News

25 Sep 2025 - How are active ETFs reshaping the European investment market?

|

Sustainable equities outlook: AI's transformative role in an evolving global economy Janus Henderson Investors September 2025 In research commissioned by Janus Henderson in mid-2025, 42% of professional investors -- collectively managing around US$800 billion -- indicated they expect the European active ETF market could grow toward US$1 trillion by 2030. How fast is the European active ETF market likely to grow?The European active ETF market surged past US$70 billion in assets under management this summer, more than doubling in size since the start of 2024. Active ETFs still only make up 2.7% of the European ETF market, but 74% of professional investors expect this share to hit 5% by the end of next year. Globally, the pace of growth in the active ETF sector is striking. In the first half of 2025, half of all ETFs launched globally were active according to industry consultancy ETFGI. Looking ahead, nearly 60% of survey respondents expect most ETF launches in 2026 to be active.

Why are "active core" ETFs proving popular?So far, adoption in Europe has been led by "active core" ETFs, which have a low tracking error to a benchmark and often focus on research enhanced index-based strategies. Most of the investors surveyed (72%) see these ETFs as replacement for their existing index-based passive exposures. In contrast, uptake of "high-conviction active" ETFs, built on deep fundamental research to develop more concentrated portfolios, has so far been slower. However, 66% of respondents see high conviction active ETFs as potential replacements for traditional mutual fund exposures, suggesting significant runway for growth. How are investor allocations to active ETFs evolving?When survey respondents were asked how they see fund allocations to active ETFs changing over the next 12 months, the vast majority (96%) noted that these will increase by between 25% to 75%. The anticipated increases suggest growing confidence in active management strategies. These strategies seek to capitalise on the expertise of fund managers to navigate complex market environments and achieve superior risk-adjusted returns. This trend underscores the growing importance of active ETFs in modern investment portfolios. As investors continue to seek ways to optimize their portfolios, active ETFs are poised to play a pivotal role in their investment strategies over the coming year. Why do fixed income and equities lead asset exposure via active ETFs?A significant 80% of respondents reported having exposure to fixed income via active ETFs while 58% of respondents use active equity ETFs. The survey results underscore a strategic utilisation of active ETFs for achieving diversified investment portfolios. The prominence of fixed income indicates a strong inclination towards stability and income, while the engagement with alternatives (55%) suggests openness to innovative investment avenues. These insights can inform future asset management strategies and active ETF product offerings, aligning them with investor preferences and market dynamics. Why is it important to align ETF offerings with investor needs?The most dynamic innovation in the ETF space is on the active side. But unlocking the full potential will require products that closely align with what investors are seeking. We believe a well-designed suite of insight-led active ETFs, offering both core and high-conviction exposures, has the potential to bring the best of active management to investors with the efficiency and liquidity of the ETF structure. While growth expectations are strong, challenges remain. These include liquidity constraints in certain asset classes, potential tracking error, and whether high-conviction active strategies can consistently justify higher fees compared with passive or traditional active funds. Disclaimer: This article is based on information available as of mid-2025. The views expressed are those of the original author and do not necessarily reflect the views of FundMonitors.com. It is provided for educational purposes only and does not constitute investment advice. Investors should conduct their own research or seek professional advice before making investment decisions. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund Source: Janus Henderson Investors commissioned the market research company Pureprofile to interview 100 professional investors working for pension funds, family offices, wealth managers, insurance asset managers in the UK, Germany, Switzerland, Italy, France, Sweden, Norway and Finland with a total of US$781.5 billion assets under management. The research was conducted in June 2025. Active investing: An investment management approach where a fund manager actively aims to outperform or beat a specific index or benchmark through research, analysis, and the investment choices they make. The opposite of passive investing. Exchange traded fund (ETF): A security that tracks an index, sector, commodity, or pool of assets (such as an index fund). ETFs trade like an equity on a stock exchange and experience price changes as the underlying assets move up and down in price. ETFs typically have higher daily liquidity and lower fees than actively-managed funds All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

