News

13 May 2025 - Performance Report: Airlie Australian Share Fund

[Current Manager Report if available]

13 May 2025 - The Future of Travel: How AI-powered travel agents are revolutionising the industry

|

The Future of Travel: How AI-powered travel agents are revolutionising the industry Magellan Asset Management April 2025 |

Planning and booking travel has long been a frustrating and time-consuming process. Travellers must sift through countless flight and hotel options, read reviews, juggle different booking platforms and coordinate schedules - all while trying to secure the best deals.However, the future of travel is about to be transformed by a new technological force - AI-powered travel agents. Unlike traditional AI, which waits passively for instructions from users, AI agents will independently navigate websites, make decisions, solve problems and adjust your travel itinerary on your behalf - just like a personal assistant, but fully automated. This isn't a distant dream; it's a reality we expect travellers to experience within the next decade. The travel industry is transforming and investors who act now will secure the biggest rewards. This breakthrough is being driven by breakthroughs in hardware and software. Advanced computing chips, which power AI training models, and sophisticated AI algorithms such as OpenAI's ChatGPT, Google's Gemini and Meta's LLaMA, are key enablers of this revolution. The most recent advancement occurred in January when OpenAI launched its next iteration of ChatGPT, Operator, an AI agent capable of independently navigating websites. Its applications extend far beyond travel, handling tasks like online shopping, filing expense reports and making restaurant reservations. By mimicking human interactions, Operator marks a major shift towards truly proactive, self-sufficient AI. These technological advancements have sparked a wave of investment and innovation across the travel industry, creating both exciting opportunities and new risks for investors. Established travel companies, agile startups and tech giants are all racing to build AI agents that could disrupt traditional travel search engines and capture significant market share. Tailored trips: Let your AI agent handle the detailsOne of the most powerful shifts brought by AI agents is personalisation. Instead of users manually searching for flights and accommodation, AI agents will predict your preferences, suggest destinations and secure bookings without requiring constant input. Imagine telling an AI agent you'd like to plan a European getaway in July. Instead of browsing for hours, your AI agent will instantly:

This reduces search time, eliminates decision fatigue and unlocks destinations travellers may never have considered. AI now smarter, cheaper, everywhereFor companies looking to capitalise on the AI agent opportunity, the first step is securing access to leading AI algorithms from OpenAI, Google and Meta. As the cost of computing continues to decline, access will become more affordable. A prime example of this shift is DeepSeek, a Chinese AI company that has demonstrated that building and training AI models can be cheaper and more efficient. This is a great outcome for AI infrastructure users such as established travel companies, allowing them to develop proprietary models while minimising their investment requirements. As AI tools become increasingly ubiquitous, the barriers to entry for companies looking to integrate AI will continue to shrink, enabling broader innovation. Data is the new travel currencyAs advanced AI infrastructure becomes widely accessible, the important question for investors is "Who will come out on top?" The power of AI lies in the underlying data. Companies with access to the richest datasets can generate superior customer insights and will dominate. For example, a company with a large user base and strong customer relationships understands a customer's travel preferences, spending habits, location history and real-time market trends, a valuable asset. For this reason, smaller competitors will likely suffer. Additionally, traditional players including shopfront travel agents, group tour companies and companies like TripAdvisor risk ceding share as AI agents eliminate the need for manual searches, directly connecting travellers with bookings and personalised recommendations. Existing giants like Booking Holdings, the parent company of Booking.com, have massive user bases and loyalty programs, giving them access to vast customer data. Booking Holdings is already incorporating insights into its early-stage AI agent to enhance the customer experience and streamline the travel booking process. In an AI-powered world, travellers are encouraged to go directly to the Booking platform, strengthening its control over the customer relationship. In this scenario, Booking's business quality and profitability are likely to strengthen, supported by a stronger market position and reduced reliance on expensive search-engine traffic. Hospitality experts the big winners in an AI-driven worldIn addition to AI infrastructure and customer data, deep expertise in travel and hospitality is essential for building effective AI agents. AI agents are here, and travel will never be the sameThe future of travel is being rewritten, with AI agents at the heart of this transformation. As the industry evolves, a fierce data race will unfold, with new sources being used to infer traveller preferences. Companies that can capture, refine and apply the richest travel insights will gain the upper hand. Tech giants are interesting in this context, as they already hold key insights into consumer behaviour: Google can scan your Gmail history for past travel bookings and requests, Apple has access to conversation data where you may be planning a trip with friends and family, and Meta, through Instagram, can analyse your travel-related posts and tagged destinations to predict future behaviours. While large tech companies may have information on the customer, they lack the operational knowledge, long-standing relationships and industry-specific insights that predicate success in the hospitality sector. Therefore, big tech's most viable monetisation path is through strategic partnerships with established travel players like Booking Holdings, Marriott and Hilton. For investors, this period of rapid change offers exciting opportunities and new risks to consider. Those investors who back the right companies will be at the forefront of the next evolution of travel, where seamless, hyper-personalised experiences redefine the industry. Market leaders will strengthen their dominance, while those slow to adapt risk being left behind in an AI-first world. The winners of this transformation will not just survive the disruption; they will shape the future of travel itself. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Core Infrastructure Fund, Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged) Important Information: Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

In this environment, the biggest winners will be companies that maintain direct relationships with accommodation owners, giving them greater control over service standards, property presentation and pricing. This close partnership is exemplified by franchised hotel chains like Hilton and Marriott, which work directly with their vast network of hotel owners. Hilton and Marriott don't just connect hotel owners with travellers; they are deeply integrated partners, offering decades of hospitality expertise that is incredibly difficult for tech giants to replicate. They provide hands-on support for hotel operations, labour management and supply procurement, even guiding owners through the hotel development process. To secure this valuable expertise, hotel owners sign long-term contracts - often up to 20 years - with these franchised giants, ensuring they maintain a vast network of properties for travellers to choose from in this era of technological change.

In this environment, the biggest winners will be companies that maintain direct relationships with accommodation owners, giving them greater control over service standards, property presentation and pricing. This close partnership is exemplified by franchised hotel chains like Hilton and Marriott, which work directly with their vast network of hotel owners. Hilton and Marriott don't just connect hotel owners with travellers; they are deeply integrated partners, offering decades of hospitality expertise that is incredibly difficult for tech giants to replicate. They provide hands-on support for hotel operations, labour management and supply procurement, even guiding owners through the hotel development process. To secure this valuable expertise, hotel owners sign long-term contracts - often up to 20 years - with these franchised giants, ensuring they maintain a vast network of properties for travellers to choose from in this era of technological change.

12 May 2025 - Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

[Current Manager Report if available]

12 May 2025 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

12 May 2025 - The Resurgence of Nuclear Energy

|

News & Views: The Resurgence of Nuclear Energy 4D Infrastructure May 2025 Nuclear energy is undergoing a renaissance. While it has long been associated with images of devastation and disaster, it is now increasingly recognised as a crucial part of the global energy transition, offering a reliable solution to rising energy demand and decarbonisation efforts. In this edition of News & Views we examine the decline of nuclear energy, the catalysts behind its resurgence and how the 4D investment strategy captures exposure to this evolving theme. Why did nuclear decline?1. Public fearAt its peak in the late 1990s to early 2000s, nuclear energy accounted for nearly 17% of global electricity generation, compared to around 9% today. Incidents like Three Mile Island in the US in 1979 and Chernobyl in 1986 increased public anxiety around nuclear energy. While both these incidents resulted in greatly increased safety regulations and oversight, the stigma remained. The 2011 Fukushima disaster in Japan reignited safety concerns, resulting in several countries scaling back or halting their nuclear programs. The US for example increased regulatory scrutiny while Germany decided to exit nuclear power altogether. 2. High costs and complex constructionHigher safety standards and regulatory obligations have made nuclear projects increasingly expensive. The need for more advanced safety systems, robust containment structures and ongoing design and regulatory changes have all increased the cost to build, operate and maintain nuclear power plants. Project management complexities have also been detrimental. With less nuclear plants being built, the industry experienced a loss of skilled labour and expertise in nuclear construction. This, coupled with the incredible complexity yet lack of standardisation in plant build, has also led to increased inefficiencies and costs. As a result, many of the more recent nuclear power plant projects have seen significant delays and cost overruns. Examples include:

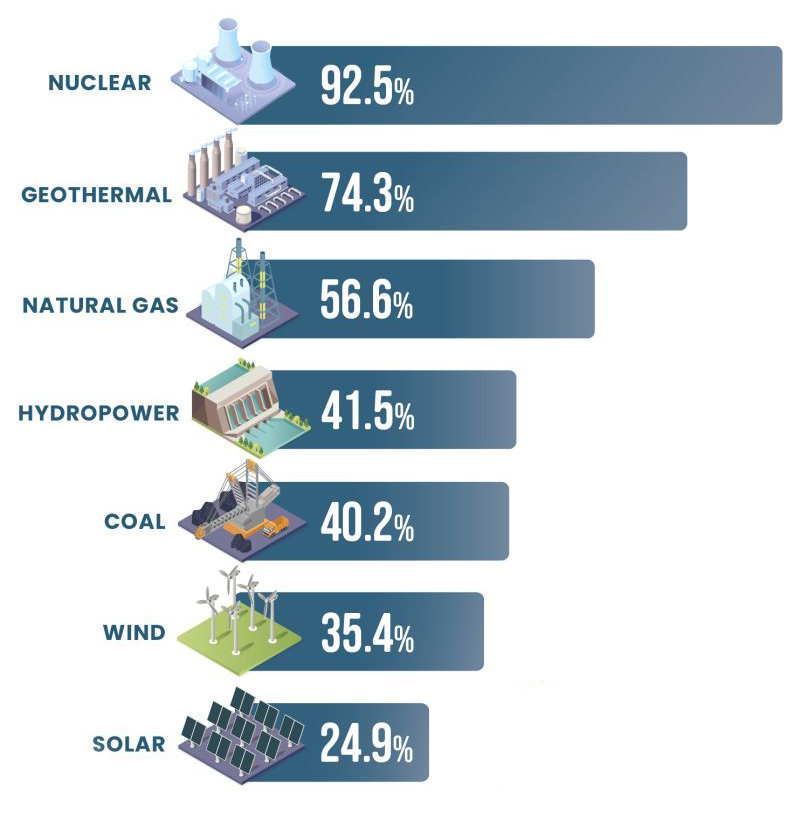

What's driving nuclear's revival?1. Reliable, carbon-free baseload powerNuclear energy offers continuous, emissions-free power -- a valuable complement to intermittent renewables like wind and solar. While wind and solar energy are expanding, they remain intermittent, generating electricity only when the wind blows or the sun shines. Managing this intermittency requires energy storage to store excess energy during high-output periods and release it during high-demand or low-generation periods. Even though storage technology and deployment has grown rapidly, costs remain too high to implement at scale. At the same time supply pressures are increasing as coal and gas-fired power plants being phased out or growing more slowly. This is why nuclear energy stands out as the only large-scale baseload power source that can reliably bridge the supply gap, combat climate change and avoid the intermittency challenges of other renewables. Capacity Factors across various energy sources

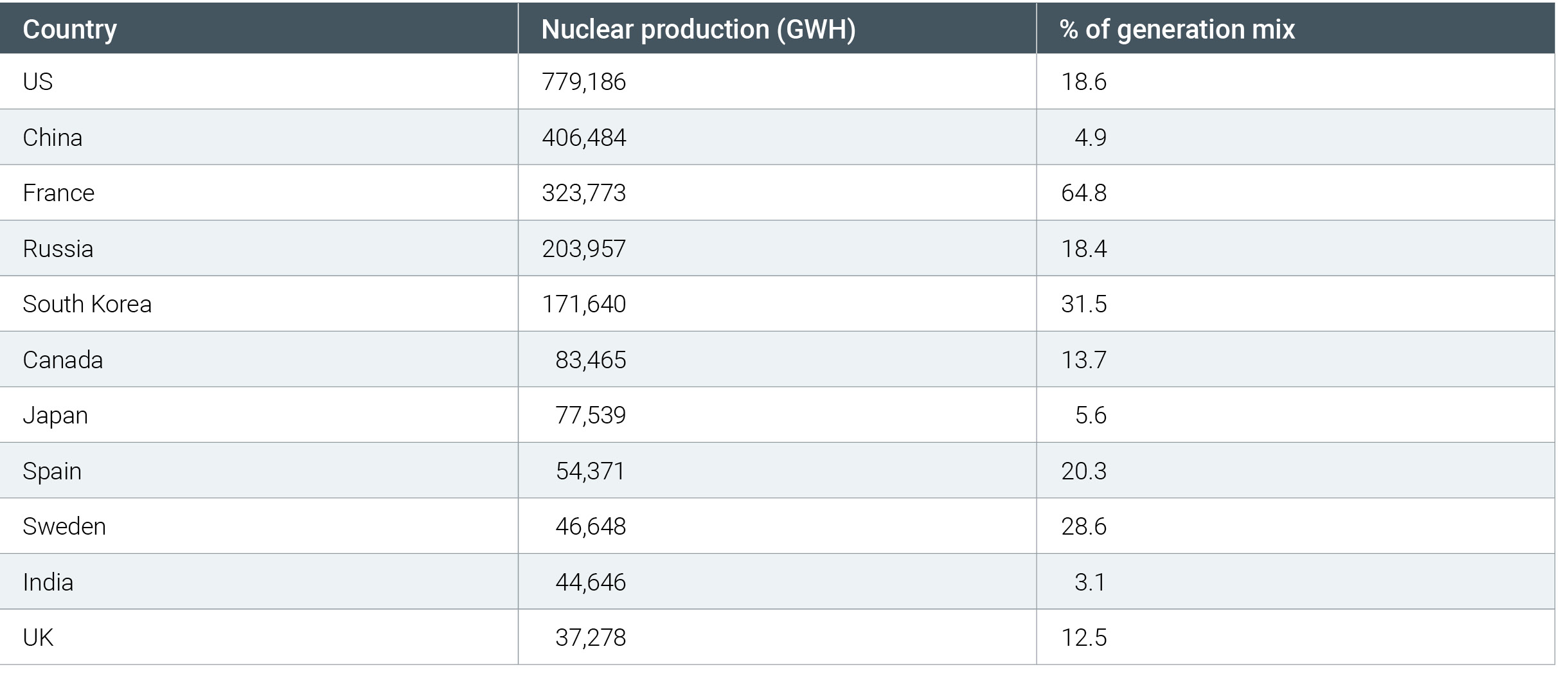

It is important to note that even with safety and cost concerns, nuclear continues to be a pivotal component of the electricity generation mix for many countries. For example, in France, where nuclear accounts for approximately 65% of the generation mix, power prices have remained relatively low compared to other European countries. The relatively low cost of nuclear power generation has also contributed to France becoming one of the world's largest net exporters of energy, bringing in €5bn in revenues in 2024.1 Recognising the value of nuclear power assets, France plans to replace its aging nuclear fleet with six new reactors by 2050, with an option for an additional eight. Nuclear Production 2023 and Proportion of Generation Mix

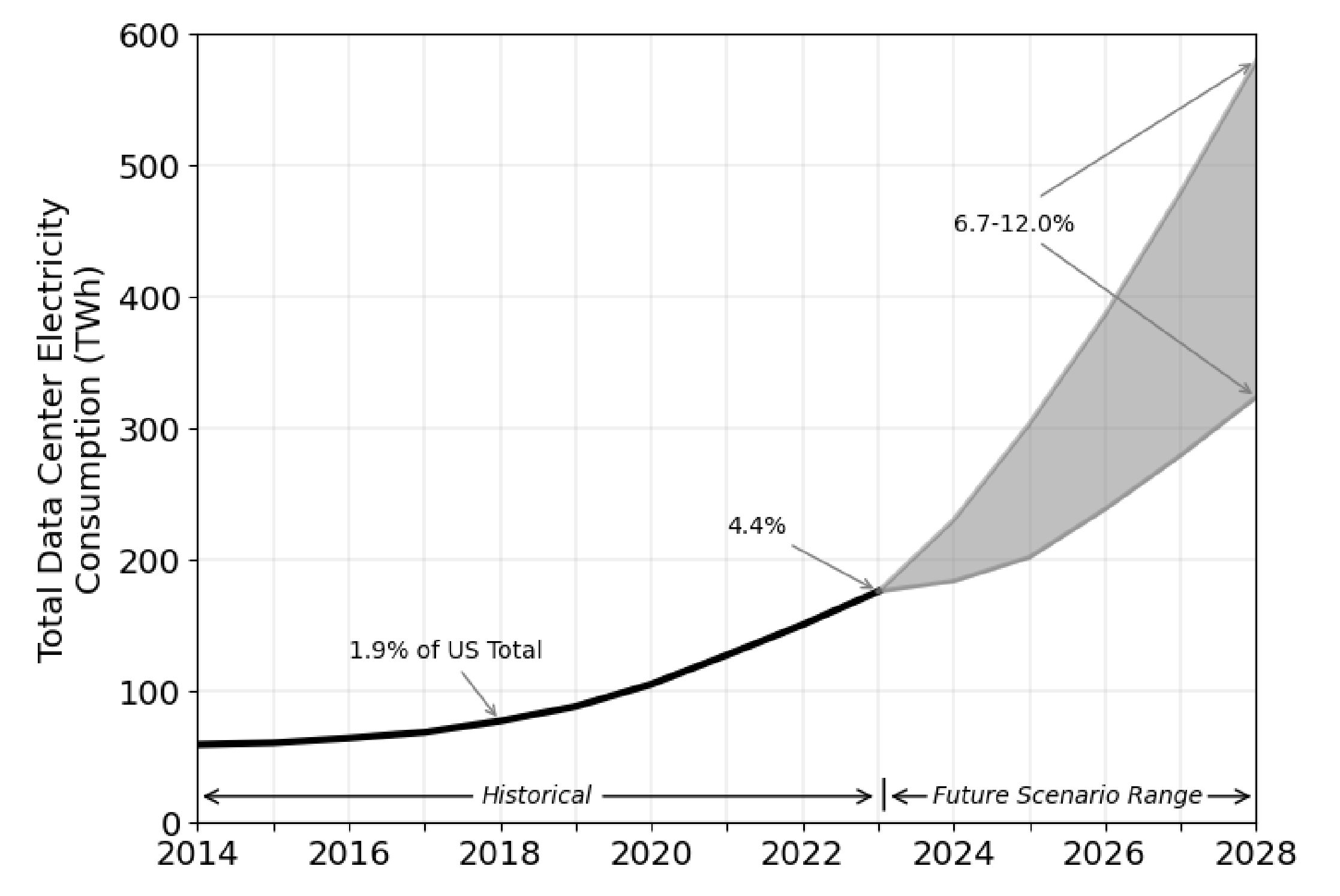

2. Rising demand from electrification and AIElectricity demand, previously growing modestly (~1% per year in the US), is now accelerating due to manufacturing onshoring, electrification and surging AI data centre usage. While estimates of demand growth are difficult to quantify, it is estimated that over the next five years the US will see load growth of at least 3%3, with further upside potential as data centre demand increases alongside demand for AI computing. Government reports project US data centre demand leaping from 176TwH in 2023 to 325-580TwH in 2028.4 This equates to between 6.7% and 12% of total US electricity consumption - up from 4% currently.5 Estimated data centre consumption growth

3. Hyperscaler investment'Hyperscalers' (large technology companies using data centres for cloud computing and data management services) are turning to nuclear energy due to its ability to provide 24/7 secure base load power for data centres while also aligning with their significant carbon reduction goals. The main drawback of nuclear power for hyperscalers is build time: with planning and construction times of over 10 years along (notwithstanding time and cost blowouts (as set out above). These long lead times conflict with hyperscalers' ambitions to deliver nascent high-profile AI technologies as soon as possible. As an alternative, hyperscalers have focused on leveraging existing nuclear capacity and exploring innovative reactor designs to mitigate cost and construction times. This is demonstrated through examples from key hyperscalers including:

4. Policy supportGovernment policy is increasingly supportive. The US Inflation Reduction Act (IRA) is the most prominent example, with the Act containing several tax credit provisions that serve to boost nuclear's financial viability. Examples include:

Nuclear's investment caseWe anticipate continued growth in nuclear demand, driven by AI-related consumption, supportive policies and decarbonisation mandates. Given the long lead times and high costs of new build, leveraging existing capacity remains the focus. Translating this to investment decisions4D supports the nuclear theme as part of the Energy Transition. However, for us to take exposure the underlying assets must meet our infrastructure definition by either being 'regulated' or 'contracted'. One or both of these arrangements serves to secure the investment and operating costs of the plant as well as the return to the shareholder. At 4D we have nuclear power generating exposures across multiple US utility investments, but most prominently through our investment in Dominion Energy (D). Dominion owns regulated nuclear facilities in Virginia and South Carolina, as well as the Millstone Nuclear Power Station in Connecticut, which the company is exploring contracting opportunities for. We also have exposure through European utilities including Iberdrola [IBE] who have some legacy nuclear exposure in Spain. We are also closely monitoring nuclear-exposed Independent Power Producers (IPPs) like Constellation Energy, Talen and Vistra. While these stocks appeal in different ways, they currently either lack the cash flow visibility we require in our investments or lack a compelling enough risk-reward proposition amid stretched valuations. Case Study: Millstone nuclear power plantOwned by Dominion Energy, the Millstone Nuclear Power Plant (Millstone) is based in Connecticut, US, and has an operating capacity of 2GW across units 2 and 3. The power station began operating in 1975 and has an operating license from the US Nuclear Regulatory Commission (NRC) until July 2037 and November 2045 for Units 2 and 3 respectively. The power station provides around 47% of Connecticut's power needs, more than 90% of the state's carbon-free power and employs around 4,000 people. Until March 2019, Millstone sold 100% of its capacity into the ISO New England merchant energy market in the northeast of the US. Prior to the Covid-19 recovery, benign growth in power demand from customers (around 1% annual demand growth for the previous decade), combined with cheaper forms of alternative energy generation (such as renewables and natural gas), meant the merchant price of power earned by Millstone was uneconomic compared to the running costs of the facility. The load-weighted average prices achieved in 2016, 2017 and 2018 were $34.62/MWh, $37.45/MWh and $52.27/MWh respectively. Dominion management lobbied Connecticut legislators and regulators, stressing they would have to decommission Millstone if the state didn't provide some form of financial support as low and volatile market prices meant the facility was loss making. In response, the Connecticut regulator, PURA, signed a fixed price agreement with Dominion for approximately half of Millstone's capacity, for a maturity of 11 years (to 2029). The price within the contract was $49.99/MWh, well above the prevailing market price achieved for the facility. This contract supported the financial viability of Millstone and incentivised Dominion to continue operating the facility. Fast forwarding to the current environment, the northeast US power market is now in short supply, driven by the aforementioned strong demand growth from data centres, onshoring of manufacturing and wider electrification efforts. This has resulted in much higher market prices with capacity contracts agreed with data centre companies at prices rumoured in excess of $100/MWh. The carbon-free, firm power capacity provided by nuclear facilities like Millstone are particularly sought after by tech companies. Dominion management are now considering options of what to do with the uncontracted capacity of the facility, and potential utilisation of capacity post expiry of the agreement with PURA in 2029. 1 https://energynews.pro/en/france-reaches-a-record-e5-billion-in-electricity-exports-in-2024/ The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. Funds operated by this manager: 4D Global Infrastructure Fund (Unhedged), 4D Global Infrastructure Fund (AUD Hedged) |

Source: US Energy Information Administration

Source: US Energy Information Administration Source: NEI, IAEA-PRIS 2

Source: NEI, IAEA-PRIS 2 Source: Berkeley Lab - 2024 United States Data Center - Energy Usage Report

Source: Berkeley Lab - 2024 United States Data Center - Energy Usage Report Source: U.S. Department of Energy

Source: U.S. Department of Energy

9 May 2025 - Hedge Clippings | 09 May 2025

|

|

|

|

Hedge Clippings | 09 May 2025 Although last week's Hedge Clippings described the election campaign as boring, disappointing and uninspiring, the outcomes and after-effects have been anything but. Anthony Albanese's victory was decisive and well deserved, even if he was ably assisted by Peter Dutton and Adam Bandt, who each contributed to Albo's success, and their own eventual demise. To what extent Dutton was supported (probably the wrong term) by the Liberal party hierarchy, or the executive and his inner circle, we'll no doubt have to wait to find out when the inevitable post-mortem is held or books are written. Treasurer Jim Chalmers summed it up on election night when he said he "couldn't believe his luck" when his opposite number announced they would vote against his across-the-board tax cuts, even though in actual dollar terms it amounts to $268 in 2026-27, and $536 in 2027-28. That's enough for one cup of coffee a week next year, and two cups the year after. We can't wait! Where the Libs go from here is anyone's guess, but if they continue to listen to the right wing of the party (or Gina Rinehart, who'd like them to be more like Trump), they're going to remain where they are, or worse, for the foreseeable future. Which, sadly, is not good for democracy. As it is, we have to hope that success will not go to Albo's and the loony left's head, and that ideas such as taxing unrealised capital gains won't spread beyond super balances above $3 million. Our guess, however, is that they will. Bottom line, congratulations to Albanese. He's only 62, so short of another Hawke/Keating type deal, Jim Chalmers will have to wait at least three years, and possibly six. So back to the real world, where they probably couldn't give a fig to Australian's antics of the past few weeks. As pointed out by PinPoint Economics' latest report (and chart pack), tariffs and trade wars are the focus of economic and political debate at present. To quote PinPoint's Executive Summary, the parameters shift on an almost daily basis, such that there's a need to cut through to the underlying fundamentals and work out what to watch.

However, the most pertinent aspect is PinPoint's view that the parameters shift on an almost daily basis. Trump's style is to come out all guns blazing in an attempt to get the upper hand - or to achieve maximum exposure, or both. What the final outcome will be once he's chopped and changed his terms on a country-by-country basis remains to be seen. First cab off the rank is the UK - (The Donald's obviously keen to make sure his invitation to Buckingham Palace is still secure), where he's kept a 10% tariff in place in spite of the US enjoying a trade surplus (like Australia) with the UK. He's also hinted that the 145% tariffs on China will be watered down, and that the White House is in talks with dozens of other countries. Trump has been less successful buying Canada and Greenland (so far), nor has he stopped the war in Ukraine or Palestine. Everything remains uncertain, making Australia a relative oasis of calm! News & Insights 10k Words | Equitable Investors Market Commentary | Glenmore Asset Management April 2025 Performance News Seed Funds Management Hybrid Income Fund Bennelong Australian Equities Fund Bennelong Long Short Equity Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

9 May 2025 - Performance Report: Quay Global Real Estate Fund (Unhedged)

[Current Manager Report if available]

9 May 2025 - Performance Report: Bennelong Long Short Equity Fund

[Current Manager Report if available]

9 May 2025 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

9 May 2025 - Are You In The Matrix?

|

Are You In The Matrix? Marcus Today April 2025 |

|

Have you been told to "buy and hold"? "It'll be fine in the long run"? "You can't time the market"? You might be in the matrix. In this video, Marcus breaks down the truth behind the mantras the finance industry repeats - not to help you, but to keep you quiet. If you've ever felt like the advice doesn't quite match reality... you're not alone. DISCLAIMER: This content is for general information purposes only and does not constitute personal financial advice. Please consider your own circumstances or seek professional advice before making investment decisions. |

|

Funds operated by this manager: |