News

28 Nov 2023 - Acceleration of innovation now spells danger for investors

|

Acceleration of innovation now spells danger for investors Insync Fund Managers November 2023

A new app, 'Threads' built by Instagram, which enables the sharing of text updates and joining public conversations, recently reached 100 million users within an astonishing five days. 'This is a powerful demonstration of the lightning speed at which innovation is accelerating,' says Insync Funds Management (Insync)'s Head of Strategy and Distribution, Grant Pearson. 'Make no mistake, the frantic pace of change now spells danger for investors.' For context, Facebook took 4.5 years to reach 100 million users, Instagram took 2.5 years, TikTok achieved it in nine months, and Chat GPT took two months. 'The reason this means big trouble for investors is that they could be in the right company today and, as little as weeks later, be in the wrong company,' Mr Pearson says. The pace of innovation does not just affect pure technology plays. 'All companies could be affected as they all rely on technology of some sort,' he says. 'If their competition embraces new technology better and faster, a dominant company today may find its revenues and profits under immediate threat. And let's not forget brand new competitors for firms that technology has opened the gates to.' Mr Pearson says that while in the past investors had months or even years to discover an emerging technological breakthrough, assess it, seek views, and then act; now they have next to no time and the skills required to do it are often outside the investment industry. 'In fact, the average life span of successful businesses is being compressed into less than 10 years duration,' he went on to say. 'This is disruption accelerating at the same time that time frames are compressing.' Annual increases in computing processing power are now many hundreds of times faster than previous computers which are themselves under five years old. 'Look out further, say six years, and it's even more profound,' he says. 'Google's latest Sycamore Quantum Computer, testing now with operational status by 2029, is an astonishing 241 million times more powerful than today's fastest supercomputers!' In other words, Sycamore can solve in seconds a problem that takes today's fastest supercomputer 47 years. 'This first iteration of Sycamore is only the 'Model T' of what is to come,' Mr Pearson says. 'The alarming thing for the investment community is that we are only at the very beginning of this acceleration. It is akin to sitting in a roller coaster as it has just tipped into its near vertical first run.' Couple this extraordinary increase in power with the advances in AI and Mr Pearson says gargantuan change is afoot, change that will revolutionise our world and turn most industries upside down, along with investor returns. 'Fund managers and researchers need to quickly create robust means to assess and counter the acceleration of technological change and shrinking time frames, to reduce the threats to returns, as well as better understand which companies will deliver the decent performances of tomorrow,' he says. 'Our industry has a reputation for being slow to change, with egos routinely getting in the way of adapting. Investors need to check carefully that their fund managers are very clear as to how these factors impact their investment processes if they are not to be blindsided and saddled with disappointing returns.' Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

27 Nov 2023 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||

| EQT Tax Aware Australian Share Fund (Retail) | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| EQT Tax Aware Australian Share Fund (Wholesale) | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| EQT Tax Aware Diversified Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| EQT Diversified Fixed Income Fund (Retail) | ||||||||||||||||||||

|

||||||||||||||||||||

| EQT Diversified Fixed Income Fund (Wholesale) | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

|

||||||||||||||||||||

| Maple-Brown Abbott Australian Sustainable Future Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||

|

Subscribe for full access to these funds and over 750 others |

24 Nov 2023 - Where nature meets business: The TNFD framework.

|

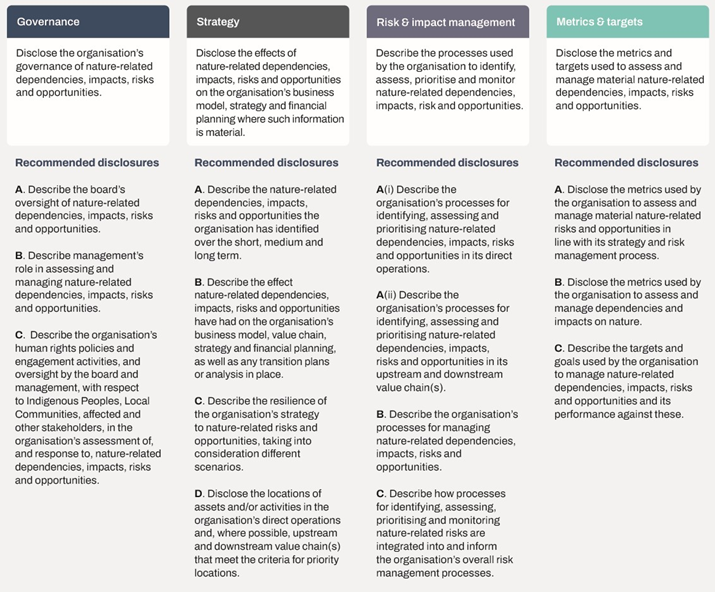

Where nature meets business: The TNFD framework. Tyndall Asset Management October 2022 The Taskforce on Nature-related Financial Disclosures (TNFD) is an international initiative that is developing a framework for companies and financial institutions to disclose their nature-related risks and opportunities. Climate and net-zero commitments are well understood, with corporations relying on the Taskforce for Climate-related Financial Disclosures that released a set of recommendations in 2017. The idea of TNFD is not entirely new. It has built upon the foundational success of the Task Force on Climate-Related Financial Disclosures (TCFD), which focuses on the financial implications of climate change for companies. However, as the global dialogue evolved, it became clear that climate was only a part of the broader environmental narrative. Biodiversity loss, land degradation, and ecosystem collapse pose significant risks to economies and businesses around the globe. The TNFD first came into existence in June 2021 to address this gap and ensure a holistic environmental approach in corporate disclosures. Importance of a nature-positive economyA 'nature-positive economy' is essential for a sustainable future and is a key concept that drives the TNFD framework. A nature-positive economy is an economy that has a net positive impact on nature, an economy that restores and regenerates nature rather than depleting it. Nature provides us with essential ecosystem services, such as clean air and water, food, and climate regulation. Without a healthy natural environment, our economy and society cannot thrive. The transition to a nature-positive economy is essential for a sustainable future. However, it is a transition that will require a concerted effort from all stakeholders, including governments, businesses, and individuals. The sectors that have the most impact on biodiversity are the logical companies that will be the early adopters of the TNFD recommendations. These sectors include materials, energy, agriculture and food & beverage. A framework for nature-based solutionsThe TNFD's final framework was published in mid-September 2023. It includes 14 recommended disclosures covering nature-related issues, impacts, risks and opportunities that are structured around four pillars (refer Figure 1). Figure 1: TNFD's recommended disclosures

Source: TNFD, Sept 2023. It is hoped that the TNFD provides a clear, structured framework that help corporates understand the implications of biodiversity and natural capital for their activities. The framework is intended to assist corporates and financial institutions manage their nature-related risks and opportunities, and to support the transition to a nature-positive economy. While it is largely based on the TCFD framework, it also considers the specific risks and opportunities associated with nature.

The TNFD framework is expected to be a valuable tool for companies and financial institutions to manage nature-related risks and opportunities. It will also help to promote the transition to a nature-positive economy. Some of the benefits of the TNFD framework include:

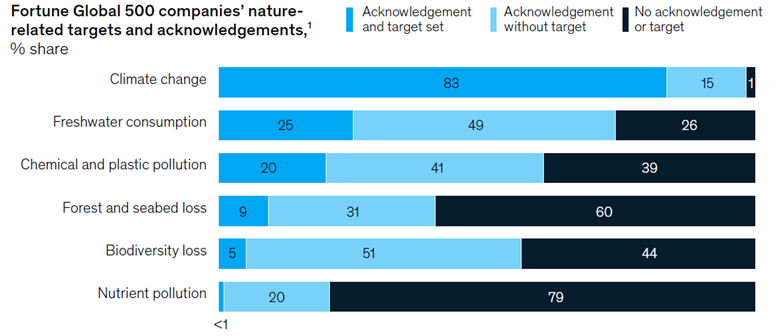

Global progressAlthough the TNFD framework has only recently been settled; governments and intergovernmental organisations have increasingly called attention to the impact on nature. Pleasingly, a rising number of businesses have made pledges relating to biodiversity. Figure 2: Corporate targets are less common for other dimensions of nature compares to climate change

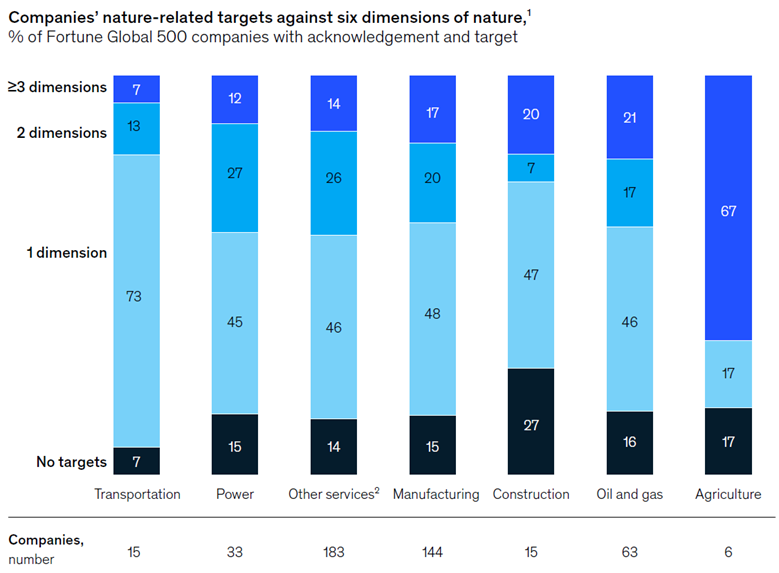

Source: McKinsey McKinsey has calculated that ~47% of Fortune Global 500 companies have set nature-related targets against one dimension of nature - generally this is against climate (refer Figure 2). Approximately 16% have set targets against three or more dimensions of nature and no companies have targets against all six dimensions that were looked at in this analysis. The Science-Based Targets for Nature (SBTN) initiative suggests that companies are more likely to focus on the key issues that directly impact their activities which could explain why no company has set targets against all six dimensions. Cutting the data based on a sector level reveals that the sectors that have a higher exposure to biodiversity risk are leading the charge on target setting. Figure 3: Fortune Global 500 Companies' nature-related targets by sector

Source: McKinsey Implementation of TNFDImplementing TNFD is not without its challenges. In particular, there's a need for:

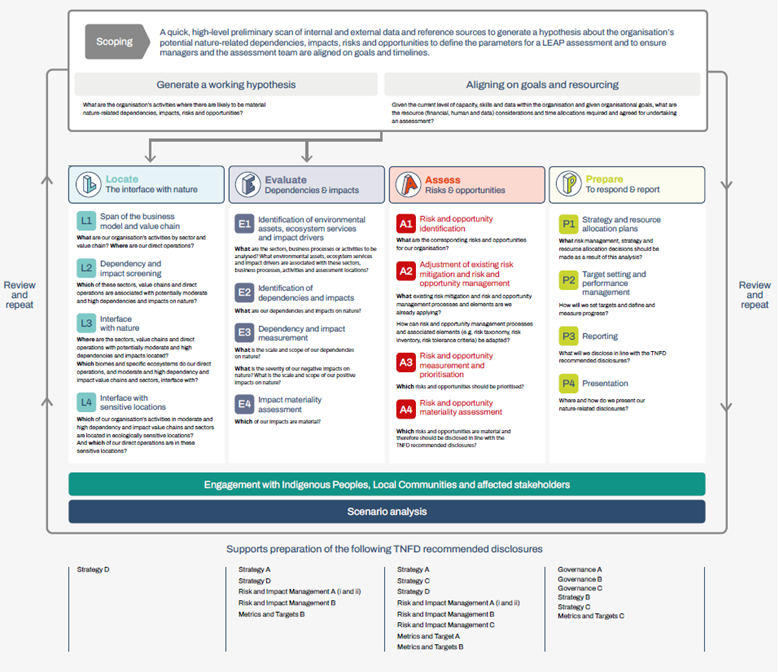

The framework is consistent with the recommended standards of the TCFD, ISSB (International Sustainability Standards Board) and GRI (Global Reporting Initiative). The recommendations have an intention to provide a practical solution for corporates to start their journey to increase the scope and disclosures over the coming years. The expectation is that, as with climate-related reporting, TNFD disclosures will improve over time. The LEAP approach - Locate, Evaluate, Assess and Prepare - has been developed by the TNFD to help organisations to identify, assess and manage nature-related risks and opportunities. While the approach is not a requirement, it is designed to help with identification and assessment. Figure 4 provides an overview of LEAP and its elements, which covers:

Figure 4: The TNFD approach for identification and assessment of nature-related

Source: TNFD, Sept 2023 Conclusion While the challenges are significant, the TNFD offers a critical pathway for integrating nature into financial decision-making and improving outcomes for our environment. The success of the TCFD suggests that with global cooperation and commitment, the TNFD can become an influential tool in driving sustainable business practices. Governments, financial institutions, environmental organizations, and businesses all have important roles to play. By implementing frameworks such as the TNFD, the global community takes a step closer to ensuring that the economic activities of today do not compromise the planet's well-being tomorrow. The shift from merely profit-driven strategies to those that also account for nature-related impacts signifies an evolution in global business practices. It is an evolution that is not just commendable but essential for the longevity and prosperity of both businesses and the planet. Tyndall will be increasingly engaging with corporates around biodiversity and promoting the implementation of the TNFD framework, as we have been with TCFD. According to work by Jarden, only 12 (24%) of ASX50 companies have nature-related targets. It was noted that BHP, Woolworths, South 32 and Origin Energy had undertaken TNFD pilots, and only Brambles and South 32 have linked nature to remuneration. Clearly, there is plenty of improvement required. We expect that those companies in sectors more exposed to nature-related risks such as agriculture, food and beverage, and mining, are likely to lead the charge. Author: Brad Potter, Head of Australian Equities Funds operated by this manager: Tyndall Australian Share Concentrated Fund, Tyndall Australian Share Income Fund, Tyndall Australian Share Wholesale Fund |

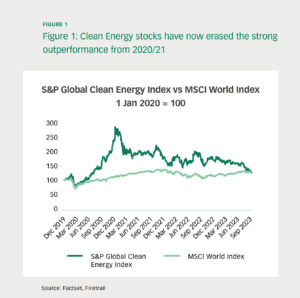

23 Nov 2023 - Renewable energy stocks: changing winds?

|

Renewable energy stocks: changing winds? Firetrail Investments October 2023 Decarbonisation is one of the most important challenges of our time, but it is also often one of the most difficult to successfully invest in. Renewable energy stocks have been among the most popular and talked about investments in recent years, thanks to low interest rates, government subsidies, and strong demand from consumers and investors who want to support a greener future. However, valuations of these stocks became very expensive, reflecting their current leadership rather than their future potential. In this article, we will explain why we have been cautious about investing in renewable energy stocks and where we see better opportunities in the energy sector. |

22 Nov 2023 - Stock Story: ResMed

|

Stock Story: ResMed Airlie Funds Management October 2023 |

|

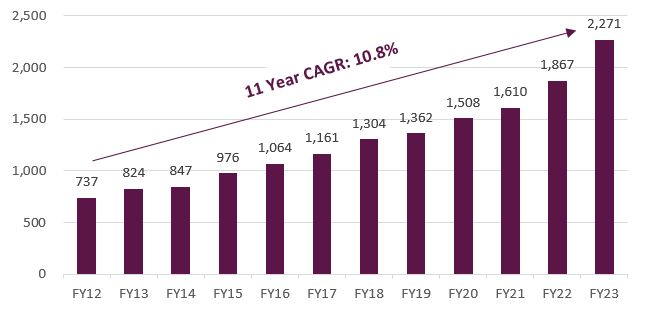

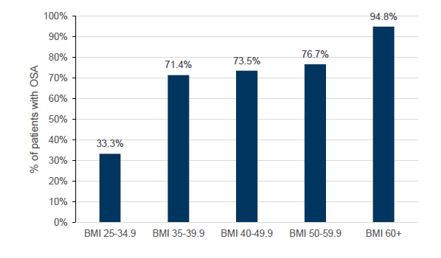

ResMed is the global leader in sleep and respiratory care primarily focused on the development and sale of positive airway pressure devices and accessories for the treatment of obstructive sleep apnoea (OSA). ResMed's share price has fallen 30% since the release of its FY23 results in August largely in response to concerns GLP-1 (Glucagon-Like Peptide-1) drugs may reduce its addressable market. In this article, we discuss the business in more detail and why we think the GLP-1 concerns are overdone. What is Obstructive Sleep Apnoea (OSA)?Obstructive sleep apnoea is a chronic illness that occurs when the muscles that support tissues in the back of the throat relax during sleep, blocking or narrowing the upper airway. This obstruction leads to impaired breathing for a short period (usually 10-20 seconds), which results in lower oxygen in the blood. The brain senses the impaired breathing, causing the individual to subconsciously rouse from sleep in order to reopen the airway. The severity of OSA is characterised by the number of events per hour: Normal < 5; Moderate 15-30; Severe > 30. Continuous Positive Airway Pressure (CPAP) devices are the accepted standard of care for treating OSA, delivering a stream of pressurised air through a mask to prevent the collapse of the upper airway during sleep. ResMed is the largest manufacturer of these products and we estimate the company currently has ~80% market share with its major competitor Philips out of the market for the past two years due to an FDA-imposed product recall. Large, undiagnosed addressable marketThe OSA market is large and mostly undiagnosed. According to the company, there are 936 million people globally with sleep apnoea and 424 million of these suffer from severe sleep apnoea. The size of the addressable market is evidenced by the fact ResMed had grown its device revenue at over 9% p.a. in the six years prior to the Philips recall (FY13-FY19). Recent growth rates have been even higher. ResMed estimates that penetration currently sits at 20% in the US and well below this percentage globally, which implies a long runway for future device and mask sales. Figure 1 - ResMed device revenue (US$) One of the highest-quality companies on the ASXAs with any new position, we tested ResMed against our key investment criteria and consider the business to be high quality based on the following factors:

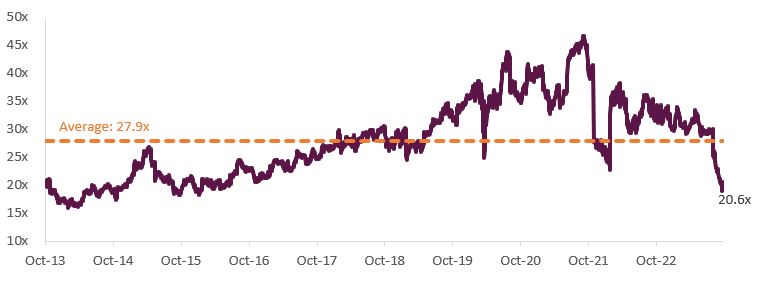

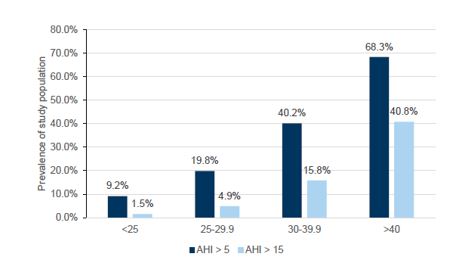

GLP-1 concerns and valuationResMed has historically traded on a forward multiple of 28x PE but is currently trading on less than 21x PE due to market concerns about GLP-1 drugs reducing ResMed's addressable market. Figure 2 - ResMed NTM Rolling PE GLP-1 drugs (branded as Ozempic, Wegovy and Mounjaro) act by mimicking hormones that are released into the gastrointestinal tract in response to eating. These drugs were initially developed to target type 2 diabetes by stimulating more insulin production but have evolved to potential applications in weight management and cardiovascular indications. Given obesity is a key risk factor for OSA (see Figures 3 and 4), there is a view that significant weight reduction from taking GLP-1s may result in reduced demand for CPAP therapy. Figure 3 - OSA severity by AHI (>5 mild) and (>15 moderate)

While we are not medical experts, we consider the significant de-rate to be an overreaction for the following reasons:

ConclusionOverall, we think the uncertainty as to the potential penetration and success of these drugs in treating OSA has created a rare opportunity to invest in one of the highest quality companies on the ASX. While we are unlikely to pick the bottom, we believe the company is trading well below its intrinsic value. By Vinay Ranjan, Senior Equities Analyst Funds operated by this manager: Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Airlie will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

21 Nov 2023 - Investment Perspectives: What does 'higher for longer' mean for real estate?

20 Nov 2023 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

|||||||||||||||||||

| EQT Cash Management Fund | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

| EQT Mortgage Income Fund (Wholesale) | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

| EQT Mortgage Income Fund (Retail) | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

|

|||||||||||||||||||

| Euree A-REIT Securities Fund | |||||||||||||||||||

|

|||||||||||||||||||

| Euree Multi Asset Balanced Fund | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

| Euree Multi Asset Growth Fund | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

Want to see more funds? |

|||||||||||||||||||

|

Subscribe for full access to these funds and over 750 others |

17 Nov 2023 - Good things come to those that wait

|

Good things come to those that wait Devon Fund Management October 2023 After a challenging few months, stock markets have started November brightly. With inflation getting under control, many central banks cooling their jets, and bond yields easing, are equity markets in for a strong end to 2023? If October was meant to be the "Bear Killer" month, it certainly didn't pan out that way. The month started brightly enough with the end of the debt ceiling standoff in the US, but the Israel/Hamas conflict came from left field and added another dimension to go with existing market uncertainties. Bond yields rose, with the US 10-year hitting the highest level in 16 years, despite many central banks pushing pause. The European Central Bank joined other majors in going on hold after 10 consecutive increases. Inflation prints meanwhile continued to be generally lower than expected, while economic data was broadly positive, as was the earnings season in the US and Europe. Nonetheless, markets continued to soften in October. The Dow Jones and the S&P500 declined 1.4% and 2.7% respectively during the month, marking the first three-month losing streak for both indices since March 2020. Europe and Asia were similarly weak. The falls in New Zealand and Australia were more pronounced. The NZX50 fell 4.8% to hit a 16-month low, while the ASX200 dropped 3.8%, back to the levels of a year ago. November has started off much brighter. As is (usually) the case with October, historically speaking, November is also seen as a strong month for markets, with seasonal tailwinds often featuring in a year-end rally. Whether this transpires may depend on what the bond market does, and on any messaging that rates may not be higher for longer. There are some hopeful signs at the start of this month, with the Federal Reserve leaving rates at a 22-year high for the second straight meeting, but with the language at Jerome Powell's post-meeting conference being interpreted by many that the central bank is "done" with rate hikes. While the year has not panned out particularly well for the NZ share market to date, there are also some positive tailwinds in the air. The switch to a right-leaning government appears to have already boosted business sentiment, while a lower-than-expected inflation print and tick-up in the unemployment rate could well mean that a rate hike is off the table when the RBNZ meets later this month. Across the Tasman it is a slightly different story with the CPI and retail sales both coming in hot at the last prints. While developments in the Middle East were a new factor for investors to consider in October, it was the rise in bond yields that provided the main headwind. Oil prices initially surged to US$95 following the incursion by Hamas, but have since settled back to where they were in September. Safe havens such as gold and cryptos rallied on rising geopolitical tension, but the oil market is not suggesting the conflict will broaden within the region. The view that rate hikes were near an end was not disrupted during the month, but the length of time they would remain elevated was. The "higher for longer" narrative provided a complication to investors buoyed by falling rates of inflation and many central banks hitting the pause button. The Fed though has perhaps provided some cause for comfort over the past week in holding the Fed Funds Rate in a target range between 5.25-5.5%. While there was no commitment to officials being "done" with further rate hikes, there were some subtle changes to the language used in the accompanying statement, while Jerome Powell suggested at the press conference that monetary policy was "sufficiently restrictive." Bond yields dropped away in the aftermath. Officials upgraded their assessment of the economy while noting that inflation (while elevated) was still falling. The Core Personal Consumption Expenditures price index, the Fed's favoured inflation gauge, increased 3.7%, the first sub-4% reading in nearly two years. Recent quarterly GDP numbers were robust, and the Fed changed its description of the economy from "solid" to "strong." All heading in the right direction. The Fed remains in data-dependent mode but also noted the dual-sided risks to the economy, with previous rate hikes likely to have a dampening impact.

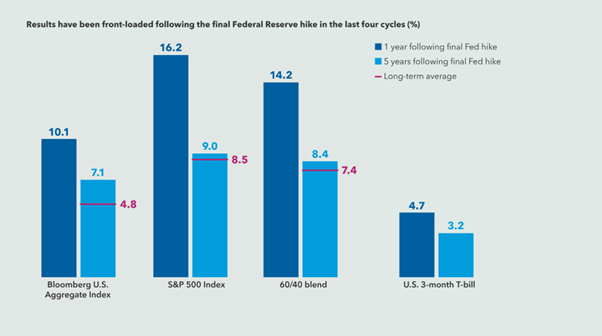

September and October proved challenging months for markets as bond yields climbed, but sentiment has turned sharply with November underway. Yields have backed away from recent highs, with the US 10-year back at 4.67% in early November after hitting 5% last month. Data released recently has given further credence to the narrative that inflation is easing, and the labour market is slowing (the cost of labour declined in the third quarter and October job additions have come in below expectations), boosting the scenario that the Fed is done with rate hikes. This would be a highly significant milestone, given the strong performance of markets in the year following the final Fed hike over the past four cycles.

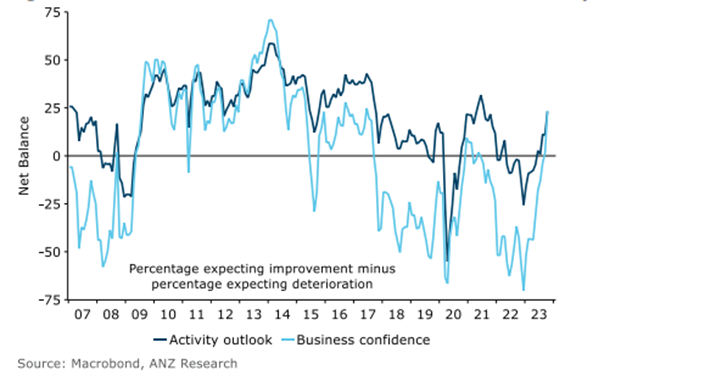

The 10-year Treasury yield hit the highest level since 2007 during the month and one area which was impacted significantly was high PE growth stocks. The tech-laden Nasdaq fell nearly 3% and had its third consecutive negative month. Super-cap tech stocks particularly the "Magnificent 7" (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) have had a big say in proceedings this year, given they account for around 30% of the S&P500. It has been a mixed bag in terms of reporting, with strong results but differing outlooks amongst the constituents that have reported to date. Alphabet, Meta and Tesla were somewhat downbeat, while Amazon and Microsoft were in the more positive camp. In recent days Apple has beat on earnings, but given a weak outlook. Nvidia reports later this month. Share price performances from the mega-cap group have been contrasting. Tesla fell 20% in October, while Nvidia and Alphabet have also underperformed the benchmark. AI has been one driver behind the blue sky that has been priced into some of the 'M7' names, meaning there is a lot to live up to in terms of valuation, and leaving these names prone to any 'imperfect' news. There have been reports that Nvidia may have to cancel billions of dollars in orders from China due to tighter US controls. Alphabet's CEO has meanwhile been in court, conceding that agreements making Google's search engine the default on smartphones and browsers can be "very valuable." Google is involved in the most significant monopoly trial in 25 years. The big super-tech names have a lot to live up to, and time will tell if any become "Maleficent" from a share price perspective. Two of the M7 however put in strong gains in October - Amazon and Microsoft. Strong results from both were matched by upbeat outlooks. Microsoft, the top holding in the Devon Global Sustainability Fund, rose around 7%. The company's Azure cloud segment is performing robustly and anticipation is building around the growth potential of Microsoft 365 Co-pilot. With the earnings season roughly three quarters through, nearly 80% of S&P500 companies that have reported to date have beaten earnings, above the 5-year average, although only around 60% have done so on revenues. This in part reflects a slowing economy, but also that margins have been resilient amidst cost-cutting. The overall share price reaction though has been heavily weighted towards what management teams have said about the outlook. Older economy stocks have mostly been positive from a reporting perspective. Results from the banks were well received, although there have been disappointments. Some companies are also handling an inflationary environment (and other challenges) better than others. Sales at McDonald's, Coca-Cola and Starbucks have been relatively inelastic as the companies have been putting up prices. The spotlight on obesity (with new wonder drugs) has also yet to have an impact where you expect it might. Consumers in the world's largest economy may be trading down but are still spending on necessities. This was also evident in knockout results from streamers Netflix and Spotify. There hasn't been too much in the way of corporate results in New Zealand, but there was an election result. There has already been some feel-good news from the business sector, with the ANZ Business Outlook showing that business confidence jumped 21 points to +23 in October. The reading is the highest level since mid-2017 when National was the government. While inflation expectations didn't fall, reported wage increases versus a year earlier dropped to 4.9% - that's the lowest read since March 2022. NZ First is now playing a role in the government, but it appears the election result is rubbing off on business optimism. The question now is will there be follow through?

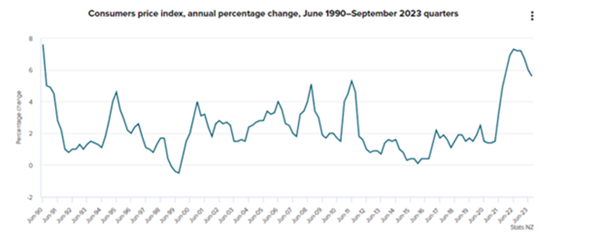

There was some good news on inflation during the month, which came in lower than expected in the September quarter. Annual CPI came in at 5.6% in the 12 months to the end of September, which was down from 6% in the three months to June. Consensus expectations were around 5.9%-6.0%, while the RBNZ forecast in the August MPS was 6%. In the quarter the CPI rose 1.8% which is below the RBNZ's forecast for 2.1%. Inflation is cooling with non-tradeable (domestically driven) inflation also coming down.

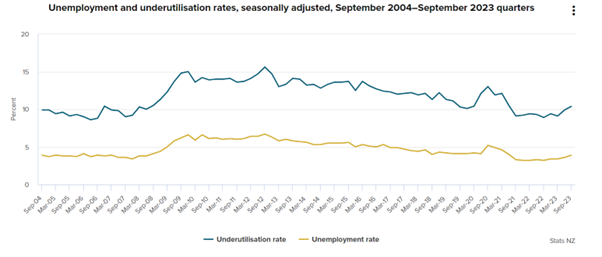

Inflation is at the lowest level in two years, which has reduced the prospect of another rate rise by the RBNZ (the next meeting is at the end of this month), as has a slight easing of pressures in the employment market. New Zealand's unemployment rate lifted to 3.9% in the year ending September, from 3.6% previously. This is materially higher than the 3.2% low in September 2022. The underutilisation rate lifted to 10.4%, up 0.5% from the previous quarter, and from 8.9% the previous year. Underutilisation is a broader measure of spare labour market capacity than unemployment alone. The employment market has been too tight, but things appear to be turning, and arguably heading back towards the "maximum sustainable level" targeted by the RBNZ.

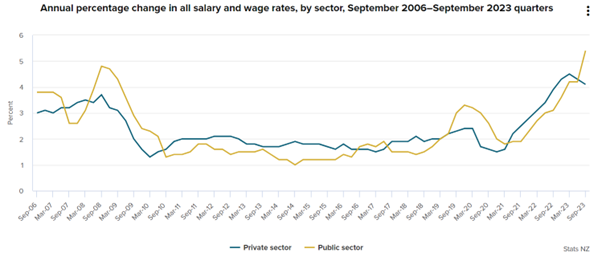

Meanwhile, wage growth is easing, at least in the private sector. The Labour Cost Index was 4.3% in the year to September 2023, unchanged from the previous quarter. Salary and wage rates for the public sector increased 5.4% annually, the highest rate since the series began in the December 1992 quarter. This has been influenced by collective agreements for teachers, nurses, and the NZ Defence Force over the past year. These settlements won't though be an ongoing feature.

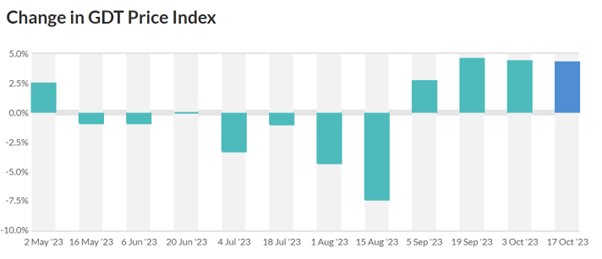

Confirmation that the RBNZ (along with many other major central banks) is also "done" with further rate hikes would be well received across the corporate sector, and the market generally. We are starting to see signs of this being acknowledged with markets rising in the early days of November. China, NZ's biggest customer meanwhile remains an unknown, but a key area of the economy - the dairy sector - is already seeing tailwinds. Milk prices have risen at the last four auctions. This could have positive trickle-down impacts on the NZ economy.

Source: Global Dairy Trade It is a slightly different story in Australia. The RBA noted at its last meeting that keeping rates on hold was a close call. Since then, two key pieces of data have boosted the case for a rate hike on Melbourne Cup day. Third-quarter inflation was stronger than expected with the CPI rising 5.4% year on year, above expectations for around 5.3%, but down from 6% in the second quarter. Core annualised inflation was up 5.2% against a forecast of 5%. This is while new Governor Michele Bullock has reiterated that officials have a "low tolerance" for a slower return of inflation to the RBA's target range.

Source: ABS The Aussie retail sales print for September was also hotter-than-expected. Retail turnover rose 0.9% month on month, around triple consensus forecasts. August and July numbers were revised upwards. Department stores and household goods were key drivers, which flies in the face of downbeat consumer confidence. We have also seen similar upbeat comments at AGM updates from several big Aussie retail names. Perhaps a resurgence in the housing market has helped liven spirits. CoreLogic data showed Aussie house prices increased further in October, underpinned by strong demand from migrants and foreign investors, amid a tight rental market. Sydney house prices are up 9.1% on a year ago, while those in Perth have jumped 11%. The broader fortunes of Australia, like NZ, remain closely tied to those of China. A rise in iron ore prices (which were already elevated from a historical perspective) in recent weeks suggests that the outlook has improved here. Once again the past month delivered a major surprise for investors to contend with. The promise of the final two months of the year being much better is however gaining credence. The soft-landing scenario remains alive and well, particularly with many central banks coming to the end of their rate-tightening programs. After a tough 2022, history is on the side of 2023 finishing positively. Uncertainty though still abounds in a number of areas, making for a productive environment for astute, active investors.

Funds operated by this manager: Devon Trans-Tasman Fund, Devon Alpha Fund, Devon Australian Fund, Devon Diversified Income Fund, Devon Dividend Yield Fund, Devon Sustainability Fund |

16 Nov 2023 - China and India's contrasting inflation front

|

China and India's contrasting inflation front Nikko Asset Management October 2023 The implications of inflation Inflation--the increase in the general price level of goods and services in an economy over a timeframe--has become one of the most closely watched economic gauges in recent years as consumer prices hit record highs. Besides bearing significant influence on standards of living, economic growth and the direction of interest rates, inflation also has significant implications on the top-down development of countries as well as the bottom-up fundamentals of companies. On a top-down basis, inflation signals the strengths and weaknesses in the overall economy and drives the policies and responses of governments and central banks, either being supportive or restrictive. From a bottom-up perspective, inflation signals whether certain industries have the pricing power to pass on the changes in costs and to generate sustainable returns from future investments. In other words, inflation encapsulates changes in both the overall economy and the operating metrics of a company. Moreover, inflation can have political implications, particularly in the developing world, as it is often a key issue in elections and can impact the popularity of elected politicians. That is why investors in the emerging markets often pay close attention to the general development of consumer prices, plus the outlook of inflation. Indeed, how a government navigates inflation often affects future investment returns. In this article, we compare and contrast two of emerging Asia's largest economies, China and India, through the lens of inflation. Today, China and India face opposite inflationary pressures, which could alter the outlook for these two large emerging economies. Inflation in China is close to zero, while that of India is above 6% (as of August 2023). Year-to-date (YTD), as at end-September 2023, the renminbi has depreciated more than 5% against the US dollar (USD), whereas the India rupee is flat versus the greenback. Equity markets also seem to be rewarding one and punishing the other; Indian equities (as measured by the MSCI India Index) were up 8.0%, in USD terms, on a YTD basis (as at end-September 2023), while China stocks (as measured by the MSCI China Index) were down 7.3% YTD. China faces deflationary pressures Let us begin with a close look at China. Concerns that China could be facing a deflationary spiral arose when the country reported that consumer inflation dropped by 0.3% YoY in July, the first decrease since February 2021. Since then, consumer prices in the world's second largest economy have moved higher, rising by 0.1% YoY in August, allaying fears a persistent deflationary trend in the nation. Headwinds from falling property prices and the decline in construction activity due to its ailing real estate sector are likely to cause more lingering deflationary pressures, in our view. Very low inflation or deflation can directly impact consumer behaviour. First, it can lead to a decrease in consumer spending as consumers may delay purchases in anticipation of lower prices in the future. This can lead to decreased economic growth and job creation. Second, low inflation can compound the debt burden. As the real value of debt increases due to the lack of inflation, this could lead to increased financial stress for households and businesses. At the same time, low inflation can discourage investments as investors may seek higher returns in other countries with higher inflation rates. And if subdued inflation persists for an extended period, it can lead to a deflationary spiral where prices continue to fall, potentially leading to a long-term economic stagnation. The big picture is that Chinese economic growth has been on a declining trajectory since the 2008 Global Financial Crisis (GFC). Having said that, if China were to achieve its government's targeted GDP growth of 5% for 2023, that would still be a decent result for a maturing economy (see Chart 1 for China's real GDP growth, inflation and real interest rates). Chart 1: China's real GDP, inflation and real interest rates

Source: Bloomberg, August 2023 More broadly, China currently faces several structural issues. It has negative population growth, a heavy debt burden in certain areas (namely property), an oversupply of goods, weak export markets and tight monetary policy. China's monetary policy has historically been on the tighter side, averaging 3% in real interest rates. Despite its recently flagging economy, China's current real interest rates still stand at 3%. There have been times when real rates in the country were lower, such as during the GFC and around the period of global economic weakness of 2015. This time around, the People's Bank of China (PBOC) is using alternative measures, like cutting mortgage rates incrementally and reducing banks' reserve requirements to boost overall liquidity. In our view, the Chinese government and the PBOC need to do more to stimulate the economy. Monetary policy loosening at a drip-feed speed is not creating a positive environment for the Chinese markets. Indeed, consumer and investor confidence in China is fading. Portfolio flows are negative and foreign investors are net sellers of Chinese equities. Nonetheless, it is not all bad for the world's second largest economy on the inflation front. One of the positives is that China is still seeing some inflation on the services side, which accounts for 40% of the inflation basket. Services-related inflation is rising at 1.3% on average, compared to overall consumer inflation at 0.1% YoY (as at August 2023). Historically, China's services-related inflation had hovered between 2-3%. During the COVID-19 lockdowns, it fell below zero. A rise in services consumer price index (CPI) is good for the overall inflation picture in China, which is growing more slowly in recent years and whose growth is largely due to government spending. All in all, China needs inflation to move higher. Higher commodity and agriculture prices could lead spur Chinese inflation Going a step deeper into the drivers of inflation in China will show that agriculture prices (namely those of soybean and pork) and commodity prices (including hydrocarbons, which are the main components of oil and natural gas) are closely related to the direction of inflation in the country (see Chart 2). As such, rising commodity prices and higher agricultural prices could pose an upside risk to inflation in China. A surge in China's inflation in 2019, for instance, was partially attributed to the outbreak of swine flu in 2018, which caused an increase in pork prices amid a drop in supply. Chart 2: China's inflation and commodity prices move in tandem

Source: Bloomberg, August 2023 COVID-19 further distorted the time series of inflation in China. Since the country's re-opening earlier in 2023 (and the absence of disease or other disruptions to supply), agriculture consumer prices look to have bottomed. Agriculture inflation in China is trending around 2% and could lift overall Chinese CPI. The same is true of rising commodity prices. Oil prices have recently risen above USD 90 per barrel. China imports around 59% of its oil needs, making it the largest oil importer globally, and higher oil prices will support inflation in the country. There is, however, a risk of stagflation if rising commodity-driven inflation is accompanied by low growth. Indeed, without productivity gains or other spending increases, inflation without growth for China may be problematic for the world's second largest economy. Chinese inflation and its impact on equity markets The Chinese equity market, as measured by the MSCI China Index, is trading close to the lowest price earnings (PE) multiples in 20 years, with very low growth priced in by the market. During the 2010-2015 period, equity valuations in China fell with declining inflation. Over that period, the market return in China averaged 1.5% on an annualised basis. Without dividends, it was negative. Today, China is once again experiencing a period of low and declining inflation, which coincides with the downturn of its equity market. However, if Chinese inflation starts to rise due to higher agriculture and commodity prices and looser monetary policy, we do expect a better showing for China stocks. This is because corporate sales and earnings per share (EPS) growth rates tend to have a positive correlation with inflation (see Chart 3). Chart 3: China's corporate sales and EPS growth are positively correlated with inflation

Source: Bloomberg, August 2023 Earnings growth in China has been decelerating since 2005 and hit bottom in 2016, when China implemented a massive monetary stimulus that lifted global equity markets and Chinese earnings. The effects of that stimulus have worn off, and the Chinese equity markets are now back to the lows of 2016. Chinese earnings growth is in a difficult position; it needs a forthcoming and large stimulus, which, in turn, will help lift inflation in the country. After China's last set of quarterly results, earnings revisions for 2023 and 2024 were negative; growth expectations, though positive, are also falling. We have looked at the annualised three-year sales growth of corporate China, working under the assumption that it takes time for inflationary pressures to work through a company's operations. Our expectations are for Chinese inflation to rise to 2% in 2024 and sales growth to follow suit. If that materialises, it would be a good result for Chinese earnings growth. All things considered, the Chinese equity market needs a source of higher profitability, and rising inflation, amongst other factors, could be key to invigorate profit levels. India at a sweet spot Viewed through the lens of Inflation, India is at the opposite end of where China is. India's Inflation, while above the Reserve Bank of India (RBI)'s target of 4%, isn't looking too elevated, as compared to its historical averages. Inflation in India has slightly eased to 6.83% YoY in August (from 7.44% in July) and is currently in line with the country's average annual inflation rate, which over the past few decades has been around 6-7%. As we see it, the Indian central bank remains accommodative, keeping real rates close to zero. The country's political climate is pro-business. The government of Indian Prime Minister Narendra Modi is in its third year of running large budget deficits, and with the coming general elections in 2024, the administration is unlikely to tighten its budget strings in the foreseeable future. At the same time, high oil prices have yet to hit the Indian economy, which is still relying on cheap Russian oil. India's annual GDP growth has hovered steadily in recent years, generally between 6% and 10%, while inflation has moved around the same levels as GDP growth (see Chart 4). India is in a sweet spot at the moment as inflation is trending lower, yet it is at a faster rate than GDP growth. Chart 4: India's real GDP, inflation and real interest rates

Source: Bloomberg, August 2023 The RBI tends to keep a closer eye on real GDP growth than inflation. In times of rising real GDP growth, the central bank has tightened monetary policy and loosened policy during periods of declining GDP growth. Expectations are for the RBI to continue to be accommodative, given that there are elections in 2024. Future agriculture prices key to India's inflation India's inflation basket is heavily weighted towards food, which makes up almost 37% of the CPI basket, while fuel comprises 5-6% of the total. Agriculture prices, on a YoY basis, have flattened, giving respite to inflationary pressures in India (see Chart 5). If there are any shocks to the global food supply, from either an escalation of the Ukraine-Russia war or from weather-related events, that could be a potential risk to inflation in India. Overall commodities, though rising largely because of higher oil prices, do not have that much of an impact on inflation in India. Chart 5: India's intertwined Inflation and commodity prices

Source: Bloomberg, August 2023 The Indian equity market and its link with inflation In India, the earnings yield, which is the inverse of the PE multiple, tends to move in tandem with inflation. During the commodities super cycle at the turn of the century, the Indian stock market did very well as inflation trended higher and valuations rose. Today, the environment looks similar. Inflation is high, growth expectations are rising and the market is starting to perform well. India's earnings growth, which is reaching historic highs, could mean persistently higher inflation. However, stand-alone valuations in the country are not excessive and rising rates haven't dampened investor sentiment. Relative to cash, equity valuations look fair, our view. Likewise, sales and earnings growth in India, historically, have had a fairly good relationship with inflation. In the post pandemic period, we have seen a divergence, however. Inflation has flattened and is expected to decline over 2024, while both sales and earnings are expected to continue to rise. Still, we reckon that if the country's sales and earnings were to remain strong in 2024, that would be supportive of higher rather than lower inflation. All in all, the Indian equity market looks well-placed with inflation under control, supportive monetary and fiscal policies. And with investors looking for alternatives to China, the uptrend in the India equity market could last for a while. Overall, the Indian equity market is pricing in a longer growth cycle; earnings growth expectations remain high, while strong macro tailwinds should continue to support the corporate sales and earnings rebound. Key takeout

Author: Mohammed Zaidi, Investment Director Funds operated by this manager: Nikko AM ARK Global Disruptive Innovation Fund, Nikko AM Global Share Fund Important disclaimer information |