24 Sep 2025 - Investment Perspectives: Riding the silver tsunami

23 Sep 2025 - Australian Secure Capital Fund - Market Update

|

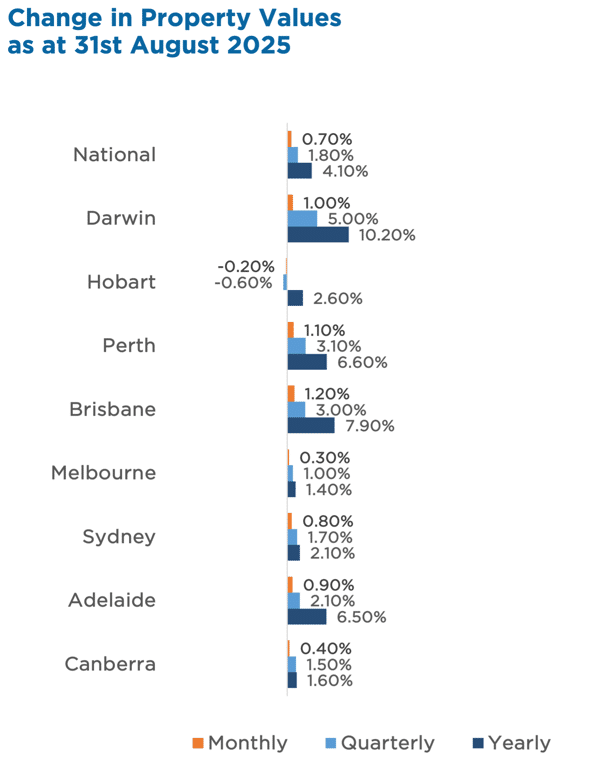

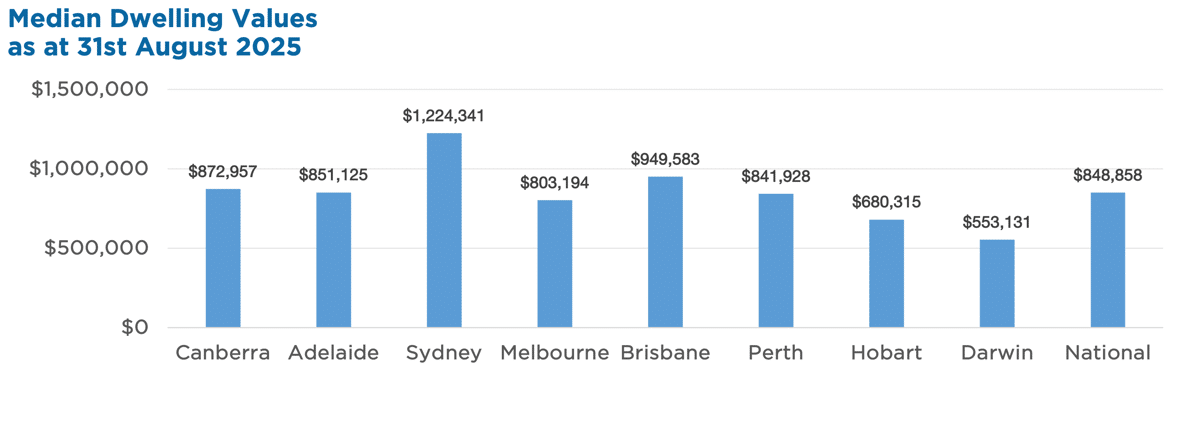

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund September 2025 Australia's housing market extended its run in August, with values up 0.7%. This is strongest monthly gain since May 2024. Annual growth now sits at 4.1%. Tight supply (listings 20% below average) and strong buyer demand pushed auction clearance rates to 70%. This is the highest since early 2024. Vendors are entering spring in a strong position, with low competition and broad-based price growth across the capitals. Highlights:

