News

20 Mar 2023 - Experiences Rule!

|

Experiences Rule! Insync Fund Managers February 2023 The Experience Megatrend, of which travel is a component, is one of 16 in our portfolio. Borders have reopened and travel is at full throttle. Growth rates in this industry are through the roof as the industry powers ahead from the COVID-19 pandemic. An individual's desire to travel is hardwired into human DNA. The rapid speed with which the recovery is occurring can be seen from the chart on the right; this is before China's reopening has its likely large impact.

Whilst airlines and cruise ships may be the more obvious ways to invest in this megatrend, they come with high levels of financial and operational risk. Companies like Qantas have had to raise capital every time there is a crisis. Their long-term performance has never reached our minimum quality hurdles. Our work has identified online travel agents are best positioned to deliver some of the highest and most consistent levels of profitability in this megatrend. No capital raisings were required, despite the shutdown in travel because of their exceptionally strong balance sheets. As we move into an environment where the use of digital apps to efficiently build travel itineraries accelerates (including researching, booking, and paying), investing in online travel agents should provide one of the highest quality ways to participate in the resurgence and secular growth in travel. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

17 Mar 2023 - Stock Story: Walmart

|

Stock Story: Walmart Magellan Asset Management January 2023 |

|

Sam Walton opened the first Walmart discount store in 1962, in the small Midwestern town of Rogers, Arkansas (population just 5,700 at the time). From these humble beginnings, Walmart grew into a retailing giant that today serves hundreds of millions of customers each week in its >10,500 stores across 24 countries. In financial year 2022, Walmart generated more than $572 billion in sales of groceries and other merchandise, making it the world's largest retailer. At year-end 2022, the company employed a total of 2.3 million people, making it the world's largest private employer as well. So how were such success and scale achieved? Over the past 60 years Walmart has followed a consistent strategy of providing the lowest possible price (Every Day Low Prices, or EDLP) for a broad assortment of products. Despite its somewhat staid reputation, Walmart has been an early adopter of new technologies and has a history of innovation. It was a pioneer of bar code scanning and analysing sales information, and in the mid-1980s it launched its own satellite network to stay in touch with its growing distribution and store network. Over time, the company has built a wide economic moat derived from scale-based efficiencies and capabilities, a persistent focus on frugality and customer value, and a strong brand that communicates this focus. One of Walmart's key competitive advantages is its unrivalled scale. As one of the largest retailers in the world, the company has significant purchasing power, which allows it to negotiate lower prices from suppliers. This in turn allows Walmart to offer lower prices to customers, driving higher sales (with volumes more than compensating for lower prices) and further increasing its competitive advantage. Additionally, Walmart's size allows it to invest heavily in technology and infrastructure, which further helps to improve efficiency and reduce costs. Another key element of Walmart's moat is its strong brand recognition and reputation. The company is known for its low prices and wide selection of products, which has helped it to attract and retain a large customer base. In recent years, Walmart has also focused on expanding its e-commerce capabilities. The company has invested heavily in its online offering and in-store pickup/ delivery, and today, Walmart.com is a major player in the online retail space. This has helped Walmart stay competitive in the face of growing competition from online-only retailers like Amazon. Despite its success, Walmart has faced criticism over the years. One concern is the company's impact on small businesses and local communities. Some critics argue that Walmart's expansion has led to the closure of small, locally owned stores, hurting the local economy. However, Walmart has also made efforts to be a positive force in the communities where it operates. The company has a long history of philanthropy and has donated billions of dollars to charitable causes around the world. Walmart has also implemented a number of initiatives to reduce its environmental impact, including reducing greenhouse gas emissions and increasing the use of renewable energy. One example of Walmart's commitment to sustainability is the company's Project Gigaton. Launched in 2017, this initiative aims to reduce one billion metric tons of greenhouse gas emissions from the company's supply chain by 2030. For comparison, that is as much as the US Government's Inflation Reduction Act aims to cut by the same date. To achieve this goal, Walmart is working with suppliers, NGOs and other partners to identify and implement sustainable practices throughout the supply chain. About 4,500 suppliers accounting for more than 70% of Walmart's sales have signed up, making it the largest private sector initiative of its kind. In addition to environmental sustainability, Walmart has focused on social sustainability. The company has a number of initiatives in place to promote diversity and inclusion at the employee and supplier levels, and it takes a leading role working with NGOs to promote ethical recruitment and working practices throughout its supply chain. Overall, Walmart's business history has been one of steady growth and innovation. The company's competitive advantages, including its vast scale, consistent strategy and strong brand, have allowed it to become one of the biggest retailers in the world. And while Walmart has faced criticism in the past, it has also made significant efforts to be a positive force in the world through initiatives focused on sustainability and social responsibility. Sources: Walmart Annual Report 2022, company filings. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. A copy of the relevant PDS relating to a Magellan financial product or service may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to be implemented and its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

