News

10 Dec 2025 - Performance Report: Airlie Australian Share Fund

[Current Manager Report if available]

10 Dec 2025 - Infrastructure in focus: The industrial heartland

|

Infrastructure in focus: The industrial heartland Magellan Asset Management November 2025 (7-minute read) |

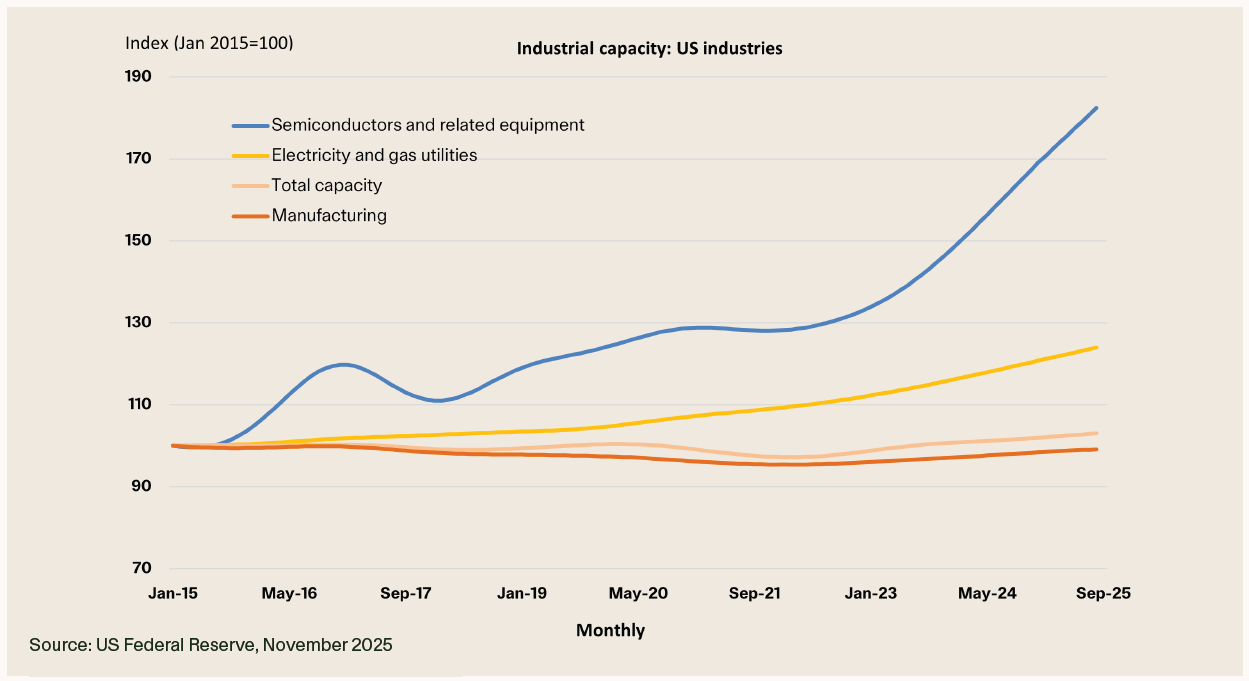

Looking at a country's industrial base can tell a lot about the makeup of its activities and its infrastructure needs. The chart below shows US industrial capacity, from 2015 to now. Several things stand out:

With the expansion in electricity and gas utility capacity outpacing total industrial capacity while growth in semiconductor production capacity is on a tear, what we see here is the real-world story of the AI boom. Exuberance on AI has been the predominant theme for markets this year, and the chart below shows a structural shift in economic activity underway.

Highlights

By Magellan Global Listed Infrastructure Investment Team |

|

Funds operated by this manager: Magellan Global Fund (Open Class Units) ASX:MGOC , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Global Fund (Hedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT) Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Magellan Investment Partners ('Magellan Investment Partners') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan Investment Partners financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan Investment Partners financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan Investment Partners or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan Investment Partners will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third-party trademarks contained herein are the property of their respective owners and Magellan Investment Partners claims no ownership in, nor any affiliation with, such trademarks. Any third-party trademarks contained herein are the property of their respective owners, are used for information purposes and only to identify the company names or brands of their respective owners, and no affiliation, sponsorship or endorsement should be inferred from such use. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan Investment Partners. (080825-#W17) |

9 Dec 2025 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

9 Dec 2025 - Performance Report: 4D Global Infrastructure Fund (Unhedged)

[Current Manager Report if available]

