News

Performance Report: Cyan C3G Fund

The Cyan C3G Fund rose by +16.11% over the past 12 months. In August, strong gains from EROAD (+56%) and Acusensus (+12%) were offset by weaker performances from Alcidion (-17%), ReadCloud (-14%) and Raiz (-12%), while Cyan remains...

Read more...

Build-to-rent housing: igniting the firepower of local pension funds

Is build-to-rent the key to hitting national housing targets?

Read more...

Performance Report: Argonaut Global Gold Fund

The Argonaut Global Gold Fund rose by +16.00% in August, outperforming the S&P Global Natural Resources AUD (TR) benchmark by +11.40%. Since inception in November 2022, the fund has returned +28.38% per annum, an outperformance of +22.38%...

Read more...

Performance Report: ECCM Systematic Trend Fund

The ECCM Systematic Trend Fund rose by +6.61% in August, outperforming the SG Trend benchmark by +3.87%. Since inception in January 2020, the fund has returned +11.90% per annum, an outperformance of +6.58% relative to the benchmark which...

Read more...

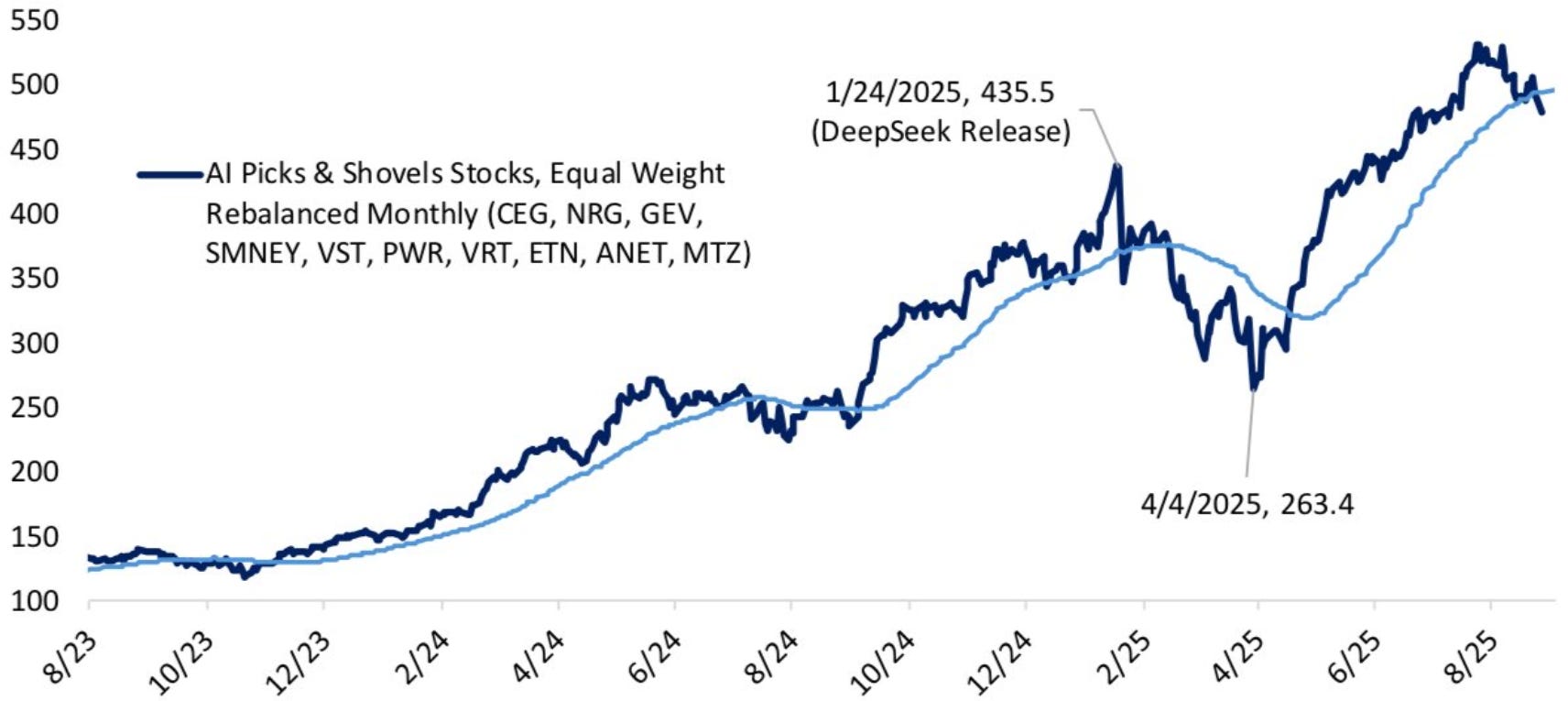

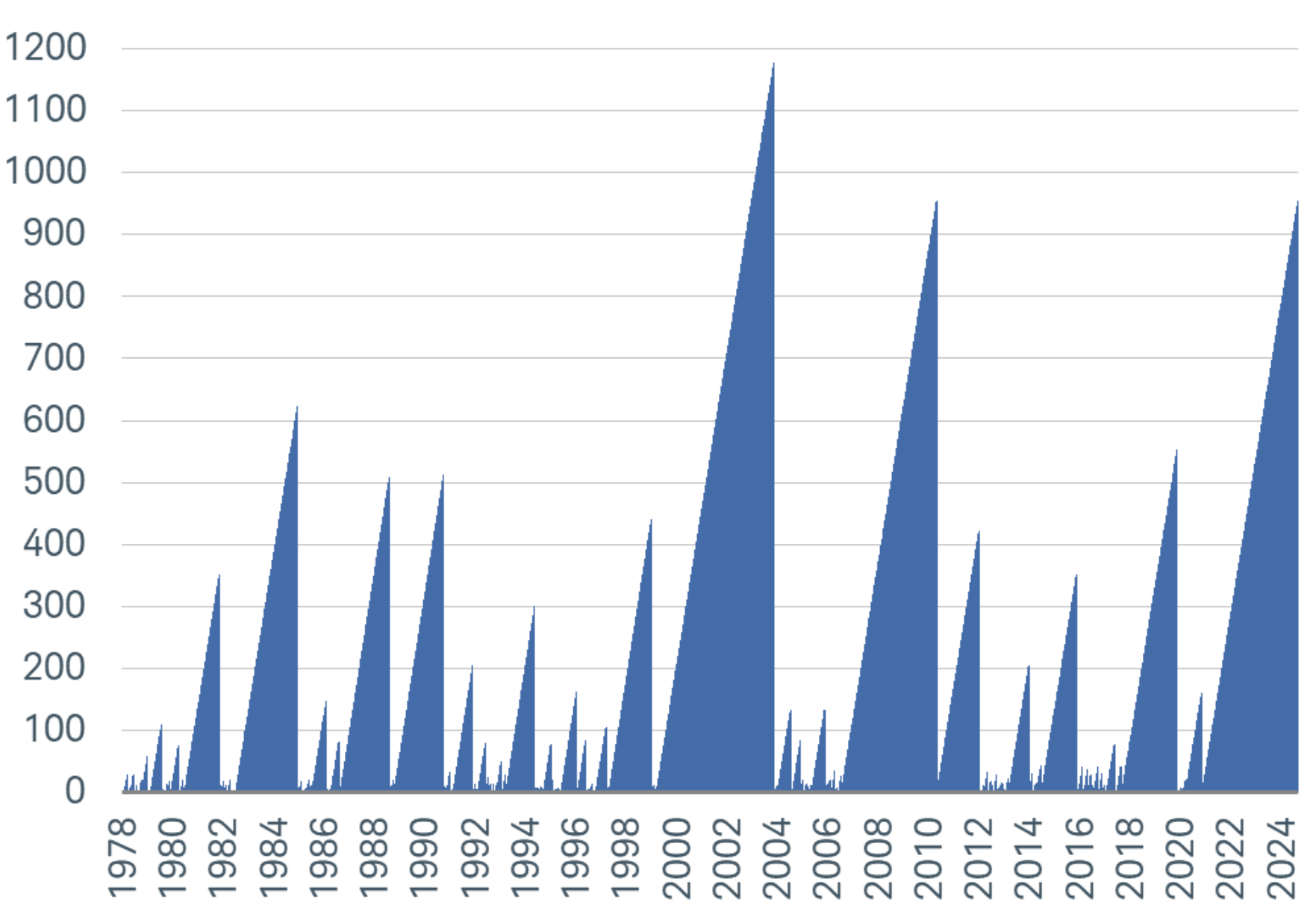

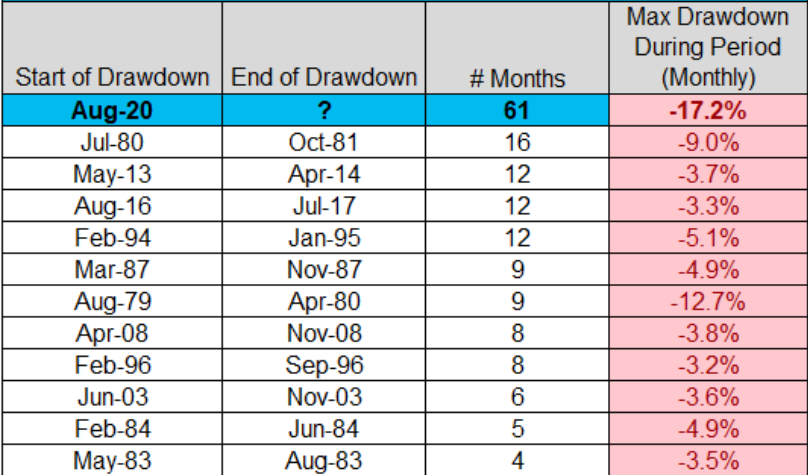

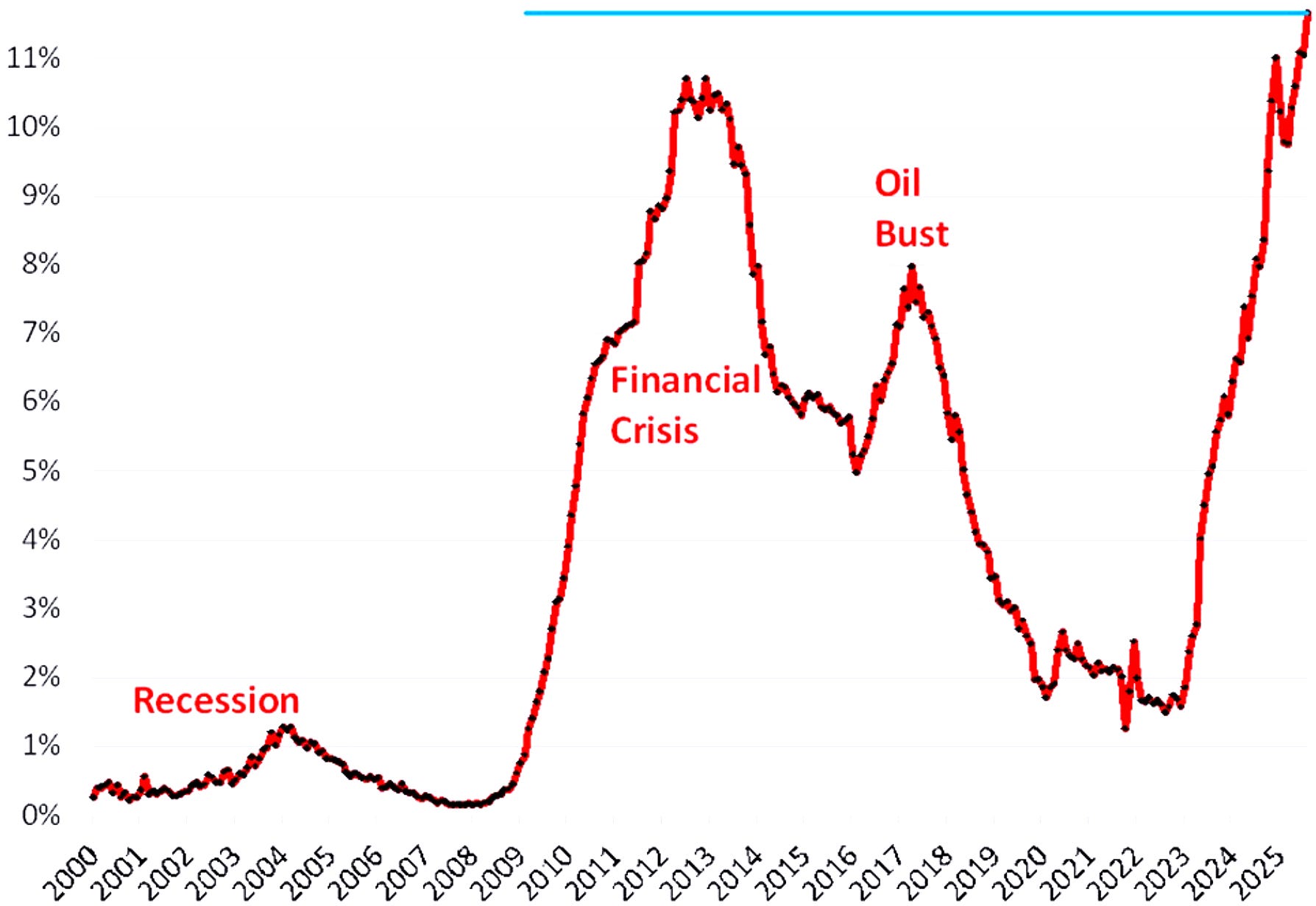

10k Words |September 2025

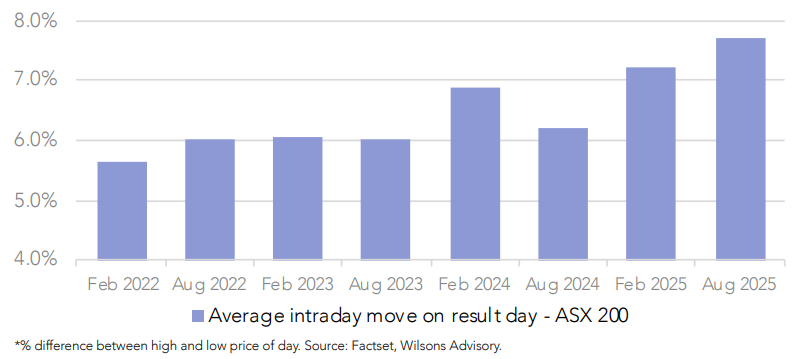

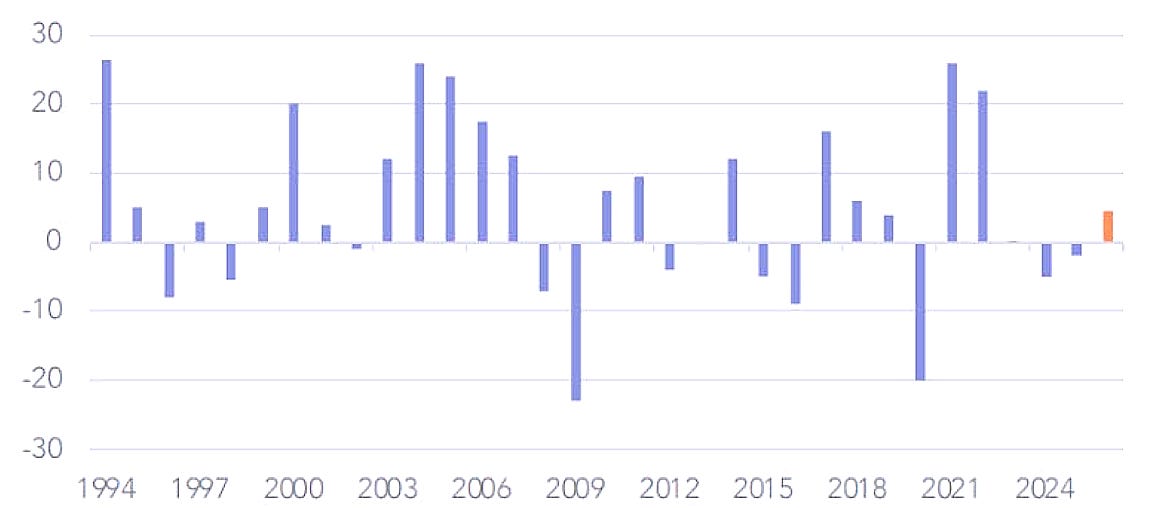

Record volatility amid an ASX reporting season delivering another year of flat-to-negative growth. Australian GDP in the June quarter compared well with peers but on a per capita basis things have been going backwards since Q4 2022.

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund rose by +6.01% in August, outperforming the ASX 200 Total Return benchmark by +2.91%. Since inception in November 2017, the fund has returned +21.13% per annum, an outperformance of +11.51% relative to...

Read more...

New Funds on Fundmonitors.com

Here are some of the latest additions to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research,...

Read more...

Hedge Clippings |12 September 2025

The Federal Reserve faces a delicate balancing act ahead of its September meeting: inflation remains stubbornly above target while the US labour market shows signs of weakening. Markets are betting on a rate cut, but whether it marks the...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +1.01% in August. Since inception in January 2013, the fund has returned +13.09% per annum, an outperformance of +3.40% relative to the ASX 200 Total Return benchmark which has returned +9.69% on an...

Read more...

Performance Report: Seed Funds Management Hybrid Income Fund

The Seed Funds Management Hybrid Income Fund rose by +0.74% in August. Since inception in October 2015, the fund has returned +6.43% per annum, an outperformance of +1.58% relative to the Solactive Australian Hybrid Securities (Net)...

Read more...