News

16 May 2025 - Performance Report: Glenmore Australian Equities Fund

[Current Manager Report if available]

16 May 2025 - Performance Report: Argonaut Global Gold Fund

[Current Manager Report if available]

16 May 2025 - Tariffs, Tension and Tech: How Trump's Second Term is Reshaping Markets

|

Tariffs, Tension and Tech: How Trump's Second Term is Reshaping Markets Sage Capital April 2025 |

|

It would be an understatement to say that the world has become a more volatile and uncertain place since Donald Trump moved back into the Oval Office in January. Given that markets don't like uncertainty, it's no surprise that both US and Australian shares have tumbled from their post-inauguration highs. The celebratory mood of the market - driven by the prospect of tax cuts, deregulation and boom times ahead - has been replaced with fear and uncertainty. Escalating geopolitical tensions, trade wars, and the moving feast that is US tariff policies have cast a shadow over the outlook, raising concerns about a recession. Among this uncertainty, one thing is becoming very clear - Trump 2.0 will be very different from Trump 1.0. As the US continues to roll out new tariff and economic policies, there is likely to be elevated volatility in the sharemarket, at least in the near term. Given the cadence of announcements from the Trump administration and their potential short-term negative impact on the US and global economy, it's fair to assume the market will remain in a state of flux for a while longer. The lengths to which Trump will go to achieve his goal of becoming a legacy president are beyond the scope of this article. Opinions vary widely. Some believe there is a method in his madness that may lead to short-term pain but long-term gain, while others view his actions as erratic and misguided. Regardless of perspective, increased market volatility should present potential attractive buying opportunities for stocks in Australia. The market had been looking very expensive, particularly in sectors such as technology. The sell-off has taken some of the froth out of the market. Buying opportunitiesWe believe there may be more downside to come in the short term as markets adjust to the new order, but we are actively watching for buying opportunities. Our focus remains on companies with a clear growth trajectory, strong control over their own destiny, and not overly exposed to tariffs or shifts in consumer sentiment. One stock we think fits this description is Life360, the family location sharing app. The Life360 app is the most-used social networking app daily in the US after Facebook and WhatsApp, with a rapidly growing user base of 80 million worldwide. Its key competitive advantage lies in its leading location tracking technology, which is well ahead of its competitors, including Apple's Find My Friends. Life360 has grown revenue by 35 per cent per annum over the past five years as more and more users see value in the increasing functionality of the app and switch from the free version to a paid subscription, or move to higher tier plans. The company is expected to continue growing at 20 per cent or more for the foreseeable future as it continues to penetrate the US, its biggest market, as well as rolling out globally and introducing new products that can monitor the safety of pets and elderly relatives. Its scalable technology allows the company to grow revenue at minimal extra cost, positioning it well for continued success. It is also harnessing artificial intelligence, not only for innovating the core app but also to enable targeted advertising that provides an additional revenue stream. With a quality management team including an enthusiastic founder, we believe Life360 can continue to deliver strong earnings growth for many years to come. Another topic on our minds that is gaining momentum in company discussions - and faster than the word "tariff" - is agentic AI. This is the next step on from generative AI and a concept we see garnering more and more attention this year. An AI "agent" is more sophisticated than being just a generator of content or a basic chatbot - it can proactively make decisions and execute actions based on real-time data. Autonomous vehicles such as Waymo are powered by agentic AI. Harnessing it in business processes could produce huge cost savings and productivity gains across a broad range of industries, particularly for those that utilise processes that require multiple repetitive steps and complex decision-making across numerous data sources. While it is early days, we are monitoring its evolution and impact closely. There's no doubt that the changes in US policies and the rapid evolution of AI are driving elevated uncertainty and volatility. The glass-half-full view is that this will result in some short-term pain for economies and sharemarkets but longer-term gains. Only time will tell. |

|

Funds operated by this manager: CC Sage Capital Equity Plus Fund, CC Sage Capital Absolute Return Fund This information is for professional and wholesale investors only and has been prepared by Sage Capital Pty Ltd ACN 632 839 877 AR No. 001276472 ('Sage Capital'). Channel Investment Management Limited ACN 163 234 240 AFSL 439007 ('CIML') is the responsible entity and issuer of units in the CC Sage Capital Equity Plus Fund ARSN 634 148 913 and the CC Sage Capital Absolute Return Fund ARSN 634 149 287 (collectively 'the Funds'). Channel Capital Pty Ltd ACN 162 591 568 AR No. 001274413 ('Channel') provides investment infrastructure services for Sage Capital and is the holding company of CIML. This information is supplied on the following conditions which are expressly accepted and agreed to by each interested party ('Recipient'). |

15 May 2025 - Performance Report: Altor AltFi Income Fund

[Current Manager Report if available]

15 May 2025 - Is this now an opportunity for china exposed stocks?

|

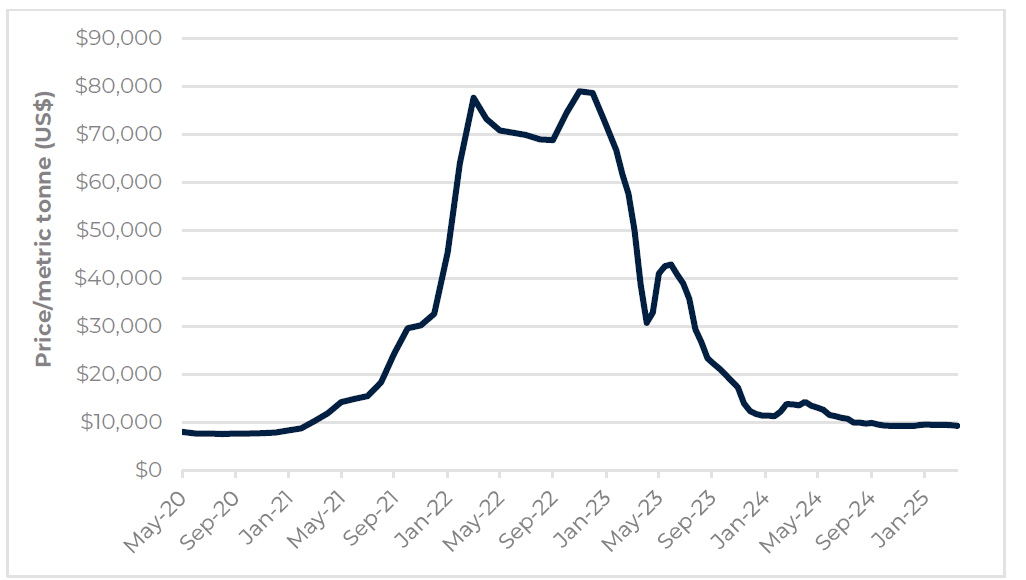

Is this now an opportunity for china exposed stocks? Tyndall Asset Management May 2025 After a significant price correction in China exposed stocks over the last year, Tyndall's Jason Kim recently went to China and met with various companies and industry experts to help determine whether some of these stocks now represent a real opportunity for investors. During the course of 2024, Australia's largest trading partner, China, went through a significant economic downturn on the back of a residential property downturn after a weak COVID bounce when China came out of lockdown in late 2022. This resulted in poor consumer sentiment, which then spiraled into a negative feedback loop with business confidence which became more pronounced during 2024. This not only impacted the broader share market, but more specifically, it directly impacted resource stocks and those companies with significant exposure to Chinese consumers. Key takeawaysAfter facing soft demand, and deflation in China during 2024, the general view for the Chinese economy was that 2024 saw the low point for the economy, and that 2025 is likely to see some improvement. Overall demand growth is at least going to improve to be marginally negative to flat, and it is possible that we see a very modest recovery. Residential property prices in tier 1 and 2 cities are now starting to show some signs of stabilisation, post-September policy support, and arguably there may now be some green shoots. However, property prices in the lower tier cities are still weak, resulting in consumer sentiment still remaining fragile. Given the focus on improving consumer sentiment, it appears most likely that any Chinese government stimulus will be targeted more at the consumer rather than in construction/fixed asset investment, and that measures will be taken to help stabilise - rather than stimulate - residential property prices. This clearly has negative implications for steel and iron ore. The key risks are US tariffs and geopolitical tensions which remain a significant wildcard impacting exports and overall sentiment. However, many experts noted that the Chinese government may have been holding back some stimulus to leave enough fire power to properly address the negative implications from the US tariffs. Key Investment OutlookIron Ore China produces approximately 1 billion tonnes of steel per annum. Due to a weak Chinese economy last year, we saw softer demand for steel domestically and an increase in steel exports to c100kt pa to shift excess production. This has seen steel profit margins decline. After meeting many steel mills, iron ore traders, and steel traders, the consensus view is that domestic steel demand still remains soft, with property and infrastructure seeing a modest contraction in demand. The key bright spots for demand are in the consumer related sectors - namely auto and appliances - after some recent consumer stimulus sought to increase demand in those industries. This view is in-line with what was discussed previously. China has increasingly imposed stricter and more frequent air pollution controls, requiring the steel mills to reduce production to reduce emissions, and this may be the mechanism that the authorities will use to help reduce oversupply. There is speculation that a government mandated production cut of 50 million tonnes per annum is imminent. Lithium An incredible surge in lithium prices in 2021 and 2022 - peaking at around $US80,000 in Dec 2022 - saw a swathe of new lithium supply come to market, which perhaps unsurprisingly was followed by a spectacular decline in prices (refer Figure 1). Figure 1: The Lithium Rollercoaster

Source: Bloomberg, April 2025. After having met many Chinese lithium miners and lithium battery makers, it appears that even after this significant price correction the outlook for lithium prices still remains challenged. Despite growing demand for lithium as we transition to renewables and EVs globally, the expected growth in supply flagged by the lithium miners we met would suggest that any demand growth will at least be met by supply growth into the medium term. Portfolio ImplicationsGiven the near-term challenges for iron ore, we have moderated our overweight position in the iron ore miners to be marginally overweight. This acknowledges that any stimulus from China, while likely to be more targeted at the consumer, could still be incrementally positive for mining stocks. Our key overweight in this sector is Rio Tinto due to its strong forecast free cash flows, and participation in the Simandou project which will be a source of meaningful growth in iron-ore supply in the near future. While lithium miners may appear attractive at current share prices, our trip suggests it is likely too early to enter this space given the challenging oversupply outlook. We continue to monitor this sector closely for any potential opportunities. Author: Jason Kim, Portfolio Manager Funds operated by this manager: Tyndall Australian Share Concentrated Fund, Tyndall Australian Share Income Fund, Tyndall Australian Share Wholesale Fund |

14 May 2025 - Performance Report: Bennelong Twenty20 Australian Equities Fund

[Current Manager Report if available]

14 May 2025 - Performance Report: Argonaut Natural Resources Fund

[Current Manager Report if available]

14 May 2025 - Tarrifs & trade wars

14 May 2025 - Isolation day: the geopolitical impact of Trump's tariffs on the world

|

Isolation day: the geopolitical impact of Trump's tariffs on the world Nikko Asset Management April 2025 "Shock and awe" intendedWhen news broke of Donald Trump's resounding victory at the November 2024 US presidential elections, many countries and businesses girded themselves for another round of trade wars. But this time, the 47th US president upped the ante from his previous term by imposing across-the-board tariffs on friends and foes alike. The Republican party's majority in both the US House of Representatives and Senate helped to ensure that Trump would have near-unchecked power, leading to such policy extremes. In light of these developments, we see markets as the remaining check and balance to hold the current administration's actions to account in the immediate term. As would be expected, Trump's tariffs roiled global stock markets. We therefore expect risk premiums for US assets to remain elevated for some time. Prior to the outcome of the US elections, we had explored the likely implications of a second Trump presidency and potential implications for portfolio companies in "If Trump wins: uncertainties and opportunities from an Asian equity perspective". Similarly, from a global perspective, the pronounced market volatility suggests that it will be hazardous to sell following large declines and to buy after major upturns unless we have greater conviction that concrete steps are being taken towards de-escalation. Energy and commodities also took a hit as the ongoing trade disputes raised doubts over future demand. We expect crude oil prices to remain lower for longer though other commodities may be more economically sensitive and thus, volatile. In our view, Trump's re-escalation of the tariff wars will only exacerbate the slowdown in global growth and may potentially plunge the US into recession unless his administration significantly reverses course with key trading partners including China, the European Union (EU), Canada and Mexico. Another factor which could prevent an impending US downturn is intervention by the Federal Reserve (Fed). However, the Fed faces a very tough task, as rising inflation poses a risk that could make it challenging for it to further reduce interest rates. China in the crosshairsAlthough seemingly indiscriminate, the so-called "Liberation Day" tariffs primarily targeted China. We believe that Washington will maintain this approach even if it rolls back punitive measures, such as with the surprise 90-day reciprocal tariff reprieve announced by the White House, for all countries apart from China. The chaos caused by Trump's unpredictable actions may seem surreal, almost like events from a reality TV show. Nonetheless, we believe he is still a businessman at heart with deal-making as his main objective. The ability of all countries to weather the US tariffs hinges on sound policy decisions, supportive domestic demand, capacity to stimulate the economy via monetary and fiscal means and the ability to negotiate concessions with the Trump administration by increasing purchases of US goods or investment. We think this last point may help countries to secure a bigger share of the export manufacturing market to the US over time if balanced correctly. The country with the most potential in this regard is India, which also stands to benefit from a sustained drop in energy prices. Most countries in Asia will likely try and hold discussions with the Trump administration. To date, over 75 countries have sought to strike a deal with the White House. Given Trump's preference to conduct one-on-one talks, we feel it would be prudent for the Association of Southeast Asian Nations (ASEAN) to negotiate as a bloc for more favourable terms as opposed to a country-by-country basis. For potential guidance ASEAN can look at the EU, which has banded together even more closely amid current developments. In the context of Asia excluding Japan, although countries that are part of the "China plus one" risk diversification strategy were also hit with tariffs to varying degrees, most of them are in the process of negotiating trade agreements with the White House. We believe that they could potentially be well-positioned to benefit from subsequent lowered duties as well as the accelerating trend of diversifying supply chains away from China. Meanwhile, the Philippines' services and agriculture-focused economy means that the reciprocal tariffs, which mainly penalise manufacturing hubs in Trump's quest to bring such jobs back to the US, will have less of a negative impact on the Philippines. And finally, while India is yet to officially respond to the sweeping US tariffs, we believe that its economy, driven more domestic consumption, puts it in a stronger position to negotiate a more favourable trade agreement with Trump compared to countries more heavily reliant on exports. Sino resolutionChina, however, is not having any of it. Compared to Trump's first term in office, Beijing is hitting back more forcefully with tit-for-tat tariffs having learned the hard way that any signs of weakness will certainly be exploited. With neither Trump nor Chinese President Xi Jinping likely to back down, we believe China's actions must be accompanied by corresponding domestic support packages to prevent Chinese assets from suffering collateral damage. Further restrictions on investments in China or the US could be on the cards should tensions escalate. US Treasury Secretary Scott Bessent raised the possibility of delisting Chinese companies from local stock exchanges following the tariffs announcements. Beijing had also earlier ordered the National Development and Reform Commission to halt approvals for Chinese firms aiming to invest in the US. Government officials have said China is ready to lower interest rates and relax the reserve requirement ratio to stimulate the economy in the face of rising trade tensions with the US. In a planned emergency meeting of high-level economic officials, we expect the authorities to redouble efforts to bolster consumption, artificial intelligence (AI) and energy infrastructure and focus on localising industries such as medical devices. Initial measures to boost domestic consumption are expected to include the streamlining of duty-free purchases by inbound tourists, which could benefit duty free names. The measures could also include a plan to ramp up health-related consumption though fitness and sports initiatives and the promotion of high-quality agricultural products. These are likely to be just the beginning of a series of policies aimed at supporting domestic demand. Manufacturing mayhemAt a sectoral level, pharmaceutical and semiconductor imports are currently not subject to US reciprocal tariffs. However, Trump is threatening to revoke these exemptions as part of a wider national security agenda. Chinese companies in these industries are the likely targets of future measures. In the broader manufacturing space, we view flexibility in production as necessary for supply chain resilience as per Apple's decision to produce more iPhones in India in a shift away from China. Nevertheless, committing to longer-term manufacturing capital expenditure decisions poses significant challenges under current conditions. A new world order born of fundamental changeTrump's unprecedented actions have torn down the established global trade order as the US seeks to structurally cut its deficit and bring back manufacturing jobs, while China has been making attempts to shift away from an export-led economy towards consumption-driven growth. The 90-day tariff moratorium may provide nations some time to assess the optimal route to navigate these US tariffs. However, the risk of further escalation is very real, given that the world's two largest economies are adamant about not appearing weak in the eyes of the other. Regardless of who gains the upper hand in the end, all countries will need to chart a new course into the proverbial unknown. Volatility typically brings both risk and opportunities. Significant fundamental changes have been set in motion and will lead to long-term, sustainable investment opportunities in the days and months ahead. Cutting through the noise and bluster to identify longer term investment opportunities is what excites us. Over the last 15 years, US equities and assets have been the biggest beneficiary of global portfolio flows. However, if US risk premiums are expected to remain elevated for an extended period, investors are likely to ask, "Where else should I reallocate my capital to"? We would not rule out large parts of Asia. Funds operated by this manager: Nikko AM ARK Global Disruptive Innovation Fund, Nikko AM Global Share Fund Important disclaimer information Please note that much of the content which appears on this page is intended for the use of professional investors only. |

13 May 2025 - Performance Report: Bennelong Concentrated Australian Equities Fund

[Current Manager Report if available]