9 Dec 2025 - News and Views: The impact of a steeper yield curve on global listed infrastructure

|

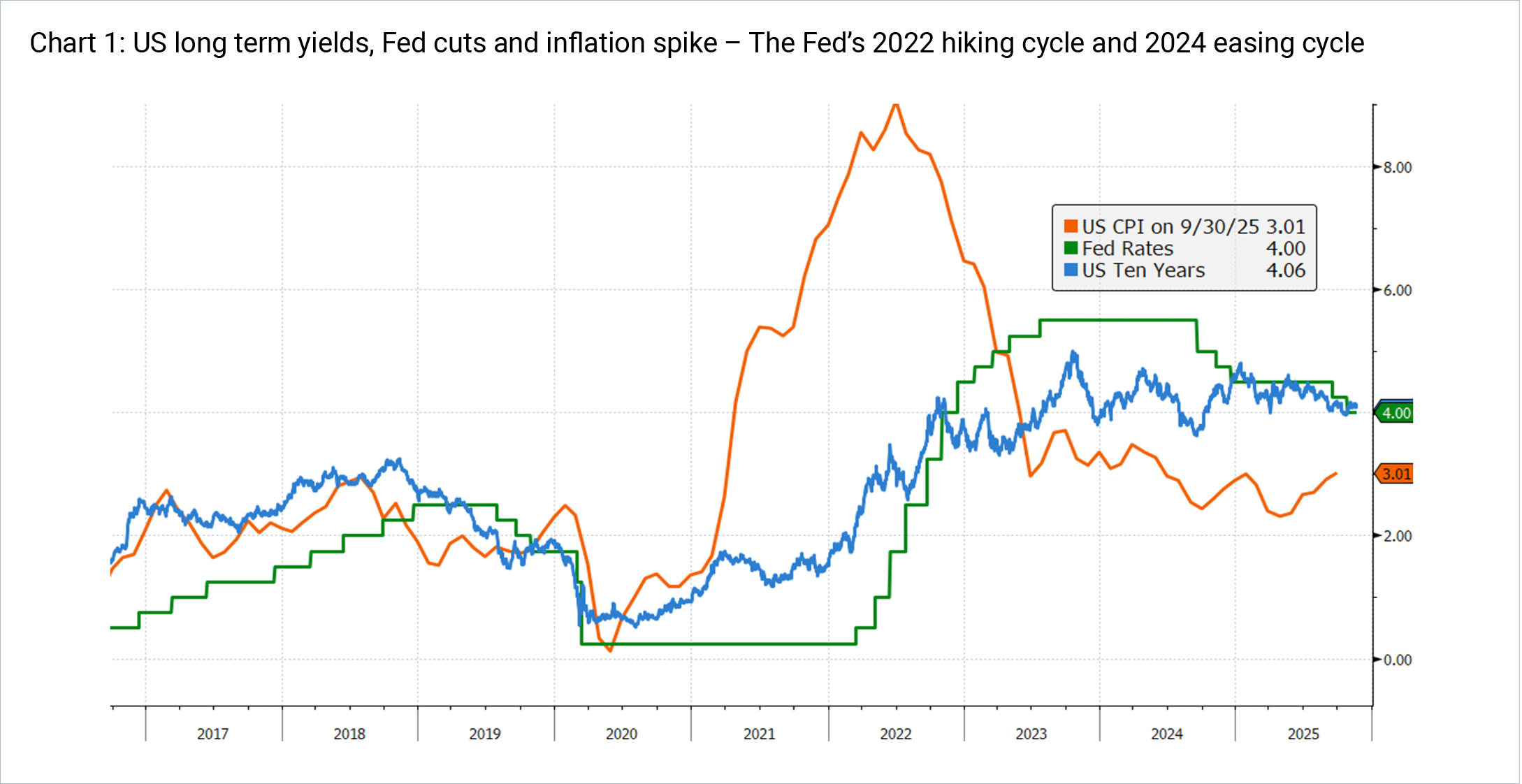

News and Views: The impact of a steeper yield curve on global listed infrastructure 4D Infrastructure December 2025 15-minute read Utilities and infrastructure valuations, typically sensitive to long-term yields, have been challenged by an exceptional rise in US bond yields despite significant Fed rate cuts, prompting an examination of the drivers, sustainability, and implications of this move for global listed infrastructure sectors. Utilities and infrastructure companies own very long dated assets characterised by high up front capital costs and returns often correlated to economic parameters. As such their valuations can be sensitive to changes in long term bond yields, some sectors more than others. The sharp inflation spike of 2021-22 led the US Fed to raise rates at a record pace, from 0.25% to 5.5% over 18 months, representing a headwind for certain segments of the infrastructure universe, particularly US utilities (no explicit inflation or interest rate pass through). Positively, this Fed action reigned in inflation and market expectations turned to Fed cuts. The subsequent easing cycle, commencing in September 2024, was expected to be a tailwind for infrastructure and in particular for utilities that have strong fundamental linkages to interest rates. While Fed interest rate cuts of at least 25bps generally coincide with a decline in long term bond yields this easing cycle has proved to be an anomaly: the Fed has cut by a cumulative 150bps and US ten-year yields have risen by ~50bps. In this News & Views we investigate what has driven this increase, if it can be sustained and the outlook from here. Finally, we then assess the impact this has on global listed infrastructure (GLI) valuations and how 4D manages these risks and opportunities. Bond yields - short & long term, components & moves after Fed cutsShort term yields are mainly driven by central bank policy rates and near-term inflation and growth expectations. By contrast, long term yields reflect expected future short-term rates as well as longer-run views on inflation, growth and a 'term premium' for compensating investors for the risk of holding longer dated bonds. Specifically, recent studies on the parameters affecting bond yields across maturities point to two key components:

As an infrastructure investor, the level and direction of long term yields are more important to us than short term moves as they have the largest impact on valuations, portfolio construction and risk management. As mentioned above, the inflation spike from very loose COVID monetary and fiscal policies led to a very steep Fed rate hiking cycle in 2022. The subsequent fall in inflation from above 9% to towards the Fed's 3% target led to the shifting of market expectations to an easing cycle.

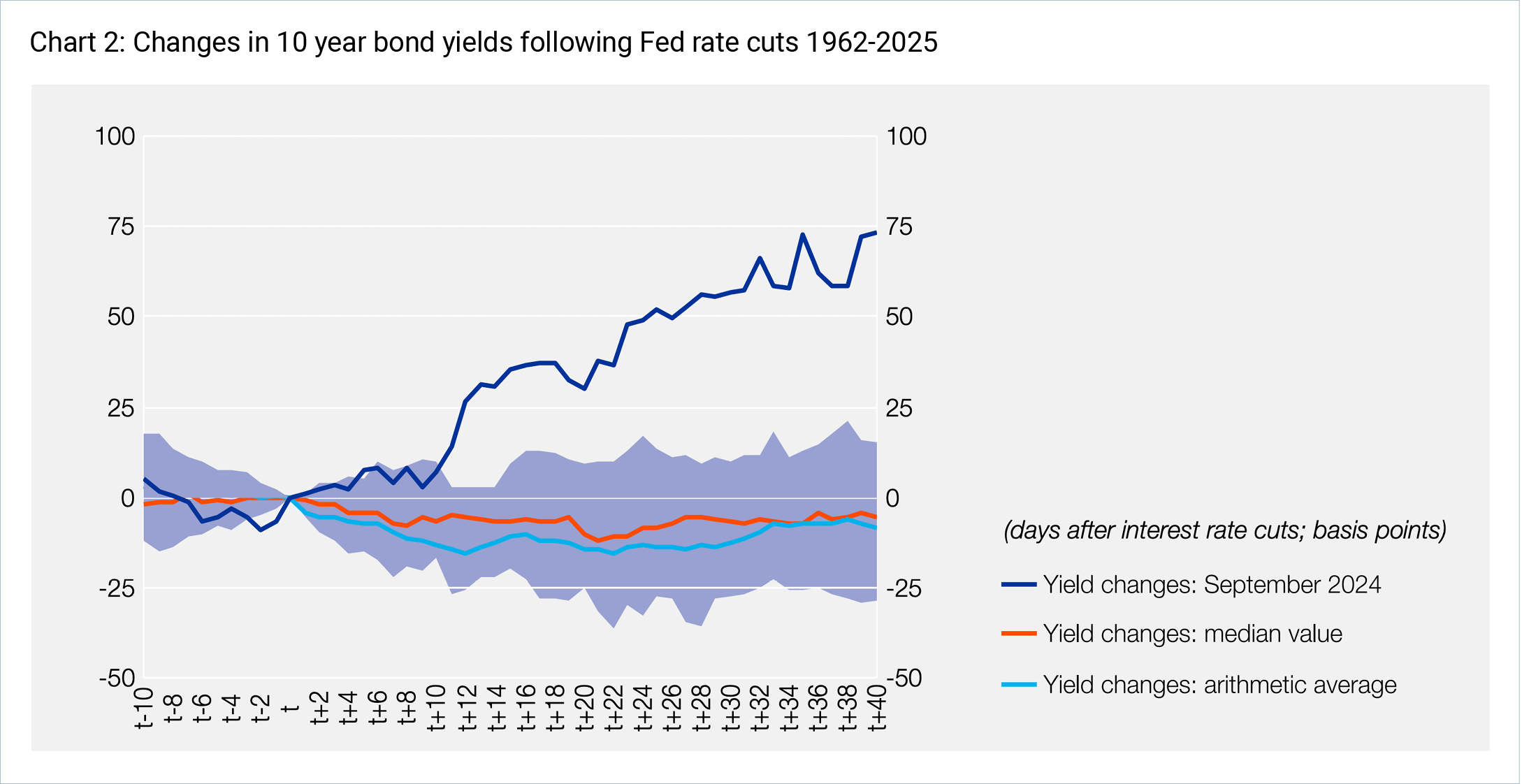

According to central bank research, since the 1960s Fed cuts of at least 25bps are followed by an average decline in long term bond yields of 10-16bps over the following calendar month, before stabilising at the lower level.2 This can be seen in the lower blue and red lines in Chart 2 below.

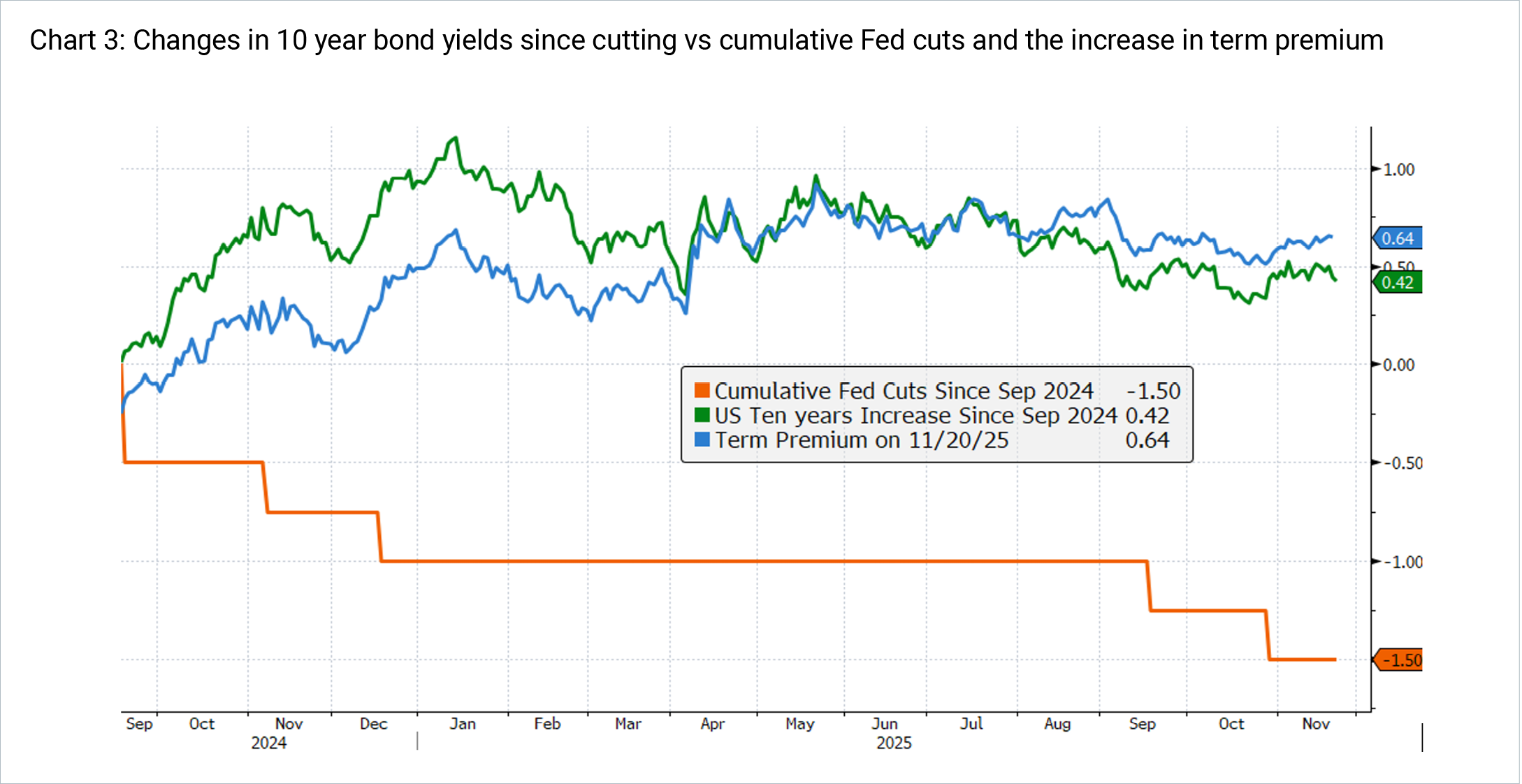

The market movements since the Fed started cutting in September 2024 have been very different to the historical price action seen above. As can be seen in Chart 3, as at November 2025 the Fed has cut 150bps while 10 year yields have increased 42bps. This move is rare - with this level of increase in the upper 10% of historical observations in the chart above, where the dark purple shaded area is the 25%-75% range of observations in the distribution.

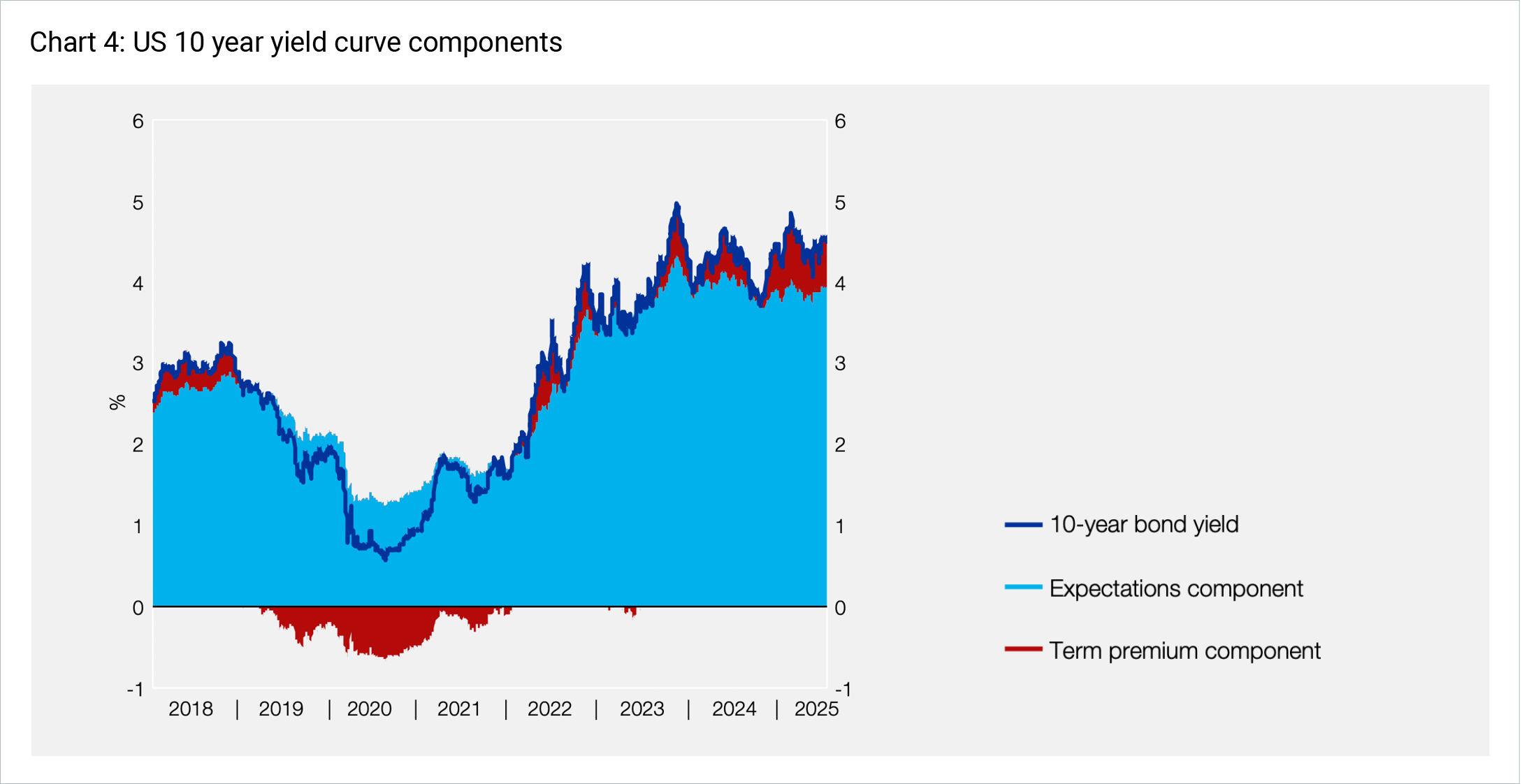

In order to investigate the reasons for the long bond yield increase, we can split up the components of the yield into its expectations component and term premium (explained above). We can see that over this recent period, the expectations component was largely stable (the light blue in Chart 4).

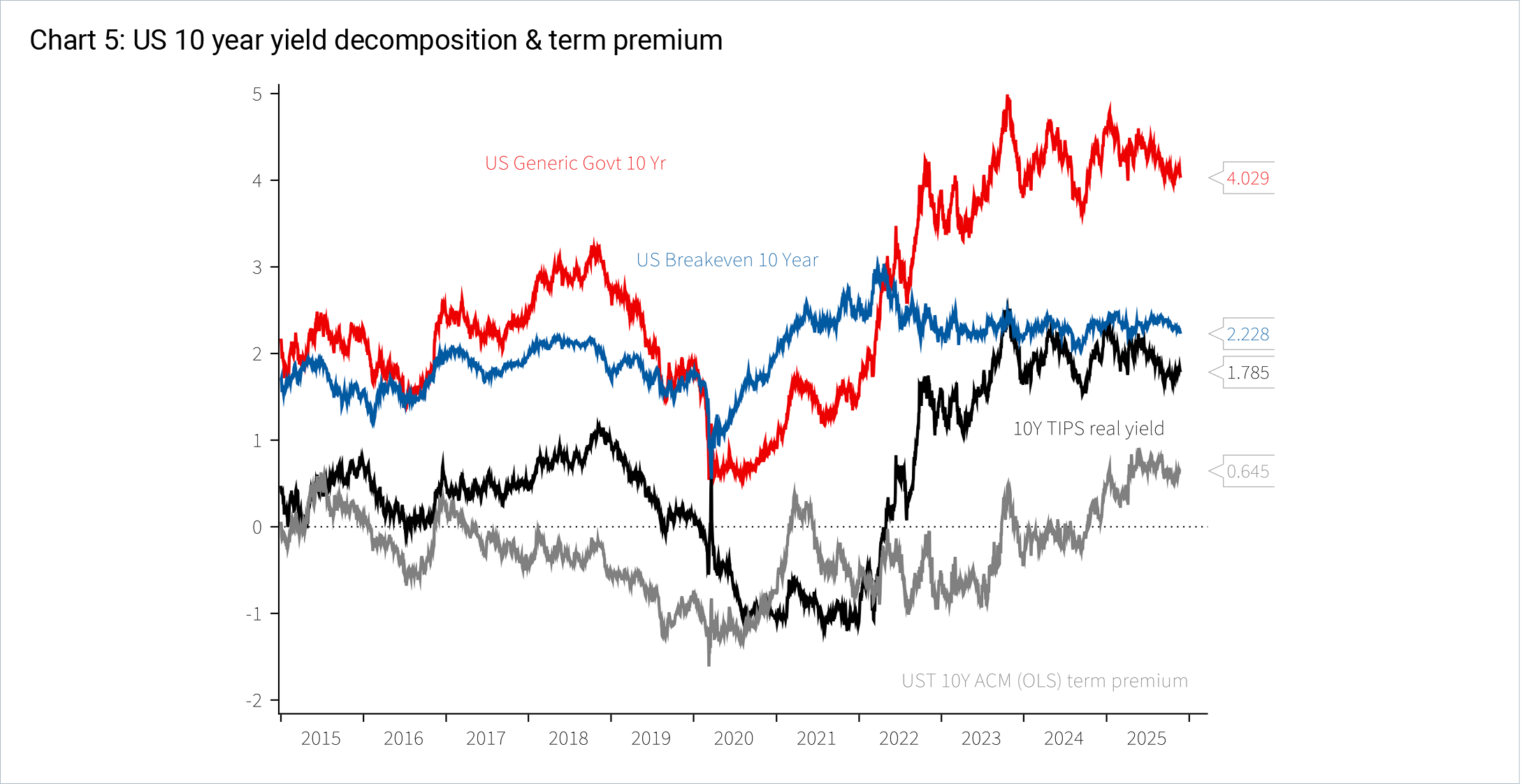

Furthermore, as can be seen in Chart 5, inflation expectations have stayed broadly stable too, indicated by the US breakeven below in blue.

This implies that an increase in term premium has caused a steepening of the yield curve, despite short rates dropping since September 2024. The term premiumOver 2025 there has been a lot of debate among central bankers, academics and market participants, as to the cause of the increase in term premiums by 50-100bps since the Fed's easing cycle began in 2024. Arguments include:

Other reasons for a steepening in the curve:

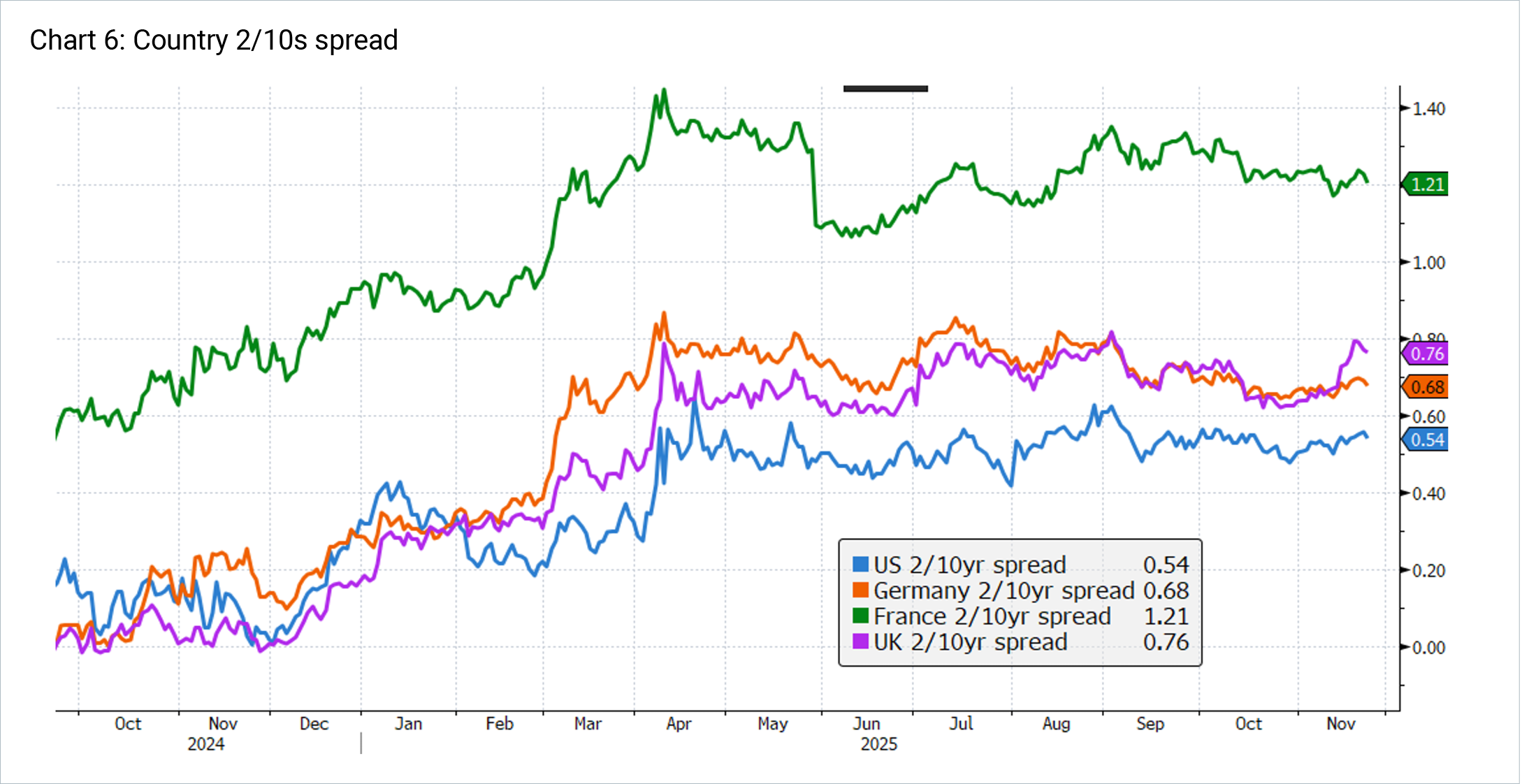

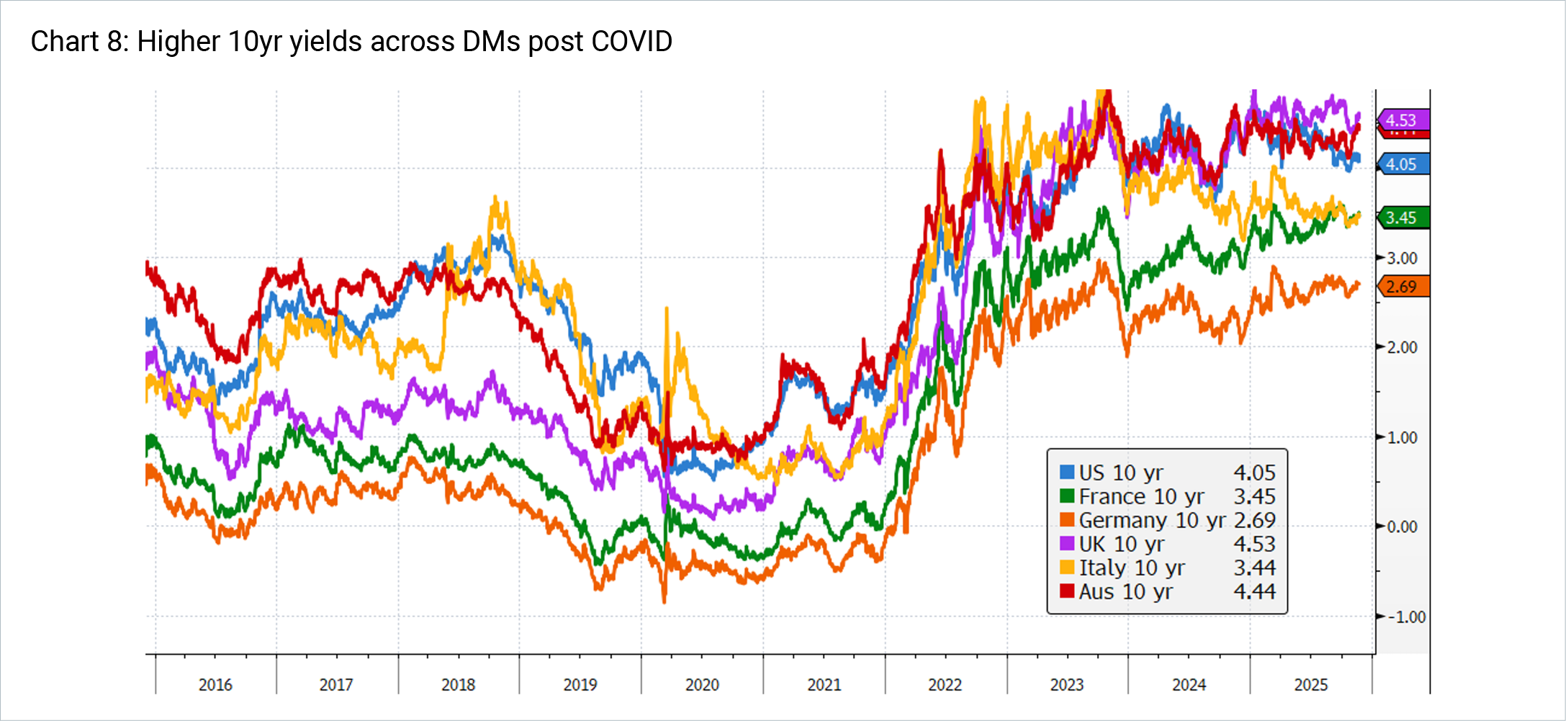

US Fed Governor Michelle Bowman summed up another risk of higher yields brought on by higher term premiums in a speech on 26 September 2025: Term premiums...A second challenge for monetary policy would be a significant rise in longer-term interest rates driven by higher term premiums, which could offset a reduction in the expectations component stemming from monetary policy easing. This scenario would weaken the transmission of changes in the policy rate to economic activity, as investment decisions of households and businesses are dependent on longer-term rates, such as mortgage rates and corporate bond yields.5 While the term premium has risen sharply, and many are looking for reasons why, it is worth noting that it remains below levels that persisted prior to the GFC. As JP Morgan note, "while this is a big move, it is not unexpected: term premium has retraced closer to average levels observed in the decade prior to the GFC, and does not seem to be unduly high in our opinion right now. Moreover, the demand for longer duration assets seems to be receding globally now as well". Transmission mechanism to the rest of the worldThe steeper yield curve has not been isolated to the US. As seen below, German, French and UK yields have also been steepening over the last 18 months - evidenced by the spread between the 2 and 10 year yields. Part of this has been the linkages in sovereign debt markets with the US, while other drivers are country specific. These all include common traits of worsening debt metrics and political impasse:

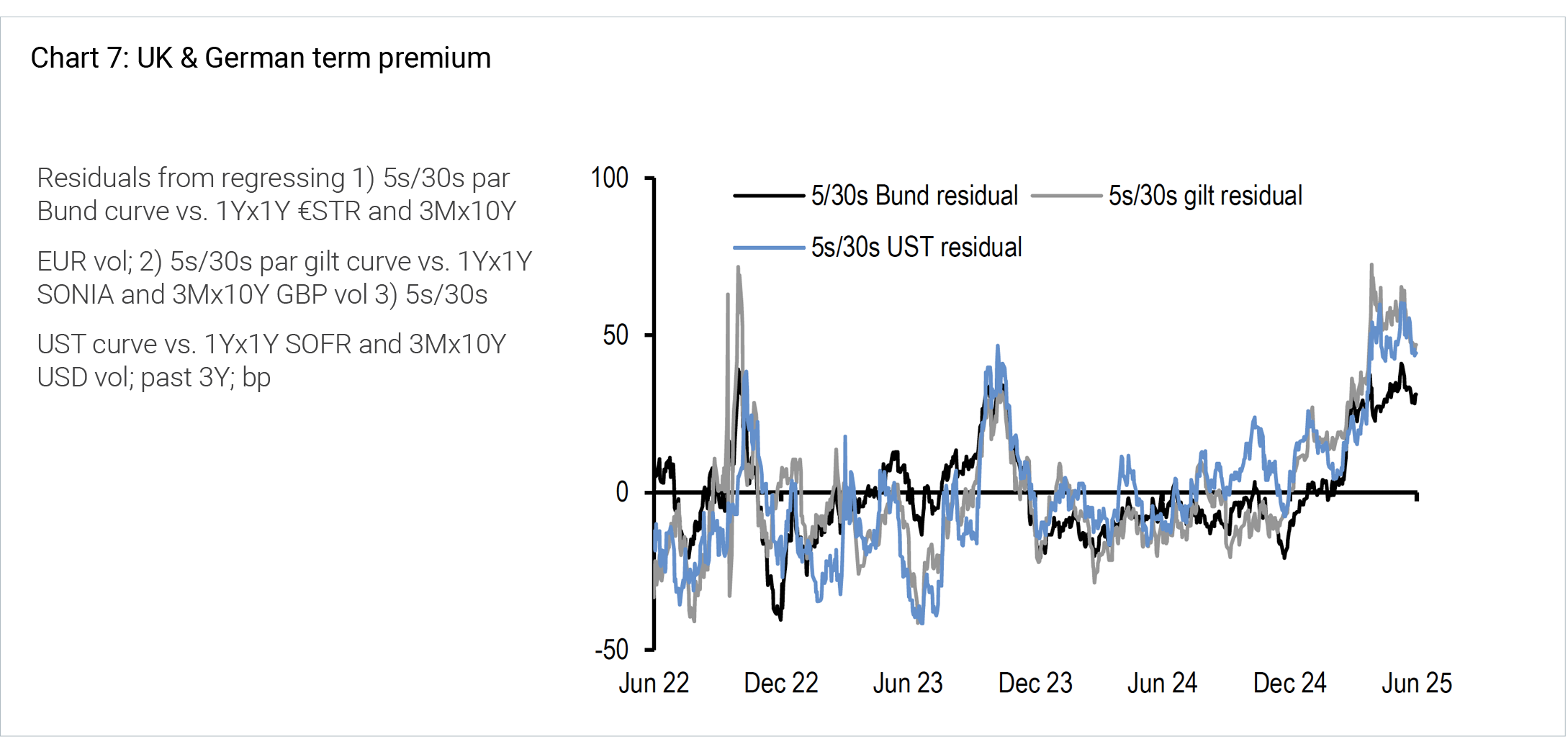

Likewise, JP Morgan analysis estimates the term premium for these economies, despite fiscal idiosyncrasies between them, remain well correlated.

At an absolute level, long bond yields across developed economies remain higher than pre-COVID. In part this is because of higher long run neutral rates (known as r*), due to structurally higher inflation expectations (less global slack), as well as larger government deficits, higher investment needs and more issuance.

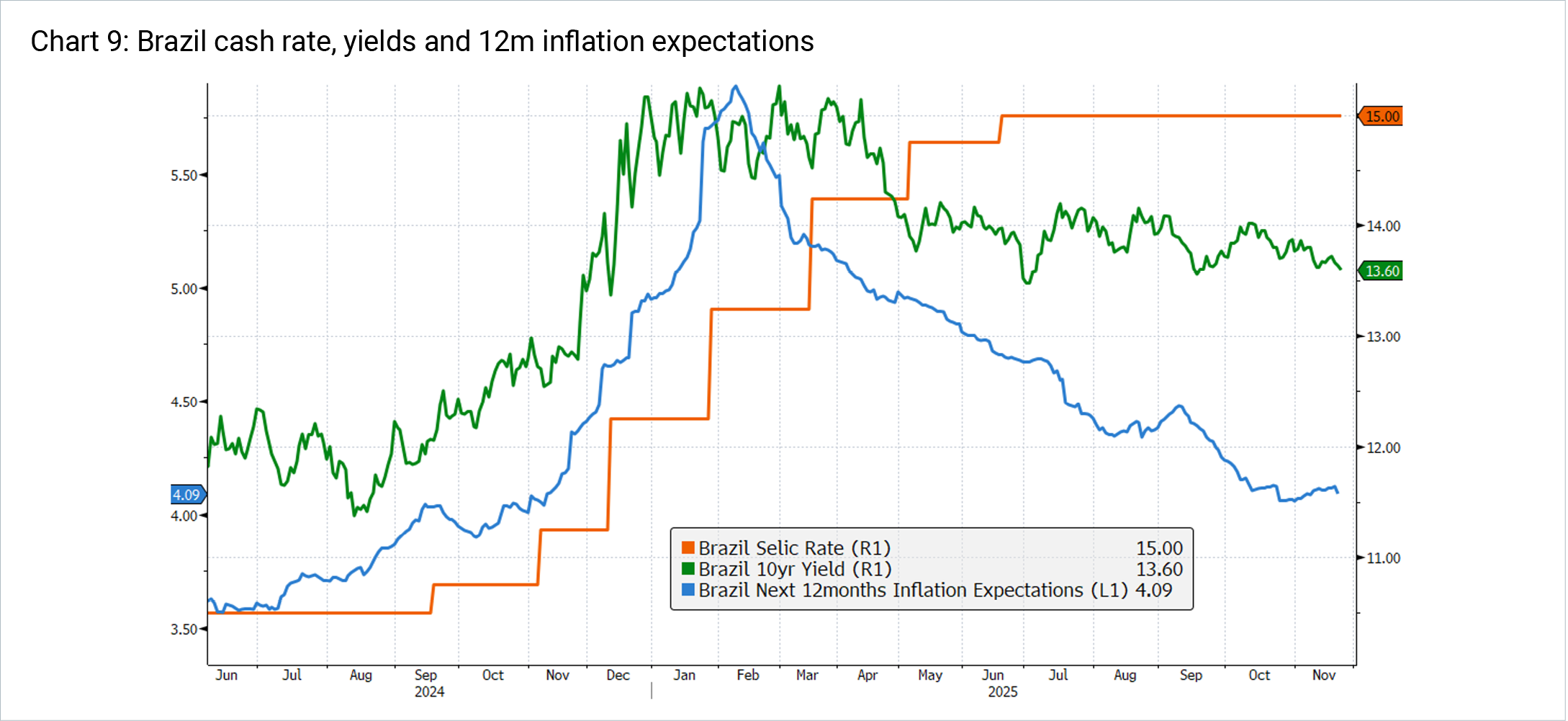

By contrast, Brazil has reported the opposite moves in short term cash rates and long term yields. From mid 2024 the central bank aggressively raised the SELIC rate 450bps to 15% to combat rising inflation expectations due to market expectations of lower government fiscal discipline and constraint around annual budget planning. This aggressive hiking cycle, while painful, also aimed to cool strong domestic economic growth. To date this has proved successful, with inflation expectations coming back down towards the target range. Since the start of 2025 cash rates are up 275bps and 10 year yields have actually fallen 120bps. A key reason for this, according to Bloomberg's Brazilian Economist, is the ultra hawkish approach has actually given the central bank a credibility boost, which has reduced the risk perception and lowered inflation expectations. Looking at the 5 year rate, which declined to 13.2% from 15.5% at the start of the year (even as policy rates rose 275bps), Bloomberg states that their "model attributes 150bps of the cumulative 240bp drop to an improvement in risk factors. In our view, this largely reflects reduced concerns over monetary policy making under Gabriel Galipolo, who became central bank governor in January for a 4 year term" 6

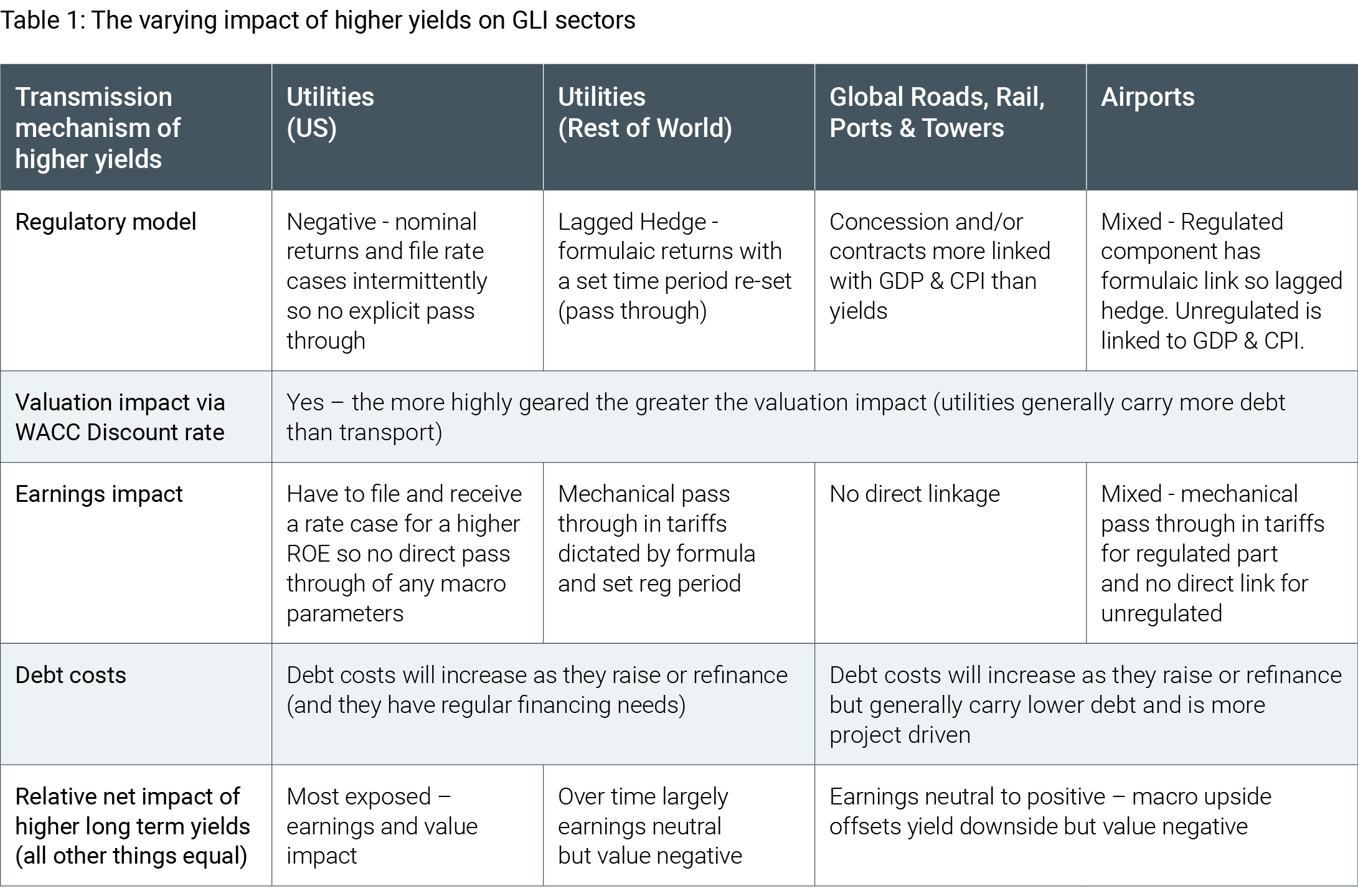

Why this matters - the relationship between infrastructure values and yieldsAt 4D, we use long bond yields to discount the cashflows from these long duration assets. Therefore, a steeper curve - as well as a permanently higher curve - has an impact on valuations of infrastructure assets as a simple function of discount rates. It also impacts fundamental cash flow modelling through forecast regulated return profiles, inflation expectations and borrowing costs, as well as the ability to borrow. In very general terms, it has a greater impact on the utility segment relative to other sub-sectors due to its greater correlation to economic indicators like government yields (as a building block of regulated returns) and in some cases inflation. This is where stock and sector selection within the GLI universe becomes crucial, and a truly active approach to investing is highly valuable. Across the global infrastructure universe 4D has the ability to shift between geographies and sectors where there is more or less sensitivity to long bond moves (both steepness and level of change) and look for exposures that can fundamentally capitalise on moves better than others - as well as exposures with greater ability to pass through inflation, serving to mitigate the impact of higher rates alone.

Also, ignoring sentiment and historic correlations, a number of sector dynamics are supporting fundamental growth outside historical long term yield dynamics. This is particularly relevant for the utility sector which is undergoing a seismic shift in investment mandates to support AI and data centre themes (US) and/or network upgrades to support energy transition and replacement spend (Europe). As such, the historic tight correlation of utility share price performance with yields is potentially no longer warranted, as seen in Chart 11 from early 2024.

ConclusionOne must be careful not to naively assume the Fed's easing cycle is a slam dunk for long duration assets such as utilities and infrastructure assets. The long end of the curve drives GLI valuations more than the short end, and since the Fed started cutting rates in 2024 we have witnessed something rare by historical standards - an increase in long term yields. This has been driven by an increase in the term premium, due to increased political and economic uncertainty, worsening debt metrics, long term budget outlooks and supply-demand dynamics. At 4D we monitor these risks and construct and actively manage a portfolio to balance the risks and opportunities across geographies and sectors. Furthermore, with an active approach to portfolio construction, we can target exposures with idiosyncratic drivers of earnings growth to offset these factors, such as those seen in the networks businesses globally.

The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. |

|

Funds operated by this manager: 4D Global Infrastructure Fund (Unhedged) , 4D Global Infrastructure Fund (AUD Hedged) |

Source: 4D, Bloomberg as at 20/11/25M

Source: 4D, Bloomberg as at 20/11/25M Source: Bank of Greece, Federal Reserve Bank of Saint Louis and LSEG

Source: Bank of Greece, Federal Reserve Bank of Saint Louis and LSEG Source: 4D, Bloomberg as at 20/11/25

Source: 4D, Bloomberg as at 20/11/25 Source: Bank of Greece, Federal Reserve Bank of Saint Louis and LSEG

Source: Bank of Greece, Federal Reserve Bank of Saint Louis and LSEG Source: NAB, Bloomberg, Fed Reserve Bank of New York, Macrobond

Source: NAB, Bloomberg, Fed Reserve Bank of New York, Macrobond Source: 4D, Bloomberg

Source: 4D, Bloomberg Source: JP Morgan

Source: JP Morgan Source: 4D, Bloomberg

Source: 4D, Bloomberg Source: 4D, Bloomberg

Source: 4D, Bloomberg

Source: 4D, Bloomberg

Source: 4D, Bloomberg

8 Dec 2025 - Performance Report: ECCM Systematic Trend Fund

[Current Manager Report if available]

8 Dec 2025 - Performance Report: Bennelong Long Short Equity Fund

[Current Manager Report if available]

8 Dec 2025 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

8 Dec 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Paradice Australian Mid Cap Fund - Active ETF | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Paradice Australian Equities Fund |

||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| Antipodes Global SMID Active ETF (ASX: MIDS) | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| ELM Responsible Investments Global Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

ELMRI ANZ Conviction Fund |

||||||||||||||||||||||

|

||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

5 Dec 2025 - Hedge Clippings | 05 December 2025

|

|

|

|

Hedge Clippings | 05 December 2025 At the kind invitation of Conexus Financial, Hedge Clippings attended their Professional Planner Researcher Forum earlier this week. Held over two days in the Blue Mountains, apart from AFM, the event brought together a wide range of industry and sector participants (including research houses Lonsec, Morningstar, SQM, and Zenith), asset consultants, platform operators, advice groups, along with many others from the industry. Keynote speakers included ASIC Commissioner Alan Kirkland, industry luminary Graham Rich, and former gold medal-winning swimming legend Grant Hackett, now CEO of GDG, the listed owner of Lonsec and Evidentia. It's fair to say that the major and constantly recurring theme was the issue of conflict of interest (potential or real, depending on one's point of view) against the backdrop of the failure of Shield and First Guardian. However, rather than trying to cover the entire proceedings in Hedge Clippings, we have included selected links below to Professional Planners' own coverage of their event, and would recommend our readers explore further if interested. Commissioner Alan Kirkland, while defending the speed at which ASIC moved to shut down Shield and First Guardian, left no one in any doubt that they will not only be taking legal action against those they believe responsible, but will be following that up with new regulations, although non-specific on what those will be. One has to hope that it will be a practical and measured reaction, although we will have to wait and see in that regard. Insignia Financials' CEO Scott Hartley predicted a chaotic year ahead, thanks to Shield and First Guardian and the regulators' response. All present agreed this combination has potentially created a watershed moment for the research and advice sector, although depending on where one's loyalties, level of conflict of interest, or culpability lies, not everyone agreed on the solution, or in the case of conflict of interest, if they had one! Of interest was Morningstar's impending change to a "pay to play" model, just as ASIC is expected to increase scrutiny on the sector. Graham Rich summed up the issue of conflict nicely by reminding all present why some people rob banks ("it's simple, that's where the money is") while others were heard to comment "no conflict, no interest". We maintain the view that the "issuer pays" model is inherently conflicted and therefore open to potential abuse, even if not by the main participants, then by the bad actors in the distribution chain, including some, such as lead generators, that ASIC claims are outside the regulator's jurisdiction. For our part, we pointed out that while the consumer (advisors and platforms) might want a research report (even if they're not paying for it), the party paying, namely the fund manager, is more interested in the actual rating. Enough! Next week, the RBA meets for the last time this year, and we'll bring you our synopsis of the outcome, thanks to Renny Ellis and Nick Chaplin, from Arculus and Seed Funds Management, respectively. And for those more interested in trivia and comedy than conflicts of interest, today marks the 51st anniversary of the last Monty Python Flying Circus show back in 1974. In our opinion, it was, and remains one of the best, and most groundbreaking comedy series ever. News | Insights New Funds on FundMonitors.com 10k Words | Equitable Investors Is travel becoming the new status symbol for Gen Z? | Insync Fund Managers October 2025 Performance News November 2025 Performance News Bennelong Australian Equities Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |