News

13 Aug 2025 - 10k Words |August 2025

|

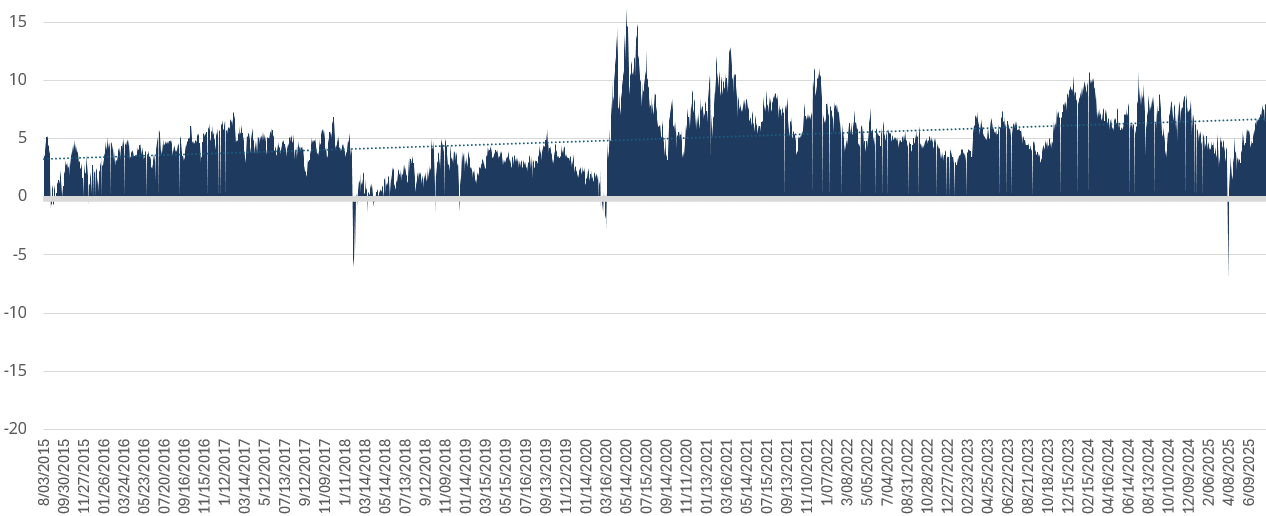

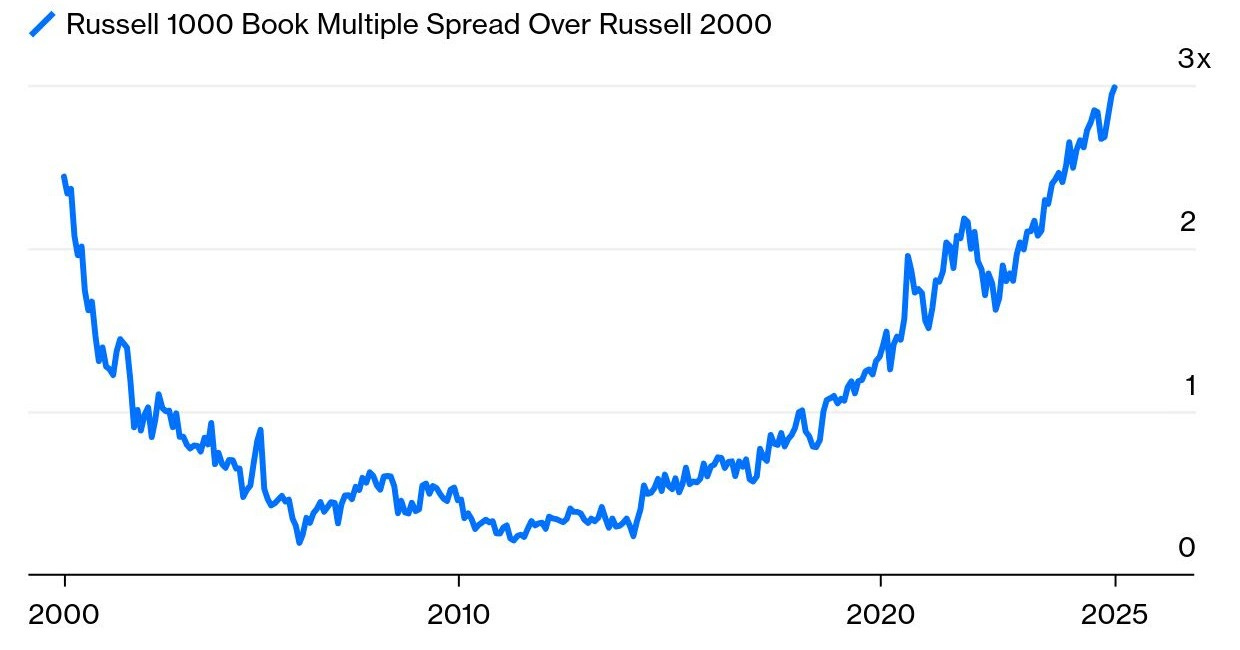

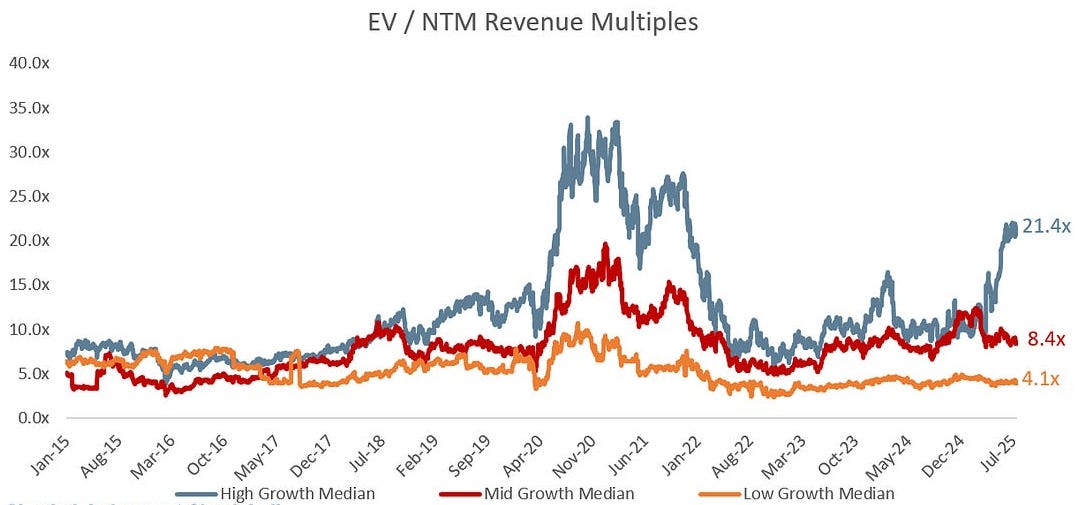

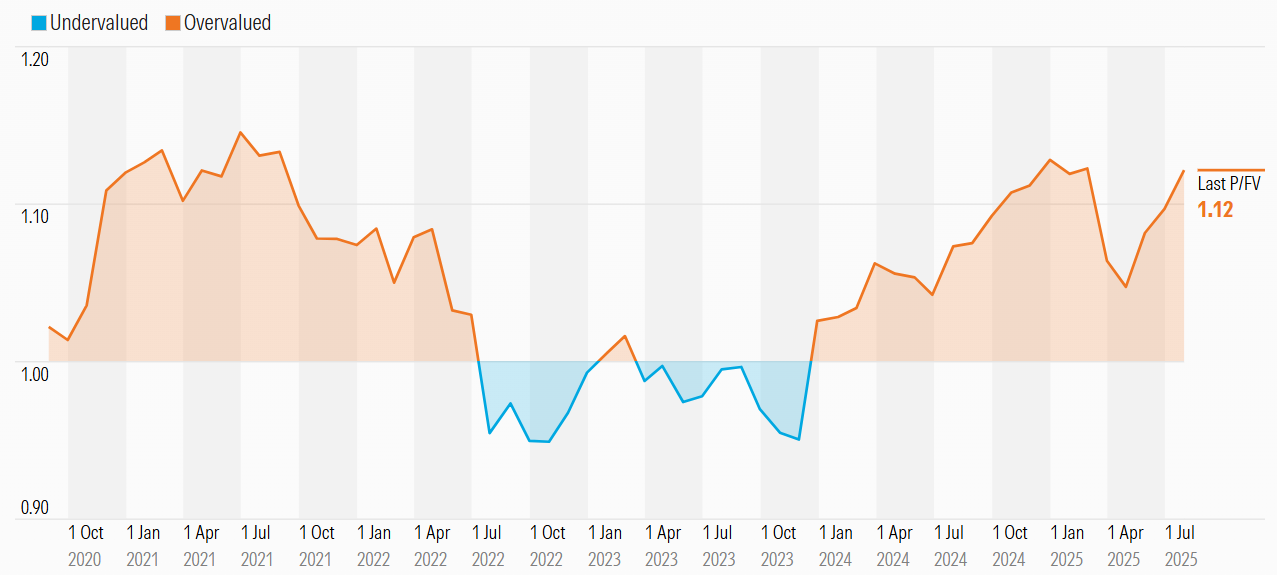

10k Words Equitable Investors Aug 2025 Apparently, Confucius did not say "One Picture is Worth Ten Thousand Words" after all. It was an advertisement in a 1920s trade journal for the use of images in ads on the sides of streetcars... There's a healthy spread between the volatility investors are pricing in for small caps relative to large caps but high yield ("junk") spreads are near historical lows. Sticking with the small-big spread, the price/book chart is smiling back at you. Valuations for high growth companies have shot away from the pack, giving the US market an edge over Australian multiples - but with both above fair value according to Morningstar. ASX large caps have seen more upgrades than downgrades in the week leading into reporting season. We divert to look at the split of assets between generations and the affordability of housing; stablecoins becoming relevant players in the US treasuries market; China's declining population of workers; and finally volatility for "Dr Copper". Spread between VIX (S&P 500 implied volatility) and Russell 2000 VIX (small cap implied volatility)

Source: Equitable Investors ICE BofA US High Yield Index Option-Adjusted Spread

Source: FRED (Federal Reserve of St Louis) Premium in US large caps' price/boom multiples is the widest in 25 years

Source: Bloomberg Recent multiple expansion in "high growth" (>25% YoY growth) companies

Source: Altimeter via Clinton Capital Forward P/E - US v Australia

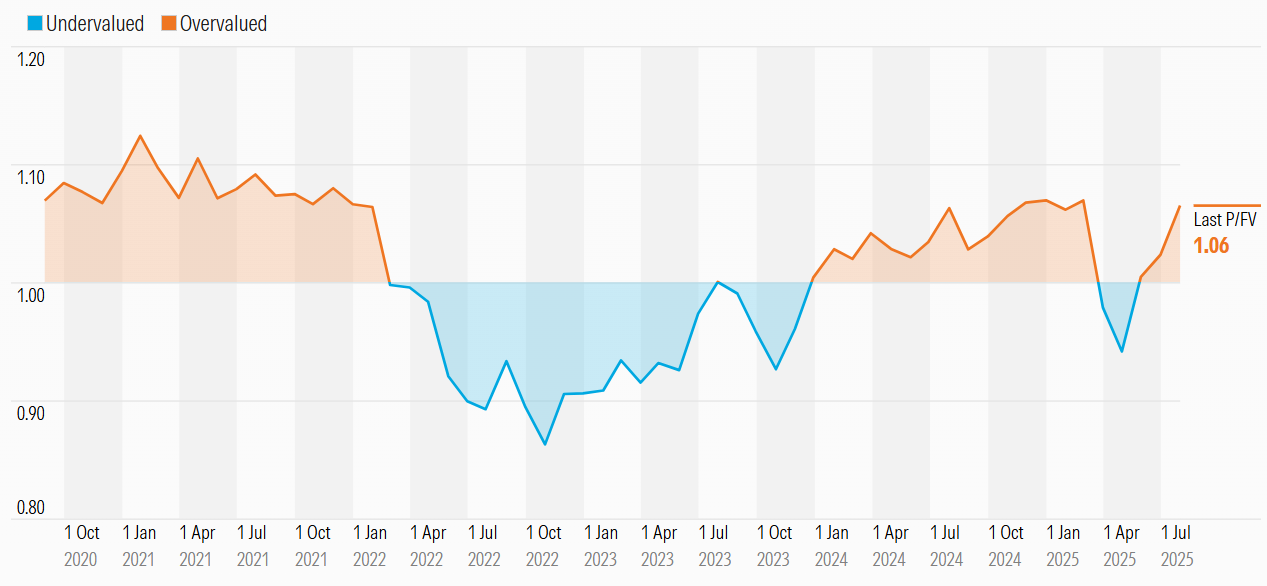

Source: Ord Minnett Australian market trading above Morningstar's bottom-up fair value estimate

Source: Morningstar US market has also return to a premium v bottom-up fair value

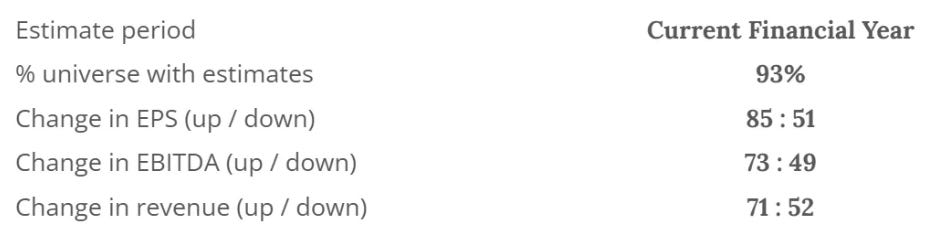

Source: Morningstar More consensus upgrades than downgrades for ASX large caps over week leading into August reporting season

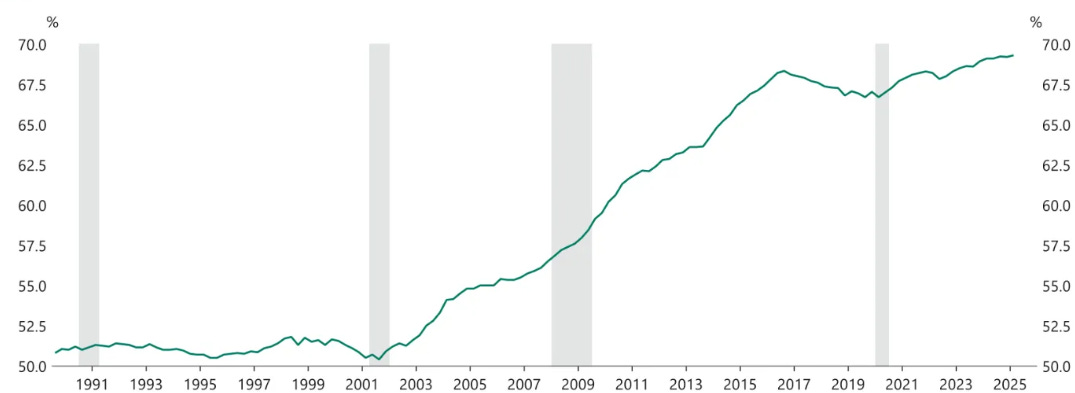

Source: Equitable Investors Share of US household assets owned by those aged 55 and above

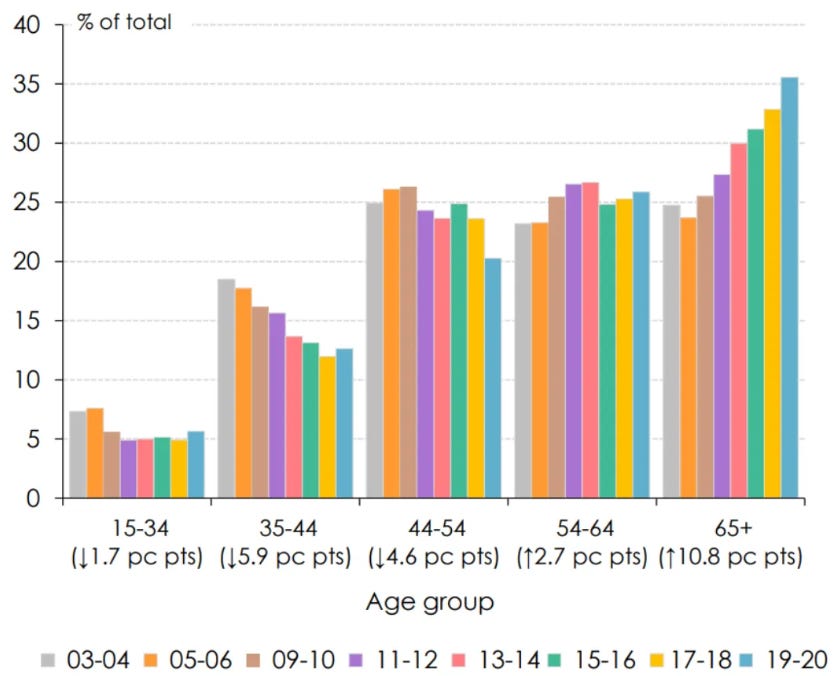

Source: Apollo Global Management Distribution of Australian household net worth by age group

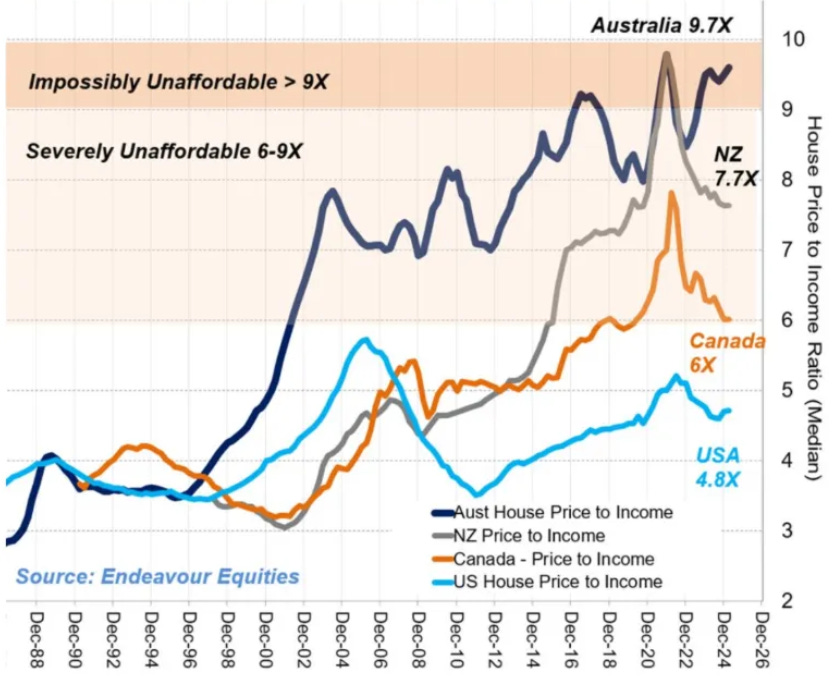

Source: Saul Eslake House price to income ratios

Source: Endeavour Equities Stablecoins the 18th largest external holder of US Treasuries

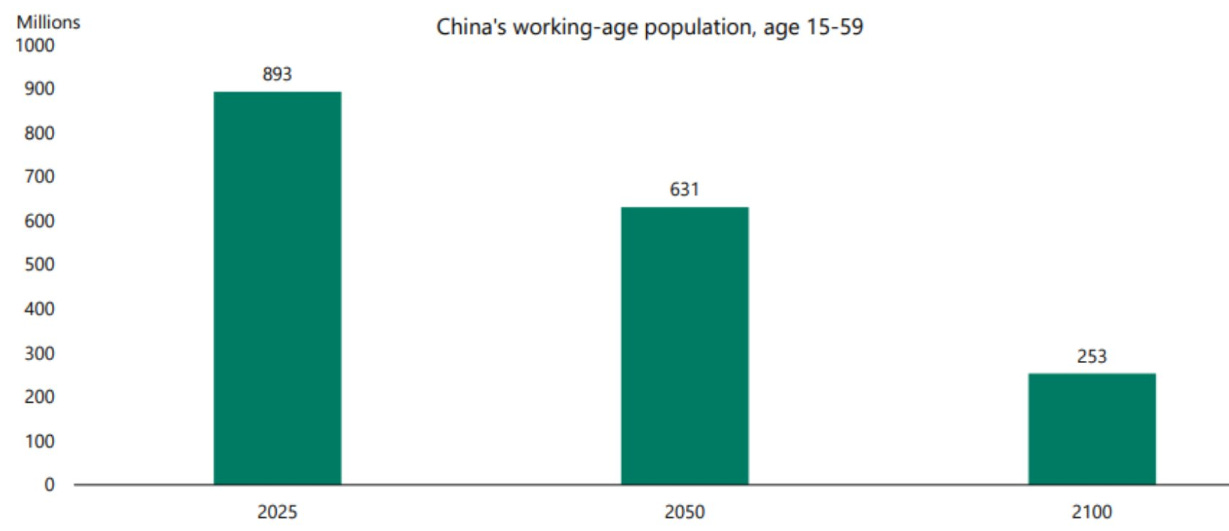

Source: The Kobeissi Letter China's working-age population expected to decline dramatically

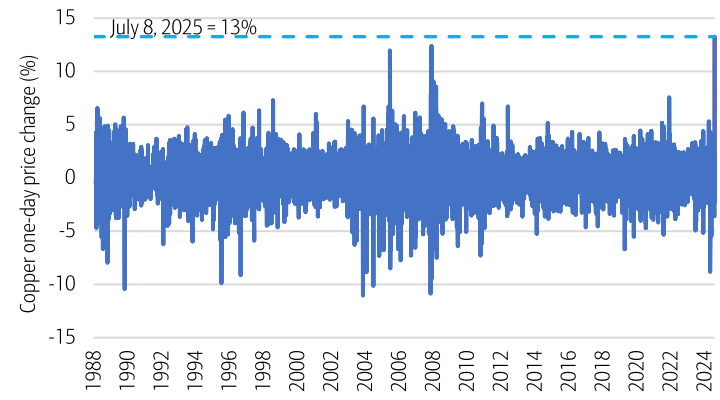

Source: Apollo via Forager Dr Copper has turned volatile - daily price changes

Source: BoAML August 2025 Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

12 Aug 2025 - Australian Secure Capital Fund - Market Update

|

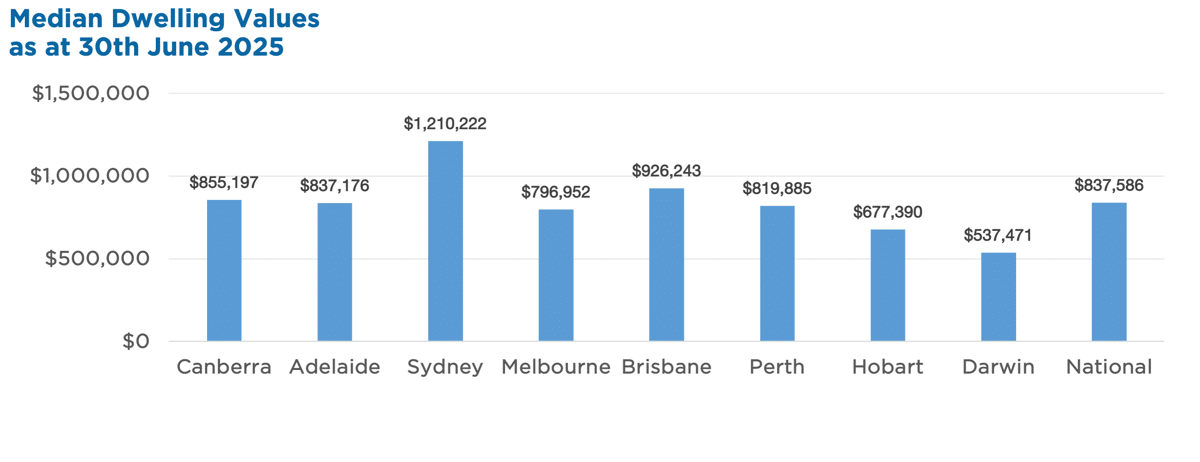

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund July 2025

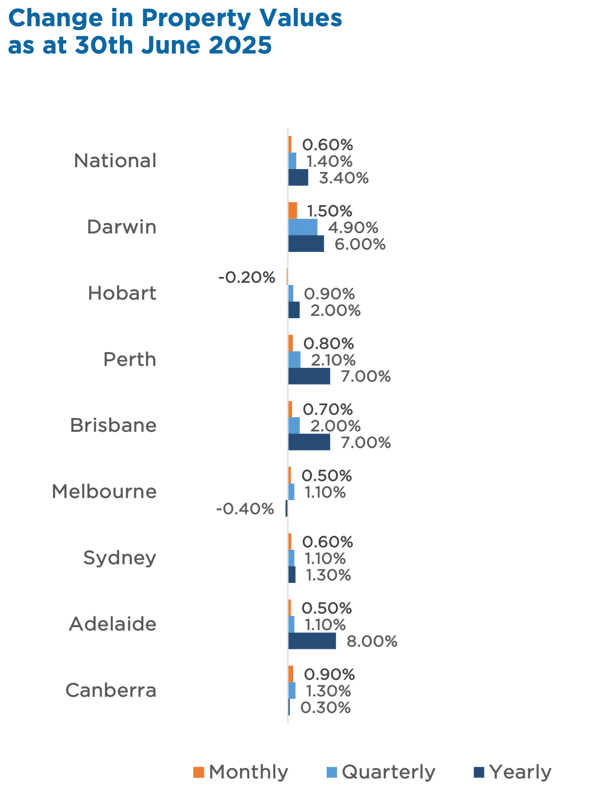

Australian housing values rose 0.6% in June, marking five straight months of growth. The June quarter saw a 1.4% national increase, with gains across most capital cities - driven by falling interest rates and low advertised stock. Key highlights:

Despite affordability constraints and economic uncertainty, tight supply and easing rates continue to support modest value growth across Australian markets. Property Values as at 30th of June 2025 Median Dwelling Values

|

11 Aug 2025 - 5 Things Investors Get Wrong About Trend-Following

|

5 Things Investors Get Wrong About Trend-Following East Coast Capital Management August 2025 5 Things Some Investors Get Wrong About Trend-Following - And Why It's Worth Rethinking Portfolio Resilience Trend-following has been a cornerstone strategy for many sophisticated allocators over decades. Yet it remains surprisingly underrepresented in the portfolios of high-net-worth individuals and family offices. Why? Because common misconceptions often overshadow its proven benefits. Below are five of the most frequent misunderstandings we hear from advisers and investors, and why it's worth taking a fresh look.

It's a refrain that pops up regularly: "Trend-following is dead." History tells a different story. During major market dislocations - such as 2008, 2014, 2020, and 2022 -- trend-following strategies have often been among the best performers. The key is understanding that trend-following is cyclical, not broken. It thrives in volatile or directional markets, i.e. precisely when traditional portfolios, heavily reliant on equities and bonds, struggle.

This is a common oversimplification. Trend-following isn't about hype, news, or hot sectors. It's about price confirmation. Systematic, rules-based models scan global markets daily, adjusting exposures based solely on observable price trends. This removes emotion and narrative bias from the equation, resulting in a disciplined process rather than a speculative bet.

Uncorrelated doesn't mean reckless. In fact, professional trend-following programs explicitly target and manage volatility. More importantly, trend-following tends to be "long volatility", meaning it often gains when traditional assets fall sharply. This provides essential ballast in downturns, preserving capital when it matters most.

That was the perception decades ago, but today's trend-following strategies are far more diversified. They trade across equities, fixed income, currencies, and commodities, spanning global liquid markets. These aren't directional commodity bets; they are dynamic, macro-driven strategies that adapt to evolving market regimes.

Some treat trend-following as purely tactical or opportunistic. The data challenges this view. Over full market cycles, trend-following has delivered consistent positive returns, low correlation to traditional assets, and strong risk-adjusted performance -- especially in equity crises. This makes it a powerful core diversifier for multi-asset portfolios focused on resilience. Conclusion At ECCM, we view trend-following not as speculation, but as a portfolio stabiliser. It requires no forecasting or macro calls, just a robust, repeatable process to adapt as markets shift. For investors seeking durable, long-term capital growth with reduced drawdowns, trend-following deserves serious consideration. Funds operated by this manager: |

8 Aug 2025 - Expert analysis on what the RBA will do next Tuesday, August 12

|

Expert analysis on what the RBA will do next Tuesday, August 12 FundMonitors.com August 2025 |

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management, and Renny Ellis, Director & Head of Portfolio Management at Arculus Funds Management, ahead of the RBA's August board meeting. Both accurately predicted July's decision to hold rates and weigh in on whether a cut is likely this time. They discuss key economic indicators--including unemployment, inflation, fiscal stimulus, and consumer sentiment--arguing that while conditions justify holding steady, political pressure may force the RBA's hand. The conversation also touches on global influences, particularly rising inflation risks in the US driven by tariffs and currency movements. Both managers share their outlook for the remainder of the year, expecting at most one further rate cut, and outline how they're positioning portfolios amid uncertainty in rates, credit markets, and global economic trends. |

8 Aug 2025 - Phil Strano: Is now the sweet spot for active bond management?

|

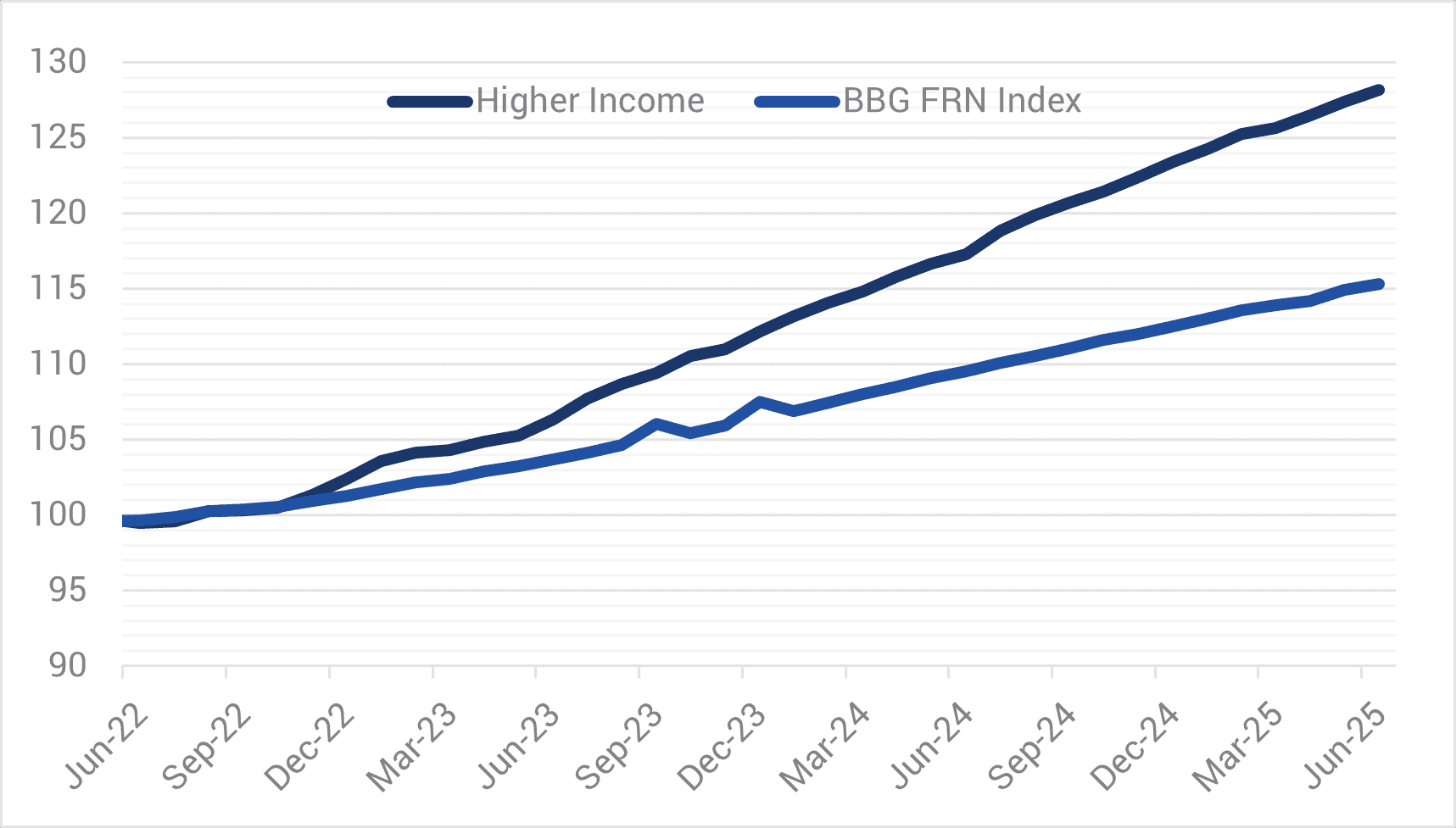

Phil Strano: Is now the sweet spot for active bond management? Yarra Capital Management July 2025 The volatility currently seen in bond markets is being fuelled by a combination of macroeconomic forces. In the U.S., ballooning fiscal deficits and a new $3.8 trillion tax bill are putting upward pressure on long-term interest rates. At the same time, foreign demand for U.S. Treasuries appears to be weakening. Central banks are reducing interest rates, yet are constrained in their influence over longer-dated bonds. Meanwhile, Australia faces a decade of projected deficits of its own, and our yield curve continues to respond more to global forces than domestic settings. These pressures are driving significant steepening in the yield curve - the difference between short- and long-dated bond yields. Steepening curves allow skilled credit managers to adjust risk exposure and capitalize on price differences. In this environment, extending the maturity of our bond holdings has become more appealing, particularly given longer-term bonds can offer stronger price gains as they approach maturity - a dynamic we term "rolldown." At the same time, we're also seeing anomalies in credit spreads, where less sophisticated investors are prioritising yield over relative value, creating pockets of possible mispricing. This is where active management proves its worth. Passive bond funds are bound by index rules. They cannot reposition for anticipated curve moves, nor can they selectively add risk when prices dislocate. Given the Bloomberg FRN Index is more highly rated (average AA- compared to BBB) with shorter spread duration (~two years compared to ~three), the Yarra Higher Income Fund (HIF) is well placed to outperform during risk-on periods (refer Chart 1). However, HIF's outperformance during certain risk-off periods demonstrates the potential benefits of active management. HIF outperformed the index through 2022 in an environment of both higher bond yields and credit spreads and more recently in April 2025. Outperformance in April provides a recent example of how nimble decision-making up and down the curve may contribute to risk adjusted returns. While the FRN Index posted a negative excess return of 11bps compared to the RBA Cash Rate, HIF posted a positive 32 bps excess return despite credit spreads widening by 20-30bps over the month. In April, we started the month expecting volatility around geopolitical events, which prompted us to lift cash levels and position our portfolios with higher overall interest rate duration. Crucially, we also implemented this with a steepening bias or, in other words, a view that long-term interest rates would rise faster than short-term rates. By focusing our exposure on the front of the curve, or short-term bonds, and being underweight long-term bonds at the back end, we were well-positioned when the long end sold off sharply while the short end remained stable. Chart 1 - Cumulative Return - Yarra Higher Income Fund v. Bloomberg FRN Index

Source: YCM/BBG, June 2025.In terms of stock selection, April also presented some fantastic buying opportunities for us to take advantage of spread widening and add high-quality credit exposures at discounted levels. One such name was the USD-denominated Perenti 2029 bonds, an issuer we had previously sold at tight spreads of BBSW+180bps and were able to buy back ~200bps wider (BBSW+380bps). Credit spreads have since contracted ~100bps from these wides, providing a tidy return on investment. While our portfolio positioning has not changed markedly from 12 months ago, these two recent examples show how we're actively managing nimble, benchmark-unaware portfolios that are more 'all-weather' credit in nature. Our April performance, in which both Yarra's Enhanced Income Fund (EIF) and Higher Income Fund (HIF) posted positive absolute returns, underscores the value of our approach. Our strategy came together as a result of preparation, speed, and conviction, none of which are available to passive strategies. Looking beyond the tactical wins, and the case for active credit is supported by the broader macro context. While spread volatility continues, outright yields in the front and mid-parts of the curve have held steady. That means the income on offer remains attractive - and investors are simply being rewarded through a different mix of risk premia. The flexibility to shift between spread and rate risk allows us to preserve capital and position for growth, depending on where the market is offering best value. It's a powerful setup. Investment-grade credit today is offering yields that, on a 12-month view, look comparable to long-term equity market returns - but without the same drawdown risk. Across the spectrum, private credit looks less compelling: the illiquidity and default risk required to justify allocations to private credit simply aren't being compensated in this environment. Looking ahead, we see the drivers of this opportunity set - fiscal overreach, inflation variability, and steepening curves - as persistent features of the bond market over the next 6 to 12 months. We believe this is a sweet spot for credit investing. High running yields and steeper curves, allowing active positioning across durations are compelling and signal the era of 'buy everything and wait' in fixed income is over. Today's market rewards clarity of view, agility of execution, and a willingness to lean into volatility when others step back. |

|

Funds operated by this manager: Yarra Australian Bond Fund , Yarra Australian Equities Fund , Yarra Emerging Leaders Fund , Yarra Income Plus Fund , Yarra Enhanced Income Fund , Yarra Australian Smaller Companies Fund , Yarra Ex-20 Australian Equities Fund , Yarra Global Small Companies Fund , Yarra Higher Income Fund |

7 Aug 2025 - Pivot, don't panic: America's next act

|

Pivot, don't panic: America's next act Magellan Asset Management July 2025 |

Every few years, geopolitical commentators declare the end of American global leadership. Sometimes it's after a messy war. Other times it's a financial crisis, political dysfunction or, most recently-- strikes on Iran or China's rise.The paradox of the United States' position is this: Even as the US navigates unprecedented challenges, it retains formidable influence in shaping the global order and the United States remains the world's indispensable power, because the US course-corrects in a few ways few nations can. Contrary to claims that the United States is retreating into isolationism, recent actions tell a different story. Despite widespread perceptions that the Trump administration is disengaging, the US remains deeply involved in every major global theatre. Before Trump's election, pundits predicted the Administration would abandon Ukraine, yet it has maintained its pursuit of difficult negotiations with Russia. In the Middle East, the US is managing complex ties with Israel, strategic imperatives surrounding Iran's nuclear program and Arab partnerships grounded by billions in energy and infrastructure deals. While these actions have dominated recent headlines, nowhere is the evolution of US leadership clearer than in Asia. For Australia and its neighbours, the question is not whether the United States is leaving, but how it is adapting militarily, economically and technologically to strengthen its partnerships and counteract China's rise. Militarily, the US remains the world's most capable power. However, enduring peace and prosperity in the Indo-Pacific require more than individual actions - it requires robust partnerships. Recognising this reality, the Administration has shifted from a traditional hub-and-spokes alliance model to a more networked, flexible architecture. On his first day as Secretary of State, Marco Rubio convened the foreign ministers of the Quad, a move that both exemplified this new approach and showcased the importance of the alliance to the Administration. The Quad, and agreements like it, remain a bipartisan priority in Washington and Canberra alike, reflecting a shared vision for regional stability that is grounded in a willingness for practical collaboration. The United States and its partners are not seeking to contain China, but to ensure that competition remains fair. Economically, US policy has forced a global reckoning with China's practices. Despite widespread criticism, tariffs have become a hallmark of Trump's novel approach to policymaking. Although critics argue that this approach has strained alliances and emboldened adversaries, it has also brought countries to the table to reassess and renegotiate for fairer terms. Notably, it has exposed systemic vulnerabilities in China's economy. The June 2025 tariff reduction agreement has placed pressure on Beijing to address structural issues like forced technology transfers and industrial subsidies. For the first time in decades, it is China - not the US - playing defence in the global economic arena, triggering a recalibration that puts Beijing on its back foot. While China's $280 billion trade surplus1 with the United States has fuelled perceptions of its rising economic dominance, Beijing's actions, from IP theft to dumping, have galvanised a global response. From Europe's industrial heartlands to Southeast Asia's ports, nations are confronting the same challenges. In 2024, the European Union launched2 several anti-dumping investigations against Chinese firms, while publishing multiple reports detailing China's widespread violations of international trade norms. These actions reflect a growing recognition that Beijing's model is incompatible with fair competition. US allies such as Australia and Japan have tightened3 foreign investment rules to counter China's strategic acquisitions. Even developing economies in Africa and Latin America are pushing4 back against predatory Belt and Road lending. The United States and China are locked in a fierce competition for technological leadership. According to the Australian Strategic Policy Institute (ASPI), China is now ahead5 in 37 of the 44 critical and emerging technologies evaluated. The United States, however, maintains a lead in several foundational sectors, including advanced semiconductor devices, high-performance computing, advanced integrated circuit design, and quantum computing. This evolving landscape highlights the urgency for the United States to sustain investment in research and development, strengthen talent pipelines and deepen international collaboration to maintain its competitive edge. While the challenges facing US leadership, such as soaring debt, domestic polarisation and strategic impatience, are undeniable threats to its global standing, history shows these are not insurmountable. To claim that US global leadership is finished misreads the moment. The trade war, for all its disruptions, has forced a long-overdue debate about fair competition, supply chain security, and technological sovereignty. China's aggression has galvanised democracies to act, while US innovation ecosystems continue to set the pace in critical industries. The US has also shown a willingness to use swift military force and support an ally The United States has navigated existential crises before, from the Great Depression to the Cold War, by adapting its leadership, not abandoning it. For Australia and the Indo-Pacific region, the future is not about choosing sides, but about building a resilient network of partnerships that can progress through uncertainty together. US leadership in Asia is not waning; it is deepening. The world still looks to Washington for leadership, but that leadership must now balance the urgency of great-power rivalry with the consistency and long-term vision needed for global order.

|

|

Funds operated by this manager: Magellan Global Fund (Open Class Units) ASX:MGOC , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Global Fund (Hedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT)

1 Office of the United States Trade Representative (USTR). (2025). China Trade Summary. https://ustr.gov Important Information: Copyright 2025 All rights reserved. Units in the funds referred to in this podcast are issued by Magellan Asset Management Limited ABN 31 120 593 946, AFS Licence No. 304 301 ('Magellan'). This material has been delivered to you by Magellan and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. The opinions expressed in this material are as of the date of publication and are subject to change. The information and opinions contained in this material are not guaranteed as to accuracy or completeness. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward looking' statements and no guarantee is made that any forecasts or predictions made will materialise. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. Further important information regarding this podcast can be found on the Insights page on our website, www.magellangroup.com.au. |

6 Aug 2025 - The enemy within

|

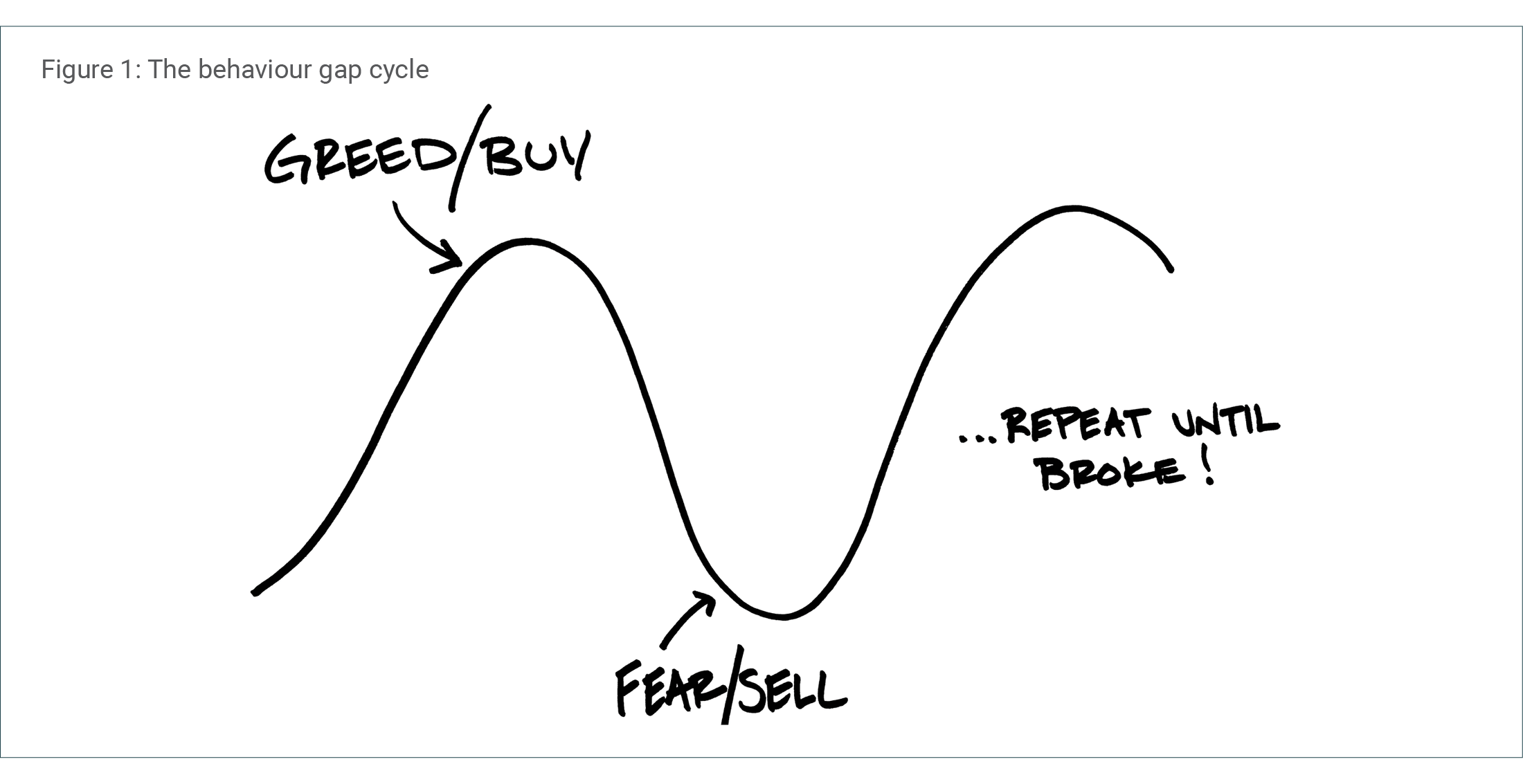

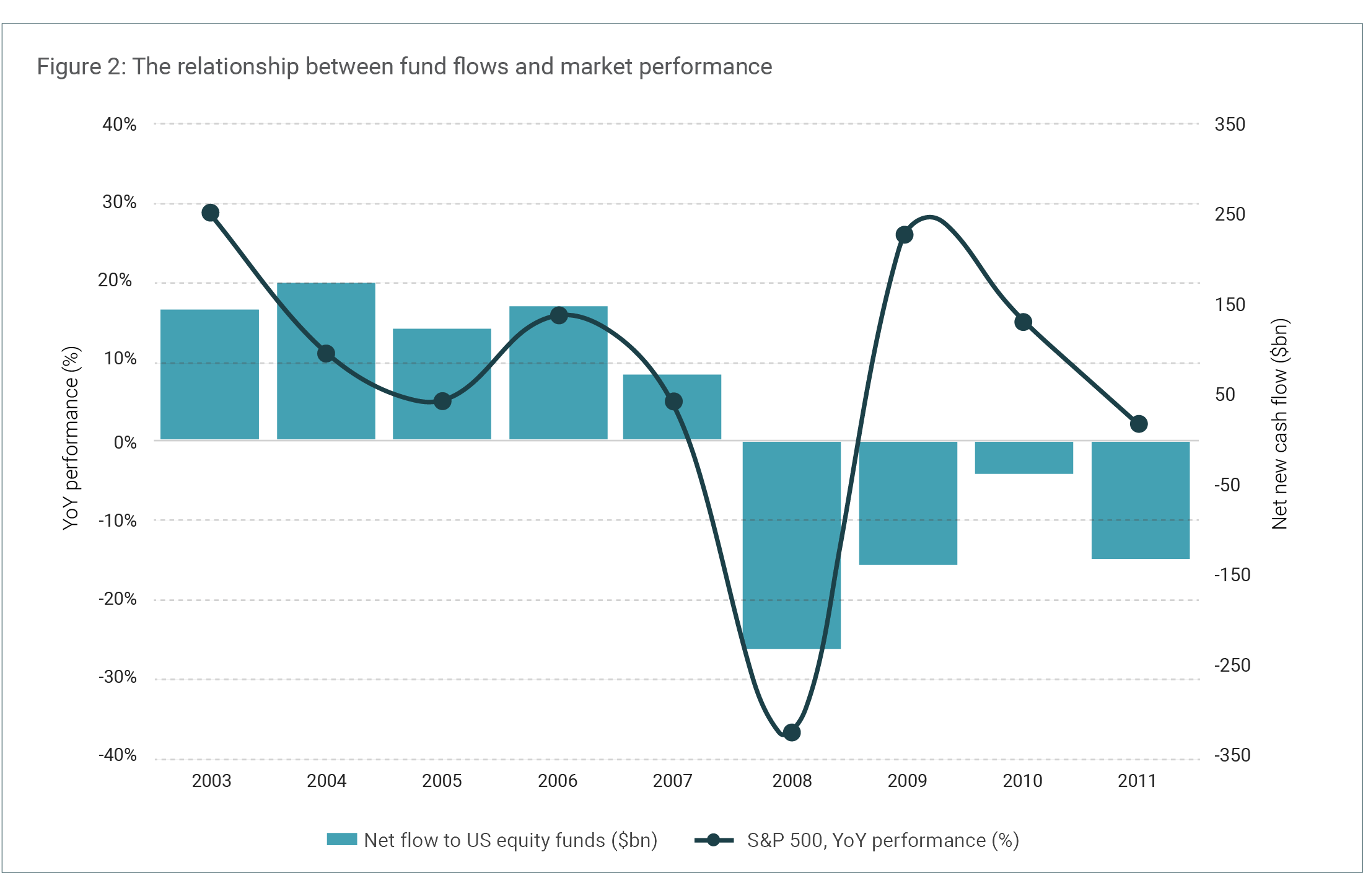

The enemy within Canopy Investors July 2025 "The investor's chief problem -- and even his worst enemy -- is likely to be himself."

|

|

Funds operated by this manager: |

Source: The Behaviour Gap, Carl Richards.

Source: The Behaviour Gap, Carl Richards. Source: Investment Company Institute, Canopy Investors.

Source: Investment Company Institute, Canopy Investors. Source: Tom Fishburne.

Source: Tom Fishburne. Source: Canopy Investors.

Source: Canopy Investors.

5 Aug 2025 - News & Views: One final round of rail consolidation?

4 Aug 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| India Avenue Equity Fund - Listed Class | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

|

||||||||||||||||||||||

| Indian Pacific Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Blackwattle Global Quality Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| VanEck Global Listed Private Credit (AUD Hedged) ETF | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

1 Aug 2025 - The Evolution and Benefits of Equity Income Funds in Australia's Growing Retirement Market

|

The Evolution and Benefits of Equity Income Funds in Australia's Growing Retirement Market Merlon Capital Partners July 2025

|

|

.Australia's growing retirement-age population has seen an increase in demand for and the availability of equity income funds over the last few decades. Australia's unique dividend imputation system means investors can successfully derive meaningful income as well as capital growth from holding Australian equities. Equity income strategies regularly make up a large component of the equity allocation for income-focused clients who seek a more defensive asset mix. Equity income funds have evolved significantly over time, beginning in the 1990s, with MLC and Colonial First State (now First Sentier Investors) launching equity income products. These initial products were not specifically focused on paying a regular, smoothed, tax-effective income but rather designed to grow capital before retirement to provide income once in retirement. The mid-2000s saw the equity income fund reimagined, designed specifically to meet retiree's key objectives - income generation, volatility management and capital growth over time. A number of managers developed products to meet these objectives at this time. The wake of the GFC saw growing recognition of the importance of total return generation from income, limiting the need to sell down holdings during market downturns. As a result, the equity income space continued to grow and through the 2010s, various managers launched new income funds, often with full market exposure. Additionally, with the rising popularity in passive investing through the 2010s, income-focused ETFs also emerged from leading ETF providers with the goal of generating income that exceeds the dividend yield offered by the broader market. With an aging population, the addressable market for equity income funds is only growing. Whilst not all equity income funds remain in existence today, there are a variety to choose from with over 15 Australian fund managers offering a product in this space. The need for regular income in retirement is well known and there are various ways to meet cashflow requirements. However, many of these tend to overlook the particularities of retirement. While fixed income products can help to meet an income objective, they fail to provide capital growth to protect against the impacts of inflation. A diminishing capital value on a real basis is inconsistent with the desire of many retirees for a growing capital base for both peace of mind and to leave an inheritance. Another option is to pursue an equity strategy centred solely on capital growth and simply selling down holdings when cashflow is required, rather than investing in income-generating investments. Yet, this ignores the fact that retirees are much more impacted by periods of drawdown than other investors, especially early in their retirement, amplified by their obligation to draw out from accounts when in pension phase. The GFC market crash and COVID-19 selloff in early 2020 demonstrated the serious consequences of needing to sell at an inopportune time and its long-term impact on total return. Skewing the components of equity total return to income removes the need to sell investments to raise cash when required. Proposed alternatives to equity income also ignore the value of franked dividends, which for retirees in pension phase present significantly more value than unfranked income or capital gains. Australian equity income strategies, when structured and executed appropriately, can provide strong total returns over time through attractive dividend yields and without sacrificing capital growth. The Merlon Australian Share Income Fund was launched in 2005 and led the innovation of contemporary equity income funds. It was the first product of its kind, aiming to provide above-market income with franking, grow capital over time with lower risk than the market. The non-benchmark portfolio has a high active share, blending well with both passive and direct share portfolios which are typically overweight large cap stocks. The Fund delivers above market income, the majority from franked dividends, paid monthly and has demonstrated strong risk-adjusted returns over multiple time periods. The strategy features a risk reduction overlay to insulate the Fund during periods of drawdown whilst retaining 100% of the franked dividend income generated from the underlying portfolio. Merlon's investment philosophy is based on the idea that behavioural biases create opportunities, even in markets considered "efficient". In particular, Merlon focuses on investing in companies where the market has become overly pessimistic, investing in undervalued companies with a focus on downside/bear case valuation to preserve capital. Merlon believes that buying companies when the market is overly pessimistic at low end of valuation range should result in growth of the capital base. Companies are valued on the basis of sustainable free cash flow, not dividend yield alone which is often a poor indicator of future performance and can lead to destruction of capital value. History has shown that investing in quality companies with sustainable free cash |

|

Funds operated by this manager: Merlon Australian Share Income Fund , Merlon Concentrated Australian Share Fund |

|

This material has been prepared by Merlon Capital Partners Pty Ltd (ABN 94 140 833 683 AFSL 343 753) (Merlon), the investment manager of The Merlon Australian Share Income Fund (Fund). Fidante Partners Limited ABN 94 002 835 592 AFSL 234668 | Fidante Partners Services Limited ABN 44 119 605 373 AFSL 320505] (Fidante) is a member of the Challenger Limited group of companies (Challenger Group) and is the responsible entity of the Fund. Other than information which is identified as sourced from Fidante in relation to the Fund, Fidante is not responsible for the information in this material, including any statements of opinion.It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. You should consider, with a financial adviser, whether the information is suitable to your circumstances. The Fund's Target Market Determination and Product Disclosure Statement (PDS) available at www.fidante.com should be considered before making a decision about whether to buy or hold units in the Fund. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Past performance is not a reliable indicator of future performance. Merlon and Fidante have entered into arrangements in connection with the distribution and administration of financial products to which this material relates. In connection with those arrangements, Merlon and Fidante may receive remuneration or other benefits in respect of financial services provided by the parties. Investments in the Fund are subject to investment risk, including possible delays in repayment and loss of income or principal invested. Accordingly, the performance, the repayment of capital or any particular rate of return on your investments are not guaranteed by any member of the Challenger Group. |