16 Mar 2023 - Thoughts on the BOJ you might not have heard, but should consider

|

Thoughts on the BOJ you might not have heard, but should consider Nikko Asset Management February 2023 Firstly, due to its importance, although few seem to be discussing it in the heat of the moment, Japan's inflation outlook, like the rest of the world, should greatly improve in the coming quarters, with consensus expecting January's headline CPI announced this week, or February's, likely to be the peak in year-on-year (YoY) terms, and then drop below 2% in the 3Q and to 1.4% in the 4Q. This would put, unlike in the US or Eurozone, inflation back below Japan's target, and, thus, will greatly relieve pressure on the new leadership at the BOJ and the Government overall. Also noteworthy is that Japan's western-style core CPI, which also excludes all food items, is only around 2% YoY now. No consensus forecasts are available for this latter figure, but it certainly seems that it should be significantly lower later this year. Also crucially important to this topic is that Japan is likely the least inflationary country in the world, with workers hardly ever striking and rarely changing jobs for higher salary. Like current Governor Haruhiko Kuroda's stance, many in the BOJ will want to see more than just one round of substantial wage hikes before believing a virtuous cycle of disinflationary growth is sustainable. Indeed, many large companies are preferring to give special inflation bonuses rather than permanent, major wage hikes. Meanwhile, many SMEs apparently are not able to pay much more at all to labour this year, although minimum wage rates are rising. Furthermore, clearly Japan's GDP has been sluggish for decades and partly due to demographics, should not greatly excel after a quarter or two of acceleration due to increased tourism. Indeed, Japanese consumers currently are far from optimistic and have curtailed spending recently due to high inflation, with it likely requiring a sustained period of lower inflation before they become comfortable with spending more fully. It is important to note the BOJ's historical context, as tightening just before recessions has been the bane of several BOJ Governors in the past, with 20/20- hindsight critics lambasting such as "mistakes". Indeed, Kuroda would very likely have been right in rejecting a broadening the YCC band, given the fact that China's economy was weakening under the zero-COVID Policy, and that the G-7 looked likely to enter recession, not to mention war uncertainties, but Xi Jinping's pivot to re-open and accelerate the economy, coupled with the resilience of the G-7 economies, forced a change in the BOJ's outlook, so it took action in December to broaden the band. Clearly, the damage to many households and the government deficit would be quite large if official policy rate rises. The former have a very large portion of mortgages on a variable rate, and the monthly payments on such would greatly increase, thus harming the economy. Meanwhile, the Ministry of Finance (MOF) likely viewed the US Congressional Bureau Office's new fiscal budget projections on interest expenses with great concern given Japan's high debt to GDP ratio. No one except some wolfish hedge funds, wants Japan to experience a crisis, as such would likely have very negative global implications, with Japan likely selling large amounts of US Treasuries and other bonds, even after last year's major sales, to bolster its domestic markets. Lastly in this regard, it bears noting that fears of a JGB crisis have existed for two decades, but Japan's economic circumstances and domestic considerations have long confounded the JGB sceptics. New BOJ leadership and team effortThe process for choosing the BOJ's leadership was confusing, as political developments in Japan often are, but optimists are calling the result a "dream team" and the nominees are all certainly highly qualified and capable. Shinichi Uchida, the Deputy Governor nominee basically in charge of internally-sourced advice and implementation of monetary policy, was an architect of the YCC policy and the negative interest rate policy (NIRP) as a senior BOJ Director since 2012. He will be a source of tremendous knowledge of the benefits and difficulties of both these and other policies, such that no BOJ decisions will be erroneously based and each will be implemented effectively. Ryozo Himino, the other Deputy Governor nominee, most recently headed MOF's Financial Services Bureau and held leadership posts there in its international division from 2016. He also was secretary-general of the Basel Committee on Banking Supervision and chaired the Financial Stability Board's Standing Committee on Supervisory and Regulatory Cooperation, which are amongst the highest posts in the international financial system. Thus, he is well known and respected domestically and internationally, and should easily be able to deal with all financial sector developments. Rather quiet and professorial, Governor-nominee Kazuo Ueda is greatly respected domestically, and given his academic credentials, a PhD under Stanley Fischer at MIT and a Tokyo University professor for many of the top BOJ and MOF staff over several decades, as well as serving on the BOJ board for seven years two decades ago, he should quickly garner international respect. Indeed, his academic qualifications are more robust than most G-7 central bankers. In public, he is likely to be somewhat arcane and highly technical in his explanations, a bit like Alan Greenspan was, when faced with questions in the Diet and by reporters. Press conferences might be rather short, not abounding in new information and somewhat inconclusive, partly due to his style but also because the BOJ and everyone else is waiting to see how this unique global situation develops in the next few months before making any momentous decisions. In the meantime, economists have been perusing Ueda's past comments and most of such have been quite dovish during the last few decades, but he has shown greater concern than Kuroda regarding the market distortions caused by some BOJ policies. However, once taking the mantle of responsibility, leaders often do not follow their ideals so strictly, especially when faced with a complex and critically important situation. This is especially applicable given that he is often called much more of a pragmatist than an ideologue, which should also affect the style and speed of policy. Lastly in this regard, the BOJ's future will be a team effort, including the Deputy Governors, the rest of the policy board and inputs from the public and private sector, so one should not place too much importance or criticism on one person. All central bank leaders rely heavily upon their professional staff, and success is never easy, especially in today's circumstances, so one should consider the capability of the entire team, which in Japan's case, seems very strong, well-balanced and likely very well coordinated. OutlookCurrently, there is a wide variety of predictions for the BOJ's actions, with some expecting imminent hawkish decisions based upon some of Ueda's "anti-distortion" comments, but changes are more likely to be gradual and tentative assuming the global economy continues improving. However, if the global economy actually remains very sluggish, coupled with declining inflation, the BOJ may not need to change much at all. If there are any changes, it may first tinker with NIRP to make it less burdensome to the few institutions that are affected by it. This would conform with Ueda's desire to remove market distortions and also with the global trend away from negative rates. Further broadening the YCC band is possible this year, but not assured. Meanwhile, it doesn't seem that just shifting the target to 5-years from 10-years conforms with Ueda's "anti-distortion" preference. ConclusionInvestors can be patient regarding predictions of the BOJ's actions over the coming months, while also analysing how the global economy transpires as a major factor in its deliberations. They can have confidence that skilled persons lead the effort and that Japan's circumstances will lead to substantially lower inflation, and, thus, reduced worries about BOJ policy and Japan's financial markets. Author: John Vail, Chief Global Strategist Funds operated by this manager: Nikko AM ARK Global Disruptive Innovation Fund, Nikko AM Global Share Fund, Nikko AM New Asia Fund, Important disclaimer information |

15 Mar 2023 - 2023 Outlook for Emerging Markets

|

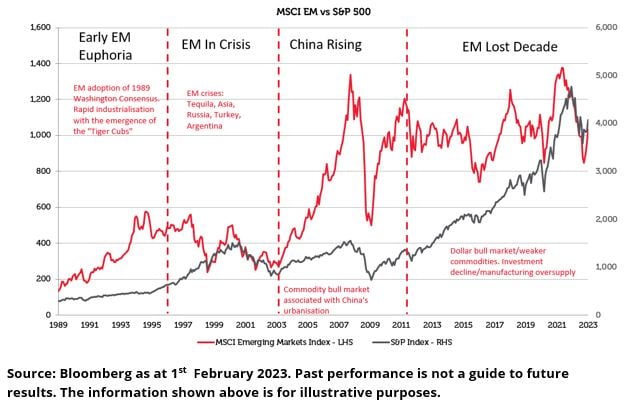

2023 Outlook for Emerging Markets Redwheel (Channel Capital) February 2023 Emerging Markets faced three main headwinds in 2022, namely, China's zero Covid-19 policy, aggressive monetary policy tightening globally and the Russian invasion of Ukraine. We see two out of those three factors turning into potential tailwinds in 2023. Firstly, China has already started to reopen its economy; therefore, the main question is the impact on the rest of the world. Secondly, we see the Fed pausing hikes at some time in H1 2023 and potentially pivoting to rate cuts in Q4 2023, which could lead to a weaker US dollar. The combination of a dovish Fed and the reopening of China's economy creates a favourable backdrop for Emerging Market (EM) equities to outperform. Additionally, there are other factors that we think will contribute to the outperformance of EM in 2023:

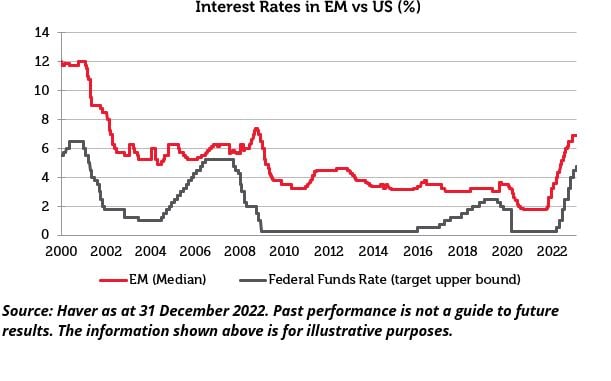

Looking at the 8 factors in more detail: 1) A dovish Fed - As discussed, we believe the Fed will pause rate hikes and then begin to cut rates later this year. Moderating US rates should take the pressure off EM central banks, which have already tightened significantly, remaining ahead of the curve. So far, the only emerging economy central bank with an easing bias is China. Looking forward, we anticipate that countries such as Brazil should also cut rates in 2023.

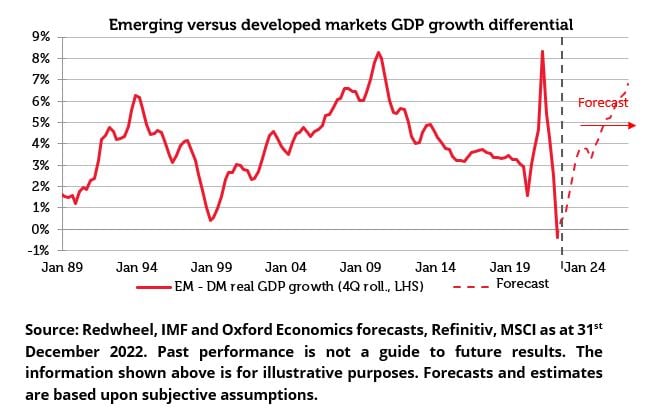

2) A Relaxation in China's Covid-19 policy - China is the world's second-largest economy and accounts for over one-third of global growth.[1] The prospect of a China reopening is a key catalyst for many EM economies and stock markets in 2023.[2] We anticipate that China's re-opening will benefit companies across our investment universe. For example, Chinese travel spending was ~$100bn in 2022 but as Covid mobility restrictions are removed, we anticipate this figure could return to pre-Covid levels of ~$250bn in 2023. This spending should impact travel-related companies in China, as well as companies in other countries that are beneficiaries of Chinese tourism, such as Indonesia and Thailand. A faster than expected removal of Covid restrictions continues to support growth sentiment and a rotation back into stocks relying on Chinese consumption and supply chains, as well as having a significant effect on the commodity market. 3) Accelerating emerging vs developed real GDP growth differential - We believe that economic growth is likely to increase in EM during 2023, bolstered by China and LatAm. In contrast, we think Developed Markets (DM) GDP growth is expected to decline close to zero. As a result, the growth differential between EM and DM could widen in 2023 and 2024. This sets a strong backdrop for EM asset prices.

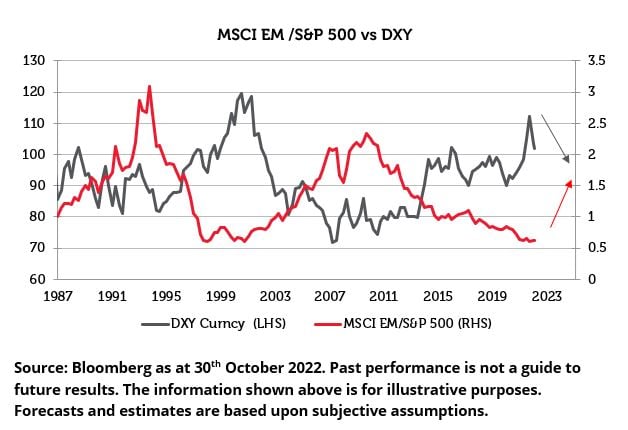

4) Emerging markets will likely benefit from a dollar bear market or a period of dollar weakness - The interest rate differential moved in favour of US dollar-denominated assets as the Fed raised policy rates more rapidly than its developed market counterparts. On the other hand, China continued to ease monetary policy. The flow of capital to the US accelerated when the Fed signalled an even tighter monetary policy than the markets were expecting in March 2022. - Going forward, we expect that the Fed's hawkishness will fade with decelerating inflation in the US due to the lagged effects of monetary tightening. As the Fed begins to become less hawkish and the ECB continues playing catch up on tightening, the interest rate differential should gradually lead to a rotation away from US dollar-denominated assets. This historically has led to EM outperforming the S&P (as seen below).

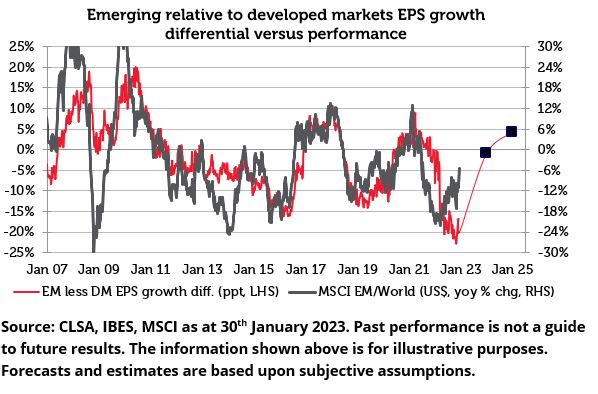

5) Stronger relative emerging market EPS growth - EM earnings expectations have already been revised to prudent levels. Looking ahead, we anticipate that the lower base should lead to increased growth of corporate earnings within EM. Additionally, there should be more price stability and a chance for favourable market surprises.

6) Evidence of investor capitulation - After the longest market drawdown in history, investor positioning in EM equities is light. Over the past 13 years, the pace of foreign net selling was only swifter in 2009 and 2020.[3] As news flow surrounding China becomes incrementally more positive, we believe we are at a turning point in investor sentiment towards emerging markets. 7) Favourable valuation dynamics - Emerging equities are trading on 10.5x P/E ratio, cheaper than the 10-year average of 11.7x. In contrast, US equities trade on a multiple of 29.1x. As a result, current valuations appear attractive in comparison to other markets and in our view offer a great buying opportunity for long-term investors.

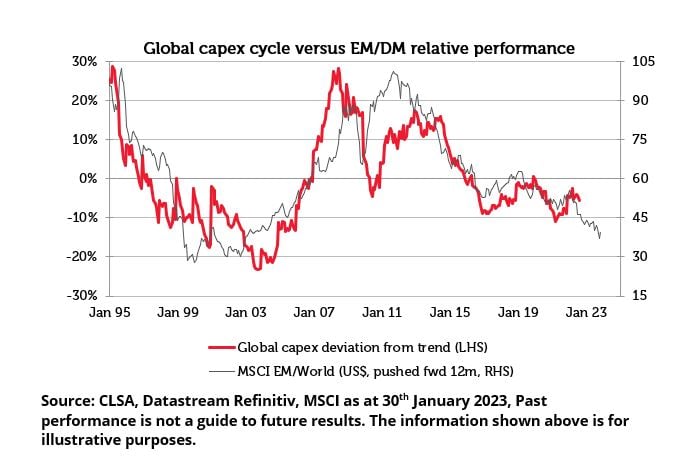

8) A global capex recovery post years of structural disinvestment - Corporates are recording an early stage—almost involuntary—uptick in investment as the capex depreciation ratio dipped to a record low in 2021. Indeed, for developed equities the ratio fell below parity for 18 months, indicative of depreciating assets not being fully replaced. - Emerging Markets relative outperformance has historically been a function of the global capex cycle given that the sector composition is heavily skewed towards capex plays.

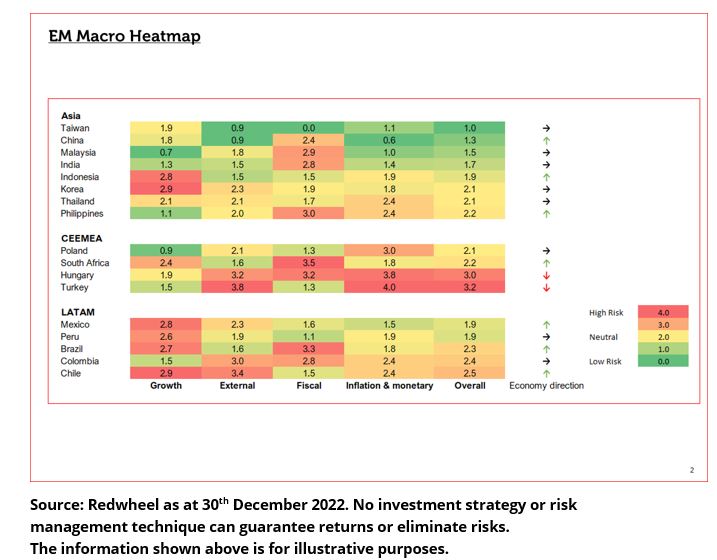

Regional Outlook We believe that China is expected to benefit from greater policy impetus following a period of destabilising politics over the past 2 years. This is already evident by several Covid-related policies and increased support for the real estate sector. We see political, economic and covid policies becoming more aligned in the domestic market while external conflicts taper off. This should allow China to continue outperforming going forward. Looking at India, the long-term investment case has strengthened in recent years and we believe the market provides a strong structural growth story. Valuations are expensive, but this comes on the back of strong earnings. External factors, such as crude oil, have turned favourable and domestic indicators continue to be encouraging. South Korea and Taiwan should benefit from a global cyclical recovery and an improvement in prospects for the semiconductor and tech hardware sectors. In Latin America, Mexico appears set to benefit from nearshoring due to its close proximity to North America. Brazil, having significantly tightened their monetary policy and will benefit from an easing monetary policy cycle as well as high commodity prices. The Middle East should continue to benefit from elevated energy prices while it diversifies its economy away from oil and broadens its capital markets. South African equities should benefit from our views on US and mainland China, even though the domestic macro trajectory is somewhat anodyne. For smaller EM and frontier markets (FM), idiosyncratic growth drivers are expected to drive asset prices. Our key themes: Commodities, New Factories of the World and Travel, across the smaller emerging and frontier markets remain intact. We have also seen a fall in prices of soft commodities. This may alleviate pressures on those countries such as the Philippines that are net importers of commodities and may abate food inflation concerns. In addition, a higher oil price is also a tailwind for many FM countries. While oil prices should remain elevated, the rate of change in oil prices should decline. The muted increases should contribute to an overall decline in inflation and allow central banks to cut rates going forward.

Commodities We believe that the recovery of Chinese demand as a result of its re-opening has the potential to outweigh any weakness in Western demand in the event of a recession. Looking at the oil supply and demand situation, a Chinese recovery to pre-pandemic levels would add 1mbpd to global demand and a full recovery of air travel and jet fuel demand, would add another 1mbpd. Looking at previous global recessions, oil demand has fallen on average by c.1mbpd. Therefore, a Chinese re-opening and economic recovery should have the capacity to more than offset any slowdown. China also accounts for more than half of the global demand for base metals and nearly two-thirds in ferrous metals and bulk commodities. For example, China remains a dominant consumer of copper, another of the strategy's key commodity exposures. With a clear sequential recovery path now expected for China in 2023, we believe that we are near the trough in the copper cycle due to a return to relatively healthy GDP growth trend. At the same time, 2022 has again demonstrated the supply constraints to the global copper supply which we expect to persist in the years to come. Long Term Growth Drivers Looking at the longer-term picture, we believe that we are at the cusp of an EM bull market after a "lost" decade in EM. The culmination of the previous 8 factors, though highly supportive for EM equities would ultimately be sufficient to drive a phase of outperformance akin to the 2016/18 episode (26% US$ outperformance over 26m), which albeit welcome at the time, lacked more structural pillars to prolong the rally. History tells us that longer duration EM outperformance is driven by earnings super-cycles where sustained and superior dollarized EPS growth against the US requires a seismic, underlying shift in the EM investment case. We believe this is coming to fruition as the global economy increasingly separates into two major trading blocs, one broadly aligned to the US and the other to mainland China. We think there will be winners from this de-globalisation and we consider four key themes; • Supply chain reorientation/Nearshoring The accumulation of these thematic pillars coupled with the previous 8 factors sets up an attractive growth story going forward.

Conclusion Emerging Markets faced numerous macroeconomic and geopolitical challenges in 2022. Despite the recent obstacles, we believe that the outlook for 2023 is positive and that we are at the cusp of an EM bull market. We expect to see a moderation in US monetary policy and a reopening of the Chinese economy which should improve sentiment and allow EM equity multiples to rerate from currently depressed levels. As a result, we believe EM equities are in a robust position to outperform developed markets and deliver high absolute returns. |

|

Funds operated by this manager: CC Redwheel Global Emerging Markets Fund, CC Redwheel China Equity Fund

Sources: [1] World Bank as at December 2022 [2] Goldman Sachs, Redwhee; and Haver as at 11 December 2022 [3] CLSA, National Stock Exchange, WFE Key information: No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to future results. The prices of investments and income from them may fall as well as rise and an investor's investment is subject to potential loss, in whole or in part. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only. |

14 Mar 2023 - January Junkyard Dogs

|

January Junkyard Dogs Arminius Capital February 2023 January looked like a great start to 2023, after the losses of 2022. The S&P/ASX200 index was up 6.2% for the month, similar to the 6.3% rise in the US S&P500 index. Share markets in Europe, China and Latin America were even stronger. But appearances can be deceptive. The January rally was built on hope, not facts. Investors were betting that the Fed would stop raising interest rates and the battered tech sector would recover. For example, Tesla gained 40%, Bitcoin jumped 38%, and even the joke Dogecoin rose 32%.

What investors were doing is called bottom fishing: that is, they were buying the assets which had fallen the furthest in 2022, on the grounds that they must be cheap after such big price falls. For example, Meta Platforms (the disaster formerly known as Facebook) fell by 76.7% from peak to trough in 2022. In January 2023 it rebounded by 109.8%: simple arithmetic tells you that it is still down 51.2%, i.e. Meta shareholders have still lost half their money. Is Meta cheap? History suggests it isn't. The investors who are buying beaten-down tech stocks in this cycle are usually too young to remember the aftermath of the 2000 dotcom boom. As PT Barnum said, "There's one born every minute." Older readers will recall that the tech stocks began to slip in April 2000, and kept sliding for the next four years. They did enjoy rebounds every few months, but these were all false dawns as the bear market persisted. The best of the tech stocks - think Amazon, Google, Microsoft - lost about 75% of their value from peak to trough. The rest of the tech stocks just disappeared altogether. In fact, if dividends are excluded, the whole US share market was no higher in 2007 than it had been in March 2000. The January 2023 rally ended in early February as the Fed (and other central banks, including our own Reserve Bank) put an end to investors' fantasies by making it very obvious that interest rates were going higher and staying up for longer. Early reporting from US companies for the December 2022 quarter showed that in many cases profitability was falling short of expectations.

Arminius continues to believe that, even though we are now in the Year of the Rabbit, several of the tigers from 2022 are still hanging around, such as oil prices and the Ukraine crisis, and they have been joined by the problem of Congressional gridlock in the US. The biggest of these tigers is inflation, which is not going back to the sub-2% levels which was obtained in the peaceful decade before Covid. At best, US inflation will abate from 7% to around 4%, but then it will get stuck. The tight US labour market is pushing up wages in key sectors, and companies are pushing through price increases in order to pass on increases in wages and input costs. Persistent inflation means that the Fed will not cut interest rates as quickly as the bond market is hoping. At worst, US inflation will fall slightly then begin to rise again, e.g. because of external factors such as higher oil prices or higher commodity prices. Under these circumstances, the Fed may have to raise interest rates again ala the Ghost of Arthur Burns past. The outlook for Australia is better than the outlook for the US, and we expect the Australian share market to outperform the US over the next three years. This has nothing to do with domestic Australian policies; if anything, it's in spite of. The main drivers of this positive outlook are China and the resources boom. The Chinese economy is not recovering as fast as the bulls might hope, but it will be back to pre-Covid levels by late 2023. In addition, the Chinese government is quietly stepping back from its unofficial bans on Australian exports from coal to lobsters. Global de-carbonization is fueling a resources boom which will focus on the minerals used in batteries and clean energy generation, "critical minerals" such as copper, nickel, cobalt, graphite and lithium. This latest resources boom means that Australian investors will enjoy a rising A$ against most major currencies, which will also help to curb domestic inflation. US investors, by contrast, will see the US$ continue to weaken, which tends to mean importing inflation. The single most important thing for investors to remember in 2023 is that the world has changed. We are not going back to the world of ultra-low interest rates because inflation is not going away, and the forty-year bull market in bonds ended abruptly and painfully in 2022. This paradigm shift means that investors need to question the habits which they have built up since the GFC, and adjust their investment strategies to a world of higher volatility, where real assets will outperform financial assets.

Australian equities will perform better than most of the world over the next three years, but the new paradigm of higher volatility means that the old strategy of buy-and-hold won't work very well in a world where commodities and resource companies lead share market performance. To cope with the coming turbulence, investors will need exposure to commodities and to long/short strategies - i.e. the ability to short shares as well as buying them. The Arminius Capital "ALPS" strategy returned +21.67% in 2022, compared to negative -19% for the US S&P500 and negative 1.1% for Australia's S&P/ASX200. The 2022 return puts ALPS among the top 3 out of 39 alternative funds. The key factors behind the ALPS annual return of +21.6% were to invest in commodities and to invest long/short. Funds operated by this manager: |

13 Mar 2023 - The Long and The Short: Could the year ahead defy the Fed?

13 Mar 2023 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

|||||||||||||||||||

| Argonaut Australian Gold Fund | |||||||||||||||||||

|

|||||||||||||||||||

|

|||||||||||||||||||

| Maxiron Monthly Income Trust | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

Want to see more funds? |

|||||||||||||||||||

|

Subscribe for full access to these funds and over 700 others |

10 Mar 2023 - When inflation meets recession

|

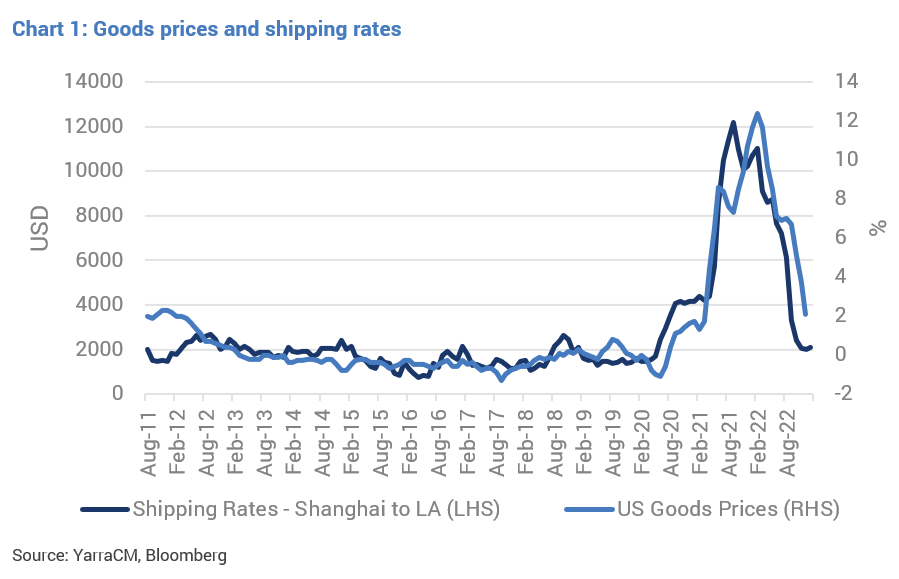

When inflation meets recession Yarra Capital Management February 2023 So, has inflation peaked or not?Given the multi-decade high inflation levels of 2022 was the precursor to aggressive interest rate hikes, a key driver for the 2023 outlook is the direction of inflation. Throughout 2022 three core factors drove higher inflation; supply chain issues, amplified goods demand due to stimulus, and a commodity price shock. All three appear to have peaked. Several economic indicators suggest that supply chain issues are behind us. The supply chain measure provided by the Federal Reserve has fallen, shipping rates between the US and China have normalised (refer Chart 1), and key global exporters such as Korea and Germany are now seeing export orders decline.

Additionally, the impact of central bank rate rises through 2022 should see consumer spending slow in 2023, as the fastest rate hiking period in the past 30 years quickly constrains household budgets. In Australia, we expect to see mortgage costs rise anywhere from 20-60% (for the typical borrower), with those who borrowed on a fixed rate over the past 18 months will see a 60% increase in payments. After an era of cheap money and stimulus provided during COVID, this should take the sails out of the outsized goods demand over the past two years.

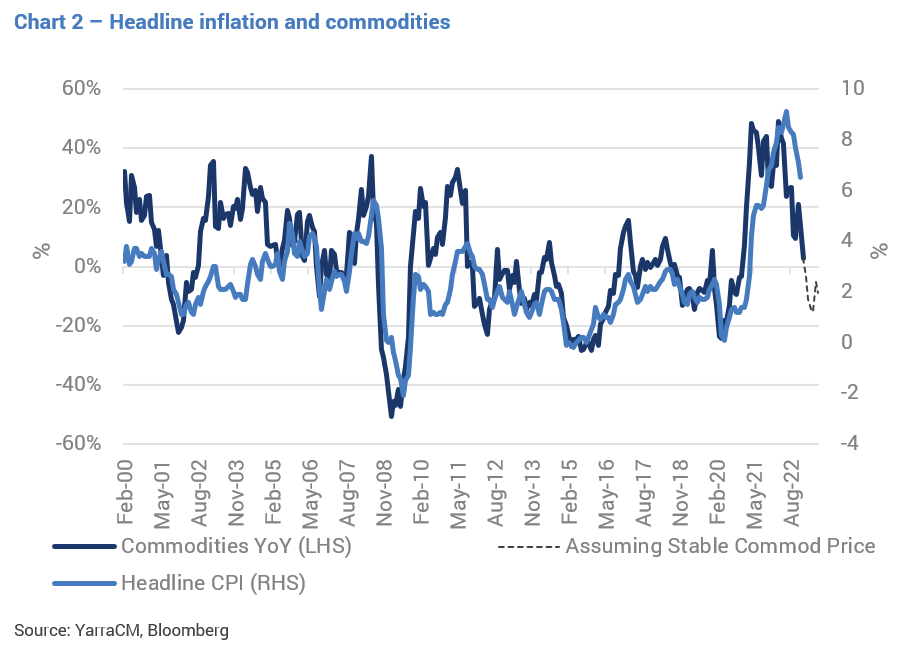

While geopolitical risk related to Russia dominated headlines in 2022, commodity prices have begun to fall. Oil is now flat on a year-on-year basis and commodities are declining. Commodity prices are one of the strongest predictors of inflation, and the more benign commodity prices, point to inflation falling away in 2023 (refer Chart 2).

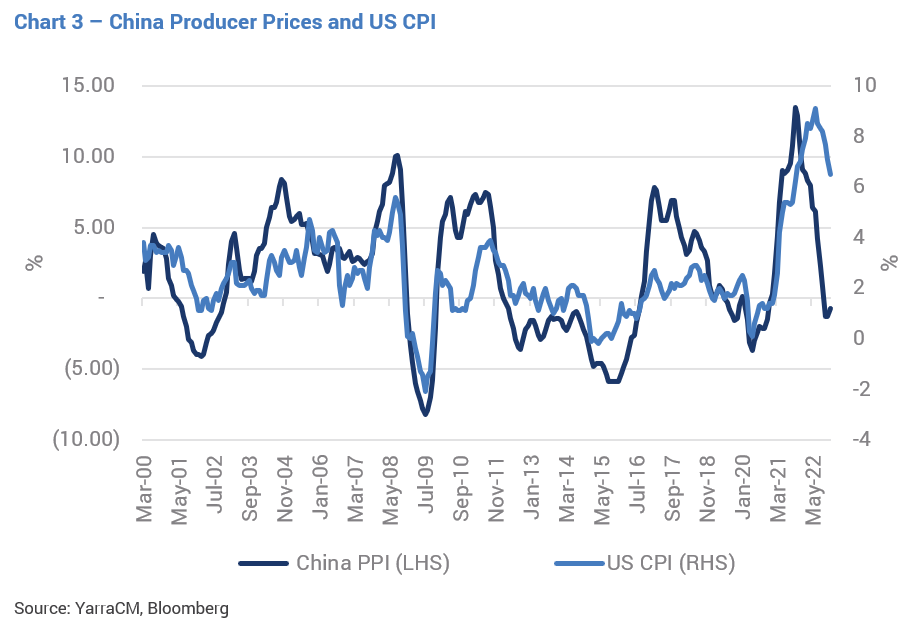

Outside of these factors, several other lead indicators of inflation are beginning to decline. These include producer prices in China dropping to deflationary levels (refer Chart 3).

PMI surveys show that firms are now reporting that input prices are falling, and small business surveys show the number of firms passing on price increases has peaked (refer Chart 4).

While the indicators do not point to a deflationary environment, the speed with which they have shifted, combined with the central bank's aggressive hiking cycle, suggests that we could see inflation back within their target bands by the middle of the year. This would encourage central banks to keep interest rates high but remove their hawkish bias. Signs pointing to rising recession riskThe second factor that is likely to determine interest rates in 2023 is related to recession risk. Historically, when a recession occurs, interest rates fall aggressively as central banks ease financial conditions to boost their economies. This has occurred in every recession over the past 50 years (refer Chart 5).

On average, following a recession, the cash rate dropped by 400 basis points, with smaller decreases only occurring when the cash rate hit the zero bound (refer Table 2). In no instance did the cash rate finish the recession higher or at the same rate it started.

If the US enters a recession in 2023, there will be pressure on the Federal Reserve to cut the cash rate. Currently, several recession indicators are starting to flash red and point to a distressing growth signal. These signals can be seen in the leading index of US growth, new orders, consumer expectations, and housing. For example, the leading US growth index has moved into contraction (refer Chart 6) and is now at a level indicative of a recession, as observed in all of the past eight occurrences.

A warning sign of recession can also be a result of falling indexes including new orders relative to inventories which have now seen the US yield curve invert across multiple maturities (refer Chart 7). Historically, this has preceded a recession by approximately six to 12 months, reflecting monetary policy has become too tight for economic conditions. As with the leading index above, curve inversion has not given a false positive and has preceded all recessions since 1970.

In addition, we are seeing recessionary signals such as a weak housing market and an extreme softening in consumer confidence.

While many may hope that the economy faces an unemployment-less recession, i.e., that unemployment doesn't rise as growth falls, this would be an extremely rare occurrence. Over the past 50 years, unemployment has never remained stable through a recession, rising anywhere from 0.6% to 3% higher over a six-month period. If the US economy does enter a recession, a rise in unemployment should not be far away.

The key takeaway is that we have not seen this many recessionary signals since 2007, creating strong pressure for central banks to ease rates should a recession occur. Interest Rate Outlook - Inflation meets recessionThese two forces produce two very different outcomes for central banks and interest rates. On the one hand, high but slowing inflation should encourage central banks to maintain their hawkish stance, hold rates high and ensure that inflation returns to its 2% targets. However, the deterioration in economic data would historically have seen a dovish tone being adopted by now. So which force should win? The below chart shows that, historically, recession risk dominates. When recession occurred in the '70s, '90s, and '00s, rates fell even when inflation was high. Furthermore, in 1974 and 2008, the cash rate fell before inflation peaked and was still running at over 5%.

Despite this, the Federal Reserve continues to present an extremely hawkish message, expecting to make cash rate moves that take little consideration of the existent lags in monetary policy. The Federal Reserve dot plot (a chart that records each Fed official's projection for the central bank's key short-term interest rate) currently shows an expectation for cash rates to be around 5.5% in 2023. Considering this, it may set up 2023 to be a tale of two halves; higher cash rates to begin the year and lower cash rates mid-year as the Fed acknowledges the recession risks. With this in mind, we believe rates will end 2023 lower than 2022, even if central banks continue to talk a hawkish message in the first few months of this year. If the recessionary indicators prove correct, then rate cuts of 400 points is the magnitude required to restart the economy, which would drag short-dated interest rates into a 1-2% range. The Yield Curve - Flatter short-term, much steeper long termThe yield curve is one of the most consistent series in bond markets as both the driver of its changes and the levels it respects. While bond yields have fallen from 15% to 0%, the spread between the two and 10-year bonds has typically been range bound between -100bps and +250bps. When looking at the two-component rates of the curve, it is easy to see that monetary policy direction is the key driver that determines both steepening and flattening. When the cash rate rises the yield curve flattens, and when the cash rate falls the yield curve steepens. This occurs as the 2-year yield makes larger moves with the change in the cash rate while the 10-year yield is slower-moving. Typically, the 2-year yield moves the fastest to cause large changes in the shape of the curve (refer Chart 11).

We can make two comments about the direction of the curve:

As such, we currently favour a steepening position for three reasons. Firstly, central banks can change their minds and we believe that the magnifying recession signals should not be ignored. If the recession risks are proven true, we should see dovish actions take place sometime in 2023 which will cause the curve to steepen. This idea is backed up by the fact that post-1970, curve inversion has signalled that rate hikes should be coming to an end.

Secondly, the typical flattening cycle occurs over multiple years, while the steepening period is usually far shorter, with the first 100 points of steepening occurring over 9-12 months.

And finally, the curve typically struggles to flatten through -50 to -75 levels that are now broken and take the inversion to historically stretched levels. As such, we are looking to position ourselves to capture the next 200-point move steeper, rather than the last 20-50 points flatter. Is the RBA done with interest rate hikes?While the majority of this outlook has focused on the US, as Australian and US long end rates are highly correlated, for short-dated rates it is important to consider whether or not the RBA has finished its hiking cycle. This is important as the differential between US and Australian short-dated rates is largely determined by the cash rate differential. When the Australian cash rate is higher than that of the US, then 2-year bond yields in Australia will be higher too. Since Australian short-dated bonds remain well below the US, the ability for them to move in a similar nature to the US will depend on the RBA's next action.

One of the key differences between Australia and the US is that the Australian mortgage market is predominantly a variable rate market, while the US mortgage market is fixed. This means the Australian household should feel the brunt of rate hikes faster and at a lower interest rate than in the US. We determine how restrictive monetary policy is by estimating the percentage of disposable income allocated to repaying loans. This measure accounts not only for interest rates but total debt loads and income in the economy. As shown below, the current RBA hikes have already taken this measure to some of the tightest monetary policy settings we have seen in the past 40 years.

Since the Australian policy setting is becoming historically tight, and the global economy is slowing, we believe the RBA is approaching the end of its hiking cycle. If this is the case, 3-year bond yields should have already peaked for this cycle and are currently close to what we consider a fair value. Whether or not short-dated bonds can rally in Australia in 2023 will depend largely on what the RBA does with the cash rate. In previous hiking cycles, if the cash rate can remain stable for 12 months or longer (1995 and 2010), then 3-year bond yields consolidated at those levels for an extended period (refer Table 3). However, when the cash rate held at its peak for only six months (such as in 2000 and 2008), bond yields rallied in anticipation of future cuts and saw yields materially under the cash rate.

Currently, it's too premature to tell whether the RBA will need to cut rates in 2023, as the lead growth indicators for Australia are not as weak as they are in the US. However, if the US and Europe enter a recession, we would expect Australia to follow. Given we are likely near the peak of the cash rate cycle, this effectively sets up an outlook where two outcomes can likely occur. If the global economy avoids a recession, Australian 3-year yields should be somewhat stable and trade around 3.50%. Alternatively, if the global economy continues to slow, we should end the year with yields well below 3%. Therefore, we expect there is a strong likelihood that short-dated yields will end in 2023 lower than in 2022. Author: Chris Rands, Co-Portfolio Manager of the Yarra Australian Bond Fund |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

9 Mar 2023 - Investment Perspectives: 10 charts for optimism in 2023

8 Mar 2023 - This retailer has been savaged on results but does it provide an opportunity?

|

This retailer has been savaged on results but does it provide an opportunity? Novaport Capital February 2023 Tim Binsted from NovaPort Capital runs the ruler over this retailer's results and provides an outlook for the coming 12 months. Specialty retail has been a tough place to operate over the past 12-18 months. Gone are the goldilocks conditions of the pandemic (at least from a retail perspective), where everyone was at home remodelling their living rooms and updating their décor. Replaced by an environment of higher interest rates, mortgage stress, and increased economic uncertainty. The company we're focused on today has been savaged by the market on the back of its latest results, perhaps unfairly, suggests Tim Binsted from NovaPort Captial.

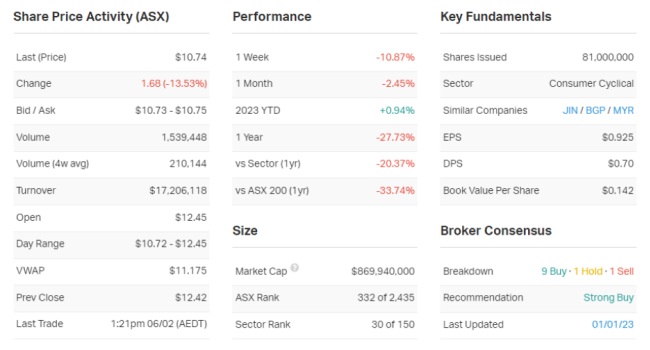

The stock in question is Nick Scali (ASX: NCK) and whilst the company's results were much stronger than a year ago, with revenue and EBITDA up more than 50% each, written sales orders were down more than 12% on January 2022 - and that's what has spooked the market. The NCK share price performance has been solid since the June low, rallying from around $7 to north of $12 before today's results. Join me as I dive into the results with Binsted and get his take on the prospects for Nick Scali as it continues to navigate the post-Covid retail landscape. Nick Scali (ASX: NCK) H1 key results and company data

In one sentence, what was the key takeaway from this result? It looks like the froth from the lockdown-driven boom in furniture sales has ended. The stock is down 13% on the results. In your view, was it an overreaction, an under-reaction or appropriate? I think it looks like a bit of an overreaction. I think we had the market jumping at shadows leading into the market lows with big fears about retail disaster. The whole sector sold off and then it rallied when trading was better than expected and it rallied quite hard into the result. Everyone was expecting that the boom in COVID sales couldn't last forever. I think it's not surprising that we've had some moderation, but the market's now extrapolating this going forward. I think it's jumped at shadows before, recovered and rallied.

We're there any major surprises in this result that you think investors should beware of? No major surprises. We've all seen rising rates. We all knew there was a huge boom in sales during COVID per this category in particular, those comps were never going to last.

I mean, they're [sales] not falling off a cliff. They're still well up on pre-COVID. I wouldn't have thought there's a massive surprise in there. The main positive surprise would be how well they're executing on the Plush acquisition. Would you buy, hold or sell NCK on the back of these results? RATING: Hold Please note that NovaCapital currently hold this stock in its portfolio. What's your outlook on NCK and its sector over the year ahead? Are there any risks to this company and its sector that investors should be aware of?

I think you'd also expect that rising rates will put a little bit of a dent in as well, but you've got very strong employment, so that should support sales to some degree. As long as unemployment is below 4%, wages are still strong. That's a mitigating factor. And then you should see them bank a lot of synergies from the acquisition of Plush, which is going really, really well. They've got one of the best management teams in the business executing that. They've got $20 million out already on a runway basis, and they're getting the margins up in that Plush business. There's 6-7% percentage points of margin that they're getting through there.

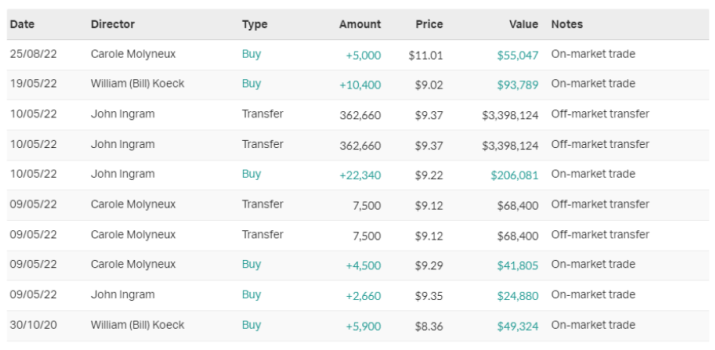

I think the retail sector, generally, it is going to get tougher with rates going up. You've got a lot of fixed mortgages rolling off, it's been well flagged, that's going to hit consumers, but we're coming off a really high base and the valuations aren't that high for Scali and some of its peers. There's a few offsetting factors there, but you have to say sales would have to be a bit less rosy, but it just depends on individual stocks and how they're placed to manage that. There will be a little bit of top-line pressure, but it's well-run business with good margins and a great acquisition to deliver synergies. From 1-5, where 1 is cheap and 5 is expensive, how much value are you seeing in the market right now? Are you excited or are you cautious on the market in general? RATING: 2-3 I think you'd have to say it's pretty exciting. I think you probably have to say somewhere between a two and a three. And the reason that I've given you a range, I'd probably skew it more towards two. For cheapness, there is value, but we just haven't really seen the earnings pressures yet. We've had a very good period for market earnings. I think we've had the PE come down, bit of a de-rate with the interest rate rises, and we haven't seen the earnings pressure yet. Maybe we're just starting to see a little bit of that through pockets of the market. I think you want to see a bit more of an adjustment there. Plus, we've had a big rally over Christmas and into February reporting, so that's taken away some of the ultra cheapness out of the market. But there's opportunity. The market's rebased a bit and it's a good time to be investing. 10 most recent director transactions

Source: Market Index Funds operated by this manager: NovaPort Microcap Fund, NovaPort Wholesale Smaller Companies Fund This material has been prepared by NovaPort Capital Pty Limited (ABN 88 140 833 656, AFSL 385 329) (NovaPort). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable, but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed. |