News

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund rose by +4.44% in April, outperforming the ASX 200 Total Return benchmark by +2.26%. Since its inception in June 2018, the fund has returned +8.86% per annum, an outperformance of +0.13% relative to the...

Read more...

Performance Report: Insync Global Capital Aware Fund

The Insync Global Capital Aware Fund has delivered positive returns 81% of the time since inception in October 2009, in months when the market was positive.

Read more...

Prediction Markets: The next big disruption in investing?

Prediction markets are moving from niche to mainstream and Investment Analyst, Emma Williams explores why traditional finance is starting to pay attention. Emma explains how these markets turn opinions into tradable probabilities, offering...

Read more...

Performance Report: Seed Funds Management Financial Income Fund

The Seed Funds Management Financial Income Fund rose by +0.65% in April, outperforming the Solactive Australian Hybrid Securities (Net) benchmark by +0.48%. Since its inception in October 2015, the fund has returned +6.35% per annum, an...

Read more...

Performance Report: Quay Global Real Estate Fund (Unhedged) Active ETF...

The Quay Global Real Estate Fund (Unhedged) Active ETF (ASX:QGRU) rose by +3.95% in April, outperforming the FTSE EPRA/ NAREIT Developed NET TR benchmark by +0.57%. Since its inception in January 2016, the fund has returned +5.59% per...

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund rose by +2.27% in April, outperforming the ASX 200 Total Return benchmark by +0.09%. Since its inception in November 2009, the fund has returned +8.78% per annum, an outperformance of +0.57%...

Read more...

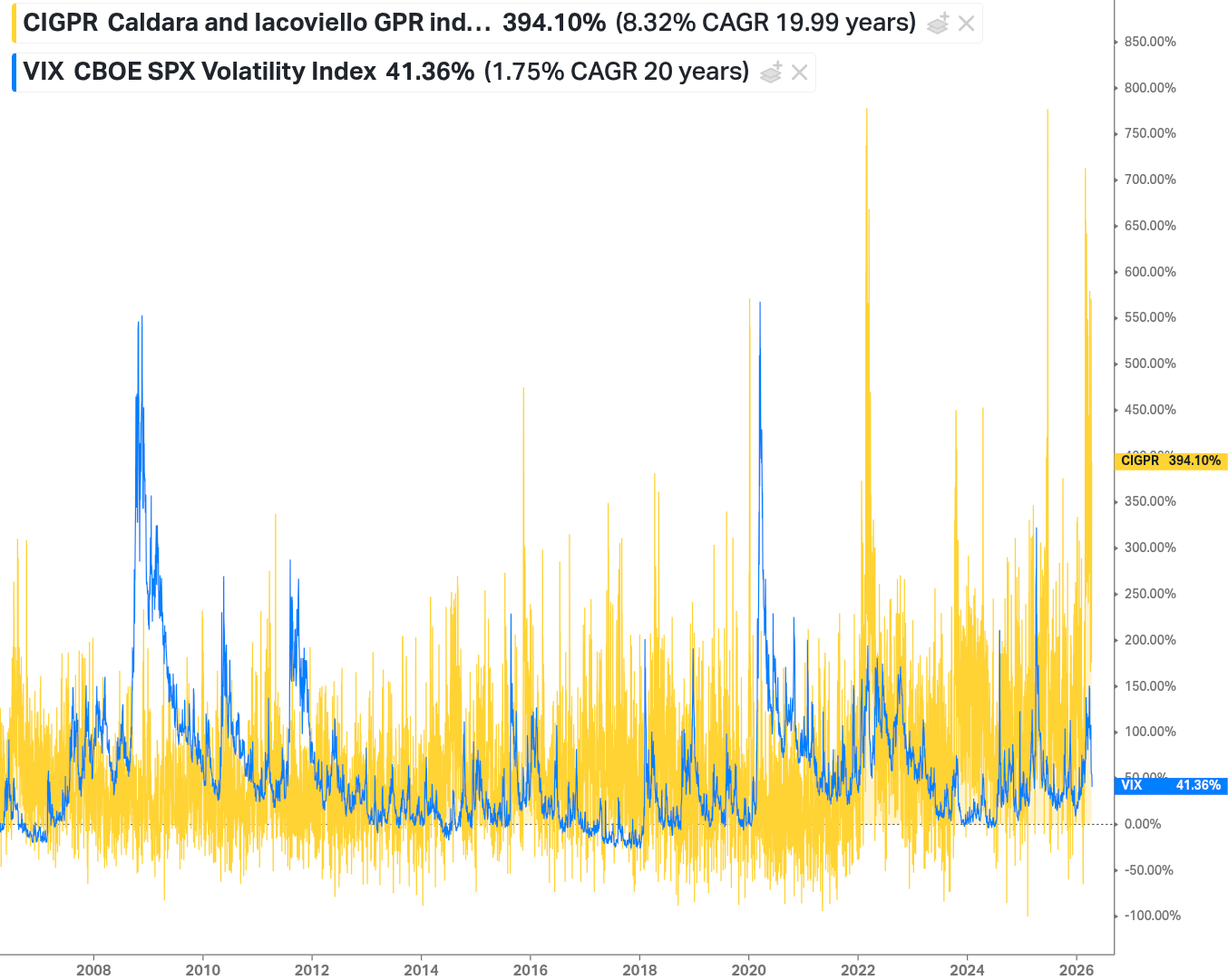

10k Words | April 2026

We couldn't help but look at geopolitical risk again - with the spike in a longer historical context than shown in March (2-minute read)

Read more...

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) rose by +13.95% over the past 12 months, outperforming the S&P Global Infrastructure TR (AUD) benchmark by +1.96%, which has returned +11.99%.

Read more...

Hedge Clippings | 08 May 2026

This week saw the RBA meet most market observers' expectations by increasing rates by 0.25%...

Read more...

Performance Report: Bennelong Australian Equities Fund

The Bennelong Australian Equities Fund rose by +3.63% in April, outperforming the ASX 200 Total Return benchmark by +1.45%. Since inception in February 2009, in the months where the market was positive, the fund has provided positive...

Read more...