News

24 May 2023 - Momentum is Building in Aged Care

|

Momentum is Building in Aged Care Novaport Capital May 2023 With established investments in both of Australia's listed residential aged care providers, Estia Health and Regis Healthcare, our positive outlook for the sector is informed by three factors. Firstly, advanced age is associated with complex and ongoing care needs which Residential Aged Care is uniquely positioned to provide. Secondly, Aged Care operators with established processes to consistently deliver care (meeting ever more demanding standards) have a clear opportunity to consolidate what is currently a fragmented sector. Finally, the demographic tailwind provided by a growing and ageing population supports demand growth for the foreseeable future. Aged Care Industry Consolidation - Number of Providers

Source: Regis Healthcare In recent years the sector had to navigate challenges including a squeeze in funding, the Royal Commission and COVID-19; however recent operational updates from the listed providers as well as an announcement from the Federal Government, highlights how positive momentum is building in the sector. Funding ClarityOn 4th May 23, the Australian Government outlined how it will fund a 15% Aged Care workforce pay increase proposed by the Fair Work Commission. It is offering a meaningful increase in the AN ACC daily funding rate (rising to over $240 per resident) as well as a 'hotelling supplement' of $10.80 (per resident per day) to cover increased wages for aligned staff such as chefs. The funding increase is expected to pass through to workers in the form of higher wages, yet it reflects a positive outcome for the sector overall. It resolves a major uncertainty has dogged the sector since the Fair Work Commission first proposed wage increases for Aged Care employees. It also indicates the current government's commitment to sustainably reform the sector. Providing financial incentives for workers to commit to a career in Aged Care should support improved quality of care and customer satisfaction. In the past, low wages have repelled workers from Aged Care and operators became increasingly reliant on temporary employment agencies to fill rosters. The margins charged by these agencies are high, therefore the financial burden of using agency staff has been punitive for operators. Stabilising the workforce represents a meaningful opportunity for Aged Care operators to improve their financial performance. Operating Metrics ImprovingRecent updates from both the listed Aged Care operators shows they have made good progress on driving operational improvement. Occupancy is trending higher following several years disrupted by the Royal Commission and then Covid-19. Higher occupancy drives both revenue and margin.

Source: Regis Healthcare Ltd, Estia Health Ltd The sector has is also making progress adapting to the AN ACC funding reforms. Following substantial changes to the funding model, Aged Care operators can now refine their operations to ensure they are adequately funded to provide better quality care to residents. Resolving the uncertainty about the funding structure has enabled operators to develop platforms and models to deliver sustainable care. Author: Sinclair Currie, Principal and Co-Portfolio Manager Funds operated by this manager: NovaPort Microcap Fund, NovaPort Wholesale Smaller Companies Fund This material has been prepared by NovaPort Capital Pty Limited (ABN 88 140 833 656 AFSL 385 329) (NovaPort), the investment manager of the NovaPort Smaller Companies Fund and the NovaPort Microcap Fund (Funds). Fidante Partners Limited ABN 94 002 835 592 AFSL 234668 (Fidante) is a member of the Challenger Limited group of companies (Challenger Group) and is the responsible entity of the Funds. Other than information which is identified as sourced from Fidante in relation to the Funds, Fidante is not responsible for the information in this material, including any statements of opinion. It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. You should consider, with a financial adviser, whether the information is suitable to your circumstances. The Fund's Target Market Determination and Product Disclosure Statement (PDS) available at www.fidante.com should be considered before making a decision about whether to buy or hold units in the Funds. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. NovaPort and Fidante have entered into arrangements in connection with the distribution and administration of financial products to which this material relates. In connection with those arrangements, NovaPort and Fidante may receive remuneration or other benefits in respect of financial services provided by the parties. Fidante is not an authorised deposit-taking institution (ADI) for the purpose of the Banking Act 1959 (Cth), and its obligations do not represent deposits or liabilities of an ADI in the Challenger Group (Challenger ADI) and no Challenger ADI provides a guarantee or otherwise provides assurance in respect of the obligations of Fidante. Investments in the Fund(s) are subject to investment risk, including possible delays in repayment and loss of income or principal invested. Accordingly, the performance, the repayment of capital or any particular rate of return on your investments are not guaranteed by any member of the Challenger Group. |

23 May 2023 - Australian Secure Capital Fund - Market Update April

|

Australian Secure Capital Fund - Market Update April Australian Secure Capital Fund May 2023 Australian housing values appear to have stabilised, with a second consecutive monthly increase as CoreLogic's national Home Value Index rose by half a per cent. The capital cities performed strongly, with Sydney leading the way with a 1.30% increase for the month, followed by Perth (0.60%), Brisbane (0.30%), Adelaide (0.20%) and Melbourne (0.10%). Canberra and Tasmania remained stable, whilst only Darwin recorded a decrease in values, with a 1.20% reduction. Similarly, the regions have also performed quite well, with South Australia seeing a 0.90% increase, followed by Queensland (0.80%) and Western Australia and Tasmania, both increasing by 0.10%. Only regional Victoria and New South Wales experienced a reduction in values, of 0.40% and 0.30%, respectively. Auction activity remained low in April, with volumes down by approximately 25% when compared to last year. Persistently low levels of residential property coming to market remains a key factor in supporting housing values. The rolling four week trend during April was around 14% below the previous five year average in new listings for April. Whilst numbers were down, clearance rates remained robust. With the decision of the RBA to once again increase the cash rate by a further 0.25% following last month's pause, the outlook for the property market remains stable but with future growth potentially constrained. Whilst we are yet to see the full impact that the rate rise cycle has had on household cashflows, foreign buyers are returning and the labor market remains tight which should keep prices stable. Clearance Rates & Auctions 17th - 23rd of February 2023 |

22 May 2023 - 4D podcast: The golden opportunities for infrastructure in a challenging environment

|

4D podcast: The golden opportunities for infrastructure in a challenging environment 4D Infrastructure May 2023 Bennelong Account Director, Jodie Saw, speaks with Chief Investment Officer and Portfolio Manager, Sarah Shaw, about how infrastructure has been performing, 4D's portfolio, and the opportunities for infrastructure growth despite a tumultuous few years. "There is a place for infrastructure in all portfolios and in all markets. It offers defensiveness with growth, and sector and regional diversity, which means infrastructure can be fundamentally positioned for all points of an economic cycle. And we think allocations to the asset class should be more representative of this opportunity set."

|

|

Funds operated by this manager: 4D Global Infrastructure Fund (Unhedged), 4D Global Infrastructure Fund (AUD Hedged), 4D Emerging Markets Infrastructure Fund For more information about 4D Infrastructure, visit https://www.4dinfra.com/ The content contained in this audio represents the opinions of the speakers. The speakers may hold either long or short positions in securities of various companies discussed in the audio. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the speakers to express their personal views on investing and for the entertainment of the listener. |

19 May 2023 - The blue sky for rare earths now a bit cloudier

|

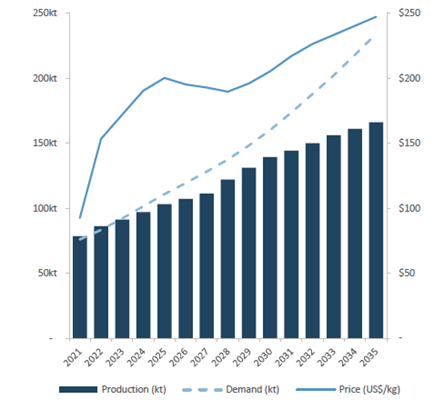

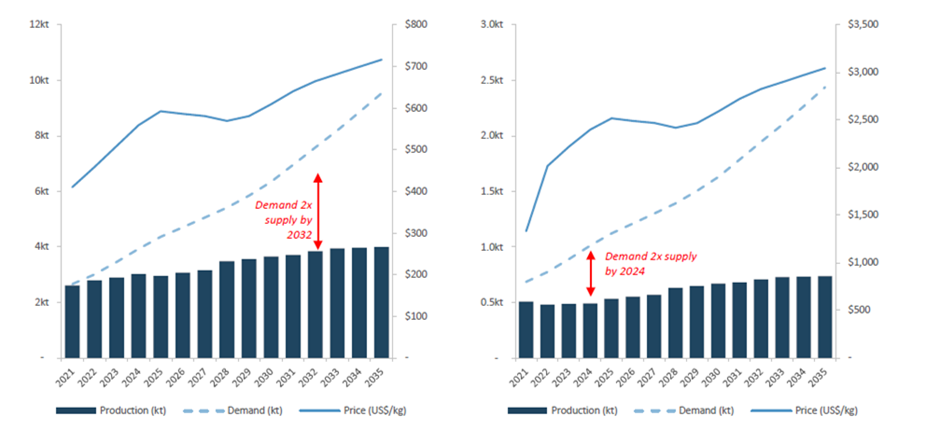

The blue sky for rare earths now a bit cloudier Tyndall Asset Management May 2022 Tesla claims it will eliminate the use of Rare Earths in its Electric Vehicles. Portfolio Manager Jason Kim investigates how realistic this claim is, drawing on insights from Adamas Intelligence, a leading research consultancy on critical minerals, and industry consultant Yoo Cheol Kim (YC Kim). During Tesla's 2023 Investor Day in March, the global electric vehicle behemoth claimed that their next generation electric vehicles (EVs) will no longer contain rare earths. Rare earths are used in some permanent magnets that are a critical component of motors in electric vehicles. These magnets contain rare earths called NdFeB magnets (Nd - the rare earth elements Neodymium and Praseodymium, in conjunction with some Terbium and Dysprosium, Fe - Iron - and B - Boron). Tesla CEO, Elon Musk, is known for making hyperbolic statements and although his statement contained no details on how this would be achieved, the impact on rare earths stocks was immediate and dramatic. Lynas, a large producer of rare earths listed on the ASX, saw its share price decline by almost 7% on the day, with further declines over the subsequent three weeks - a cumulative 23% decline during March alone (although part of this decline may also reflect the coincident announcement of an increased Chinese production quota of rare earths). Similar declines were seen elsewhere, including in China, the dominant producer and processor of rare earths, with key stocks in China falling anywhere from 4% to the daily limit of 10% on the day after Tesla's statement. Ferrite Magnets - the only feasible option currentlyTesla had previously used AC induction motors (with no rare earths) in their earlier models but replaced them with permanent DC magnet motors which contained rare earths (NdFeB magnets). Tesla's decision to switch away from AC induction motors was driven by a range of factors, including problems with unbalanced voltage supply, rotor locking, and interference with the complex network of sensors found in modern vehicles. In light of these challenges, a number of experts in the field of EVs and rare earths predict that Tesla will not return to using AC induction motors. According to Adamas Intelligence, the only current feasible alternative to rare earth-containing magnets is ferrite magnets. Moreover, ferrite magnets are currently being used by Proterial (formerly Hitachi Metals) in its latest EV motor design and have previously been used in vehicles such as GM's 2016 Chevy Volt. Germany's BMW has been active in steering away from rare earth magnets, with the company prompted to reduce its rare earths consumption to limit over-reliance on Chinese-based supply chains given growing geopolitical tensions. However, while ferrite powered motors can match the performance of NeFeB powered motors to some extent, this performance comes with a significant weight and efficiency penalty that has made the switch unattractive to date. This means that the manufacturer must accept a reduced driving range or an additional cost for a larger battery to maintain the driving range. There is also the issue of a material reduction in torque with the ferrite powered motors. Given the bigger batteries, as well as more copper required, some experts believe there is no material cost advantage to using ferrite powered motors to NdFeB powered motors. Why is Tesla looking to stop using Rare Earth (NdFeB) powered motors?Tesla's move reflects concerns that there is insufficient supply of rare earths to meet the projected demand for EVs over the coming years. Rare earths industry consultant, YC Kim, subscribes to this view. He has stated that the global EV market is projected to grow from 8.2 million units in 2022 to 39.2 million units by 2030, a nearly 5-fold increase in eight years. While these numbers are forecasts and subject to significant uncertainty, there is little doubt that the switch away from internal combustion engine (ICE) vehicles is accelerating. The result will be an increase in demand for EVs such that production volumes will be multiple times higher by the end of the decade. In 2022, Adamas Intelligence data indicates that passenger EV motors were responsible for 12% of global NdFeB magnet consumption.¹ According to YC Kim, if global EVs production grows to 39.2 million units by 2030, then EVs will account for roughly 50% of the NdFeB magnet consumption in 2030. This would see total demand for NdPr (Neodymium and Praseodymium) growing to almost four times its current size by 2030.² Where will all these Rare Earths come from?This fourfold increase in demand for rare earth minerals appears difficult to satisfy based on current supply forecasts. Indeed, the supply-demand forecasts of both Adamas Intelligence and YC Kim indicate a substantial shortfall in the supply of these rare earth elements (refer Figures 1 and 2). Figure 1: NdPr demand-supply balance (LHS) vs price (RHS) Source: Adamas Intelligence, and Australian Rare Earths Ltd. Figure 2: Dysprosium and Terbium demand-supply balance (LHS) vs price (RHS)

Source: Adamas Intelligence, and Australian Rare Earths Ltd. This supply shortfall will be very positive for pricing, as higher prices will be necessary to incentivise new supply to come to market. If Tesla wants to meet its target, it is clear that based on current supply forecasts, there simply won't be enough rare earths to produce their targeted number of EVs using NdFeB powered motors. YC Kim's discussions with major auto manufacturers suggest the first preference is to use NdFeB powered motors. He is of the view that while ferrite powered motors will work, given the significant trade-offs, they will only be suitable for lower priced mass market cars. It is simply a matter of rationing the limited supply of rare earths. YC Kim is also concerned that the growing demand for EVs within China could result in the cessation of rare earth exports as soon as 2025. Further, China has issues with its own supplies currently and has stepped out to neighbouring countries such as Myanmar (via China-controlled entities) to produce rare earths. This looming supply shortfall and potential cessation of Chinese supply has not gone unnoticed by Western governments, as detailed by Stefan Hansen in his note The Value in Securing Critical Mineral Supplies. ConclusionDespite Tesla's ambitious claim that it will cease using rare earths, it appears the demand for rare earths will continue to grow and that supply growth still remains an issue. This will most likely result in the various industries increasingly using lower quality alternatives purely out of necessity and not out of choice. There are some possible advancements that may result in true alternatives to rare earths in motors, such as manganese bismuth magnets. However, they are all still in their development infancy, and their commercialisation, if they prove to work, is still several years away. Iluka Resources, which is predominantly a mineral sands miner with a very large presence in titanium dioxide and zircon markets, has been a beneficiary of government support aimed at increasing the supply of critical minerals including rare earths. This support will assist in the acceleration of Iluka's emerging, but potentially very large, rare earths mining and processing business. As we transition towards a net-zero world while being in a period of heightened geo-political tensions, Tyndall AM believes that Iluka Resources offers a unique and undervalued opportunity. The market has not fully understood the potential upside from their rare earths opportunity, and the significance of the government support that this project has received. Author: Jason Kim, Portfolio Manager Funds operated by this manager: Tyndall Australian Share Concentrated Fund, Tyndall Australian Share Income Fund, Tyndall Australian Share Wholesale Fund

References

Important information: This material was prepared and is issued by Yarra Capital Management Limited (formerly Nikko AM Limited) ABN 99 003 376 252 AFSL No: 237563 (YCML). The information contained in this material is of a general nature only and does not constitute personal advice, nor does it constitute an offer of any financial product. It does not take into account the objectives, financial situation or needs of any individual. For this reason, you should, before acting on this material, consider the appropriateness of the material, having regard to your objectives, financial situation, and needs. The information in this material has been prepared from what is considered to be reliable information, but the accuracy and integrity of the information is not guaranteed. Figures, charts, opinions and other data, including statistics, in this material are current as at the date of publication, unless stated otherwise. The graphs and figures contained in this material include either past or backdated data, and make no promise of future investment returns. Past performance is not an indicator of future performance. Any economic or market forecasts are not guaranteed. Any references to particular securities or sectors are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities or sectors and no warranty or guarantee is provided. |

18 May 2023 - Learning the lessons of history

|

Learning the lessons of history JCB Jamieson Coote Bonds May 2023 Investors have been faced with more historic events in the past three years than most people see in two decades. Charlie Jamieson and Mark Burgess share their views on what's ahead and how lessons from the GFC have prepared investors.KEY TAKEAWAYS:

Investors have been through a range of extreme events in the past three years. Those trials have included zero interest rates followed by the fastest rate hiking cycle in history, oil prices turning negative, two of the largest banking collapses in US history, several crypto crashes and - most obviously - a global pandemic. Now, three years on from the start of the pandemic, Jamieson Coote Bonds (JCB) Chief Investment Officer, Charlie Jamieson and Mark Burgess, Chair of the Advisory Board, have shared their views on the path ahead for markets. SKILL TO DRIVE FUND MANAGER RETURNSIn the years following the global financial crisis (GFC), falling cash rates drove better returns from bonds, according to Mr Burgess. When central banks cut their cash rates following the GFC (and abruptly 'raced to zero' during the early stages of the pandemic), it helped fund managers deliver generally better results, he said. Typically, banks lower their borrowing costs as the cash rate trends downward. As a result, falling rates reduce the cost of capital for businesses and increase the expected return on investments*. Lower borrowing costs also encourage businesses to invest more in new capital assets. But that situation has changed with significant lifts to cash rates worldwide in the past 12 months. Mr Burgess said fund performance will come to lean more heavily on the skill of fund managers. Their ability to pick assets, the strategies they employ and the timing of their implementation will be vital to their success. "So the choice of manager matters," Mr Burgess reiterated. "Skill will be the biggest proportion of return, rather than falling rates which has been the biggest proportion of returns in my career. And if you have invested with a fund manager who's not that skilled, you're about to find out about it." NO 'V-SHAPED' RECOVERYMr Burgess explained that while there's little doubt the global economy is in the throes of a bear market, there's some debate over whether this is a normal cyclical bear market, or a structural one. If it's a structural bear market, the correction will be "far deeper and longer" than if it were simply cyclical. Mr Burgess, however, is not in the structural camp. "For that correction to happen, the structure of the system has to break," he said. Mr Burgess went on to explain that while the environment remains fragile, lessons from 2008, interventions by authorities in any failing institutions and better capitalised core banking systems, should allow for less cyclical damage than markets such as 2008 or 1970s which saw severe structural corrections. He noted however that the environment remains challenging, which will limit the ease of an immediate recovery. "It's no longer about creating credit; it's about how we structure debt and refinance. With high levels of debt refinancing is the key and the recovery there will be challenging." Although assessing the current bear market as cyclical, JCB does not expect to see a 'V-shaped' recovery in which asset prices enjoy a sharp rise back to previous highs after a similarly sharp decline. "Barring a catastrophic and systemic shock we're not going to be cutting rates," Mr Jamieson said. "That's why it's such a different go-forward, because all of the things that got carried to that very high place pre-COVID are unlikely to get carried in that same way. "So, as we've had these adjustments through the bond market, through some credit markets and the like, we're not going to get that V-shaped recovery." PLENTY OF CASH ON THE SIDELINESMr Burgess said one of the big surprises is how much money is currently "sitting underneath the market". This, he said, is likely driven by the lessons learned in 2008 during the GFC. "One of the advantages of having had a global financial crisis in '08 is that when you get a financial crisis, you actually get some future benefit, and that future benefit is that you know how to handle a financial crisis," he said. "The way people are preparing for it is that a lot of high-net-worth investors have a lot of cash ready to buy distressed assets." Most institutional investors have already pre-allocated cash to purchase distressed or oversold assets, he said. However, in some cases Mr Burgess said the volume of cash sitting in some areas such as private equity and institutional and high net worth holding is notable. Other areas however will see cash constraints - such as speculative technology. COMMERCIAL REAL ESTATE SECTOR SET TO DIPProperty markets have received significant attention as rising interest rates place the sector under mounting pressure. In the residential space the effects of these rate changes are already being felt, Mr Jamieson noted. "Anecdotally, from talking to my friends, we're all in our 40s - we've got our own families, we've got a high cost base at this point in our family lives - everybody knows it's going to be hard," he said. "I don't feel like anyone's really well set up for it yet. They just think that they'll make the adjustment if and when it comes." In the commercial property sector, however, some interesting themes are starting to take root. Mr Burgess noted that between higher interest rates and the 'work-from-home' revolution that started in COVID-19 lockdowns, office spaces may not be generating the same returns. The outlook for the sector remains negative, he added, and some investors are now looking at strategies to profit off this weakness. He cited Blackstone's newly launched US$30.4 billion distressed property fund as a prime example of this approach. Mr Burgess cautioned that while he expects prices for commercial property in Australia to continue falling, he doesn't think the downturn will be as pronounced as in past cycles. "There's not so much distress out there that people are going to have to give buildings away this time around." BONDS STAGE A RETURNThroughout the past cycle, Mr Burgess said, markets were plagued by "too much capital" chasing select stocks - with buy-now-pay-later businesses, speculative technology areas and video streaming giant Netflix both prime examples. This excess capital pushed distorted valuations and ultimately hurt returns. Mr Burgess said much of this excess capital has already "been washed out" of the market but cautioned "there's other areas that have yet to play out". With this in mind, Mr Burgess predicted a return to "good old-fashioned investing" where investors are wary of too much capital flowing into companies they're looking at. At the same time, Mr Burgess said investors are starting to look to government bonds as another option for their portfolios. "What I hear as a bond manager is that people are buying government bonds through gritted teeth, but bonds have gone back into some sort of normalised range," he said. "Now institutions are gradually allocating to bonds because they're starting to think it actually makes sense. The sharp rise in interest rates have made bonds quickly attractive again". The key to navigating the next 12 months, he said, would be to consider the current market with fresh thinking, weigh up which direction capital is flowing (and how much of it is moving), and using 'age-old' investing techniques to generate returns. True investment skill will finally be back in fashion he noted. * Reserve Bank of Australia, 'The Transmission of Monetary Policy: How does it work?', September 2017, accessed 20 April 2023.Author: Charlie Jamieson and Mark Burgess Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) References

|

17 May 2023 - Cashflow matching

|

Cashflow matching abrdn May 2023 In UK, the bulk purchase annuity (BPA) market has seen around £150bn of value transferred from pension schemes to insurers over the last five years. 1 Projections for the next decade suggest further transfers of over £500bn, fuelled in part by higher interest rates improving schemes' funding ratios. Although the backdrop may seem irrelevant in APAC, the capability to efficiently construct cashflow-matching portfolios is of increasing importance to both insurers and pension schemes in the region. In this article, we take a look at how novel portfolio construction techniques offered by asset managers can allow insurers and pension schemes to accurately match their liability cashflows whilst also ensuring their risk appetite and specific fund tolerances are fully considered. HolisticWith a holistic cashflow match framework, it is possible to optimally construct portfolios which offer desirable levels of yield, whilst reflecting all possible specific client specifications and restrictions. This includes clients who want their matching portfolio to meet the requirements for Matching Adjustment (MA) compliance under Singapore RBC 2 currently and the upcoming Hong Kong RBC. An investment manager can also offer pre-trade modelling and optimisation capability As well as portfolio construction, efficient ongoing portfolio management ensures assets also continue to be rebalanced and optimised throughout mandate life cycle. Later in this article we will examine the range of assets and different client specifications that can be embedded into a flexible portfolio construction and management framework. But first, what about risk appetites and tolerances? FlexibleA cashflow matching framework is centred around maximising the correspondence between the asset cashflows and the client's liability cash flow. The latter can be on best estimate basis, or based on guaranteed cash flow, depending on the nature of the mandate requirements. The asset cashflows may also include haircuts reflecting the imperfect FX hedge, necessary for example in matching adjustment mandates. It is through the additional constraints, however, that the portfolio can be tailored to meet client and regulatory requirements. For example, asset managers' tools can include:

Such a framework is flexible enough to meet any requirements or risk appetites. It's also important that asset managers work collaboratively to ensure clients' views and demands are fully reflected in the portfolio construction and on-going fund management tools. The full client life-cycle and all asset classesCashflow-matching managers are able to incorporate the full client life-cycle and a wide range of asset classes ensuring they are particularly well-placed to work with insurers and pension schemes. But what should these clients look out for in terms of manager skills, tools, capabilities and scale? The best teams benefit from a suite of proprietary, on-desk cashflow matching tools and use these to manage sizable matching portfolios in accordance with regulations in different jurisdictions . These tools aid portfolio managers and clients throughout the full lifecycle of such funds: *Initiation of mandates and fund restructuring e.g., a fund uprisking from government bond to credit or switching from credit to higher-rated supranational bonds whilst maintaining the match *Pre-trade modelling to ensure proposed new purchases and switches are suitable from a cashflow matching or on-going matching adjustment compliance point of view. *Portfolio rebalancing/liquidity management to meet cash requirements in and out of the fund. With a fast growing MA market and a limited supply of eligible public securities in local currency, it's a key requirement for MA portfolios to widen the scope of asset classes in order to continue to offer attractive solutions within a competitive market place. As such, in addition to local currency investment grade fixed income securities, best-in-class cashflow matching solutions can include overseas debt, e.g., USD corporate bonds, paired together with cross-currency swaps or repackaged up as a special purpose vehicle. It's a key requirement for Muli-Asset portfolios to widen the scope of asset classes The capability to model private placements, commercial real estate loans, and infrastructure bonds is also crucial. Naturally embedding such securities allows for efficient management of public credit alongside non-public debt within cashflow matched & matching adjustment mandates. Quantitative portfolio designIn short, proprietary quantitative portfolio design can be applied on a wide and diverse investment universe. This design may be tailored to meet clients' needs and constraints. Such a flexible and transparent process also allows for informed discussion between key stakeholders, enabling comparison of the relative merits of a spectrum of matching portfolios with different 'risk-return' profiles. To illustrate this point, we showcase such an 'efficient frontier' of matching adjustment compliant portfolios for a stylised liability profile and a public credit universe in Chart 1 and Chart 2 below. Chart 1 Matching Adjustment 'efficient frontier' constructed from the public credit universe. Typical portfolio issuer/sector /rating constraints. Liabilities c. 12y duration. Close of Business (CoB) 30-Dec-2022. A "Best cashflow match" portfolio with no yield constraint (meets various portfolio limits & MA CF-Match Tests). B Better yielding MA Compliant Portfolio (still meeting all limits & CF-M tests) C Pushing yield at the expense of cashflow match (portfolio only just matching adjustment compliant). Source: abrdn. For illustrative purposes only. Chart 2 Cashflow match plots for the three highlighted portfolios along the MA 'efficient frontier'. Stylised liabilities of c. £1bn PV (present value) and 12-year duration. All portfolios meet the required'Tests'. CoB 30-Dec-2022. Source: abrdn. For illustrative purposes only. The above portfolios also embed insurers' typical issuer, rating and sector limits and demonstrate the benefits of an optimisation exercise, potentially resulting in a 30bps gain in spread whilst retaining an acceptable quality of cashflow matching. A huge opportunity for insurers and pension schemesWith Hong Kong insurers embracing the upcoming Hong Kong RBC and Singapore insurers moving from RBC adoption to RBC optimisation, we are witnessing a trend in APAC similar to what has been ongoing among their European peers. Asset managers with proprietary techniques and insurance asset management capabilities could be well placed to support this journeys that lie ahead. Author: Mark Cathcart, Investment Director, Liability Aware |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund 1 Source: Professional Pensions, October 2022 |

16 May 2023 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

|||||||||||||||||||

| Ellerston Overlay Australian Share Fund | |||||||||||||||||||

|

|||||||||||||||||||

|

|

|||||||||||||||||||

|

|||||||||||||||||||

| Tribeca Vanda Asia Credit Fund - Founders Class | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

|||||||||||||||||||

| Avari Capital Partners - Private Loan Income Fund | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

|||||||||||||||||||

| Victor Smorgon Partners Global Multi-Strategy Fund | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

Want to see more funds? |

|||||||||||||||||||

|

Subscribe for full access to these funds and over 700 others |

16 May 2023 - 10k Words | May Edition

|

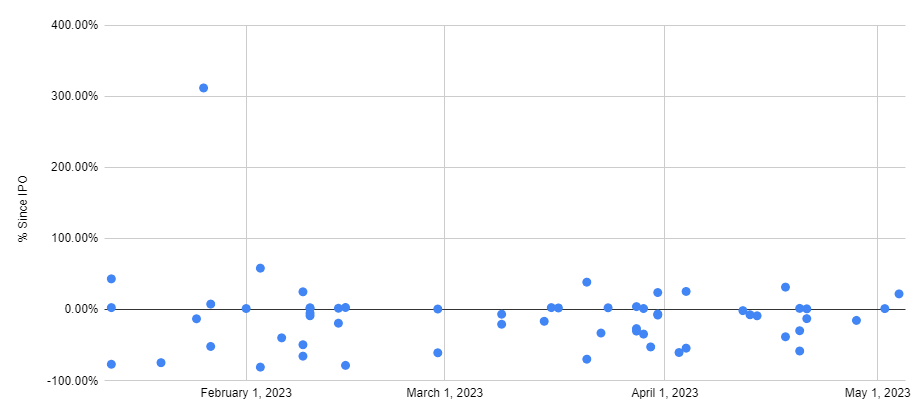

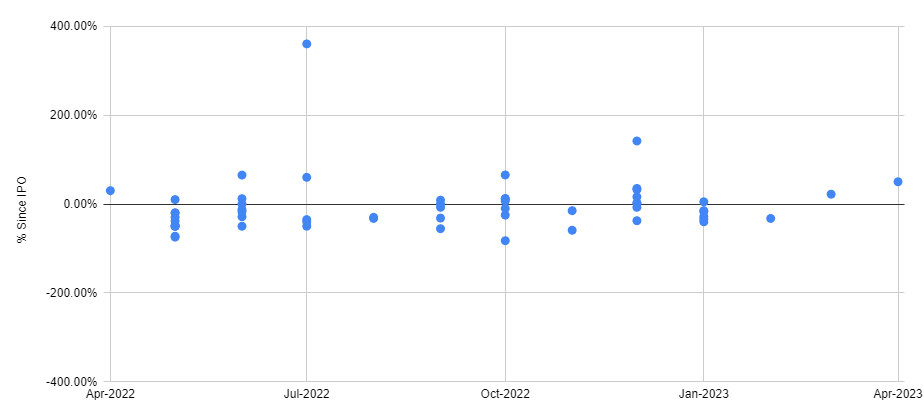

10k Words Equitable Investors May 2023 Miserable IPO returns have been the story even though Kenvue got away with a 22% stag on day one of its US listing last week; a gap has opened between small and large stocks with the "jaws" notable in both price movements and valaution comparisons; in that context it is interesting to see how smaller stocks have outperformed historically coming out of market drawdowns; in Australia the industry survey looks negative but S&P/ASX EPS revisions haven't really been notable; insolvency is on the rise as is US consumer credit card debt; and finally for whoever is advising the state fo Victoria, credit ratings do matter. Distribution of returns from US IPOs by issue date (2023 to date)

Source: Equitable Investors, StockAnalysis Distribution of returns from ASX IPOs by issue date

Source: Equitable Investors ASX small caps (SSO - orange) v large caps (STW - blue)

Source: Equitable Investors, TIKR US micro caps (IWC - orange) v large caps (IVV - blue)

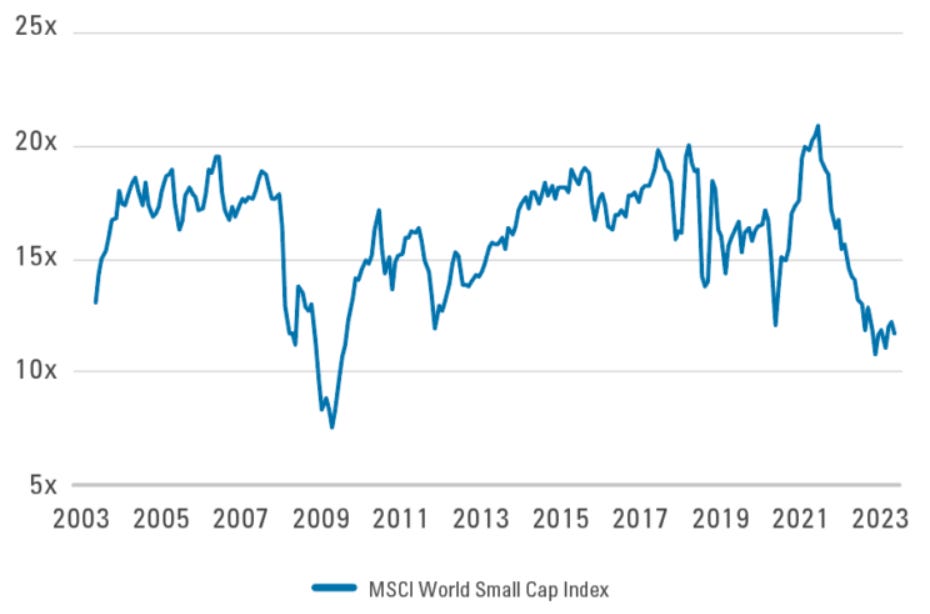

Source: Equitable Investors, TIKR Past 20 Years World Small Cap P/E Ratios

Source: Pzena Nasdaq 100 Price/Sales Ratio

Source: Charles Schwab & Co. US small caps v large caps during & after the "dot-com bubble"

Source: abrdn US small caps v large caps during & after the GFC

Source: abrdn S&P/ASX small v large during & after the "dot-com bubble"

Source: Equitable Investors, Iress S&P/ASX small v large during & after the GFC

Source: Equitable Investors, Iress AIG Industry Index

Source: IFM, AIG Consensus EPS expectations for S&P/ASX 200

Source: Cannacord Large bankruptcies ($US50m+ liabilities) - Jan-Apr count for 2023

Source: Bloomberg, @jsblokland Australian companies entering external administration for the first time (FY23 = black line)

Source: ABS US Consumer Loans (Credit Cards & Other Revolving Plans, All Commercial Banks)

Source: @glightfinancial, FRED Government Bond Yields and their S&P credit ratings

Source: Equitable Investors, worldgovernmentbonds.com May Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Nothing in this blog constitutes investment advice - or advice in any other field. Neither the information, commentary or any opinion contained in this blog constitutes a solicitation or offer by Equitable Investors Pty Ltd (Equitable Investors) or its affiliates to buy or sell any securities or other financial instruments. Nor shall any such security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. The content of this blog should not be relied upon in making investment decisions. Any decisions based on information contained on this blog are the sole responsibility of the visitor. In exchange for using this blog, the visitor agree to indemnify Equitable Investors and hold Equitable Investors, its officers, directors, employees, affiliates, agents, licensors and suppliers harmless against any and all claims, losses, liability, costs and expenses (including but not limited to legal fees) arising from your use of this blog, from your violation of these Terms or from any decisions that the visitor makes based on such information. This blog is for information purposes only and is not intended to be relied upon as a forecast, research or investment advice. The information on this blog does not constitute a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Although this material is based upon information that Equitable Investors considers reliable and endeavours to keep current, Equitable Investors does not assure that this material is accurate, current or complete, and it should not be relied upon as such. Any opinions expressed on this blog may change as subsequent conditions vary. Equitable Investors does not warrant, either expressly or implied, the accuracy or completeness of the information, text, graphics, links or other items contained on this blog and does not warrant that the functions contained in this blog will be uninterrupted or error-free, that defects will be corrected, or that the blog will be free of viruses or other harmful components. Equitable Investors expressly disclaims all liability for errors and omissions in the materials on this blog and for the use or interpretation by others of information contained on the blog |

15 May 2023 - Airlie Quarterly Update

|

Airlie Quarterly Update Airlie Funds Management April 2023 |

|

Emma Fisher, Portfolio Manager, provides her views on the current market environment and discusses her recent trip to Europe where she visited CSL and QBE Insurance, which are two holdings in the Airlie Australian Share Fund. Author: Emma Fisher, Portfolio Manager Funds operated by this manager: Important Information: Units in the fund(s) referred to herein are issued by Magellan Asset Management Limited (ABN 31 120 593 946, AFS Licence No. 304 301) trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks.. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

12 May 2023 - Why investors shouldn't desert quality banks

|

Why investors shouldn't desert quality banks Pendal April 2023 |

|

Here, Pendal's head of global equities ASHLEY PITTARD makes the case for quality banks ahead of a likely US recession

THE turmoil among global banks over the past six weeks has created opportunities for investors, with Swiss based UBS and Wall Street giants JP Morgan and Wells Fargo the top picks, says Ashley Pittard, our head of global equities. "I think UBS is a standout for the next ten years as an investment," he says. "You want to invest in a bank that's one or two in its market, and has high quality management. "Bank stocks can go down in a crisis environment, but the quality banks don't go broke and that's a key point." Banks should do well in coming quarters as they reprice credit and achieve higher margins. "Near term, interest rates have stopped rising and the yield curve is flattish or even inverted. "But if we fast-forward through the year, we believe there's going to be a recession in the US. That would likely mean the Federal Reserve will have to cut rates into next year. "The yield curve will steepen and that's good for banks because they borrow short and lend long and they are going to get a wider spread. That will feed back in a couple of years' time into higher earnings." The current turmoil could push out weaker lenders who aren't pricing loans rationally - which would help the top banks. Short-term risks Pittard warns there are risks in the short term. "What are the write-downs going to be, particularly if the recession is hard? That's the big near-term risk. "That's why you want to be with the highest quality banks - number one or two in their market." On UBS, Pittard says its metrics are strong. It has just absorbed its second largest competitor, has a 30 per cent plus share in retail banking in Switzerland, and is the number one global bank for ultra-high net worth individuals. Importantly, UBS has strong management, he says. "The new CEO, Sergio Ermotti, is the Tom Brady of European banking," Pittard says, referring to most successful quarterback in US football. Ermotti left the bank in 2020 after a successful stint, and then took the top job again on April 5. "He first came to UBS after the global financial crisis and got them out of high-risk investment banking, increased market share in their ultra net worth business, and boosted dividends and the stock price. "He just grinds away. He gets costs out of the business, right sizes the riskier parts and gives money back to shareholders." Pittard says two US bank stocks worth looking at are JP Morgan, run by the very experienced Jamie Dimon, and Wells Fargo, run by Charles Scharf. "Dimon is the last remaining US bank CEO who actually went through the GFC," Pittard says. "Scharf got the CEO job at Wells Fargo in late 2019 and has cleaned it up and ticked all the boxes." In terms of why the global banking sector found itself in its current situation, there are several factors, Pittard says. "There were poor management practices. There's also been mishandling of the repricing of the rapid interest rate changes over the last year. You've also had volatility around what the US Federal Reserve is going to do." Pittard says there's also a regulatory overlay. "When Donald Trump was in power, he rolled back some of the banking regulations that were put in place directly after the global financial crisis which meant the regulation of smaller banks, like Silicon Valley Bank, was lighter than regulation of the big banks," Pittard says. "Also stress testing of the bank last year didn't consider large jumps in interest rates, which is what actually happened." Author: Ashley Pittard, Pendal's Global Equities |

|

Funds operated by this manager: Pendal Focus Australian Share Fund, Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Regnan Global Equity Impact Solutions Fund - Class R, Regnan Credit Impact Trust Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |