear all these factors to its detriment. Genuine active management, fundamental research, risk management and conservatism appear essential in this environment. We still see the end of a previously favourable period of globalisation and peaceful prosperity. Wages pressure, demographic issues and greater protectionism, regionalism, autocracy and greater socialism, along with less workforce participation, mean the labour and capital balance is shifting. Higher structural inflation and volatile inflation outcomes in coming years, along with various tail risks, must be carefully considered when building a portfolio and mean that the portfolio of the 2020s should be fundamentally different from years past. It is essential to be more conservative and have better diversification in this environment rather than simply gambling on strong financial asset returns, as the latter approach is best suited to a period that has now gone. 2022 has shown that many bottom-up investors who ignored these crucial top-down factors have been severely punished, for example, by holding large allocations to growth stocks or investing in what were traditionally defensive investments such as government bonds. Funds operated by this manager: WealthLander Diversified Alternative Fund DISCLAIMER: This Article is for informational purposes only. It does not constitute investment or financial advice nor an offer to acquire a financial product. Before acting on any information contained in this Article, each person should obtain independent taxation, financial and legal advice relating to this information and consider it carefully before making any decision or recommendation. To the extent this Article does contain advice, in preparing any such advice in this Article, we have not taken into account any particular person's objectives, financial situation or needs. Furthermore, you may not rely on this message as advice unless subsequently confirmed by letter signed by an authorised representative of WealthLander Pty Ltd (WealthLander). You should, before acting on this information, consider the appropriateness of this information having regard to your personal objectives, financial situation or needs. We recommend you obtain financial advice specific to your situation before making any financial investment or insurance decision. WealthLander makes no representation or warranty as to whether the information is accurate, complete or up-to-date. To the extent permitted by law, we accept no responsibility for any misstatements or omissions, negligent or otherwise, and do not guarantee the integrity of the Article (or any attachments). All opinions and views expressed constitute judgment as of the date of writing and may change at any time without notice and without obligation. WealthLander Pty Ltd is a Corporate Authorised Representative (CAR Number 001285158) of Boutique Capital Pty Ltd ACN 621 697 621 AFSL No.508011. |

19 Jan 2023 - Oil drops to lowest level of 2022 but supply-demand is likely to tighten over the medium term

|

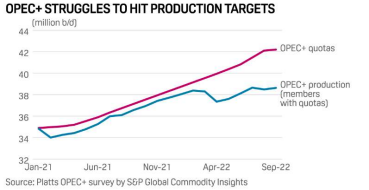

Oil drops to lowest level of 2022 but supply-demand is likely to tighten over the medium term Ox Capital (Fidante Partners) December 2022 The low oil price today is a result of weak demand (global economic malaise) and increased supply (US strategic oil reserve release). These factors will likely normalise in coming quarters. Over the longer term, demand is set to pick up driven by China opening up and the secular economic growth of other emerging economies. Demand is likely to significantly outstrip supply given the lack of investment that has gone into the sector.

Oil price has pulled back from over US$120 per barrel in June to less than US$80 per barrel over the last week. The oil market is factoring in a short-term slowdown in demand as rising interest rates start to impact real economic activities globally. We remain optimistic about the return potential of the energy sector in the coming years. Approximately 100M barrels of oil are consumed globally each day. A surplus or deficit of 1% or ~1M barrels can lead to significant price move. At present, oil demand is artificially low and is still below pre-covid levels. In China, oil demand is ~1M barrels per day below 2021 levels because of Covid lockdown, and global jet fuel consumption is ~2M barrels per day below 2019 levels. In terms of supply, the US government has been releasing its strategic petroleum reserves, adding 0.8M barrels a day to global supply since March 2022. This will slow as we go into 2023. As a result of the short-term demand and supply distortions, OPEC+ is cutting output by 2M barrels per day by the end of 2023 to support prices, illustrating supply discipline that can be flexibly applied to uphold a quasi-price floor if required going forward. Over the longer term, it has been evident that the members of OPEC+ has been struggling to produce to their quotas over 2021 and 2022. This is likely a result of a lack of investment in oil projects over the last decade. The upside for oil price can be significant as China opens up and other emerging economies continue to grow. Supply will struggle to keep up. Major oil companies in Europe are attractively valued and are trading at a significant discount to many of the oil majors in the US. Even at an oil price of US$70, European energy companies are typically trading on 5xPE, 15% free cash flow yield, compared to 14xpe and 7.5% free cash flow yield for the Americans. Ox has selective investments in some of the leading players in this space. The current pullback in oil can create additional investment opportunities for 2023, of which we are on the lookout. Funds operated by this manager: |

18 Jan 2023 - Australian Secure Capital Fund - Market Update

|

Australian Secure Capital Fund - Market Update November Australian Secure Capital Fund November 2022

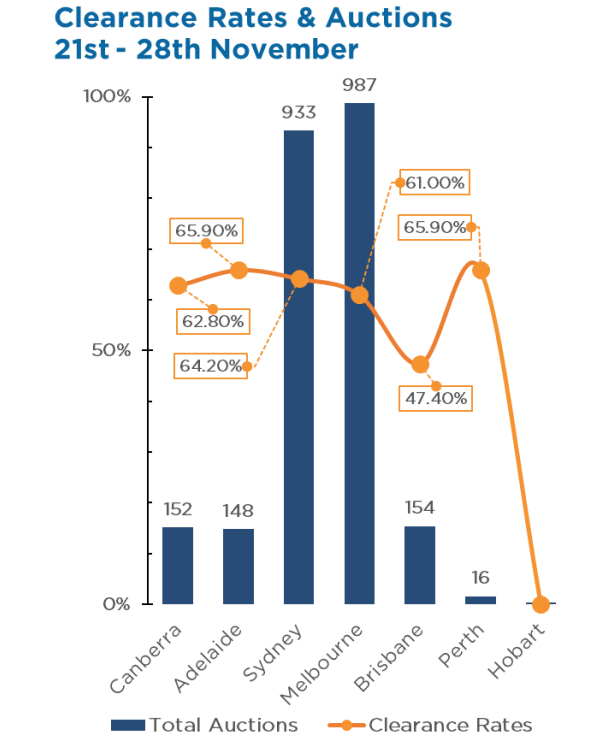

Property prices continued to fall across the nation with values declining a further 1.00% throughout November. This brings an approximate 7.00% (average of $53,400) decline since national property prices peaked in April of this year. Whilst this marks the seventh month of decline, the rate at which prices are declining is beginning to soften, with the 1.00% reduction being the smallest since the 1.60% monthly decline in August. Queensland again recorded the most significant monthly reduction, along with Tasmania with a 2.00% reduction in the Home Value Index. New South Wales, Canberra, Victoria and South Australia also experienced a reduction in value with 1.30%, 1.20%, 0.80% and 0.30% respectively. Western Australia remained stable, and the Northern Territory actually saw a small increase of 0.20% for the month. Record low vacancy rates of 1.00% have allowed unit prices continue to remain somewhat resilient, recording a 0.60% reduction for the month, bringing 4.70% reduction since prices peaked. The number of auctions held in the last weekend of November remained considerably below that of last year, with 2,393 auctions taking place as opposed to 4,251 last year. Whilst well below that of last year, the number of auctions were up 4.10% on the previous weeks results and were in fact the highest since a weekend in mid-June recorded 2,528 auctions. Clearance rates across the nation were also down on last year's figures, with only 61.50% of auctions clearing (down from 68.50% last year) indicating that vendors may not yet have responded to market conditions. Adelaide again recorded the highest clearance rate for the weekend with 65.90%, followed by Sydney (64.20%), Canberra (62.80%), Melbourne (61.00%) and Brisbane (47.40%). Source: Article, Report Funds operated by this manager: ASCF High Yield Fund, ASCF Premium Capital Fund, ASCF Select Income Fund |

17 Jan 2023 - Glenmore Asset Management - Market Commentary

|

Market Commentary - November Glenmore Asset Management December 2022 Equity markets globally were stronger in November. In the US, the S&P 500 was up +5.4%, the Nasdaq rose +4.4%, whilst in the UK, the FTSE 100 increased +6.7%, boosted by its heavy mining weighting. On the ASX, the All Ordinaries Accumulation Index rose +6.4%. Utilities were the best performing sector, boosted by the takeover bid for index heavyweight Origin Energy, which was up +41% in the month. Materials was the next best sector, driven by investor optimism around China loosening its covid lockdown measures. Telco's, financials and technology all underperformed in the month. Bond yields declined in November as investors started to become more positive that the pace of interest rate hikes from central banks will moderate along with some signs that inflation has potentially peaked. In the US, the 10 year bond yield fell -30 basis points (bp) to close at 3.74%, whilst in Australia, the 10 year rate fell -23bp to 3.53%. During the month, the RBA increased interest rates by 25bp for the seventh month in a row, taking the official cash rate to 2.85%. The A$/US$ rallied in the month, up +6.0% to close at US$0.68. Commodity prices were broadly higher. Nickel rose +23%, whilst copper, aluminium and lead also rose between +6-8%. Thermal coal rebounded +11.4% after an -18% decline in October. Also of note, iron ore was up +25.6% after falling for seven months in a row. Brent crude oil fell -10.0%. Funds operated by this manager: |

16 Jan 2023 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

|||||||||||||||||||

| Collins St Convertible Notes Fund | |||||||||||||||||||

|

|||||||||||||||||||

|

|||||||||||||||||||

| Capital Group Global Total Return Bond Fund (AU) | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

|||||||||||||||||||

|

Emit Capital Climate Finance Equity Fund |

|||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

Want to see more funds? |

|||||||||||||||||||

|

Subscribe for full access to these funds and over 700 others |

16 Jan 2023 - The Investment Outlook 2023

|

The Investment Outlook 2023 abrdn December 2022 As we look back on 2022, to describe the year as eventful seems an absurd understatement. So many events have dominated the news, each individually significant, and in aggregate almost overwhelming in consequence, both politically and economically. Here's a reminder of just a few of those events:

Climate crisis uncertaintyYet all these things will be relatively short-lived in their impact (and manageable) when compared to the existential threat that continues to grow relatively unabated from our failure to make progress on constraining global warming to the agreed target of 1.5°C. COP 27, the climate change conference held this year in Egypt, largely failed to expand on commitments made a year earlier with regards to phasing out fossil fuels, despite all the strong statements made around the necessity to do so. The one major step forward was the agreement of a deal that has been sought for over 30 years to launch a fund for 'loss and damage' to support those nations most exposed to the consequences of climate change. But details and financial funding have not been agreed. We can already observe more extreme weather events - notably the recent floods in Pakistan - which have devastating effects on impacted economies and contribute to the risk of a steady but dramatically expanded flow of migrants to other countries. Don't give upBut, as the old saying goes, where there are challenges, there are also opportunities. Here's where we see them:

Reasons to be optimisticIt's easy to be overwhelmed by all the uncertainty. That said, we've also seen steady progress in many places that may offer an antidote to the gloom:

2023 may well be a pivotal year for markets amid the economic challenges that remain. While these are clearly important, we mustn't take our eyes off potentially existential long-term issues. Author: Sir Douglas Flint, Chairman of abrdn |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund , Aberdeen Standard Life Absolute Return Global Bond Strategies Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund |

22 Dec 2022 - Investment Perspectives: The yield curve, recessions and soft landings

22 Dec 2022 - Why the cloud investment opportunity will outlast an economic downturn

|

Why the cloud investment opportunity will outlast an economic downturn Magellan Asset Management November 2022 |

|

The global shift to cloud computing is a seismic and transformational trend that we have backed for several years at Magellan. For the hyperscale public cloud vendors outside China - Amazon, Microsoft, and Google (the Magellan Global Fund holds all three companies) - it has created unprecedented market opportunity. These vendors have consistently generated strong double-digit revenue growth at scale and continue to do so to this day. Yet in the most recent two financial quarters, hyperscale cloud revenue has faced decelerating growth as enterprise customers reign in spend amid the uncertain macroeconomic backdrop. Has the story come to an end?

The trend this year is apparent. Excluding the impact of currency movements, hyperscale cloud revenue grew in aggregate 42% year-over-year in Q1. In Q2, the growth rate fell to 38%, and in the most recent Q3, the growth fell further to 34%. The two largest vendors, Amazon and Microsoft, expect this deceleration to continue, which means we should expect the growth rate to decline even more in Q4. On top of that, margins are falling, with both companies dealing with rising energy costs in their data centres while continuing to maintain their pace of double-digit operating expense growth. All of this may seem dire but let us unpack it further. We start by recognising that the deceleration this year appears more severe because it is being compared to several quarters of strong growth in 2021 due to cloud demand created by the pandemic responses. To try to adjust for this by looking at this year's quarterly growth rates on a 2-year annualised basis, we see a steadier growth trend, albeit one that is still slowing - from 40% in Q1, to 39% in Q2, to 38% in Q3. (The fact that we are seeing this type of growth on an aggregate US$160 billion in annualised revenue is staggering on its own). These decreases are more marginal and subject to noise, but there is broader evidence that IT spend is generally tightening. The unfavourability of these recent IT spending trends are, we believe, cyclical not structural. Market uncertainty has compelled enterprise customers to become more prudent or selective about their IT investments. Some customers are in industries facing challenges of their own such as supply chain issues, inflation, or labour shortages. We also expect some spend was driven by the period of excessive cheap, available money and this spend will not return. And as their customers seek to tighten their belts, hyperscale cloud vendors are taking it a step further and in fact helping customers to improve the efficiency of their spend (e.g., through lower priced options). In other words, the cloud vendors are effectively contributing to their own growth headwinds. Why do this? It is about driving trusted partnerships with customers for long term growth, rather than short-sightedly focusing on maximising growth today. This makes sense if one believes, as we do, that cloud has a significant multi-year growth runway ahead. In fact, the ability for customers to proactively dial up and down cloud spend according to their needs - rather than being burdened with the large, fixed costs of an on-premises data centre when times are tough - is one of the fundamental value propositions of the cloud, and the current environment reinforces this validity. Put another way, hyperscale cloud is doing exactly what it was meant to do. The effect of rising energy costs on the hyperscale cloud vendors has been negative but comparably modest so far. Amazon cited a 200bps impact to AWS margins in aggregate over two years, and for Microsoft we expect an impact of less than 100bps to its cloud margins this financial year, unless costs rise significantly higher. The cloud vendors are absorbing these higher costs in the near term, but we believe they possess the pricing power to share rising costs with customers over the longer term. An underappreciated point is that the energy efficiency of hyperscale data centres is far superior to what customers can achieve on their own, which is further demonstrating to these customers the advantages of being in the cloud. Cloud computing is proving its value to customers as much in this environment as it ever has, and we can see this when we delve beyond the quarterly headlines. It is why we continue to view this investment opportunity as compelling on the longer time horizon. It is an attractive, enduring, and multi-year opportunity that will deliver robust growth and attractive margins on the other side of the economic cycle we find ourselves in today. Author: Adrian Lu, Investment Analyst Sources: Company filings and Magellan estimates |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. A copy of the relevant PDS relating to a Magellan financial product or service may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to be implemented and its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |