News

15 May 2025 - Is this now an opportunity for china exposed stocks?

|

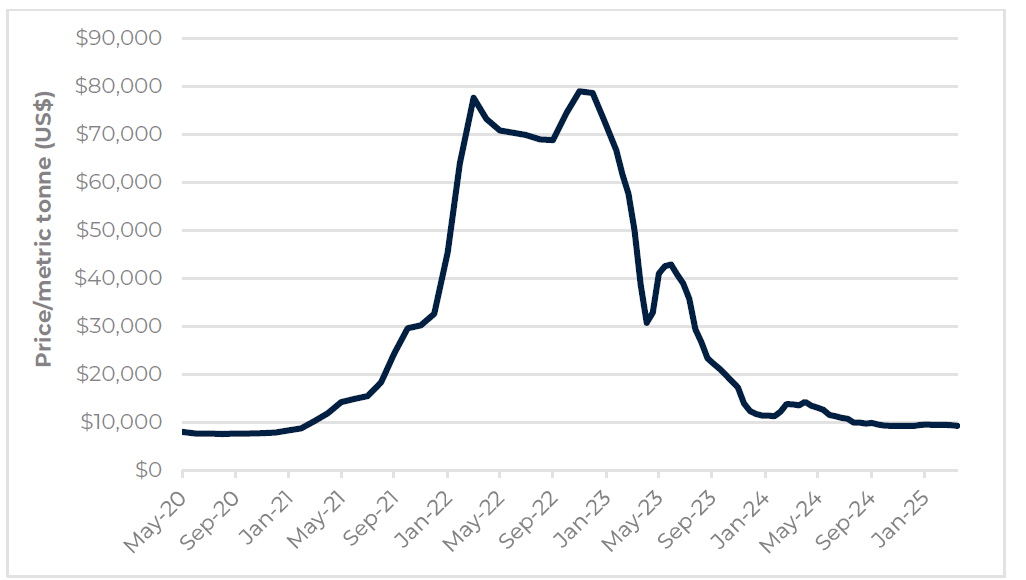

Is this now an opportunity for china exposed stocks? Tyndall Asset Management May 2025 After a significant price correction in China exposed stocks over the last year, Tyndall's Jason Kim recently went to China and met with various companies and industry experts to help determine whether some of these stocks now represent a real opportunity for investors. During the course of 2024, Australia's largest trading partner, China, went through a significant economic downturn on the back of a residential property downturn after a weak COVID bounce when China came out of lockdown in late 2022. This resulted in poor consumer sentiment, which then spiraled into a negative feedback loop with business confidence which became more pronounced during 2024. This not only impacted the broader share market, but more specifically, it directly impacted resource stocks and those companies with significant exposure to Chinese consumers. Key takeawaysAfter facing soft demand, and deflation in China during 2024, the general view for the Chinese economy was that 2024 saw the low point for the economy, and that 2025 is likely to see some improvement. Overall demand growth is at least going to improve to be marginally negative to flat, and it is possible that we see a very modest recovery. Residential property prices in tier 1 and 2 cities are now starting to show some signs of stabilisation, post-September policy support, and arguably there may now be some green shoots. However, property prices in the lower tier cities are still weak, resulting in consumer sentiment still remaining fragile. Given the focus on improving consumer sentiment, it appears most likely that any Chinese government stimulus will be targeted more at the consumer rather than in construction/fixed asset investment, and that measures will be taken to help stabilise - rather than stimulate - residential property prices. This clearly has negative implications for steel and iron ore. The key risks are US tariffs and geopolitical tensions which remain a significant wildcard impacting exports and overall sentiment. However, many experts noted that the Chinese government may have been holding back some stimulus to leave enough fire power to properly address the negative implications from the US tariffs. Key Investment OutlookIron Ore China produces approximately 1 billion tonnes of steel per annum. Due to a weak Chinese economy last year, we saw softer demand for steel domestically and an increase in steel exports to c100kt pa to shift excess production. This has seen steel profit margins decline. After meeting many steel mills, iron ore traders, and steel traders, the consensus view is that domestic steel demand still remains soft, with property and infrastructure seeing a modest contraction in demand. The key bright spots for demand are in the consumer related sectors - namely auto and appliances - after some recent consumer stimulus sought to increase demand in those industries. This view is in-line with what was discussed previously. China has increasingly imposed stricter and more frequent air pollution controls, requiring the steel mills to reduce production to reduce emissions, and this may be the mechanism that the authorities will use to help reduce oversupply. There is speculation that a government mandated production cut of 50 million tonnes per annum is imminent. Lithium An incredible surge in lithium prices in 2021 and 2022 - peaking at around $US80,000 in Dec 2022 - saw a swathe of new lithium supply come to market, which perhaps unsurprisingly was followed by a spectacular decline in prices (refer Figure 1). Figure 1: The Lithium Rollercoaster

Source: Bloomberg, April 2025. After having met many Chinese lithium miners and lithium battery makers, it appears that even after this significant price correction the outlook for lithium prices still remains challenged. Despite growing demand for lithium as we transition to renewables and EVs globally, the expected growth in supply flagged by the lithium miners we met would suggest that any demand growth will at least be met by supply growth into the medium term. Portfolio ImplicationsGiven the near-term challenges for iron ore, we have moderated our overweight position in the iron ore miners to be marginally overweight. This acknowledges that any stimulus from China, while likely to be more targeted at the consumer, could still be incrementally positive for mining stocks. Our key overweight in this sector is Rio Tinto due to its strong forecast free cash flows, and participation in the Simandou project which will be a source of meaningful growth in iron-ore supply in the near future. While lithium miners may appear attractive at current share prices, our trip suggests it is likely too early to enter this space given the challenging oversupply outlook. We continue to monitor this sector closely for any potential opportunities. Author: Jason Kim, Portfolio Manager Funds operated by this manager: Tyndall Australian Share Concentrated Fund, Tyndall Australian Share Income Fund, Tyndall Australian Share Wholesale Fund |

14 May 2025 - Tarrifs & trade wars

14 May 2025 - Isolation day: the geopolitical impact of Trump's tariffs on the world

|

Isolation day: the geopolitical impact of Trump's tariffs on the world Nikko Asset Management April 2025 "Shock and awe" intendedWhen news broke of Donald Trump's resounding victory at the November 2024 US presidential elections, many countries and businesses girded themselves for another round of trade wars. But this time, the 47th US president upped the ante from his previous term by imposing across-the-board tariffs on friends and foes alike. The Republican party's majority in both the US House of Representatives and Senate helped to ensure that Trump would have near-unchecked power, leading to such policy extremes. In light of these developments, we see markets as the remaining check and balance to hold the current administration's actions to account in the immediate term. As would be expected, Trump's tariffs roiled global stock markets. We therefore expect risk premiums for US assets to remain elevated for some time. Prior to the outcome of the US elections, we had explored the likely implications of a second Trump presidency and potential implications for portfolio companies in "If Trump wins: uncertainties and opportunities from an Asian equity perspective". Similarly, from a global perspective, the pronounced market volatility suggests that it will be hazardous to sell following large declines and to buy after major upturns unless we have greater conviction that concrete steps are being taken towards de-escalation. Energy and commodities also took a hit as the ongoing trade disputes raised doubts over future demand. We expect crude oil prices to remain lower for longer though other commodities may be more economically sensitive and thus, volatile. In our view, Trump's re-escalation of the tariff wars will only exacerbate the slowdown in global growth and may potentially plunge the US into recession unless his administration significantly reverses course with key trading partners including China, the European Union (EU), Canada and Mexico. Another factor which could prevent an impending US downturn is intervention by the Federal Reserve (Fed). However, the Fed faces a very tough task, as rising inflation poses a risk that could make it challenging for it to further reduce interest rates. China in the crosshairsAlthough seemingly indiscriminate, the so-called "Liberation Day" tariffs primarily targeted China. We believe that Washington will maintain this approach even if it rolls back punitive measures, such as with the surprise 90-day reciprocal tariff reprieve announced by the White House, for all countries apart from China. The chaos caused by Trump's unpredictable actions may seem surreal, almost like events from a reality TV show. Nonetheless, we believe he is still a businessman at heart with deal-making as his main objective. The ability of all countries to weather the US tariffs hinges on sound policy decisions, supportive domestic demand, capacity to stimulate the economy via monetary and fiscal means and the ability to negotiate concessions with the Trump administration by increasing purchases of US goods or investment. We think this last point may help countries to secure a bigger share of the export manufacturing market to the US over time if balanced correctly. The country with the most potential in this regard is India, which also stands to benefit from a sustained drop in energy prices. Most countries in Asia will likely try and hold discussions with the Trump administration. To date, over 75 countries have sought to strike a deal with the White House. Given Trump's preference to conduct one-on-one talks, we feel it would be prudent for the Association of Southeast Asian Nations (ASEAN) to negotiate as a bloc for more favourable terms as opposed to a country-by-country basis. For potential guidance ASEAN can look at the EU, which has banded together even more closely amid current developments. In the context of Asia excluding Japan, although countries that are part of the "China plus one" risk diversification strategy were also hit with tariffs to varying degrees, most of them are in the process of negotiating trade agreements with the White House. We believe that they could potentially be well-positioned to benefit from subsequent lowered duties as well as the accelerating trend of diversifying supply chains away from China. Meanwhile, the Philippines' services and agriculture-focused economy means that the reciprocal tariffs, which mainly penalise manufacturing hubs in Trump's quest to bring such jobs back to the US, will have less of a negative impact on the Philippines. And finally, while India is yet to officially respond to the sweeping US tariffs, we believe that its economy, driven more domestic consumption, puts it in a stronger position to negotiate a more favourable trade agreement with Trump compared to countries more heavily reliant on exports. Sino resolutionChina, however, is not having any of it. Compared to Trump's first term in office, Beijing is hitting back more forcefully with tit-for-tat tariffs having learned the hard way that any signs of weakness will certainly be exploited. With neither Trump nor Chinese President Xi Jinping likely to back down, we believe China's actions must be accompanied by corresponding domestic support packages to prevent Chinese assets from suffering collateral damage. Further restrictions on investments in China or the US could be on the cards should tensions escalate. US Treasury Secretary Scott Bessent raised the possibility of delisting Chinese companies from local stock exchanges following the tariffs announcements. Beijing had also earlier ordered the National Development and Reform Commission to halt approvals for Chinese firms aiming to invest in the US. Government officials have said China is ready to lower interest rates and relax the reserve requirement ratio to stimulate the economy in the face of rising trade tensions with the US. In a planned emergency meeting of high-level economic officials, we expect the authorities to redouble efforts to bolster consumption, artificial intelligence (AI) and energy infrastructure and focus on localising industries such as medical devices. Initial measures to boost domestic consumption are expected to include the streamlining of duty-free purchases by inbound tourists, which could benefit duty free names. The measures could also include a plan to ramp up health-related consumption though fitness and sports initiatives and the promotion of high-quality agricultural products. These are likely to be just the beginning of a series of policies aimed at supporting domestic demand. Manufacturing mayhemAt a sectoral level, pharmaceutical and semiconductor imports are currently not subject to US reciprocal tariffs. However, Trump is threatening to revoke these exemptions as part of a wider national security agenda. Chinese companies in these industries are the likely targets of future measures. In the broader manufacturing space, we view flexibility in production as necessary for supply chain resilience as per Apple's decision to produce more iPhones in India in a shift away from China. Nevertheless, committing to longer-term manufacturing capital expenditure decisions poses significant challenges under current conditions. A new world order born of fundamental changeTrump's unprecedented actions have torn down the established global trade order as the US seeks to structurally cut its deficit and bring back manufacturing jobs, while China has been making attempts to shift away from an export-led economy towards consumption-driven growth. The 90-day tariff moratorium may provide nations some time to assess the optimal route to navigate these US tariffs. However, the risk of further escalation is very real, given that the world's two largest economies are adamant about not appearing weak in the eyes of the other. Regardless of who gains the upper hand in the end, all countries will need to chart a new course into the proverbial unknown. Volatility typically brings both risk and opportunities. Significant fundamental changes have been set in motion and will lead to long-term, sustainable investment opportunities in the days and months ahead. Cutting through the noise and bluster to identify longer term investment opportunities is what excites us. Over the last 15 years, US equities and assets have been the biggest beneficiary of global portfolio flows. However, if US risk premiums are expected to remain elevated for an extended period, investors are likely to ask, "Where else should I reallocate my capital to"? We would not rule out large parts of Asia. Funds operated by this manager: Nikko AM ARK Global Disruptive Innovation Fund, Nikko AM Global Share Fund Important disclaimer information Please note that much of the content which appears on this page is intended for the use of professional investors only. |

13 May 2025 - The Future of Travel: How AI-powered travel agents are revolutionising the industry

|

The Future of Travel: How AI-powered travel agents are revolutionising the industry Magellan Asset Management April 2025 |

Planning and booking travel has long been a frustrating and time-consuming process. Travellers must sift through countless flight and hotel options, read reviews, juggle different booking platforms and coordinate schedules - all while trying to secure the best deals.However, the future of travel is about to be transformed by a new technological force - AI-powered travel agents. Unlike traditional AI, which waits passively for instructions from users, AI agents will independently navigate websites, make decisions, solve problems and adjust your travel itinerary on your behalf - just like a personal assistant, but fully automated. This isn't a distant dream; it's a reality we expect travellers to experience within the next decade. The travel industry is transforming and investors who act now will secure the biggest rewards. This breakthrough is being driven by breakthroughs in hardware and software. Advanced computing chips, which power AI training models, and sophisticated AI algorithms such as OpenAI's ChatGPT, Google's Gemini and Meta's LLaMA, are key enablers of this revolution. The most recent advancement occurred in January when OpenAI launched its next iteration of ChatGPT, Operator, an AI agent capable of independently navigating websites. Its applications extend far beyond travel, handling tasks like online shopping, filing expense reports and making restaurant reservations. By mimicking human interactions, Operator marks a major shift towards truly proactive, self-sufficient AI. These technological advancements have sparked a wave of investment and innovation across the travel industry, creating both exciting opportunities and new risks for investors. Established travel companies, agile startups and tech giants are all racing to build AI agents that could disrupt traditional travel search engines and capture significant market share. Tailored trips: Let your AI agent handle the detailsOne of the most powerful shifts brought by AI agents is personalisation. Instead of users manually searching for flights and accommodation, AI agents will predict your preferences, suggest destinations and secure bookings without requiring constant input. Imagine telling an AI agent you'd like to plan a European getaway in July. Instead of browsing for hours, your AI agent will instantly:

This reduces search time, eliminates decision fatigue and unlocks destinations travellers may never have considered. AI now smarter, cheaper, everywhereFor companies looking to capitalise on the AI agent opportunity, the first step is securing access to leading AI algorithms from OpenAI, Google and Meta. As the cost of computing continues to decline, access will become more affordable. A prime example of this shift is DeepSeek, a Chinese AI company that has demonstrated that building and training AI models can be cheaper and more efficient. This is a great outcome for AI infrastructure users such as established travel companies, allowing them to develop proprietary models while minimising their investment requirements. As AI tools become increasingly ubiquitous, the barriers to entry for companies looking to integrate AI will continue to shrink, enabling broader innovation. Data is the new travel currencyAs advanced AI infrastructure becomes widely accessible, the important question for investors is "Who will come out on top?" The power of AI lies in the underlying data. Companies with access to the richest datasets can generate superior customer insights and will dominate. For example, a company with a large user base and strong customer relationships understands a customer's travel preferences, spending habits, location history and real-time market trends, a valuable asset. For this reason, smaller competitors will likely suffer. Additionally, traditional players including shopfront travel agents, group tour companies and companies like TripAdvisor risk ceding share as AI agents eliminate the need for manual searches, directly connecting travellers with bookings and personalised recommendations. Existing giants like Booking Holdings, the parent company of Booking.com, have massive user bases and loyalty programs, giving them access to vast customer data. Booking Holdings is already incorporating insights into its early-stage AI agent to enhance the customer experience and streamline the travel booking process. In an AI-powered world, travellers are encouraged to go directly to the Booking platform, strengthening its control over the customer relationship. In this scenario, Booking's business quality and profitability are likely to strengthen, supported by a stronger market position and reduced reliance on expensive search-engine traffic. Hospitality experts the big winners in an AI-driven worldIn addition to AI infrastructure and customer data, deep expertise in travel and hospitality is essential for building effective AI agents. AI agents are here, and travel will never be the sameThe future of travel is being rewritten, with AI agents at the heart of this transformation. As the industry evolves, a fierce data race will unfold, with new sources being used to infer traveller preferences. Companies that can capture, refine and apply the richest travel insights will gain the upper hand. Tech giants are interesting in this context, as they already hold key insights into consumer behaviour: Google can scan your Gmail history for past travel bookings and requests, Apple has access to conversation data where you may be planning a trip with friends and family, and Meta, through Instagram, can analyse your travel-related posts and tagged destinations to predict future behaviours. While large tech companies may have information on the customer, they lack the operational knowledge, long-standing relationships and industry-specific insights that predicate success in the hospitality sector. Therefore, big tech's most viable monetisation path is through strategic partnerships with established travel players like Booking Holdings, Marriott and Hilton. For investors, this period of rapid change offers exciting opportunities and new risks to consider. Those investors who back the right companies will be at the forefront of the next evolution of travel, where seamless, hyper-personalised experiences redefine the industry. Market leaders will strengthen their dominance, while those slow to adapt risk being left behind in an AI-first world. The winners of this transformation will not just survive the disruption; they will shape the future of travel itself. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Core Infrastructure Fund, Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged) Important Information: Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

In this environment, the biggest winners will be companies that maintain direct relationships with accommodation owners, giving them greater control over service standards, property presentation and pricing. This close partnership is exemplified by franchised hotel chains like Hilton and Marriott, which work directly with their vast network of hotel owners. Hilton and Marriott don't just connect hotel owners with travellers; they are deeply integrated partners, offering decades of hospitality expertise that is incredibly difficult for tech giants to replicate. They provide hands-on support for hotel operations, labour management and supply procurement, even guiding owners through the hotel development process. To secure this valuable expertise, hotel owners sign long-term contracts - often up to 20 years - with these franchised giants, ensuring they maintain a vast network of properties for travellers to choose from in this era of technological change.

In this environment, the biggest winners will be companies that maintain direct relationships with accommodation owners, giving them greater control over service standards, property presentation and pricing. This close partnership is exemplified by franchised hotel chains like Hilton and Marriott, which work directly with their vast network of hotel owners. Hilton and Marriott don't just connect hotel owners with travellers; they are deeply integrated partners, offering decades of hospitality expertise that is incredibly difficult for tech giants to replicate. They provide hands-on support for hotel operations, labour management and supply procurement, even guiding owners through the hotel development process. To secure this valuable expertise, hotel owners sign long-term contracts - often up to 20 years - with these franchised giants, ensuring they maintain a vast network of properties for travellers to choose from in this era of technological change.

12 May 2025 - The Resurgence of Nuclear Energy

|

News & Views: The Resurgence of Nuclear Energy 4D Infrastructure May 2025 Nuclear energy is undergoing a renaissance. While it has long been associated with images of devastation and disaster, it is now increasingly recognised as a crucial part of the global energy transition, offering a reliable solution to rising energy demand and decarbonisation efforts. In this edition of News & Views we examine the decline of nuclear energy, the catalysts behind its resurgence and how the 4D investment strategy captures exposure to this evolving theme. Why did nuclear decline?1. Public fearAt its peak in the late 1990s to early 2000s, nuclear energy accounted for nearly 17% of global electricity generation, compared to around 9% today. Incidents like Three Mile Island in the US in 1979 and Chernobyl in 1986 increased public anxiety around nuclear energy. While both these incidents resulted in greatly increased safety regulations and oversight, the stigma remained. The 2011 Fukushima disaster in Japan reignited safety concerns, resulting in several countries scaling back or halting their nuclear programs. The US for example increased regulatory scrutiny while Germany decided to exit nuclear power altogether. 2. High costs and complex constructionHigher safety standards and regulatory obligations have made nuclear projects increasingly expensive. The need for more advanced safety systems, robust containment structures and ongoing design and regulatory changes have all increased the cost to build, operate and maintain nuclear power plants. Project management complexities have also been detrimental. With less nuclear plants being built, the industry experienced a loss of skilled labour and expertise in nuclear construction. This, coupled with the incredible complexity yet lack of standardisation in plant build, has also led to increased inefficiencies and costs. As a result, many of the more recent nuclear power plant projects have seen significant delays and cost overruns. Examples include:

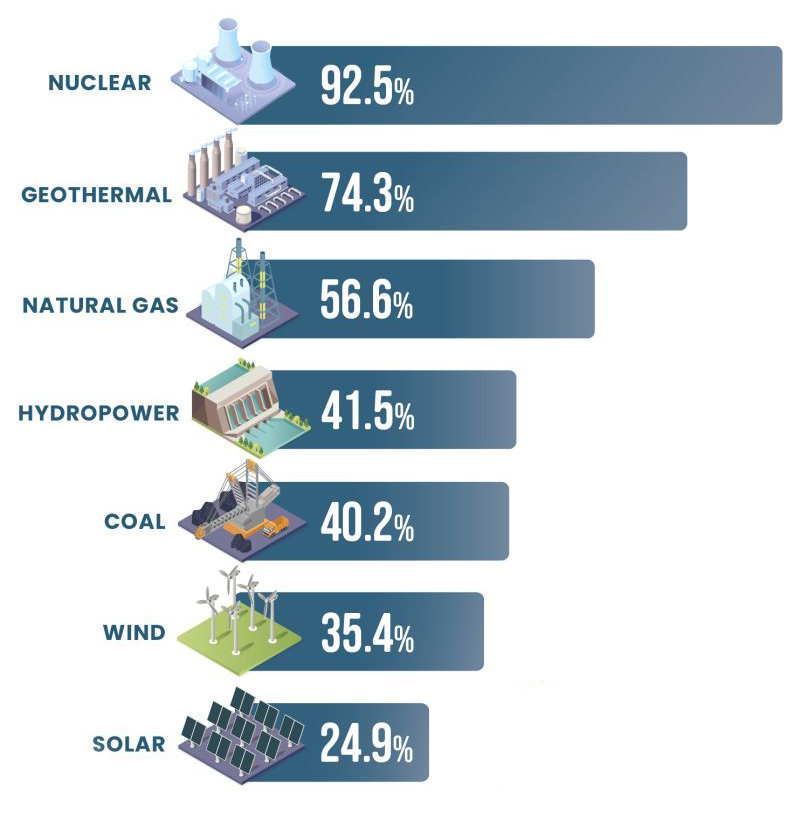

What's driving nuclear's revival?1. Reliable, carbon-free baseload powerNuclear energy offers continuous, emissions-free power -- a valuable complement to intermittent renewables like wind and solar. While wind and solar energy are expanding, they remain intermittent, generating electricity only when the wind blows or the sun shines. Managing this intermittency requires energy storage to store excess energy during high-output periods and release it during high-demand or low-generation periods. Even though storage technology and deployment has grown rapidly, costs remain too high to implement at scale. At the same time supply pressures are increasing as coal and gas-fired power plants being phased out or growing more slowly. This is why nuclear energy stands out as the only large-scale baseload power source that can reliably bridge the supply gap, combat climate change and avoid the intermittency challenges of other renewables. Capacity Factors across various energy sources

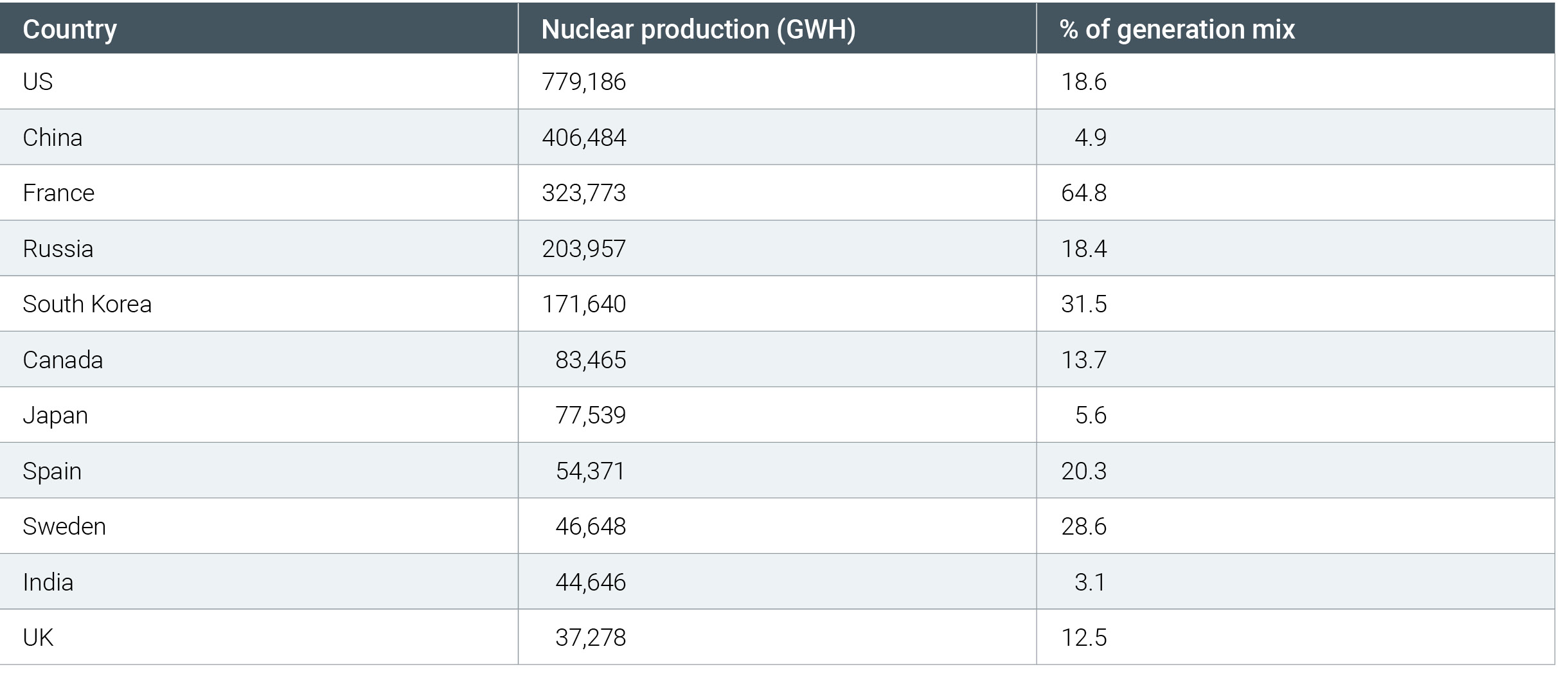

It is important to note that even with safety and cost concerns, nuclear continues to be a pivotal component of the electricity generation mix for many countries. For example, in France, where nuclear accounts for approximately 65% of the generation mix, power prices have remained relatively low compared to other European countries. The relatively low cost of nuclear power generation has also contributed to France becoming one of the world's largest net exporters of energy, bringing in €5bn in revenues in 2024.1 Recognising the value of nuclear power assets, France plans to replace its aging nuclear fleet with six new reactors by 2050, with an option for an additional eight. Nuclear Production 2023 and Proportion of Generation Mix

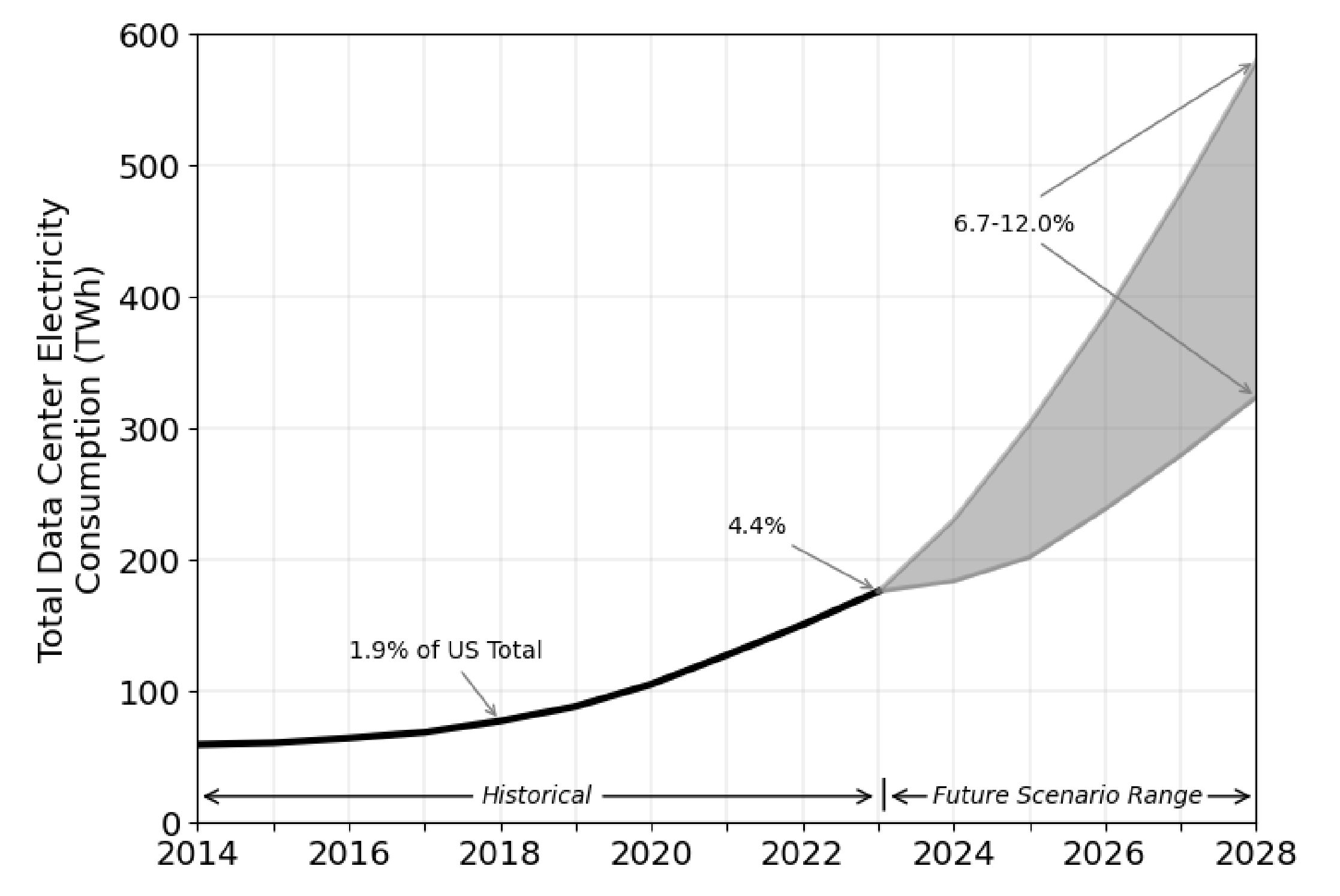

2. Rising demand from electrification and AIElectricity demand, previously growing modestly (~1% per year in the US), is now accelerating due to manufacturing onshoring, electrification and surging AI data centre usage. While estimates of demand growth are difficult to quantify, it is estimated that over the next five years the US will see load growth of at least 3%3, with further upside potential as data centre demand increases alongside demand for AI computing. Government reports project US data centre demand leaping from 176TwH in 2023 to 325-580TwH in 2028.4 This equates to between 6.7% and 12% of total US electricity consumption - up from 4% currently.5 Estimated data centre consumption growth

3. Hyperscaler investment'Hyperscalers' (large technology companies using data centres for cloud computing and data management services) are turning to nuclear energy due to its ability to provide 24/7 secure base load power for data centres while also aligning with their significant carbon reduction goals. The main drawback of nuclear power for hyperscalers is build time: with planning and construction times of over 10 years along (notwithstanding time and cost blowouts (as set out above). These long lead times conflict with hyperscalers' ambitions to deliver nascent high-profile AI technologies as soon as possible. As an alternative, hyperscalers have focused on leveraging existing nuclear capacity and exploring innovative reactor designs to mitigate cost and construction times. This is demonstrated through examples from key hyperscalers including:

4. Policy supportGovernment policy is increasingly supportive. The US Inflation Reduction Act (IRA) is the most prominent example, with the Act containing several tax credit provisions that serve to boost nuclear's financial viability. Examples include:

Nuclear's investment caseWe anticipate continued growth in nuclear demand, driven by AI-related consumption, supportive policies and decarbonisation mandates. Given the long lead times and high costs of new build, leveraging existing capacity remains the focus. Translating this to investment decisions4D supports the nuclear theme as part of the Energy Transition. However, for us to take exposure the underlying assets must meet our infrastructure definition by either being 'regulated' or 'contracted'. One or both of these arrangements serves to secure the investment and operating costs of the plant as well as the return to the shareholder. At 4D we have nuclear power generating exposures across multiple US utility investments, but most prominently through our investment in Dominion Energy (D). Dominion owns regulated nuclear facilities in Virginia and South Carolina, as well as the Millstone Nuclear Power Station in Connecticut, which the company is exploring contracting opportunities for. We also have exposure through European utilities including Iberdrola [IBE] who have some legacy nuclear exposure in Spain. We are also closely monitoring nuclear-exposed Independent Power Producers (IPPs) like Constellation Energy, Talen and Vistra. While these stocks appeal in different ways, they currently either lack the cash flow visibility we require in our investments or lack a compelling enough risk-reward proposition amid stretched valuations. Case Study: Millstone nuclear power plantOwned by Dominion Energy, the Millstone Nuclear Power Plant (Millstone) is based in Connecticut, US, and has an operating capacity of 2GW across units 2 and 3. The power station began operating in 1975 and has an operating license from the US Nuclear Regulatory Commission (NRC) until July 2037 and November 2045 for Units 2 and 3 respectively. The power station provides around 47% of Connecticut's power needs, more than 90% of the state's carbon-free power and employs around 4,000 people. Until March 2019, Millstone sold 100% of its capacity into the ISO New England merchant energy market in the northeast of the US. Prior to the Covid-19 recovery, benign growth in power demand from customers (around 1% annual demand growth for the previous decade), combined with cheaper forms of alternative energy generation (such as renewables and natural gas), meant the merchant price of power earned by Millstone was uneconomic compared to the running costs of the facility. The load-weighted average prices achieved in 2016, 2017 and 2018 were $34.62/MWh, $37.45/MWh and $52.27/MWh respectively. Dominion management lobbied Connecticut legislators and regulators, stressing they would have to decommission Millstone if the state didn't provide some form of financial support as low and volatile market prices meant the facility was loss making. In response, the Connecticut regulator, PURA, signed a fixed price agreement with Dominion for approximately half of Millstone's capacity, for a maturity of 11 years (to 2029). The price within the contract was $49.99/MWh, well above the prevailing market price achieved for the facility. This contract supported the financial viability of Millstone and incentivised Dominion to continue operating the facility. Fast forwarding to the current environment, the northeast US power market is now in short supply, driven by the aforementioned strong demand growth from data centres, onshoring of manufacturing and wider electrification efforts. This has resulted in much higher market prices with capacity contracts agreed with data centre companies at prices rumoured in excess of $100/MWh. The carbon-free, firm power capacity provided by nuclear facilities like Millstone are particularly sought after by tech companies. Dominion management are now considering options of what to do with the uncontracted capacity of the facility, and potential utilisation of capacity post expiry of the agreement with PURA in 2029. 1 https://energynews.pro/en/france-reaches-a-record-e5-billion-in-electricity-exports-in-2024/ The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. Funds operated by this manager: 4D Global Infrastructure Fund (Unhedged), 4D Global Infrastructure Fund (AUD Hedged) |

Source: US Energy Information Administration

Source: US Energy Information Administration Source: NEI, IAEA-PRIS 2

Source: NEI, IAEA-PRIS 2 Source: Berkeley Lab - 2024 United States Data Center - Energy Usage Report

Source: Berkeley Lab - 2024 United States Data Center - Energy Usage Report Source: U.S. Department of Energy

Source: U.S. Department of Energy

9 May 2025 - Are You In The Matrix?

|

Are You In The Matrix? Marcus Today April 2025 |

|

Have you been told to "buy and hold"? "It'll be fine in the long run"? "You can't time the market"? You might be in the matrix. In this video, Marcus breaks down the truth behind the mantras the finance industry repeats - not to help you, but to keep you quiet. If you've ever felt like the advice doesn't quite match reality... you're not alone. DISCLAIMER: This content is for general information purposes only and does not constitute personal financial advice. Please consider your own circumstances or seek professional advice before making investment decisions. |

|

Funds operated by this manager: |

7 May 2025 - Sustainability: Is this the end for sustainable investing?

|

Sustainability: Is this the end for sustainable investing? abrdn April 2025 This is a crucial year for sustainable investing. With a heady mix of regulatory change, political backlash and changing sentiment, we ask whether it's over for sustainable investment? Investors who have set interim climate targets for 2030 have less than five years to achieve them. But even with an increase in the regularity and severity of extreme weather events, many investors have faced a political backlash against climate change and sustainable investing. These developments have accelerated in recent months with a drastic shift in the US political climate. This has led to big-name US asset managers and companies abandoning climate commitments and rushing to roll back on diversity, equity and inclusion (DEI) pledges. But behind the headlines, we see a more nuanced evolution of the sustainable investing world - one in which demand for sustainability strategies remains strong. This is being driven by institutional investors demanding bespoke solutions to meet specific goals and these asset owners are backing up their talk with action. Transatlantic splitThe US and Europe are heading in opposite directions. Political pressures have led to a retreat from sustainable investment in the US, while Europe largely remains committed. President Donald Trump plans to dismantle the previous US administration's measures to promote sustainability and wants to increase coal, oil and gas exploration on federal land - his recent executive orders demonstrating his intent. He has weakened the Environmental Protection Agency and pulled the US out of the Paris climate agreement. Some US asset managers, facing legal challenges, have turned their backs on climate targets and withdrawn from international climate initiatives, such as the Net Zero Asset Managers and the Climate Action 100+ initiatives. But across the Atlantic, it's almost business as usual for a region that has long been at the vanguard of international efforts to promote sustainability and sustainable investing. Last December, regulators there started applying the European Union's (EU) Green Bonds regulation. These rules aim to clarify eligibility criteria on what qualifies in the EU as a 'green bond'. The goal is to improve investor protection by preventing 'greenwashing'. It's not all plain sailing even in the EU. In a bid to boost competitiveness, Europe's Omnibus package rolls back flagship sustainable investment policies including the Corporate Sustainability Reporting Directive and the Corporate Sustainability Due Diligence Directive, amid proposals to dilute the region's Sustainable Finance Disclosure Regulation. This divergence in philosophy amid pressures to weaken existing measures complicate global operations for asset managers and asset owners alike. It is simply no longer possible to operate with a one-size-fits-all approach. Big investors lead the wayThat said, many institutional investors continue to demand sustainable investing strategies. This isn't always obvious, but it is a critical component of the current investment landscape. In February, a group of 27 asset owners - primarily from the UK but also representing European, Australian and US investors - signed the 'Asset Owner Statement on Climate Stewardship' to reinforce their support for sustainability principles and to spell out what they expect from fund managers. There is growing demand for tailored investment solutions. While these are predominantly focused on asset owners looking to meet their climate targets, there is also interest in deploying strategies to protect natural environments in bespoke, or 'segregated', mandates. In our own assets under management, those we classify as 'sustainable' investments, grew to £87 billion (US$112.4 billion) by end-2024 from £55 billion a year earlier. This increase was largely attributable to segregated sustainable investment mandates. We are also seeing cases in which asset managers who turn away from sustainability goals may be punished by some asset owners. For example, both the UK's People's Pension and Denmark's Akademiker Pension pulled mandates from one US fund manager amid disagreements over climate stewardship. DEI requires diverse solutionsCompanies employ DEI policies for reasons including employee wellbeing, legal compliance and enhancing brand image. But critics equate DEI with the prioritisation of identity over competence. Many US companies have been diluting or scrapping their DEI policies in response to Trump's executive order on DEI and to avoid litigation. DEI-related quotas and affirmative-action programs have been under particular scrutiny. Opponents say they are discriminatory and that employees hired through these initiatives have not been chosen on merit. Some firms have removed gender quotas on boards, for example. The response from asset managers has been mixed amid a growing number of DEI cases going to court. While some have gone quiet on DEI, other fund managers continue to engage with companies and deepen long-term relationships to drive improvements in this area. The changes companies are making with regards to DEI, as a result of navigating new pressures and expectations, is yet another facet of the evolving nature of sustainability investing in a complex world. Final thoughtsMany recent headlines have painted a grim picture for sustainable investing, with phrases like 'sustainability in crisis' making the rounds. There's no doubt that the honeymoon for sustainable investing is over. However, a closer look reveals a more nuanced story. A hostile political environment in the US makes it more difficult to follow sustainable investment principles there. However, the demand for sustainability strategies remains strong, especially from institutional investors who remain committed to achieving sustainability targets and need customised investment solutions. Once the marketing hype is stripped away, sustainable investing has always been fundamentally about financially-material issues. These issues continue to be critical regardless of the political whims of the day. This is why asset owners, as long-term investors, remain committed. This is why there are opportunities for those investors who can navigate this complex landscape. Sustainable investment is not dead - it is reforming and evolving to meet the demands of a changing world. It took over 100 years to secure agreement on globally-accepted accounting principles. We are trying to achieve the same thing with less time and as the world gets hotter each year. Is it any wonder there are a few bumps along the road? |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund, abrdn Emerging Opportunities Fund, abrdn Global Corporate Bond Fund (Class A), abrdn International Equity Fund, abrdn Multi-Asset Income Fund, abrdn Multi-Asset Real Return Fund, abrdn Sustainable International Equities Fund |

7 May 2025 - Tim Hext: Art of the deal or new world order?

|

Tim Hext: Art of the deal or new world order? Pendal April 2025 |

|

PRESIDENT TRUMP's "reciprocal" tariffs caught many - me included - by surprise last week. Until then, I mistakenly believed tariffs were all part of the art of the deal. Tariff talk, which was seen as a tactical ploy to get a better deal for the US, suddenly seemed to have larger ideological aims. How else can you explain the ridiculous calculation method for reciprocal tariffs? There is still a lot of water to go under the bridge in the weeks and months ahead as negotiations go bilateral - but understanding Trump (always a difficult exercise) will help navigate markets. When China entered the World Trade Organisation in 2001, the US trade deficit with China was $84 billion. The US had a $300 billion deficit overall in manufacturing. Over next two decades, the manufacturing deficit grew $1 trillion to $1.3 trillion by 2022. China accounted for almost $600 billion of this growth. Overall, this was seen as a win/win. China got to develop on the back of hard work and exporting to the US. And US consumers got plenty of cheap goods from China, protecting a standard of living in the face of slow wage growth. The bonus for the US was that in an attempt to keep its currency lower, the Chinese government bought US dollars and became huge buyers of US Treasuries. Its FX reserves went from $300 billion to over $3 trillion during this period. Let's not forget the most important thing: since 2000, around 500 million Chinese people have emerged from poverty to middle incomes. By 2018, however, geopolitics started to kick in. As China started to flex its muscle globally, not all in the US were happy. The narrative began to change. In his first term, Trump launched a trade war with China, causing negative equity returns. Helping the Chinese economy was now seen as a negative, not a positive. That trade war now seems tame. It seems the narrative from Trump is effectively that the US can handle some pain if it means achieving a longer-term new world order. The US will retreat back to some supposed golden age. Time will tell. Implications for bond marketsAs evidenced this week, all these actions from Trump are a mixed bag for US bonds. Firstly, economic weakness should mean Fed cuts and rallies in bonds. However, tariffs will mean higher inflation - at least near term. Throwing more confusion into the picture is foreign buying (or more likely selling) of US bonds. Smaller trade deficits mean smaller capital surpluses and therefore, at best, smaller inflows into US capital markets. Where it gets more interesting, though, is the weaponisation of financial flows - not just trade flows. Rumours have been circling that China is dumping part of its US Treasury holdings. Other countries may follow - after all, like any investments, you want to know the CEO knows what they are doing, and simply put, credibility and confidence has evaporated. Who would want to lend money to an entity that is acting so aggressively against your interests? Therefore, the flight to quality is more of a flight to cash and short bonds, not long bonds. Yield curves are steepening faster than economic fundamentals suggest. It was only late last year when US exceptionalism became the investment theme for this decade. That exceptionalism remains but is quickly being redefined from a positive to a negative. Implications for our portfoliosWe have been leaning into duration for a number of months, but are very disappointed by the lack of a reaction from our long end. Short-end duration has worked, but unlike Covid and the GFC, the long end has been left behind. The RBA will also be cautious. The expected low CPI print on 30 April will give the central bank cover to cut at its 20 May meeting, but unless it keeps getting worse, its recent form suggests only a 25-basis-point (bps) cut. It will then adopt a wait-and-see approach for how it all impacts Australia. But given there are six weeks till then, markets are right to price some risk of a larger cut - though, current levels of 40bps of cuts looks a little too much. The random nature of announcements mean we are generally keeping risk close to home. Our caution around credit means we are avoiding the major drawdowns that will be hitting more aggressive investors. Now is not the time to charge in. However, we are still looking for relative value opportunities in a volatile market to keep adding value in these stressed times. LiquidityAnd just like that - liquidity in many sectors dries up in a puff of smoke. Our portfolios at Pendal Income and Fixed Interest have always operated at the more liquid end of markets. We leave the less-liquid, high-yield chasing to others. Government bonds remain highly liquid. Semi-government bonds are hanging in there though bid/offers are widening. You can transact senior bank paper assuming manageable size and paying a wider spread. However, as we have often warned, beyond there it gets very tricky. Everything is liquid in good times, but it is a shortlist in a time of crisis. The RBA sets the liquidity rules and its world is one of cash, bank bills/NCDs and government bonds (all known as High Quality Liquid Assets). These remain open for business, but beyond that point, it is buyer-beware for liquidity. Author: Tim Hext |

|

Funds operated by this manager: Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Multi-Asset Target Return Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Pendal Sustainable Australian Share Fund, Regnan Credit Impact Trust Fund, Regnan Global Equity Impact Solutions Fund - Class R |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

6 May 2025 - Glenmore Asset Management - Market Commentary

|

Market Commentary - March Glenmore Asset Management April 2025 Globally, equity markets fell sharply in March. In the US, the S&P 500 fell -5.8%, the Nasdaq declined -8.2%, whilst in the UK, the FTSE outperformed, falling just -2.6%. Relevant for the Glenmore Australian equities fund was the ASX small industrials accumulation index, which fell -6.7% in March. Gold stocks were the strongest performer on the ASX, boosted by a +10.6% increase in the gold price. Defensive sectors such as utilities, telco's and insurance also outperformed. Growth stocks (in particular technology stocks) fell sharply, due to investors adopting a "risk off" approach as well as growing concern about the rate of global economic growth. The catalyst for the negative returns in March was continued discussion around the US government introducing tariffs on various trading partners. The proposed tariffs and general uncertainty around US president Donald Trump's policy making resulted in investors becoming very cautious towards global economic growth and equities across all sectors. In addition, the tariffs imposed by the US have the potential to be inflationary in the short term, which could pose a new risk for investors. Bond markets were quite subdued during the month despite the equity markets volatility. In the US, the 10-year bond yield fell -3 basis points (bp) to 4.21%, whilst its Australian counterpart rose 9 bp to close at 4.39%. The Australian dollar was broadly unchanged over the month, closing at US$0.62. Our view is that the recent sell off over the last two months will likely prove to a good buying opportunity for investors willing to a take a medium-term view. As is typically the case in these market corrections, growth stocks and small/mid cap stocks were sold off very significantly, whilst large caps stocks outperformed given their safe haven status. The fund currently has a cash weighting of ~15%. As we have done in past periods, we have used this period of weakness to add to a number of stocks in the fund at attractive valuations. In addition, if global economic growth does slow materially over the course of 2025, we believe central banks will consider interest rate reductions, which would likely to be positively received by investment markets. Funds operated by this manager: |

5 May 2025 - 10k Words | April 2025

|

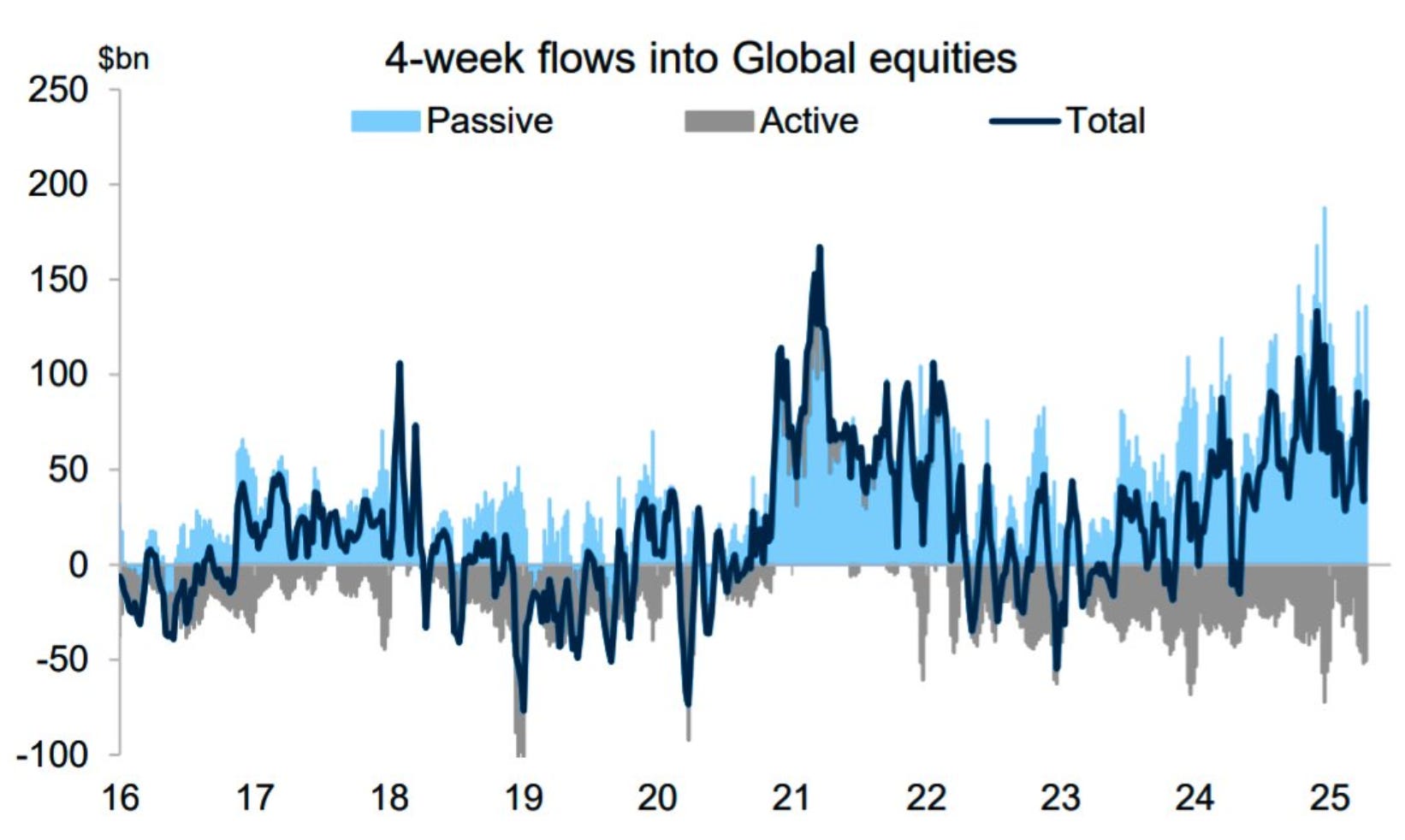

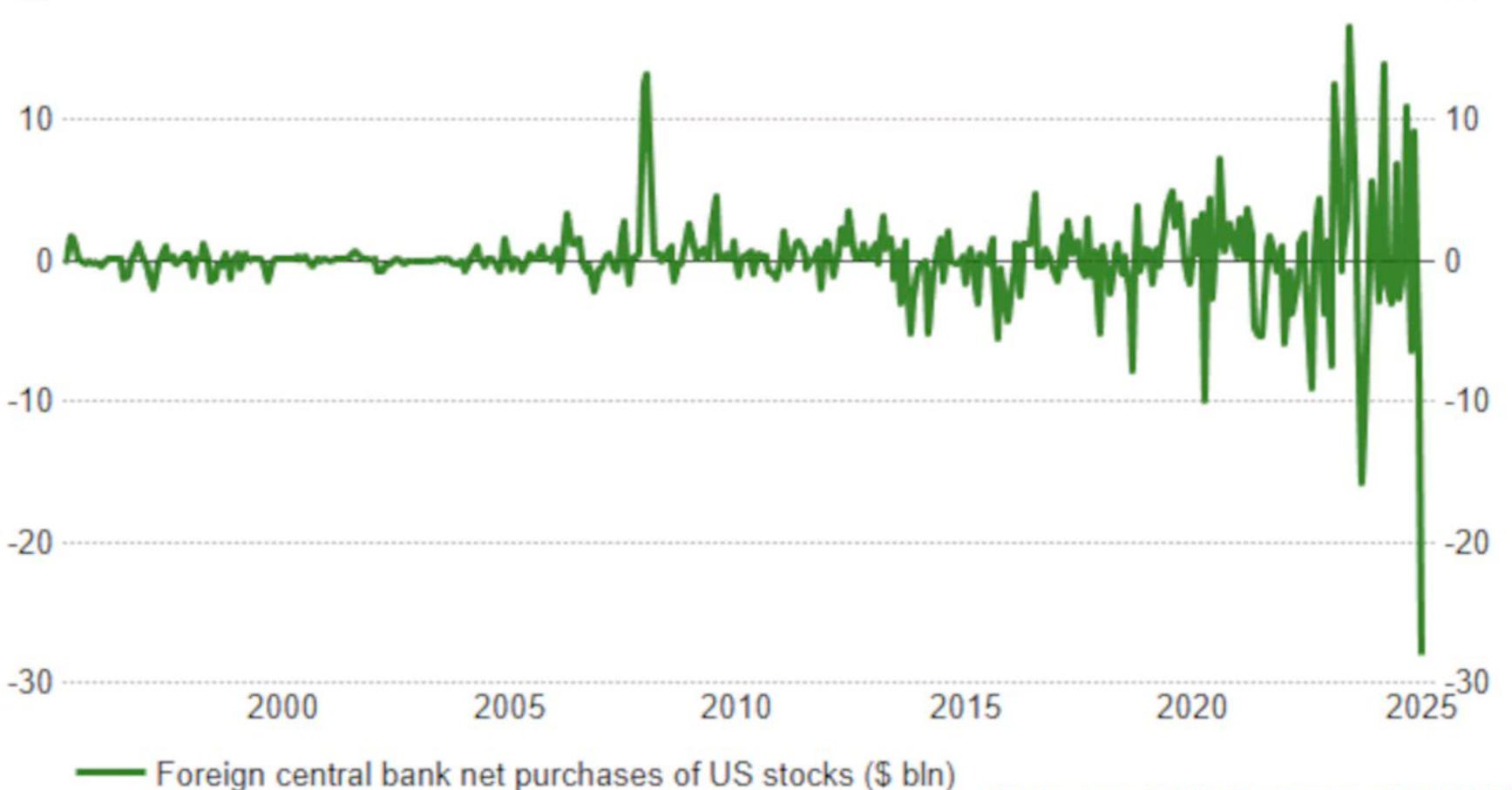

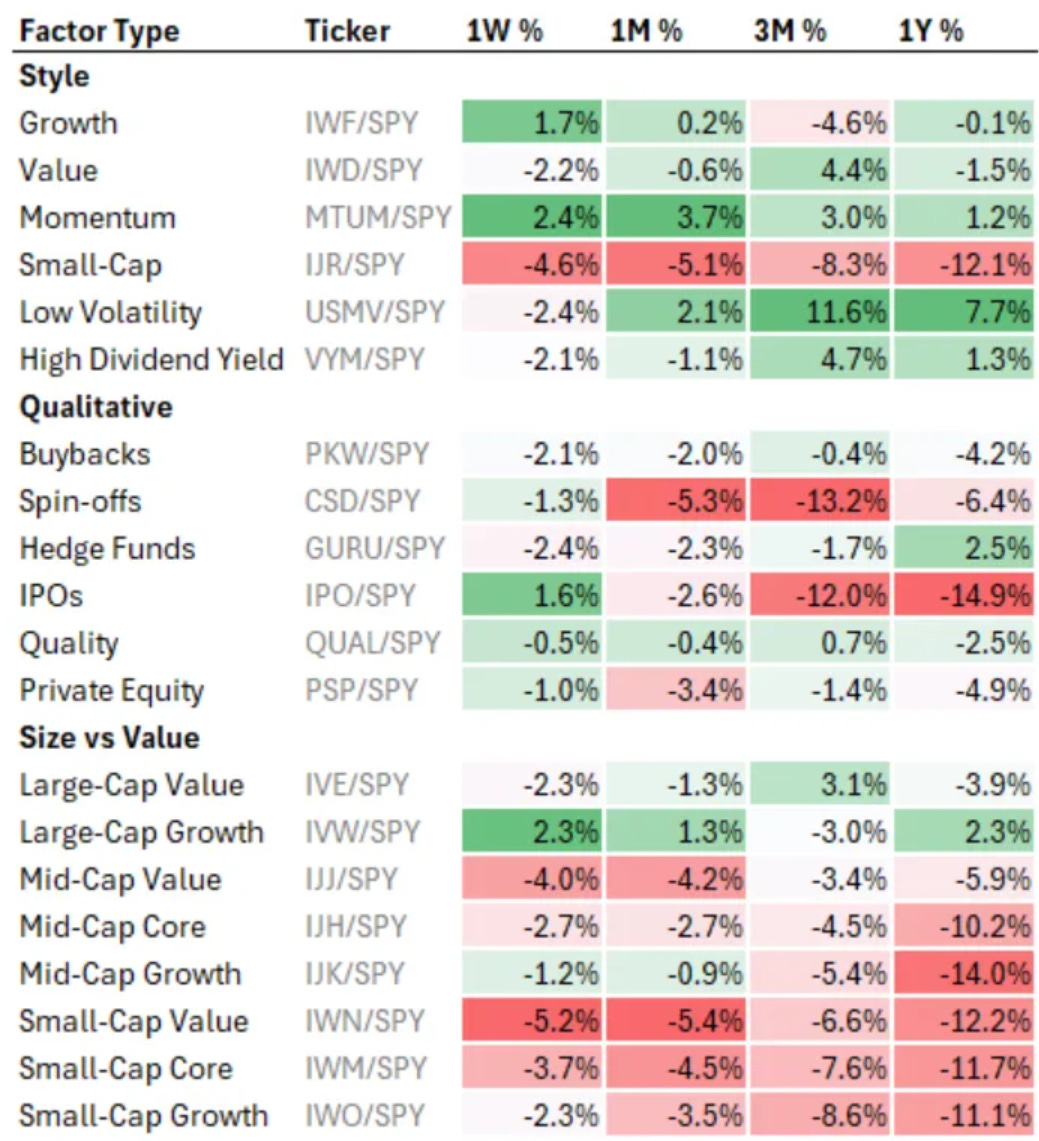

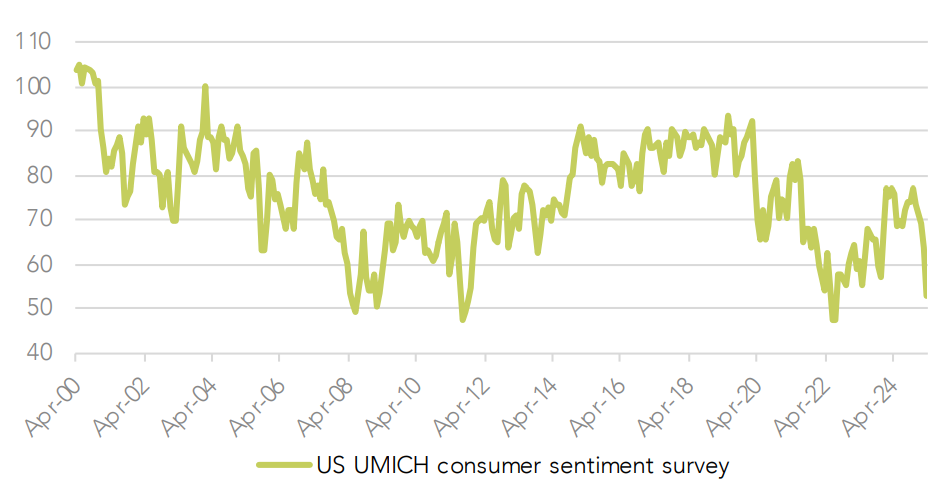

10k Words Equitable Investors April 2025 Apparently, Confucius did not say "One Picture is Worth Ten Thousand Words" after all. It was an advertisement in a 1920s trade journal for the use of images in ads on the sides of streetcars... Passive investment in global equities appears to have continued on while active flows remain negative and foreign demand for US stocks reverses sharply. But in the US, momentum was the winning factor in the past volatile week and month, a factor small caps have been lacking, with small cap earnings growth over the past decade generally not accompanied by multiple expansion. Credit spreads have been on the rise and the correlation between credit spreads and the valuation of equities has also been increasing. The post-tarrif volatility has cut back the forward PE on the ASX sharply BUT it is worth bearing in mind that the ASX's largest companies were established in a more distant era than the dominant companies in the US, where multiples are higher. On the US - inflation was retreating nicely prior to the tarrifs but consumer confidence is at GFC levels. Finally, we divert to look at online penetration of lottery sales around the world. Flows into global equities

Source: Goldman Sachs Foreign official demand for US stocks

Source: Reuters, Charles Schwab US equity market factor performance as of end of last week (ETF factor proxies)

Source: Koyfin, Equitable Investors Strong earnings growth for small caps but their returns lagged as their valuation multiples remained more or less the same (2015-2024)

Source: Robeco ICE BofA US High Yield Index Option-Adjusted Spread

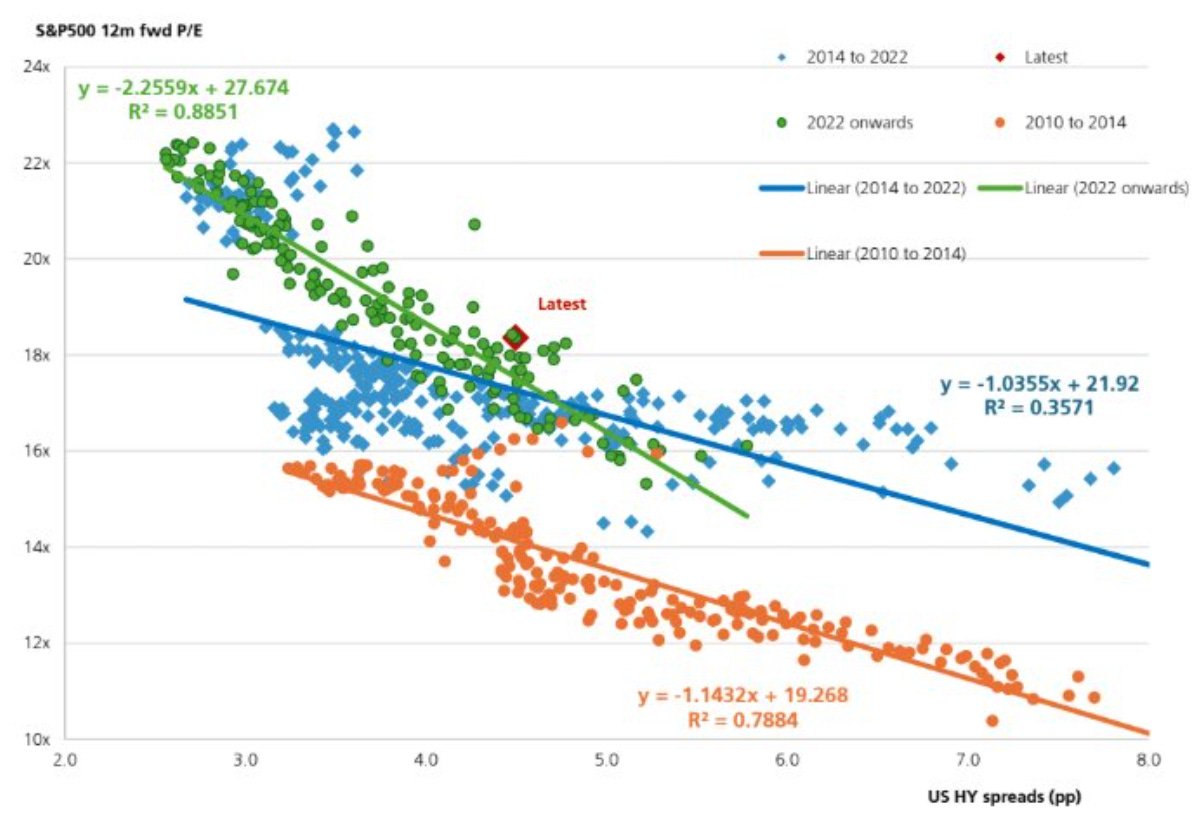

Source: FRED Relationship between the S&P 500 forward PE multiple & credit spreads

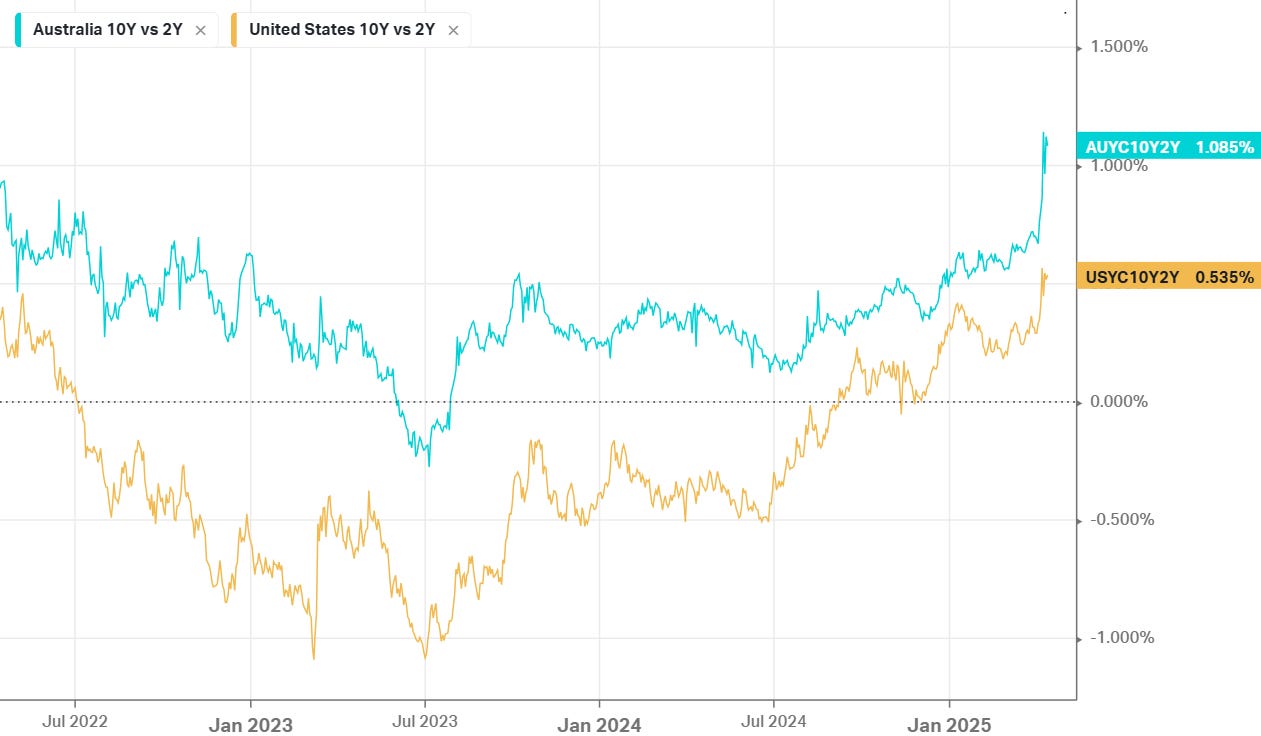

Source: UBS US & Australian government bond yield spreads (10 year v 2 year)

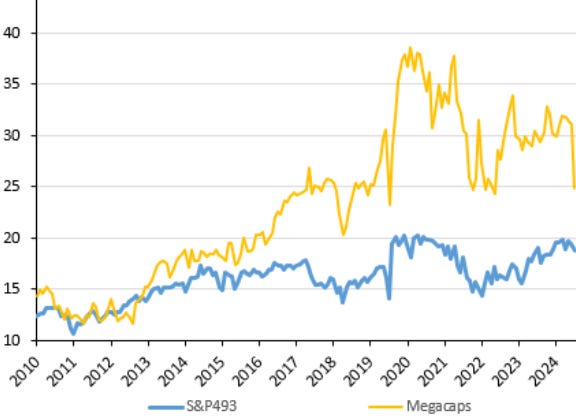

Source: Koyfin ASX forward PE multiple

Source: Evans & Partners Australia's largest companies from a different era to the US

Source: Owen Analytics Forward PE on US equities

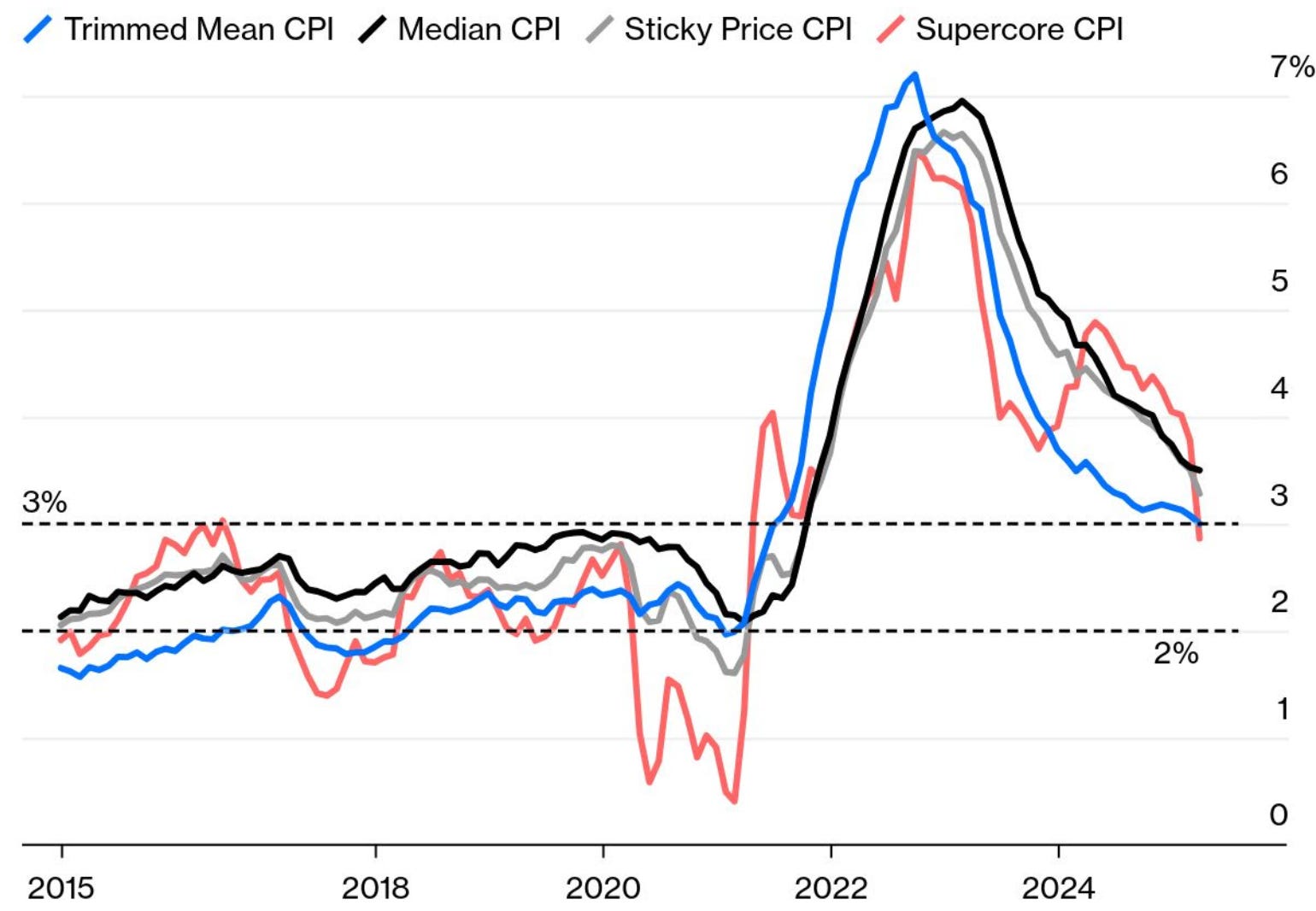

Source: Evans & Partners US core inflation had been falling sharply

Source: Bloomberg US consumer confidence drops to GFC levels

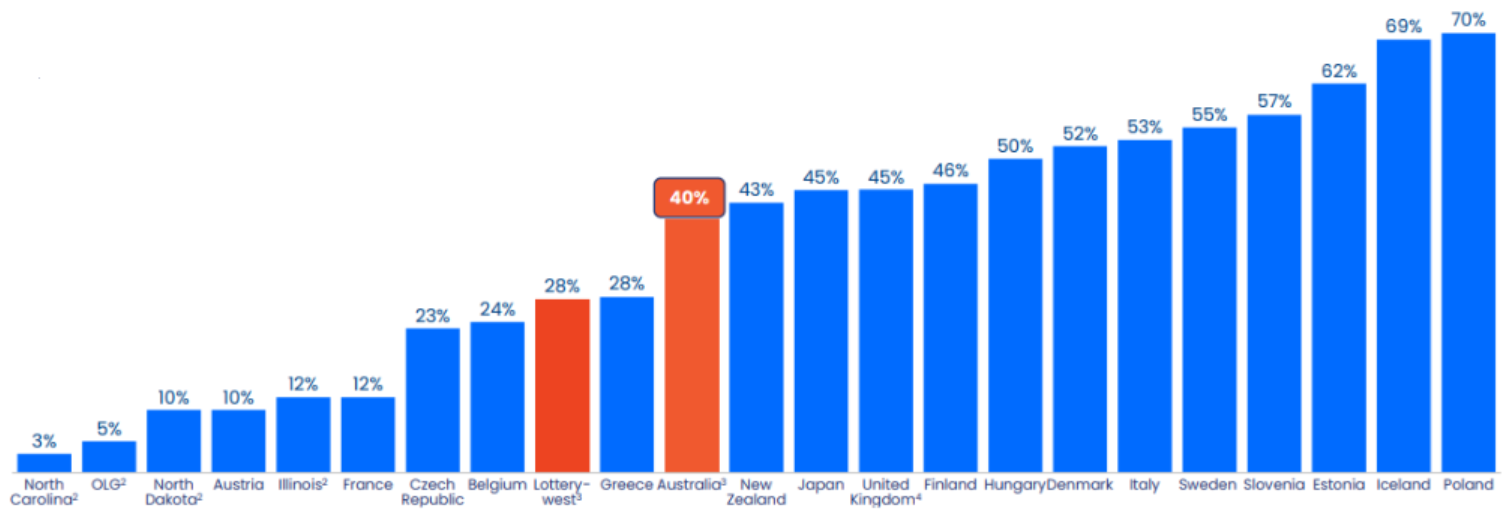

Source: Wilsons Advisory Online penetration of lottery sales Source: Jumbo Interactive (ASX code: JIN) April 2025 Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |