News

Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

The Skerryvore Global Emerging Markets All-Cap Equity Fund rose by +1.88% in March, outperforming the MSCI Emerging Markets (MMEF) AUD benchmark by +1.46%. Since inception in August 2021, the fund has returned +5.34% per annum, an...

Read more...

The Evolving Landscape of Fixed Income Investing

A key investment theme in recent years has been strong demand for corporate bonds. In particular, investors have favoured high-quality investment-grade assets, while demand for sub-investment-grade (high-yield) debt and private credit has...

Read more...

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund has returned +17.19% per annum since inception in June 2017, an outperformance of +8.92% relative to the ASX 200 Total Return benchmark which has returned +8.27% on an annualised basis over the same period.

Read more...

Performance Report: Bennelong Long Short Equity Fund

The Bennelong Long Short Equity Fund has returned +12.06% per annum since inception in February 2002, an outperformance of +4.00% relative to the ASX 200 Total Return benchmark which has returned +8.06% on an annualised basis over the same period.

Read more...

Everyone has a plan until they get punched in the face

"Know what you own and know why you own it."

Long-term investment success requires differentiated thinking supported by genuine conviction. At Canopy, we believe conviction cannot be borrowed or assumed; it must be built through...

Read more...

Source: FactSet, Canopy Investors.

Source: FactSet, Canopy Investors.

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) rose by +3.62% in March, outperforming the S&P Global Infrastructure TR (AUD) benchmark by +2.02%. Since inception in March 2016, the fund has returned +9.28% per annum, a difference of -0.83%...

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund rose by +24.10% over the past 12 months. Since inception in November 2017, the fund has returned +19.00% per annum, an outperformance of +10.94% relative to the ASX 200 Total Return benchmark which...

Read more...

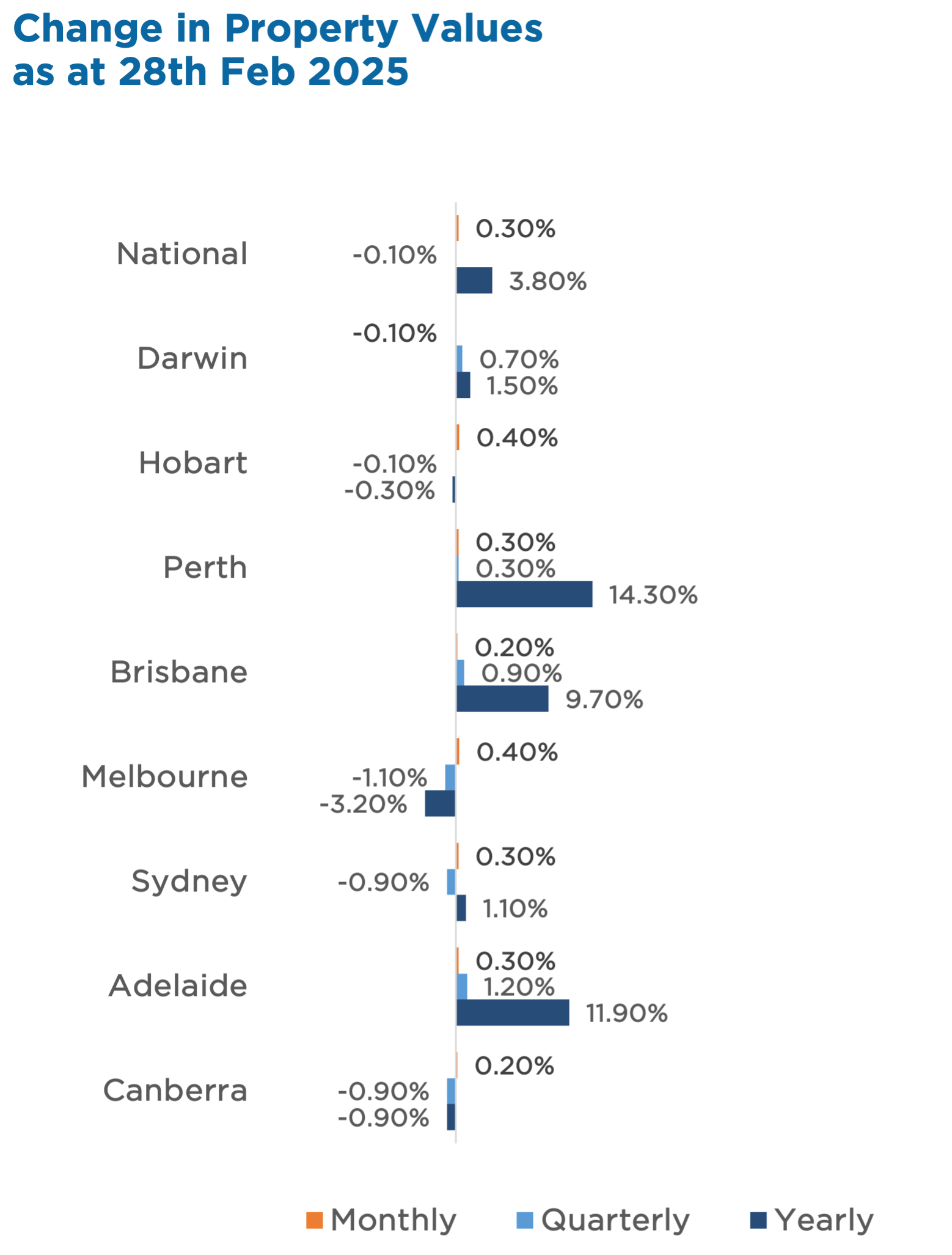

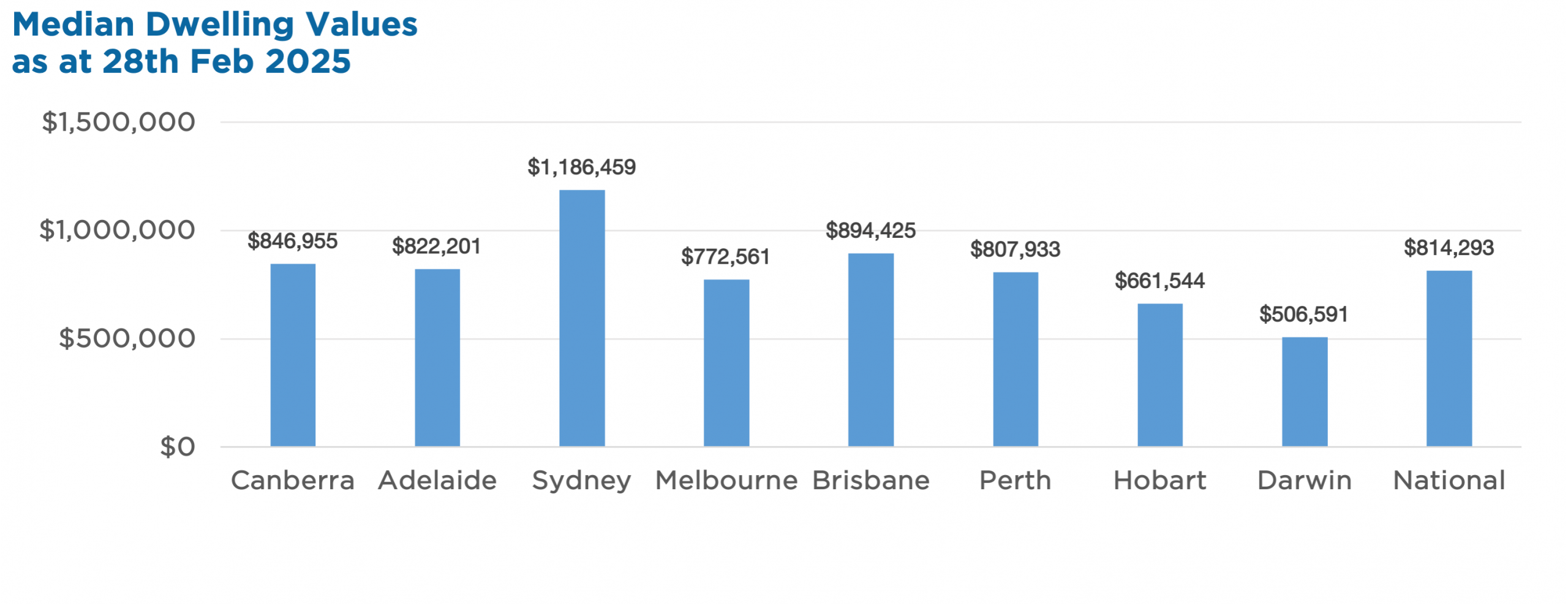

Australian Secure Capital Fund - Market Update

February marked a shift in Australia's housing market, with national home values rising 0.3%, ending a three-month downturn. Gains were widespread, with Melbourne and Hobart leading at +0.4%, while regional markets continued to outperform,...

Read more...

Manager Insights | Euree Asset Management

Chris Gosselin, CEO of FundMonitors.com, speaks with Winston Sammut, Property Director at Euree Asset Management.

Read more...

Hedge Clippings | 04 April 2025

It's difficult to add anything new to the commentary about Donald Trump's "Liberation Day" that hasn't already been said or written. Outside his immediate circle of acolytes, seemingly led by Commerce Secretary Howard Lutnick, we have...

Read more...