News

7 Feb 2023 - Tips on Managing your own Super

|

Tips on Managing your own Super Marcus Today January 2023 |

|

I had a question about Portfolio Management from a Member. I sent him this. It might interest you. Two processes run side-by-side:

STOCK PICKING AND TIMING Stock picking and timing involves a few basic tenets that you might adopt. They include (and apologies for the simplicity):

MANAGING MARKET RISK As you probably know by now, I believe you can time the market and everyone who says you can't is an inexperienced amateur that has heard too many Buffett quotes or is a financial professional that has an interest in you doing nothing (because they don't have to make decisions but still get your fee). You can manage market risk by raising and lowering your cash weighting. One of the great advantages of managing your own money as an individual without oversight is that you can go to 100% cash. Something the big funds could never do. This allows you to protect capital in a bear market, whereas most of the major funds have no choice, they have a mandate which forces them to hold the market through thick and thin. They will play with a small cash weighting (5-15%?), but it is immaterial come a big market sell-off. They will never get out of the market in a bear market. You can. How much cash you hold is a daily debate, and there are no rules. I simply wake up every morning and make a decision. I rarely get scared by the market but will rapidly run up cash levels if I think its going wrong. And reverse it again when the squall is over. When it comes to running up the cash, I may sell a few stocks outright (the ones that are not performing) but will essentially take the top off every stock rather than stock pick. The main issue is to run up the cash and not get cute about which stocks to do it with. When it comes to this decision - read the Strategy section - it's what it's all about! Author: Marcus Padley, Founder of Marcus Today |

|

Funds operated by this manager: Marcus Today Equity Income SMA, Marcus Today Growth SMA

|

6 Feb 2023 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

|||||||||||||||||||

| Harbour T. Rowe Price Global Equity Fund | |||||||||||||||||||

|

|||||||||||||||||||

|

|||||||||||||||||||

| Cordis Global Medical Technology Fund | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

|||||||||||||||||||

|

Rixon Income Fund |

|||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

Want to see more funds? |

|||||||||||||||||||

|

Subscribe for full access to these funds and over 700 others |

6 Feb 2023 - Cycle is not a dirty word

|

Cycle is not a dirty word Airlie Funds Management January 2023 |

|

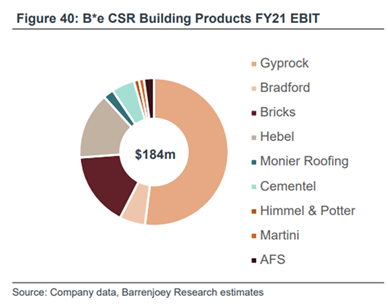

January 2023 In a perfect world, every stock we own would be net cash, generate high returns, be run by a world-class management team, and cheap. In practice, the presence of the first three criteria usually means that the investment falls over at the last criterion. Just like we don't tend to stumble across $500k houses in Point Piper with Sydney Harbour views, the stock market is rational: it usually bids the best businesses up to the highest price. This means we usually have to compromise on something. The one thing we never compromise on is the balance sheet - a business must have the appropriate financial structure for its business model or else we equity investors may find out exactly where we rank in the capital stack! Assuming the balance sheet is appropriate, we rely on our judgement as investors to juggle the trade-offs between business quality, management quality and valuation. One hunting ground where we tend to find businesses with attractive valuations is when everyone is very worried about "the cycle". For example, with a consensus view that a recession looks likely in the US, Europe and potentially Australia, we are seeing opportunities in businesses that are leveraged to the building cycle. The first thing to figure out when sifting through these ideas is whether the business sells a commodity. In investing it pays to have an open mind: cyclical businesses that sell commodity products can be great investments; one need look no further than BHP to find such an example. However, we have a few requirements. Firstly, we want to see a pristine, (preferably net cash) balance sheet. Returns are outside the company's control - typically dictated by the level of demand for a commodity and hence the price. Financial leverage combined with operating leverage can mean lights out. Second, we look for evidence of good industry structure. This means as few players as possible. Very few things are "pure" commodities. Often there are hidden barriers to entry - start-up costs, distribution networks or captured supply chains - that keep industries rational and cosy. This seems particularly prevalent in Australia. The tyranny of distance, both from global supply chains and having a small population spread across a large country, means a fixed profit pool that often doesn't support a third or fourth entrant. Two or three rational market players can see everyone making OK returns on their capital. Finally, we want a compelling valuation. If there's no intangible franchise value in a business, if it just makes bog-average products, you don't want to pay a high price for it. Luckily, the tendency for investors to tie themselves in knots trying to forecast where we are in a cycle tends to throw off frequent opportunities to buy cyclical businesses at good prices. Unluckily, those opportunities usually only come around when the cycle looks particularly on the nose. As such, we find you have to be brave and also be prepared to be early (potentially very early!), and willing to add to a position if it continues to fall as the cycle deteriorates. The risk in investing in cyclical commodity businesses is that, as Howard Marks says, to be too far ahead of your time is indistinguishable from being wrong. It is for this reason that we rarely make these initial investments our largest positions, preferring a smaller position size that we can add to should the leading indicators deteriorate further. One business we feel ticks these boxes is CSR , a recent addition to the portfolio. The company manufactures and distributes plasterboard, aerated concrete, bricks, fibre cement, insulation and other products under a range of different brands. CSR also has a 25% effective interest in the Tomago aluminium smelter in Newcastle. We are under no illusions as to the underlying quality of this business. With perhaps the exception of aerated concrete, where CSR has exclusive rights to the Hebel brand, the bulk of what CSR makes, and sells are commodity products. Returns will be cyclical, dominated by the level of residential building activity in Australia. Our thesis in owning CSR is that (a) the value of the surplus property underpins the bulk of the valuation, such that we aren't paying a very high residual price for the building products business, and (b) this building products business is probably a shade higher quality than it has been historically; mid-cycle margins and returns for CSR's building products should be higher this decade than the prior decade due to improving industry structure. Throwing in a rock-solid balance sheet ($142m net cash) makes the investment proposition stack up for us, albeit this is not without risks. Our valuation is based on our assessment of mid-cycle EBIT; however, we will be wrong on this assessment if industry rationality breaks down as demand falls (that is, if we see evidence of price-cutting to chase market share). Building products business: average quality but industry structure has improvedFrom an earnings perspective, the three most important businesses in CSR's Building Products portfolio are plasterboard (Gyprock), Bricks and Hebel (aerated concrete), making up a combined c75% of EBIT.

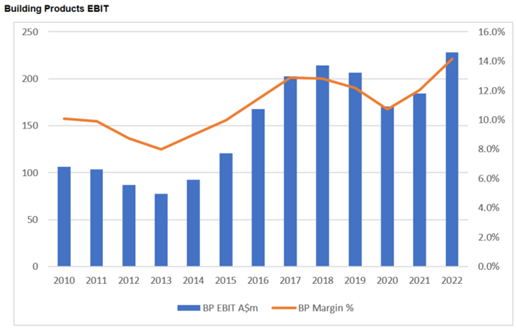

CSR has a dominant market share position in each of the plasterboard, brick and aerated concrete markets as a function of recent industry consolidation (Gyprock, PGH Bricks) and product exclusivity (Hebel). As per the below chart, EBIT margins are highly cyclical: in a great year (like FY23F) CSR is on track to make a 14% EBIT margin; in a bad year (2013) it made only 8% EBIT margins. We believe a return to these lows is unlikely for reasons we step through below. As such, we forecast trough EBIT margins of 10% rather than a historic 8%, and mid-cycle EBIT margins of 12% rather than a historic 10%.

Plasterboard is the most important business, accounting for over 50% of the building products' EBIT. East-coast plasterboard is a three-player market, with CSR and Knauf enjoying c35-40% market share each, and ETEX 20%-30%. Boral used to be the main player against which CSR competed; however, Knauf recently effectively bought Boral out of its local assets in 2021. Boral historically had a reputation as the competitor you didn't want in any market, as it leant heavily on price to chase market share during downturns. This weighs on returns for all players. We view the exit of Boral from plasterboard as a net positive for industry rationality. While plasterboard is undoubtedly a cyclical business, our discussion with industry participants suggests plasterboard is at the lower end of cyclicality - the plasterboard cost base is fairly variable as you can pull shifts off when demand declines, protecting EBIT margins. We believe EBIT margins vary by only a few percentage points through the cycle. The main driver of our assumption that CSR is unlikely to retest its prior EBIT margin lows is the improved industry structure in bricks. The Australian bricks market has gone from a three-player market to two after CSR bought Boral out of their joint venture in late 2016. A bricks business has a huge fixed-cost base; a brick kiln runs 24/7, so it's hard to pull costs out in a downturn. Conversations with industry participants suggested CSR's bricks business was breakeven at best during the prior housing downturn of 2010-2013. Management is also proactively managing the asset base to recycle unrequired brick sites into the property portfolio for alternative uses. For example, CSR were able to close a brick manufacturing site at Darra in Queensland and push the capacity through an upgrade at their NSW site in Oxley, freeing up the Darra land to be redeveloped and sold. We estimate Darra could generate over $100m in EBIT for the business over several years via the sale of subdivided land. This network optimisation reduces the risk that high-fixed-cost brick plants will swing to EBIT or cash loss-making at the bottom of the cycle. These improvements in industry structure lead us to an estimate of mid-cycle EBIT for building products of c$200m. (Note the building products business is on track for >$250m EBIT this year.) Deducting the full corporate costs of c$25m from this division gives mid-cycle group EBIT of $175m ex-aluminium. Property underpins 65% of market capitalisationCSR's property division looks to maximise financial returns of surplus former manufacturing sites and industrial land. The bulk of the value of this division was a 'gift from the gods': in what was surely one of the most sizeable value transfers in recent Australian corporate history, CSR was able to acquire Boral's 40% interest in its brick JV for $126m in 2016. Extraordinarily, this included 12 manufacturing operations and mothballed sites, including the aforementioned Darra site, as well as 140ha of developable land at Badgerys Creek in Western Sydney. This is valuable land, located on the southern boundary of the future Western Sydney Airport. CSR recently sold a small parcel of this land at $4.5m/ha, implying the remaining site could be worth >$600m. Cheers, Boral! This episode is another reminder of why we put a huge emphasis on the quality of a management team. It's not always around the value creation they can achieve, but also avoiding the significant value destruction that can occur if a business is poorly run. CSR have had their total "as is" property book independently valued at $1.5bn ($1.1bn for 450ha of Western Sydney property, and $400m for additional freehold properties), which compares to a market capitalisation of $2.3bn. While this value will be realised over the long term via redevelopment and sale of surplus land, this implies a residual value for the business of c$800m, which is cheap when set against our estimate of mid-cycle EBIT of $175m (4.5x EBIT). We note peer Fletcher Building currently trades on just under 8x arguably peak-cycle EBIT. This also ignores any earnings from aluminium. To us, CSR is not a particularly high-quality business, and the cycle is clearly unsupportive from here. However, we believe there has been an improvement in the quality of the business as a result of favourable industry consolidation, and see compelling value in the combination of OK assets, solid property underpinning, and a net cash balance sheet that provides optionality through a downturn. Author: Emma Fisher, Portfolio Manager Funds operated by this manager: Important Information: Units in the fund(s) referred to herein are issued by Magellan Asset Management Limited (ABN 31 120 593 946, AFS Licence No. 304 301) trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks.. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

3 Feb 2023 - 2023 Global macro outlook: Ten predictions

|

2023 Global macro outlook: Ten predictions Nikko Asset Management December 2022 No single catch-phrase epitomises the 2023 global macro outlook, but here are ten predictions: 1. 2023 will be a year like no other. Investors should not rely heavily on traditional models of previous economic and financial market recoveries, especially ones that worked best since the mid-1990s, as we are entering a unique era; rather, they should maintain a somewhat cautious and balanced perspective, with targeted risk-taking in select countries, sectors and stocks, as described in our other 2023 outlook pieces. Indeed, active stock selection, in particular, will be more important than ever in 2023, so special attention is required in selecting managers who have excelled in the last several challenging years. 2. Re-balancing and China's positive pivots: China, after a hesitant start, will likely see much improved economic growth in 2023 while most of the rest of the world will be sluggish. Its recent surge in the financing of property development was a major pivot in policy that will greatly support economic growth, although the previous mania for purchasing property and the economy's reliance on such will continue to be diminished. This should help keep global commodity prices fairly stable. Also, the sudden pivot towards détente in foreign policy in mid-November has considerably brightened the 2023 global outlook. There will be, however, many challenges to this détente, and as it is not firmly rooted yet. Especially with the likely visit to Taiwan by the new US House Republican leadership and continued trade restrictions, there is a chance that any rapprochement may prove short-lived. Clearly, both "sides" will benefit from a respite in economic and political tensions. For its part, China will likely resume purchases of US Treasuries after major sales in 2022. It also desires a more stable backdrop as it addresses the weakness in its housing sector and parts of its financial markets, while also improving the troubling situation for ordinary citizens and local governments. Meanwhile, US and other countries' corporations, especially Apple, hope that their factories there can keep producing despite various restrictions, that China will remain an important client and that the entire global supply chain will continue healing. 3. COVID will remain a factor, especially China's citizens' fear of such. We have predicted that China would open up the country sooner than expected, though gradually and somewhat furtively, but such has been accelerated by the recent protests and the increasing weakness in the economy. While cases and casualties will likely rise, the government clearly wishes to promote economic growth now and springtime will likely witness a near full opening in China, especially after the National People's Congress in March. We expect that the fears of such there, and globally, will abate in healthy, sustainable fashion. 4. Central banks, excluding that of Japan, will keep rates high to hamper "second-round effects." These "effects" will be the key factor in how inflation evolves. Labour's wage demands, coupled with the strikes and harmful supply shocks usually affiliated with such, obviously stand out, but the perceived "pricing power" of corporations and landlords will also be key, and they all will be watching how determined central banks will be to maintain high rates given the increasing political pressure as economies weaken further. This is most true in Europe, where inflation is the highest in the developed world and where labour is very powerful, especially in key political, infrastructure and economic channels. The media is not widely covering the strike actions, so investors should often screen the news themselves for such. Conversely, countries with low labour demands should have an advantage, especially Japan and much of Asia excluding Korea. 5. Countries with too much concentration in the tech hardware sector may not flourish, as industry fundamentals will remain challenged, including the upcoming oversupply of semiconductors over the intermediate term as countries around the world rush to build their own fabs for national security and other reasons. Due to this, semiconductor production equipment manufacturers, however, should see improved orders after their recent cutbacks. 6. For overall global risk markets, one should expect neither "Doom and Gloom" ahead, nor a Goldilocks scenario. The US equity market is not cheap, so a strong rally seems unjustified from December levels, but most other countries are quite inexpensive and could perform reasonably well. Europe, however, is suffering from unique difficulties, so it may remain inexpensive. Within this backdrop, stock and sector selection will clearly be the most important key to achieve positive returns. 7. Avoiding Short-term scares; many macro-economic, corporate earnings and credit shocks likely lie ahead in the short-term, as the global economy descends further into a semi-stagflationary period in which former excesses are "cured;" however, this is part of the healing process in which the intermediate-term outlook is actually improving, so investors should not panic in the short-term. Indeed, as for corporate earning shocks, as long as such are not far below analysts' estimates, investors may forgive such, especially if the outlook remains positive. 8. The global crypto infrastructure and some other ultra-growth industries are likely to continue to encounter troubles. The recently exposed lack of due diligence by many institutional investors is shockingly disappointing, as were the attitudes and practices of many industry leaders. Partly because of this, most "growth at any price" companies and industries will now be heavily scrutinized by venture capitalists, public-market investors, banks and regulators. This is bound to expose other problems that could spread. Indeed, ultra-growth companies will likely need to show a clear path to profitability on a GAAP basis in order to entice funding; however, such companies definitely exist and should benefit as they will likely attract much more investor interest. 9. Geopolitics will continue to be a factor: the "Clash of Systems and Philosophy" will clearly continue, especially with Russia, Iran and China pursuing their own path. The Russia-Ukraine war will continue through 2023, but possibly in much less bloody way, so this may calm risk markets. One also needs to keep a careful eye on the Middle East, especially Iran, as tensions remain greatly elevated given its internal problems and an even more assertive new Israeli government. As mentioned above, it will be important to watch Taiwan as well. One hesitates to mention North Korea, as it is a perennial, unpredictable worry, but hopefully China will restrain it from its increasingly provocative actions so that both "sides" can reduce the tension. 10. Troublesome domestic politics will be important; fiscal stimulus globally is already greatly constrained due to fears of its inflationary effects and as interest expenses surge, but even the normal functioning of fiscal affairs may encounter significant turbulence. In the US, the Republican control of the House of Representatives is bound to cause major disputes in 2023 and if a financial market or economic accident somehow occurs, action will need to be taken. If it is not taken, much like the initial stages of the Global Financial Crisis, financial markets could revolt. House investigations of various political matters are also likely to cause great discord in 2023, as well. In Europe, political dissent beyond strikes is likely to be intense especially as energy subsidies wane due to the need for fiscal restraint. Asia, however, looks much calmer on the political front. ConclusionWe greatly hope that these comments, as well as the other outlook pieces, will prove useful to our investors and we are always willing to address their thoughts and questions. We could all use a bit of good luck in the year ahead after the tumult of the last few years. Author: John Vail, Chief Global Strategist Funds operated by this manager: Nikko AM ARK Global Disruptive Innovation Fund, Nikko AM Global Share Fund, Nikko AM New Asia Fund, Disclaimer Please note that much of the content which appears on this page is intended for the use of professional investors only. This material has been prepared by Nikko Asset Management Europe Ltd (NAM Europe) which is authorised and regulated in the United Kingdom by the FCA. This material is issued in Australia by Yara Capital Management Limited (formerly Nikko AM Limited) ABN 99 003 376 252, AFSL 237563. To the extent that any statement in this material constitutes general advice under Australian law, the advice is provided by Yarra Capital Management Limited. NAM Europe does not hold an AFS Licence. Effective 12 April 2021, Yarra Capital Management Limited became part of the Yarra Capital Management Group. The information contained in this material is of a general nature only and does not constitute personal advice, nor does it constitute an offer of any financial product. It is for the use of researchers, licensed financial advisers and their authorised representatives, and does not take into account the objectives, financial situation or needs of any individual. For this reason, you should, before acting on this material, consider the appropriateness of the material, having regard to your objectives, financial situation and needs. The information in this material has been prepared from what is considered to be reliable information, but the accuracy and integrity of the information is not guaranteed. Figures, charts, opinions and other data, including statistics, in this material are current as at the date of publication, unless stated otherwise. The graphs and figures contained in this material include either past or backdated data and make no promise of future investment returns. Past performance is not an indicator of future performance. Any economic or market forecasts are not guaranteed. Any references to particular securities or sectors are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities or sectors and no warranty or guarantee is provided. Portfolio holdings may not be representative of current or future investments. The securities discussed may not represent all of the portfolio's holdings and may represent only a small percentage of the strategy's portfolio holdings. Future portfolio holdings may not be profitable. Any mention of an investment decision is intended only to illustrate our investment approach or strategy and is not indicative of the performance of our strategy as a whole. Any such illustration is not necessarily representative of other investment decisions. Portfolio holdings may change by the time you receive this. Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold, or directly invest in the company or its securities. The information set out has been prepared in good faith and while Yarra Capital Management Limited and its related bodies corporate (together, the "Yarra Capital Management Group") reasonably believe the information and opinions to be current, accurate, or reasonably held at the time of publication, to the maximum extent permitted by law, the Yarra Capital Management Group: (a) makes no warranty as to the content's accuracy or reliability; and (b) accepts no liability for any direct or indirect loss or damage arising from any errors, omissions, or information that is not up to date. Yarra Capital Management. Copyright 2022. |

2 Feb 2023 - Is private debt ready for recession?

1 Feb 2023 - Did Amazon cancel Christmas?

|

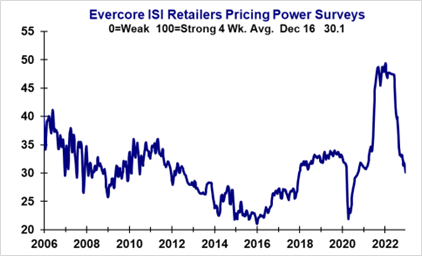

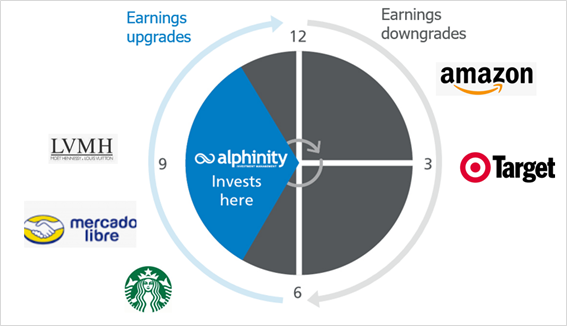

Did Amazon cancel Christmas? Alphinity Investment Management December 2022 Christmas fever was running high with beautifully decorated trees and colourful lights cheering us on every corner. The tone was however a lot less cheery when Amazon recently reported their 3Q22 results and downgraded their 4Q22 revenue guidance. Similar sentiments were reflected across a large range of consumer names noting pricing pressure and a lack of holiday shopping visibility. There is also clear evidence that inventories have been building across US retailers with supply chain constraints lifting and post covid "revenge spending" tapering off. We maintain our preference for companies with strong pricing power, exposure to the more resilient high-end consumer and companies with global reach that can also benefit from a China reopening. LVMH, MercadoLibre and Starbucks are three diverse consumer names that we believe can withstand a less cheery Festive Season. Why Amazon's revenue downgrade is a concernAmazon is a behemoth e-commerce platform with tentacles across most consumer channels and verticals. They have access to extensive supporting data that can paint a clear picture of the general consumer outlook. Historically we have seen Amazon downgrade earnings expectations, but this is the first time in many years that they've downgraded revenue expectations. The fourth quarter outlook is specifically prevalent given that it includes big spending days in the US, such as Black Friday, Cyber Monday, and Christmas. Amazon cited slowing consumer trends particularly in the US and Europe and a lack of holiday season visibility. Whilst there were several consumer companies that reported relatively good 3Q22 results, outlook statements echoed Amazon's concerns and remained cautious around peak season sales and beyond. Consumers are still nervous and hunting for bargainsSofter economic data points are now becoming more frequent following the flurry of central bank interest rate hikes year to date. The US composite PMI slipped to just 44.6 in December, US housing continues to cool down, layoffs are surging, and consumer sentiment remains at levels last seen in 2009 despite a recent recovery. US consumer spending has remained relatively resilient during 2022 as households continued to draw on excess savings accumulated during the pandemic. Post COVID pent up demand have been driving a revenge spending cycle focused on travel, leisure, occasion-based spending (for example weddings), beauty, entertainment and more. Recent data points however suggest a softening in these trends with consumer wallets facing more constraints (softer macro/inflationary pressures). According to Evercore ISI's December company surveys, current holiday sales remain focused on consumer staples products while discretionary category sales are slow, and consumers are focused on discounted goods. More broadly pricing power continues to soften across industries from elevated levels as global growth slows. Pricing power continues to soften across industries

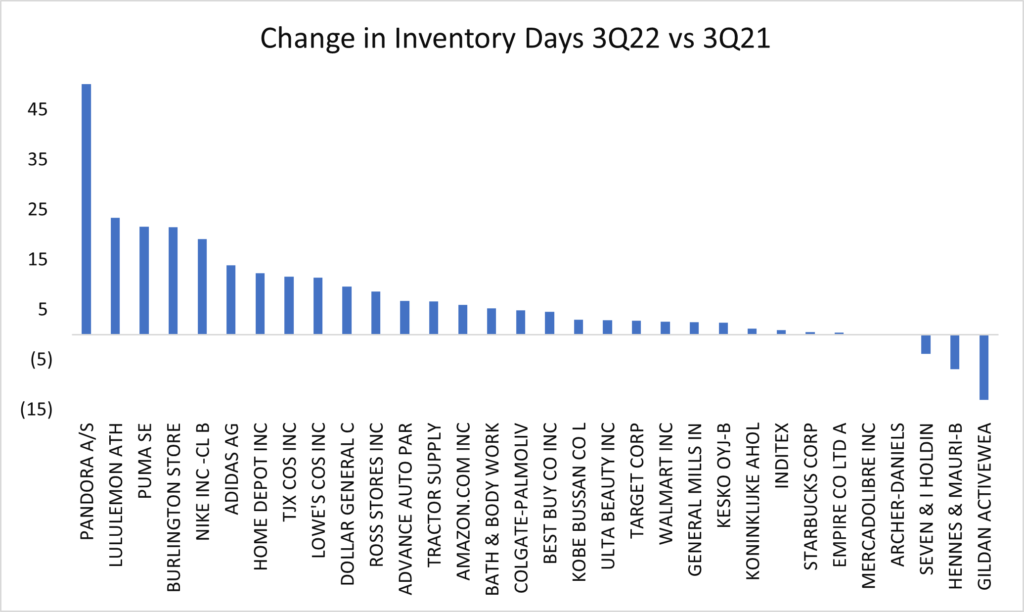

Source: Evercore ISI, December 2022 Signs of inventory build are intensifyingMany companies across a range of sectors reported higher inventory levels during the 3Q22 results season. A result of continued supply chain disruption improvement and softer demand. Target (US general merchandise discount store) and Nvidia (inventor of graphics processing units) were two examples of big bellwethers that guided to big inventory build, - adjustments, and/or write-offs. Our detailed analysis of inventory levels for a sample of 30 global consumer stocks across retailing, food, and apparel, suggest a sobering level of inventory build across the consumer landscape. We looked at the change in inventory as a % of sales and inventory days (average number of days a company holds its inventory before selling it) between the latest reported quarterly numbers (3Q22) and the same quarter last 2021 heading into the Festive Season (3Q21). The results showed that there are only 3 stocks with lower inventory days and only 5 stocks with lower inventory as a % of sales in our sample. There is specifically a clear inventory build in sportswear with Adidas, Puma, and Lululemon the worst offenders. For example, Adidas's inventory to sales is now almost 30% up from c17% at 3Q21 and Lululemon's inventory days are up from 126 days to 150 days (see chart below for the change in Inventory Days) over the same period. Increased inventories a concern across many consumer names

Source: Alphinity, Bloomberg, December 2022 Positioning in companies with strong inventory management and pricing powerAlphinity invests in quality companies that are in an earnings upgrade cycle that trade at a reasonable valuation. In our view, excellent inventory management skills and strong pricing power will be critical in determining the winners vs losers in the 2023 consumer race. Companies that can withstand margin pressures in an environment where business offload excess inventory and consumers hunt for bargains. Investing in quality companies at the right time in their earnings cycles

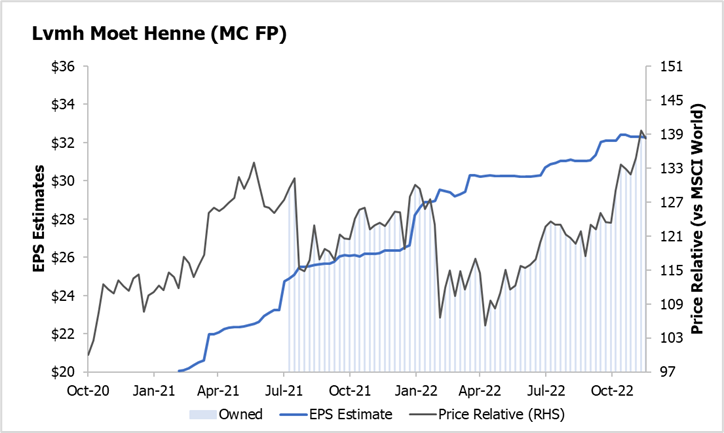

Source: Alphinity, December 2022. Note: Alphinity currently owns LVMH, MELI & SBUX, but not AMZN & TGT. Pricing power remains critical: LVMH, the world's largest luxury group, is currently our biggest position in our Global Equity Fund as we head into 2023. Demand for their luxury products have remained resilient despite slowing macro trends, with the company able to pass through inflation given their very price insensitive customer base. LVMH has been in an impressive earnings upgrade cycle since 2020, delivering earnings growth across sub-segments, brands and increasingly across geographies. Management also remains confident in a demand recovery in China once restrictions have lifted. Despite the relative strong performance of the last 12 months, the company still trades at an undemanding 22x 12-month forward Price to Earnings, which is at the bottom of its 5-year trading range (20-35x) LVMH - Strong pricing power & resilient demand drive an impressive earnings upgrade cycle

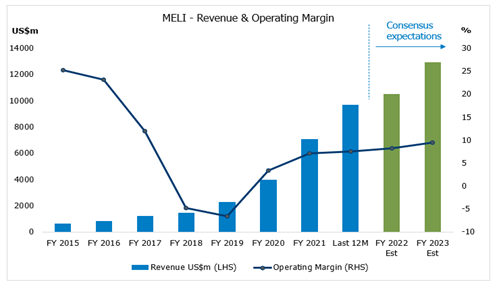

Source: Alphinity, Bloomberg, December 2022 The US consumer is not the global consumer. Certain emerging market countries, such as Brazil, are ahead in the business cycle vs major developed markets, where inflation, interest rates and unemployment are already past peak levels. MercadoLibre (MELI), is the largest e-commerce and fintech company in Latin America, with over 88 million subscribers and exposure across 15 countries. MELI has a unique eco-system model with their marketplace, payments, credit, logistics and other services all reinforcing each other, driving strong top line growth. MELI's reported very strong 3Q22 results well above their peer group, with accelerating sales growth and margin expansion reflective of their core strengths, including their broad category base, continued logistics improvements and a step change in marketing. Management noted they continue to "manage for growth and market share leadership" MELI consistently delivering strong Revenue growth and Operating margin expansion

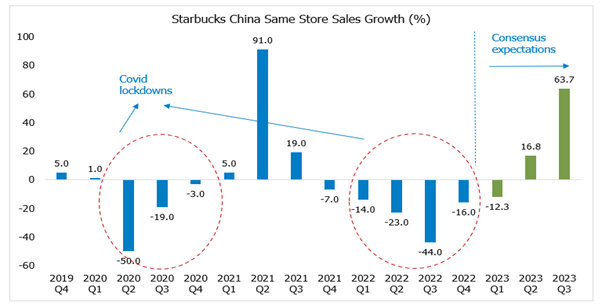

Source: Bloomberg, December 2022 China reopening will be an important earnings driver of 2023 earnings for multi-national companies: Starbucks (SBUX), is the leading specialty coffee retailer in the world, operating across more than 80 markets through company-operated and franchised stores. SBUX experienced a tough time during COVID, with many store closures resulting in a big drop off in sales and margins across all markets. Looking ahead, we expect their new strategy to drive a strong recovering in same store sales growth across their international markets and a return to profitability. SBUX is also well positioned to benefit from a China reopening, where they continued to open new stores during the pandemic (going from 4123 stores at the end of 2019 to 6000), that can return to profitability. China Same Store Sales Growth - Potential to rebound on reopening

Source: Bloomberg, December 2022 We will only know during the first quarter of 2023 if Amazon did indeed cancel Christmas and if general market jitters were justified. Regardless, good inventory management, strong pricing power and the right geographical exposures will remain critical elements for consumer companies as they navigate yet another tough macro year ahead. At Alphinity we will continue to do bottom-up analysis and global company visits to find the highest quality companies that have these attributes and can deliver higher than expected earnings. Author: Elfreda Jonker (Client Portfolio Manager) This information is for advisers & wholesale investors only. |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Sustainable Share Fund Disclaimer |

31 Jan 2023 - Global Matters: 2023 outlook

30 Jan 2023 - Equities 2023 - What's the bigger risk?

|

Equities 2023 - What's the bigger risk? Insync Fund Managers January 2023 Insync Funds Management CEO, Monik Kotecha, says there's no denying that 2022 was a difficult year for equities - but as one US commentator recently pointed out, years in which the S&P was down more than 18%, as it was in 2022, have been followed by years of 20% plus returns, every single time for the past 90 years. This, plus a few other key factors identified by Insync suggest that standing on the sidelines may pose a bigger risk than investing. Equities 2023 - What's the bigger risk? As we enter 2023, Insync Funds Management CEO, Monik Kotecha says standing on the sidelines may pose a bigger risk than investing. Everybody, and their mother, brother, sister, cousin, and uncle, is negative on the first half of 2023. Wealth destruction was the dominant theme of 2022. The global equity market shrank US$15 trillion in market capitalization, while global bond markets saw US$30 trillion in value wiped out. Virtually every asset class declined. Oil held up better, rising strongly in the first half but correcting as global growth expectations faltered, ending the year flat. The US dollar was the big winner, which rose 9% year-to-date. Cash, which was considered 'trash', gained 1.8%. High inflation, slowing growth and monetary tightening largely characterized the global economy throughout 2022. Rising inflation and slowing growth created stagflation concerns. But we think the market may surprise on the upside in 2023. The impact of 2022 There's no denying that 2022 was a difficult year for equities - but as US senior investment analyst, Luke Lango, from InvestorPlace recently pointed out, years in which the S&P was down more than 18%, as it was in 2022, have been followed by years of 20% plus returns, every single time for the past 90 years.

The sentiment at year-end was very negative, which is a good contrarian indicator. Typically, the average forecast from Wall Street's top strategists predicts the S&P 500 climbing by about 10%, which is in line with historical averages. This time around, the pros are unusually cautious, with most expecting the S&P to end 2023 lower. A Bank of America fund manager survey shows fund managers relative positioning of stocks versus bonds is the lowest level since 2009. Fund managers also hold the highest level of cash (5.9%) since the bursting of the technology bubble in 2000/01. The consensus view is that earnings have further to fall in 2023 and this remains a top investor concern. The market (buyside) tends to look out 6-12 months ahead of sell side analysts, and anticipates any earnings decline in advance of it actually happening. Earnings have historically bottomed after stocks bottomed. Since 1950, the trough in earnings growth lagged the bottom in the S&P 500 by about 6-7 months. Stock prices tend to inflect upwards before we see improvements in earnings, GDP, and employment. October 2022 may well have marked the lows in stock prices which has already discounted the fall in earnings ahead of sell side analysts. Looking ahead As we enter 2023, we think standing on the sidelines may pose a bigger risk than investing. Here's why. The US midterm elections The US midterm elections were held in November 2022. Historically, the S&P500 has outperformed the market in the 12-month period after a US midterm election with an average return of 16.3%, and not delivered a negative return during this period over the past 60 years. Inflation may still prove to be transitory Many argue that inflation will be much stickier than markets currently discount, and that it will take multiple years to restore price stability (2% inflation). However, we continue to believe that the outbreak of inflation is squarely the result of the pandemic shock. As the pandemic-related economic dislocation renormalizes and the Federal Reserve continues to tighten monetary policy, inflation may well eventually fall back to pre-pandemic norms. An area of additional concern, as a result of the pandemic, has been the reduction in the labour market participation rate. This has the potential to drive sustained increase in wages inflation and lower levels of productivity. We are today living in the golden age of technology and innovation which we continue to consider to be deflationary for two primary reasons: 1. Technology reduces the demand for labour, which puts downward pressure on wages and employment levels, which in turn reduces demand for goods and services because workers have less money to spend 2. Technological innovation also leads to automation, tools that make workers more efficient, and the elimination of some job roles So where are the opportunities? We have found that the long-term cash flows and valuation of companies exposed to megatrends do not change as a result of an increase in interest rates, or a slowdown in the global economy. Megatrends are unstoppable long-term growth trends with profitable industry structures. Here's just one example. The 60+ age cohort is set to more than double to 2.1 billion by 2050. This is what we call a demographics megatrend. The fastest ageing group within this cohort is those aged 70-75 and this is where we have identified prime investing opportunities. As the population ages, so does the incidence of chronic disease. Older people also often suffer from multiple chronic conditions at the same time. The second leading cause of death within those aged 70-75, after heart disease, is cancer. The demand for companies providing cancer drugs is not reduced by changes in interest rates, inflation, or recession. These factors also do not change the trajectory of ageing populations, nor the increasing demand for solutions for chronic diseases. Current volatile market conditions provide opportunities to invest in highly profitable businesses benefitting from megatrends at lower prices. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

27 Jan 2023 - The net-zero journey: creating a just transition for workers

|

The net-zero journey: creating a just transition for workers abrdn December 2022 A 'just transition' refers to the way the world transitions to low-carbon energy sources. It is a crucial part of the climate agenda. A just transition aims to minimise adverse impacts from the energy transition and to see everyone share its benefits - including workers, suppliers, communities and consumers. The journey to net zero will have uneven effects across industries and countries. One key aim of a just transition is to support vulnerable workers by creating green, high-quality jobs and helping equip workers with the skills necessary for achieving net zero. Net job impactsThe prevailing view is that the transition to a net-zero economy would lead to more job gains than job losses. According to McKinsey's calculation based on a net-zero 2050 scenario, the transition could create around 200 million jobs and displace around 185 million jobs. This could result in a net impact of around 15 million more jobs by 2050.1 These job gains include around 162 million jobs in operations and maintenance across different sectors of the economy, and around 41 million jobs associated with spending on physical assets needed for the net-zero transition by 2050. The International Labour Organisation (ILO) paints an even more positive picture, estimating that a net increase of 18 million jobs by 2030 is possible.2 What sectors and countries will be most affected?According to the ILO, most of the job creation that results from the energy transition will happen in construction, electrical machinery manufacturing, copper mining, renewable energy production, and biomass crop cultivation. Most of the job losses will occur in petroleum extraction and refinery, coal mining, and thermal coal. In addition, the shift to electric vehicles will require fewer workers for production, leading to net job losses - something that is already happening within the sector. The impact on jobs also varies by country, depending on its economic exposure to the net-zero transition. The transition would unevenly affect lower-income and fossil-fuel-producing countries, such as Pakistan, India, Bangladesh, Kenya, Nigeria and Indonesia. How companies manage the impacts of the transition on their workforce will pose considerable investment risks and opportunities for investors These tend to be countries with a relatively higher proportion of jobs, gross domestic product and capital stock in sectors that are more exposed to the transition - that is, sectors with emission-intensive operations, products and supply chains. Significant fossil-fuel resource production also creates high exposure for some countries, such as Qatar, Russia and Saudi Arabia. Investment implicationsHow companies manage the impacts of the transition on their workforce will pose considerable investment risks and opportunities for investors. There are two types of risks facing companies within the sectors that are most exposed to the energy transition: restructuring risks and human-capital risks. Firstly, when it comes to restructuring risks, the most obvious of these is operational disruption caused by mass redundancies. This can lead to costly pay-outs and challenging labour relations. Research shows that the top performers with higher restructuring management practices tend to be concentrated in Europe. This is also the case for companies within the fossil-fuel and emission-intensive sectors, which indicates that European companies are relatively more prepared for a just transition. Secondly, human-capital risks mainly manifest as skills mismatches and shortages, which can impede a company's progress on the green transition. According to the International Energy Agency (IEA), the energy sector already faces difficulty hiring qualified talent to keep pace with the growth in clean energy. If solar and wind installations reach four times today's annual level by 2030, as called for in the IEA's net-zero scenario, these labour constraints could impede the world's ability to accelerate the shift to a low-carbon future.3 According to the ILO's survey, while most countries have environmental policies, there are only a handful of countries with corresponding policies at either the national or the regional level for skills development. These are Denmark, Estonia, France, Germany, the UK, the US, China, India, South Korea, the Philippines and South Africa. Similarly, few countries have incorporated skills for the green transition into the formal vocational training curriculum.4 Companies also have an important role to play in identifying and anticipating skills, and in providing access to jobs and training for the green transition. In practice, this can be done in partnership with the government and educational organisations. Investors need to understand how these risks are being managed. For example, through our own extensive engagement with auto makers, we have learned that the industry is managing these risks through early retirement schemes, upskilling of the existing workforce, and proactive engagement with trade unions. In general, to understand how companies are managing these risks, investors can focus on four key indicators:

ConclusionThe energy transition will have a significant impact on employment. It will lead to the creation and displacement of millions of jobs. While the overall net impact is likely to be positive, the projected job gains will concentrate in sectors like renewable energy, electrical machinery and construction. From a geographical perspective, a higher level of disruption to the labour market is expected in developing countries that rely heavily on fossil-fuel and emission-intensive sectors. How companies and governments manage these impacts will present risks and opportunities for investors. Our ongoing research and engagement aim to understand the social impacts and potential risks to our investments from the energy transition. Our research in this area is expected to expand and grow in the future, in conjunction with our ongoing climate change, human rights, and labour and employment work. For example, building on our focus on workers in the energy transition, we will also consider the perspectives of communities and consumers, in order to integrate further insights into our investment process. Author: Ziggy You, Sustainability Analyst and Elizabeth Chiwashenga, Senior Sustainability Analyst |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund , Aberdeen Standard Life Absolute Return Global Bond Strategies Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund 1. The net-zero transition: Its cost and benefits | Sustainability | McKinsey & Company |

25 Jan 2023 - Cashflow pothole in energy transition journey

|

Cashflow pothole in energy transition journey Yarra Capital Management December 2022

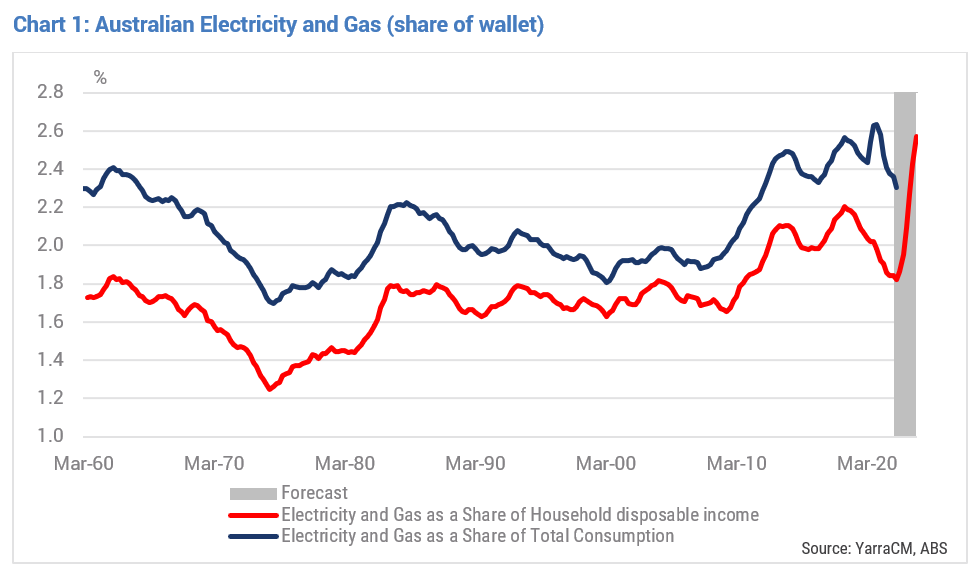

By now, people whose eyes don't immediately glaze over once discussions of personal or national budget are broached are well aware of an upcoming spike in their electricity and gas bills. However, for the majority of the Australian citizenry the 'sticker shock' from the increase in utility bills will still be felt in real time. Tim Toohey, Head of Macro and Strategy, details why for many Australians this will merely compound an already dire cashflow situation. For context, the Australian Treasury has assumed that electricity prices will rise 20% (y/y) by late 2022 and a further 30% in 2022-23. This will take utilities to an unprecedented share of wallet in 2023, some 2.6% of household income by Dec 2023 (refer Chart 1). While that may not sound like a particularly scary figure, it's 25% above the 10-year average and 49% above the long run average dating back to 1960. It will also represent the biggest one year rise in utility bills in the post-War period. The cause for the spike has been well documented. A surge in global coal and energy prices in reflex to the invasion of the Ukraine was the dominate force, some unfortunate timing of coal-fired power station maintenance and some less than transparent behaviour by market participants all played a role. Yet the cause of the trend rise in utility costs is less well understood at the household level; the rapid transition to renewables is unravelling the economics of running coal and gas-fired generation at an even more rapid rate.

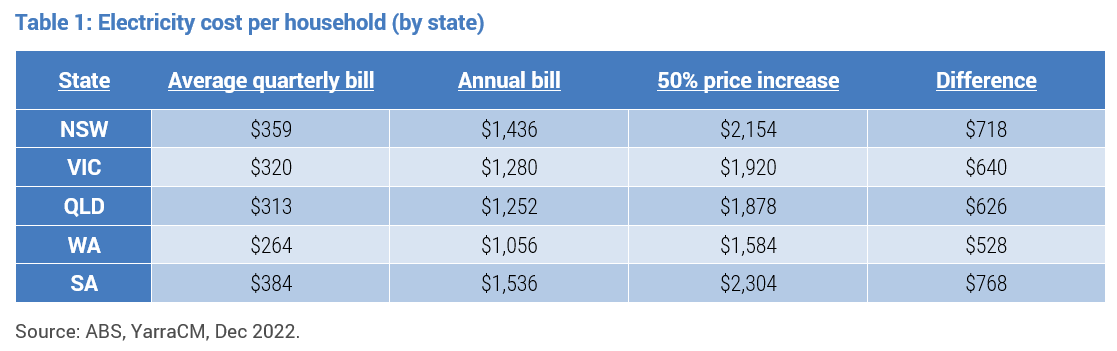

This is not to say that decarbonising the grid in an expeditious manner is not necessary or desirable. It merely means that the cost of the transition will be felt well beyond well-heeled investors asked to dig deep into their pockets to finance the capital cost of the transition. Indeed, it is the consumer that will invariably be forced to pay for the potholes in the road to decarbonisation as firms seek to recover the cashflow hit from declining economics of traditional generation via higher power bills. Utility companies know this. Politicians should know this. Households largely have no idea that they are ultimately on the hook if best intentions of a smooth energy transition turn to custard somewhere along the journey. To overwork the analogy, we have barely gotten the car out of the driveway with a long journey ahead to a known destination but without a clear map of how to get there. We don't have enough cash in our wallet to complete the journey, some of the roads have not yet been built, and the kids who have been fighting politically for years before getting in the car are continuing to do battle in the backseat. For those of us scarred from family car trip holidays at this time of year, we are collectively at the point where optimism and excitement at the start of a trip are about to be overwhelmed by the reality of a long-haul car trip in the Australian heat. The feeling of sizzling hot car seats, the taste of Aerogard inadvertently sprayed into a protesting mouth and the injustice as youthful back seat rebellion is brutally supressed by the front seat elites. Yes, it's going to be a long and painful journey. But to get a sense of who will bear more of the cost, we can look at the average quarterly electricity bill across different dimensions.

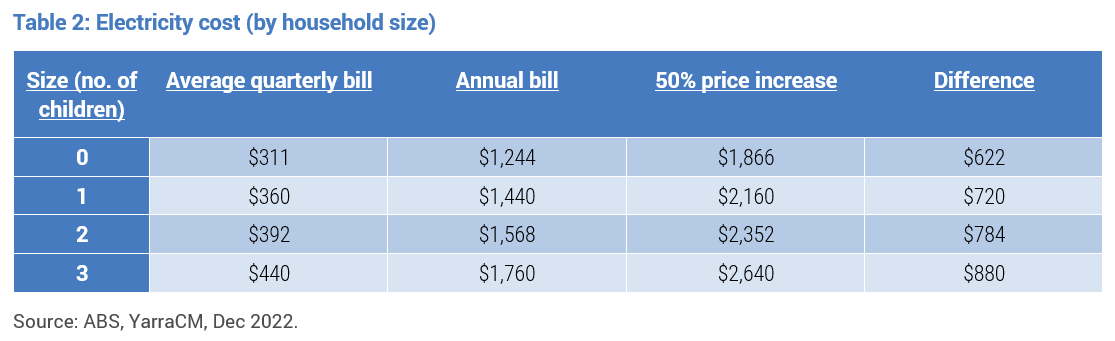

By household size (refer Table 2), the more children you have the greater the power bill increase (and the more time the parent spends wandering around the house turning off lights left on by their children).

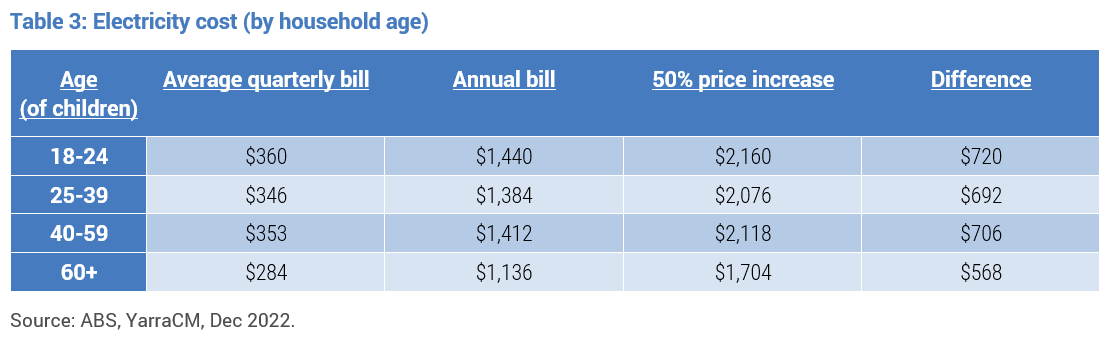

By age, it's the young that will feel the pain more acutely (refer Table 3). Indeed, Gen Z (18-24yo) power bills will swamp the bills of Baby boomers (60+) by $150 p.a. Yes, despite the moral superiority of youth, it seems it takes more power to fuel video gaming sessions in the wee hours and to charge the armoury of devices required to keep your social media presence tip top!

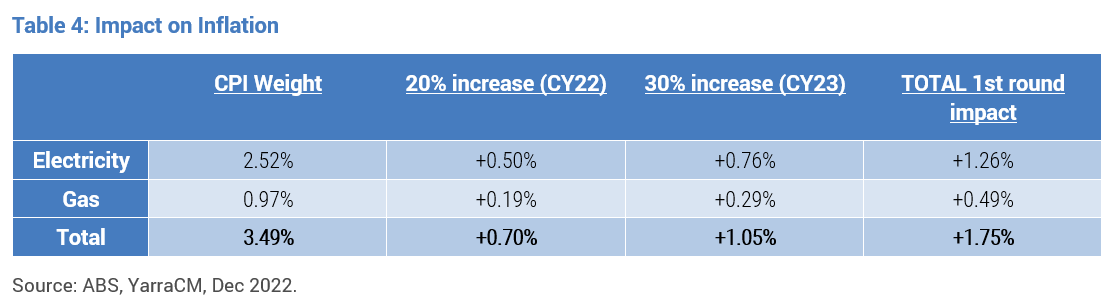

From the perspective of a top-down economist, the addition increment to inflation from rising power and gas bills could add 1.75% to inflation by the end of 2023 in first round impacts and potentially a further 0.35% in second round effects (Refer Table 4). That's a lot, but that's an average estimate. From the perspective of young households with multiple children living in the Eastern States, the impact will be larger and more painful.

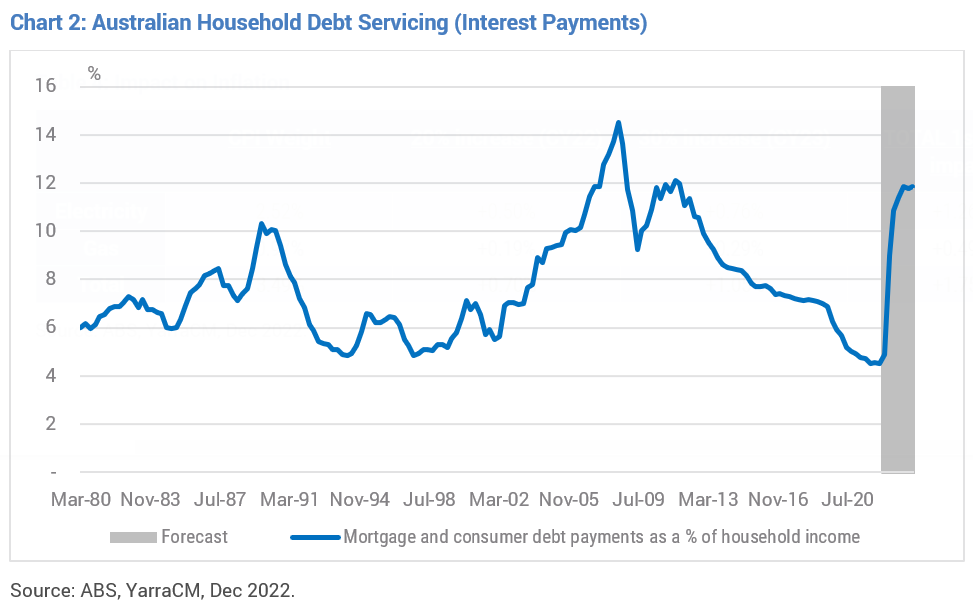

Worst still, this is the slice of the population that are most at risk of rising education, health, insurance and housing costs. We all know that the interest payments on the stock of existing total household debt are set to rise incredibly sharply in 2023, compounded by the roll off of fixed rate mortgages (refer Chart 2).

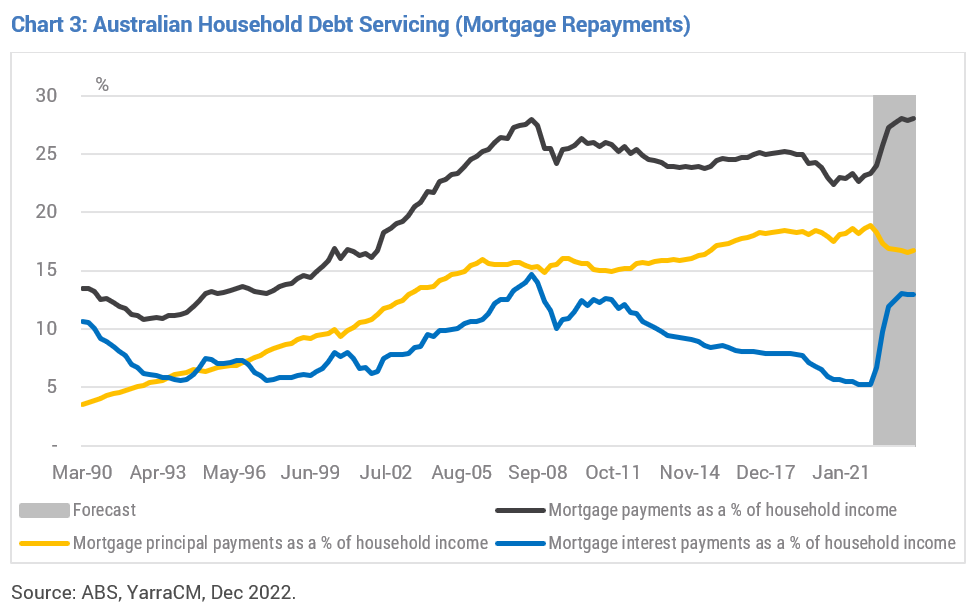

In conjunction with principal payments, debt servicing for the average household is set to breach the prior record during 2023 (refer Chart 3). Again, this is for the average household. The situation for young mortgaged households is far more dire, not to mention a rising proportion of the recent new homeowners who are now entering negative equity scenarios for their homes.

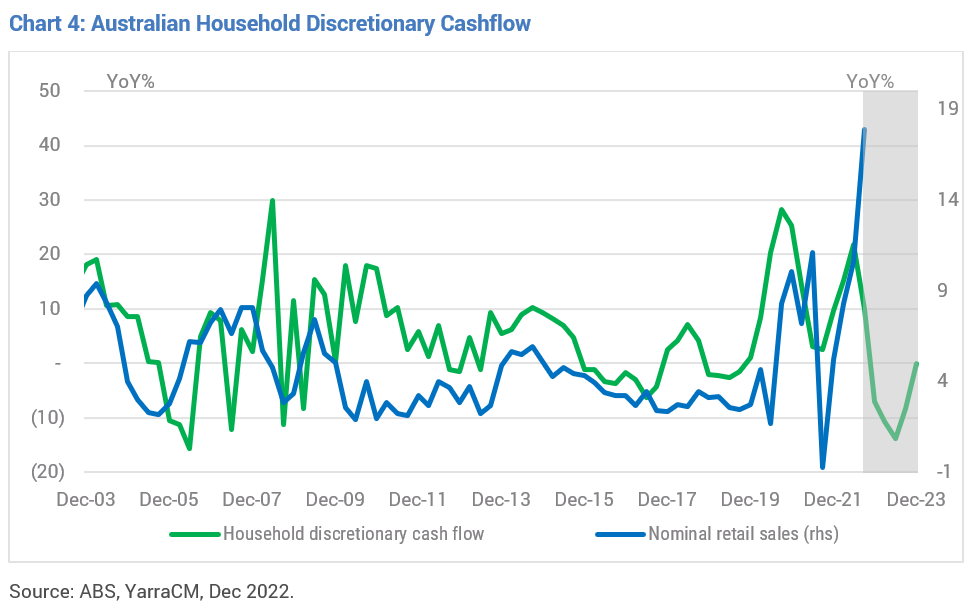

This will place an enormous impost on a large section of society. Nobody likes having their discretionary income squeezed and nobody likes an unexpected spike in their gearing ratio via falling asset prices. Even if we assume the ongoing robust growth in wages and employment in 2023 the impost of higher interest costs, utility costs, insurance costs and rents will be sufficient to see average discretionary cashflow fall by 15% by mid-2023 (refer Chart 4), and much more for young households with large families and large mortgages.

Given, retail sales growth normally closely tracks our measure of discretionary cashflow, we expect that retail sales will slow from the rapid rate of close to 20%(y/y) to zero growth by mid-2023. Note, this is likely the best-case scenario. It could easily be worse if sub-trend economic growth reveals labour market weakness with a lag, as observable in all prior downturns. The argument that Australians have accumulated 'buffers' via $260bn in 'excess savings' since the pandemic and via pre-payments on mortgages will exceed additional interest payments - for most borrowers at least - is illusionary. While this might be true in an accounting sense, the RBA is likely asking itself the wrong question. It is not a question of how big a 'buffer' is before tightening policy will hurt, it is why did households accumulate such a buffer in the first place? And is the economic outlook improving or deteriorating? Excess fiscal stimulus obviously contributed to the initial saving spike, but what if the ongoing accumulation of savings was more about de-risking asset exposure in an uncertain time or because a large cohort of the population is simultaneously entering retirement (COVID may have expedited this decision for many Baby Boomers). If this is the case, then the 'excess saving' is not suggestive that a consumption boom lies ahead that threatens future inflation. Quite the opposite: in times of rising economic uncertainty households tend to initially lift their saving rate. They do not decrease it. There has been ongoing debate whether the government has a role to play in capping utility costs. And, if so, whether that should be at the company level or the consumer level. Given the recent history of firms profiteering through the crisis by lifting prices rather than absorbing margin pressure and the impending cashflow hit for households, the answer should be obvious. More importantly, if the government wants to keep everyone in the car playing nicely during the initial phase of the energy transition, then the answer is very much yes: utility costs need to be controlled. Let's just hope that there are enough fiscal resources and goodwill to get us to that new energy destination as quickly and efficiently as possible. Author: Tim Toohey, Head of Macro and Strategy |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |