News

Stock Story: Ampol

Pathway to unlocking value outside the headlines. (5-minute read)

Read more...

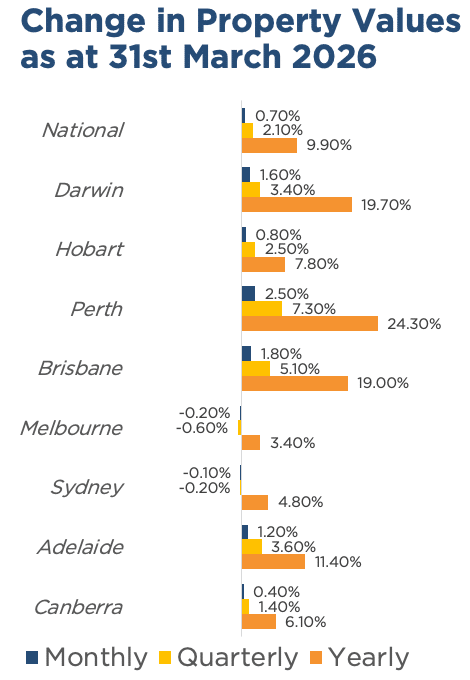

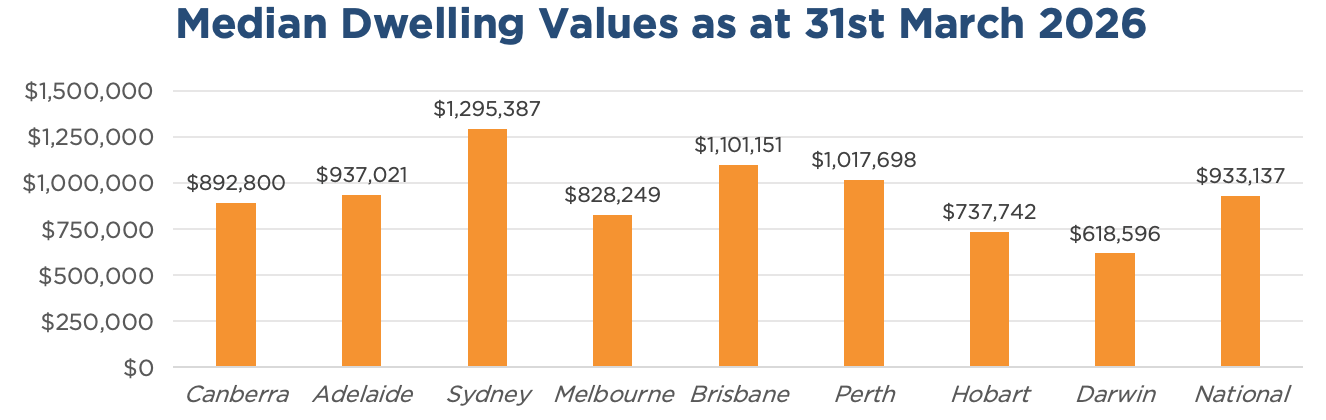

Australian Secure Capital Fund - Property Update

March was another steady month for Australian property values, posting a national rise of 0.7%, down slightly from 0.8% in February. (1-minute read)

Read more...

Manager Insights | Altor Capital

Chris Gosselin, CEO of FundMonitors.com, speaks with Benjamin Harrison, Chief Investment Officer at Altor Capital.

Read more...

Expert analysis on what the RBA will do next Tuesday, May 5

Chris Gosselin, CEO of FundMonitors.com, speaks with Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management and Renny Ellis, Director & Head of Portfolio Management at Arculus Funds Management.

Read more...

Hedge Clippings | 01 May 2026

The March inflation number looks ugly at first glance. Headline CPI jumped to 4.6%, up from 3.7% in February, with transport, housing and food doing much of the damage.

Read more...

Performance Report: Equitable Investors Dragonfly Fund

The Equitable Investors Dragonfly Fund has delivered positive returns 58% of the time since inception in September 2017, in months when the market was positive. March was a challenging month for microcaps, with Energy Technologies the top...

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund has delivered positive returns 93% of the time since inception in November 2009, in months when the market was positive.

Read more...

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund has returned +16.73% per annum since its inception in June 2017, an outperformance of +8.08% relative to the ASX 200 Total Return benchmark which has returned +8.65% on an annualised basis over the same period.

Read more...

Performance Report: Cyan C3G Fund

The Cyan C3G Fund has delivered positive returns 77% of the time since inception in August 2014, in months when the market was positive.

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +1.00% in March, outperforming the RBA Cash Rate + 5% benchmark by +0.27%. Since inception in April 2018, the fund has returned +11.52% per annum, an outperformance of +4.40% relative to the benchmark...

Read more...