News

12 Jun 2025 - Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

[Current Manager Report if available]

12 Jun 2025 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

12 Jun 2025 - One Year On: Responsible AI engagement examples and reflections

|

One Year On: Responsible AI engagement examples and reflections Alphinity Investment Management May 2025 |

|

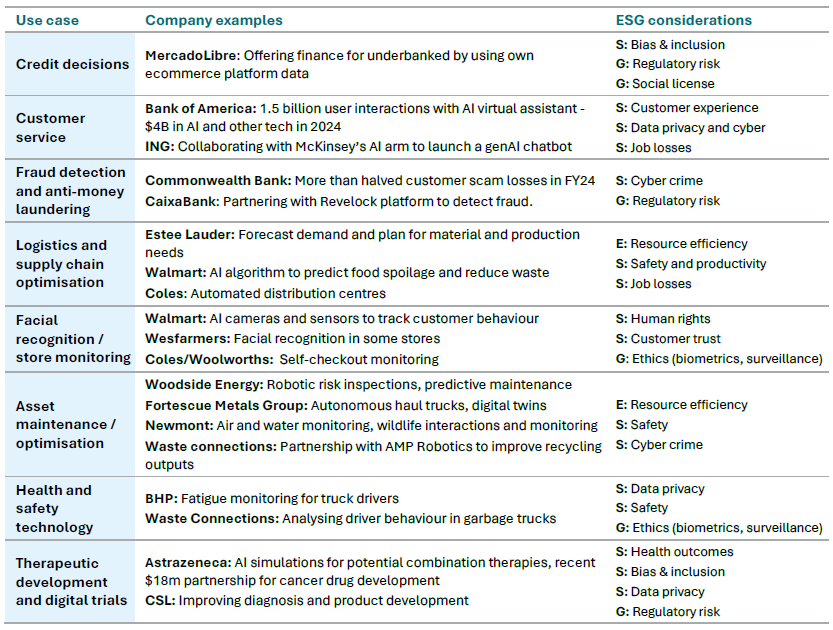

Artificial Intelligence (AI) is fast becoming a powerhouse for individuals and businesses, offering automation, data-led insights and boosted efficiency. With this huge opportunity, however, comes challenges and risks that need to be carefully considered. With AI uptake moving quicker than many expected, Responsible AI needs to match the pace. Alphinity has been digging into the ethics of AI technologies for quite some time, considering the potential risks to companies, society and the environment. This curiosity led to an exciting collaboration with Australia's premier national science research agency, Commonwealth Scientific and Industrial Research Organisation (CSIRO), in 2023. We co-developed a landmark Responsible AI Framework which was released in 2024. Now, after a year of use, we have some reflections to share. This article highlights AI use cases that we see companies adopting, some of the related ESG risks, and notable company engagements that were driven by applying the framework to our investments. Spotlight: Responsible AI FrameworkIn May 2024, Alphinity and CSIRO released a Responsible AI Framework (RAI Framework) to assist both investors and companies navigate the flourishing AI opportunity. The framework is a practical, three-part toolkit that bridges the gap between emerging responsible AI considerations and existing ESG principles such as workforce, customer, data privacy and social license. The framework is designed to set a standard in responsible AI and can be used flexibly depending on the investor's scope and needs. It is also intended to help companies understand investor expectations around responsible AI implementation and disclosure. The report and toolkit can be explored here: A Responsible AI Framework for Investors - Alphinity Why should investors care about responsible AI today?AI holds significant potential but also presents various environmental and social risks. For instance, the reliance on data centres leads to increased greenhouse gas emissions, which may result in climate change-related risks, including carbon pricing. Additionally, their high water usage could need to be restricted during droughts, or be subject to future regulations as recently proposed in Europe. The business stability of entities within the AI value chain could be adversely affected if these issues are not promptly identified and managed. These risks are prevalent throughout the AI value chain, from semiconductor producers to software providers, but are particularly significant in the short-term for hyperscalers such as Microsoft, Alphabet, and Amazon. AI can help drive automation, supercharge productivity and assist with the performance of repetitive tasks. But what happens when workers are displaced, or when the AI tool hallucinates or malfunctions? Employees and unions could react, creating social tension and affecting customer service. Wider operational disruptions and/or cybersecurity issues are also possibilities. A consideration in the healthcare industry is to balance the cost and timing benefits around clinical trials and product development, with the potential risks to data quality, bias and real-world validation of AI-lead drug discovery. We believe that in order for AI opportunities to be realised, the governance, design, and application of the AI needs to be undertaken in a responsible way, considering any environmental, social, and evolving regulatory considerations of AI and mitigating these impacts wherever possible. To help us think through these implications, we take a use case first approach. That is, we identify the relevant use cases by sector or company, then assess the relevant ESG considerations including the company specific mitigation efforts. This has supported more proactive and targeted research and engagement with companies and has enabled us to better identify and integrate the various risks and considerations into our ESG assessments. This approach has been illustrated in the table below. It presents some of the more common use cases, some company examples and the relevant ESG threats and/or opportunities.

40+ company meetings: Continued engagement on responsible AISince publishing the framework, our focus has been on assessing responsible AI risks and opportunities within our investments. Building on the 28 company interviews conducted in 2023 for the research project, our engagement with portfolio companies and prospects has continued. These discussions not only shed light on how AI use cases are evolving, they also help us to assess how responsible AI practices are progressing. Since publishing the report in May last year, we've undertaken a further 15 engagements where insights from our RAI Framework guided the discussions. We shared our framework with organisations such as Wesfarmers, Medibank, AGL, Origin, Aristocrat Leisure, Netflix, Intuitive Surgical, Novonesis, Mercadolibre, Thermo Fisher, CaixaBank and Schneider Electric. The RAI framework has been a practical way to communicate the types of information investors seek to evaluate AI-related risks. Pleasingly, companies like Medibank and MercadoLibre have said that the resource has been helpful to guide internal responsible AI practices. Insights and examples from these engagements are categorised into: Financial services, Healthcare, Technology products and platforms, and Industrials and energy services. Financial servicesCaixaBank: AI Investment Guided by Governance Framework CaixaBank, a prominent Spanish bank, is investing €5 billion in AI to benefit millions of customers. The bank has seen early success with AI in customer service claims, call centre operation, and code generation. There are regulations in the European AI Act that require additional controls and governance mechanisms to ensure the quality of AI outputs in the banking sector. We spoke with the Head of Data Governance to explore the bank's responsible AI approach, confirming preparedness for AI regulation. The company's AI Governance Framework ensures oversight of AI applications and adhered to principles like cybersecurity, fairness and reliability. We recommended that CaixaBank publish a responsible AI policy and disclose more on AI implementation to further enhance its leading approach. Commonwealth Bank of Australia (CBA): Advanced Technology and Responsible AI Strategy CBA's responsible AI strategy is globally recognised, leveraging the company's advanced technological background and ethical AI programs since 2018. Ranked first in the Evident AI Index for leadership in Responsible AI, CBA collaborates to manage regulatory and reputational risks. The bank introduced a Responsible AI Toolkit in 2024 and completed 15,000 modules on Generative AI and Deep Learning. We view CBA's approach as leading and are supportive of its ongoing disclosures to shareholders. In 2023, we provided feedback to CBA that it should consider publishing its Responsible AI Policy. The Bank published this policy later the same year and is presently one of the only Australian companies with a publicly disclosed position. HealthcareMedibank: Leveraging AI for customer service and healthcare analytics In early 2024, we engaged with health insurer Medibank to explore AI opportunities in healthcare and the way in which it considers related implications such as data privacy, bias and customer trust. The company has been using AI to support customer call experiences and to improve healthcare analytics. Medibank has established an AI Governance Working Group that evaluates each AI use case before implementation, to consider aspects such as customer, reputation and data risks. We are pleased to share that Medibank has adopted our Responsible AI Framework to benchmark its own practices. Medibank is also considering our feedback on publishing a responsible AI policy and disclosure on AI governance implementation. Intuitive Surgical: Enhancing minimally invasive surgery and patient outcomes with AI US medical device company Intuitive Surgical is a pioneer in health technology and has moved to improve robotic surgery processes through machine learning and predictive analytics. We engaged with the company to better understand these exciting use cases and explore its responsible AI strategy. For instance, postoperative recommendations have become more effective as they combine surgery indicators, such as blood loss or operating time, with patient outcomes like pain levels and recovery. Future opportunities point to AI being used within surgery, for example staplers using AI to measure and adjust tissue compression in real-time to help with precision and patient recovery. The company manages cybersecurity and data privacy to high standards, and we suggested that publishing a responsible AI policy that outlines governance - including its management of important risks like bias and quality control - would be useful to investors. Thermo Fisher: Enhancing healthcare through AI, overseen by a bioethics committee US healthcare company Thermo Fisher Scientific has been using AI and machine learning for many years to streamline internal operations and improve productivity, especially in clinical trials where AI can support disease detection, drug discovery and diagnostics. We engaged with the company to learn more about these AI applications and responsible AI considerations. Thermo Fisher highlighted the role of its bioethics committee, which was established in 2019 and has subject matter experts developing a policy commitment, in guiding its responsible AI activities. We provided information on our Responsible AI Framework and encouraged the publication of the policy in line with best practices. Technology products and platformsNvidia: Launched an AI Ethics Committee and customer KYC process Nvidia is a renowned AI enabler which supplies more than 40,000 companies, including 18,000 AI startups. Early in 2025, we had a meeting in which we discussed the balance between sustainability solutions which could be brought by AI, with the energy and water needed to power these tools. Nvidia highlighted that AI provides many exciting solutions like advanced weather modelling for adaptation and resilience, enhanced maintenance practices via digital twins, and automation and route optimisation to lessen carbon emissions in manufacturing and transport. The company is working to disclose these different end-markets, along with energy and water use, which will offer greater insight into Nvidia's sustainability contributions. Nvidia also established an AI ethics committee in 2024 to oversee the development of AI with an emphasis on trust and ethics. The committee's initial focus was to identify new AI use cases and develop a framework to recognise potential risks in product development and customer use. For instance, the committee recommended additional testing and the implementation of guardrails for a specific product, which subsequently increased due diligence requirements for sales to certain customers. These were subsequently adopted by the development and sales teams. We feel this demonstrates a good level of responsible AI integration through the business. Aristocrat Leisure: Balancing innovation with responsible AI We conducted a responsible AI assessment utilising our framework and engaged with Aristocrat Leisure to understand the AI use cases across its business. We learned that the more recent generative AI use cases include coding, creative development, marketing and general employee productivity. The company has an AI governance program which includes regular use case reviews by a central AI Working Group. This is a good structural model and the Board receives updates at least semi-annually. Aristocrat has also engaged external advisors to provide additional guidance on responsible AI. Workforce impacts and employee sentiment are being considered through employee surveys that measure the impact of AI tools. Overall, we observed that Aristocrat is adopting new AI tools, had a good level of workforce adoption and is building a good foundation in responsible AI. We provided feedback that a responsible AI policy would be a good next step. Industrials and energy servicesSchneider Electric: Enhancing AI and industrial automation Since 2021, French electrical parts company Schneider Electric has expanded AI hubs in India, France, and the US to improve electrification, energy efficiency, and automation. It plans to invest more than $700 million in the US to enable AI growth, domestic manufacturing and energy security, creating 1,000+ new jobs and boosting digital capabilities. In December 2024, we engaged with the company and discussed AI opportunities and responsible practices. Its AI solutions follow strict governance and ethics standards, managing bias and discrimination through a responsible AI program. A broader AI strategy for 2025-2030 is in development, and we provided our research report as feedback. We also recommended publishing an AI policy to enhance confidence in managing AI risks and opportunities. AGL: AI in energy networks AGL Energy has been using AI for some time in various areas, including energy generation, network maintenance and in the electricity retailing part of the business. AGL introduced a relatively recent technology strategy in which AI is one of the four key pillars, and one of the significant use cases discussed was in predictive maintenance. AGL is on the journey to embed responsible AI practices into its operations and are considering suitable governance structures. Reflections and conclusionAs companies continue to invest in AI, the transformative business impacts are becoming increasingly clear. As described in the company engagement examples above, AI's potential is evident in areas such as healthcare, industrial automation, energy management, and improving general productivity through processes like coding, customer service and marketing. From a responsible AI perspective, we have noticed an increase in cross-functional governance structures and policy commitments, as well as a growing awareness of the legal, ethical and ESG risks that come with AI deployment. In terms of external benchmarking, there has been some progress including the finalisation of the ISO27001 AI Safety Standard, which indicates a trend towards verified AI systems. Important disclosure metrics related to responsible AI, however, as detailed in the deep-dive component of our framework, are still in early stages. We would like to see metrics such as the number of AI-related incidents, energy usage from applying AI, cost savings from AI, the number and outcomes of AI audits, and the number and types of complaints related to AI. With 'agentic AI' now the next frontier, we are aware this will bring another level of complexity to AI decisions. We feel that responsible AI governance structures, such as those outlined in our framework, can help organisations to harness AI opportunities, while steering away from some of the risks. Therefore, the three main engagement priorities for portfolio companies are:

Regulatory developments continue to progress (for example, the EU AI Act and the recent AI Action Summit where a joint declaration on inclusive and sustainable AI was signed by 58 countries) but we have observed that no significant or compelling regulations have emerged recently. As such, we continue to monitor resources such as the World Benchmarking Alliance's Digital Benchmark as well as newer benchmarks like the Evident AI Index, which offer useful insights. We have also been broadening our research scope to benchmark and evaluate the ESG risks within the AI value chain, including emissions, energy, and water usage in data centres. We hope to be able to share more on this in future. |

|

Funds operated by this manager: Alphinity Australian Share Fund , Alphinity Concentrated Australian Share Fund , Alphinity Sustainable Share Fund , Alphinity Global Equity Fund , Alphinity Global Sustainable Equity Fund

This material has been prepared by Alphinity Investment Management ABN 12 140 833 709 AFSL 356 895 (Alphinity). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed. |

11 Jun 2025 - Performance Report: Airlie Australian Share Fund

[Current Manager Report if available]

11 Jun 2025 - Performance Report: Quay Global Real Estate Fund (Unhedged)

[Current Manager Report if available]

11 Jun 2025 - Canopy Highlights - insights from our global research

|

Canopy Highlights - insights from our global research Canopy Investors May 2025 With quarterly results now in for most of the companies we follow, we've compiled the latest Canopy Highlights-insights from our global research. Just as investors have faced heightened volatility, business leaders are navigating a similarly complex environment. According to The New York Times and FactSet, 87% of corporate earnings calls this season referenced the word "uncertainty," up from 38% in the previous three months-a theme echoed by many of the companies we look at. Tariffs front and centre While many businesses had already begun diversifying manufacturing and sourcing in response to US tariffs introduced during the previous Trump administration, renewed uncertainty is accelerating those efforts. Take Floor & Décor, a US hard surface flooring retailer: in 2018, ~50% of its products were sourced from China. By the end of FY25, that figure is expected to fall to the low- to mid-single-digits, though most of its sourcing will remain outside the US. Another example is Yeti, which sells drinkware and coolers. While ~80% of its drinkware was produced in China as at the end of FY24, it is targeting a reduction to ~10% by the end of FY25, with most of that capacity being relocated elsewhere in Asia. However, for many, shifting production remains impractical, with most companies indicating plans to pass on tariffs through price increases. Bigger ripple effects? The larger impacts may be indirect: falling consumer confidence, delayed capital decisions, and a general pause in big-ticket spending were cited across sectors-from global luxury to US industrial spending to housing. Much of this stems from a lack of US policy certainty and high interest rates. As Assa Abloy, a global supplier of locks and doors put it: "The challenge with the tariffs is a little bit that it changes every day...So, the answer I can give you is only the answer as it is today, as the tariffs stand...this morning, because perhaps they change this afternoon". Some tailwinds too Not all companies are struggling. Discount retailer Dollar General is benefitting from trade-down by lower-income consumers. Fixed income trading platform MarketAxess is seeing gains from increased market volatility, with average daily credit trading volumes up >30% in April-an improvement from flat growth in the two quarters to March. And some international companies we've spoken with have cited rising anti-American sentiment as a potential commercial tailwind.

|

|

Funds operated by this manager: |

10 Jun 2025 - Performance Report: Bennelong Long Short Equity Fund

[Current Manager Report if available]

10 Jun 2025 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

10 Jun 2025 - Performance Report: Glenmore Australian Equities Fund

[Current Manager Report if available]

10 Jun 2025 - Australian Secure Capital Fund - Market Update

|

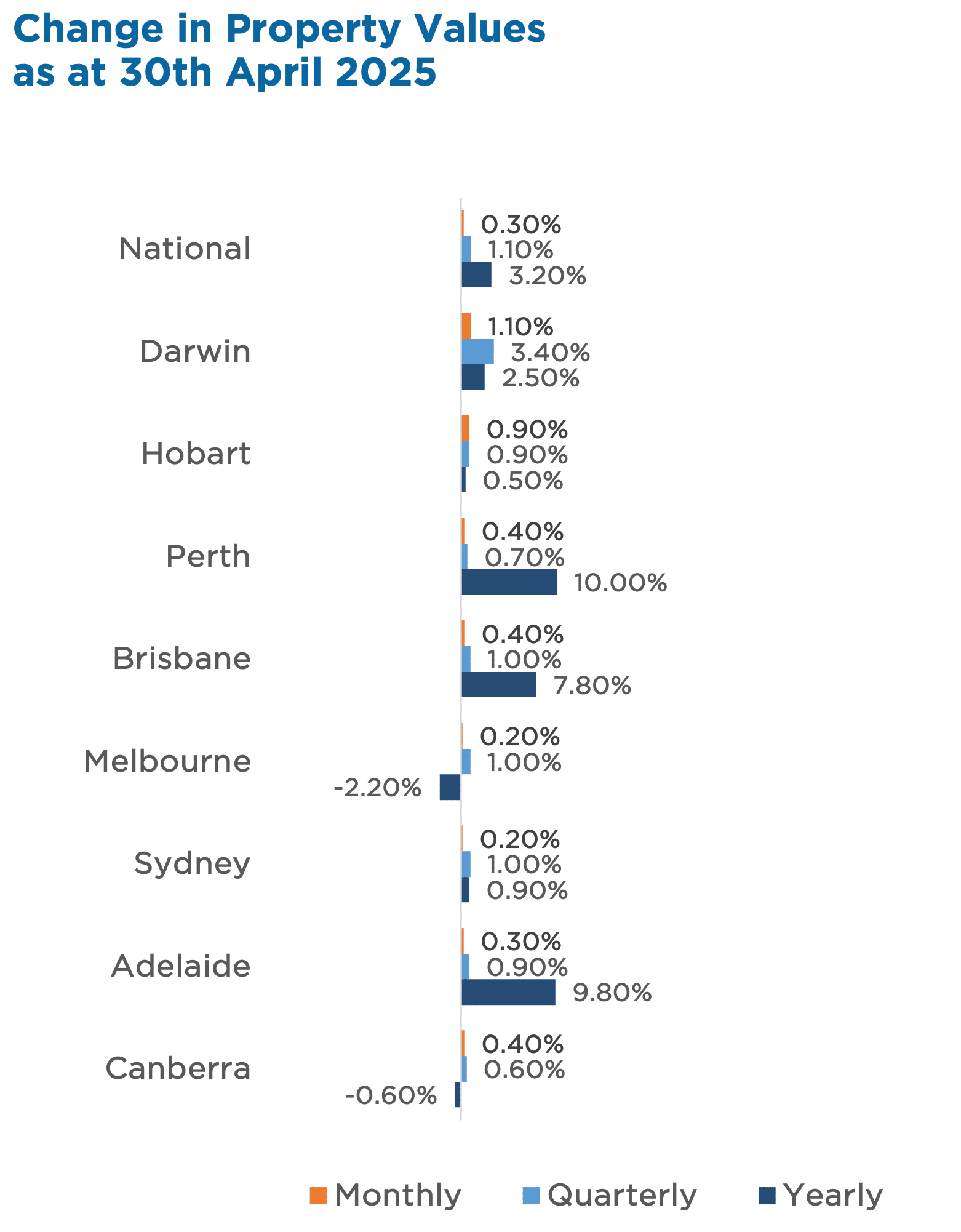

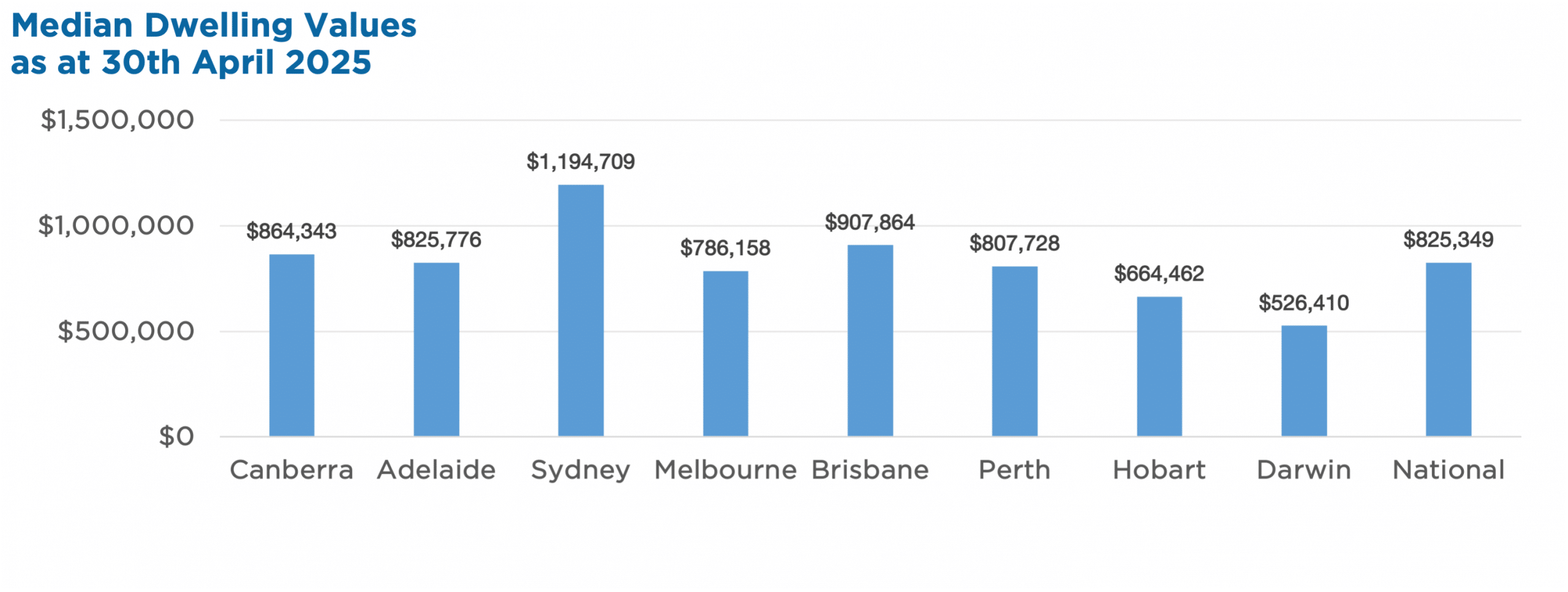

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund May 2025 National home values rose for the third month in a row, with CoreLogic's Home Value Index up 0.3% in April, adding roughly $2,720 to the median Australian dwelling. Growth was recorded across all capital cities, though the pace slowed slightly from March. While mid-sized capitals and regional markets led the charge, Sydney and Melbourne remain below previous highs. Annual growth eased to 3.2%, reflecting last year's broader slowdown despite a recent rebound since February's rate cut. Key Highlights:

Property Values

|