Property Values as at 31st of August 2025

|

22 Sep 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Arrowstreet Global Small Companies Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Arrowstreet Global Equity Fund (Hedged) | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Arrowstreet Global Equity Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Allan Gray Australia Balanced Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

19 Sep 2025 - Why the Gold Price Keeps Rising

|

Why the Gold Price Keeps Rising Marcus Today August 2025

|

|

Why does the gold price go up? Let me tell you the main reason the gold price goes up. All the gold dug up in the world is a lump of metal: 20.4m by 20.4m by 20.4m. That's all the gold ever dug up in the world. It grows about 2% per annum with production, and it shrinks about 2% per annum with consumption in things like electronics. So you've got this inert lump of metal, 20.4m square, sitting there -- earning nothing, doing nothing, looking pretty if it can -- and a whole load of people are running around it deciding what the price is. In the last couple of decades, two things have happened. One is exchange traded funds came along and bought. If it bought three metres by three metres by three metres, it completely changed the supply dynamics of this inert piece of metal. It's an amazing thought that if you could create an exchange traded fund backed by physical gold and start selling it, then as you sell you've got to find the gold. So you go into this inert, stable 20.4m cube and start buying chunks of it so that people invest in gold. It was self-fulfilling really. When exchange traded funds started in 2003, people started buying gold as an investment. It shoved demand up. Consequently, the gold price went from between $200 and $500 an ounce to $3,500. Now it's 20 years later and it's still going on. Exchange traded funds are buying gold, and when gold has a run it's a squeezy commodity to get hold of. That is backed by physical gold. So gold is being squeezed -- and squeezed again. Add on top of that currency. If you've got an inert piece of metal and everyone's running around it wondering what price it should be, and it's priced in US dollars, then because of a global financial crisis you print twice as many US dollars, the US dollar is worth half as much. For one thing it was the GFC, then Covid for another. Print twice as many US dollars and the currency is worth half as much. So the price of gold, and anything else priced in US dollars, doubles -- not because gold is worth any more, but because the currency is worth less. That's what's driven the gold price as well. One of the biggest drivers for the gold price is when the US dollar goes down. You'll find the gold price goes up. At the moment the US has a lot of debt. That weakens the currency. A currency is really a reflection of how strong an economy is. If they put tariffs in and it slows the US economy down, the US dollar goes down. If they start to cut interest rates, which it looks like they're going to, the currency goes down because it doesn't yield as much. All this is pushing towards a weaker US dollar. And a weaker US dollar is going to cause the gold price to go up again. So combined with the risk of "The Big One", a falling US dollar, exchange traded fund buying -- the gold price goes up. And that's what's going on at the moment. DISCLAIMER: This content is for general information purposes only and does not constitute personal financial advice. Please consider your own circumstances or seek professional advice before making investment decisions. |

|

Funds operated by this manager: |

18 Sep 2025 - Build-to-rent housing: igniting the firepower of local pension funds

|

Build-to-rent housing: igniting the firepower of local pension funds abrdn September 2025 The UK is at a critical juncture in addressing its long-standing housing undersupply. While the challenge of meeting housing demand is not breaking news, the scale of the shortfall keeps making headlines. In 2024, a shake-up in how housing need is calculated pushed the government's annual target to a bold 370,000 homes - a 20% jump from the previous benchmark. Ambitious? Absolutely. But let's be clear: the UK hasn't built at this pace since the late 1960s. If we're serious about unlocking economic growth and making housing more accessible, we need a smarter, more scalable strategy. That means building where demand is surging - and today, that's in our cities. With urban living on the rise, the build-to-rent (BtR) sector is perfectly positioned to lead the charge. Chart 1: Annual housing completions Investing and planning to meet housing targetsMeeting national housing targets requires action across all tiers of governance and investment. National policy must provide the enabling framework, regional authorities must align infrastructure and planning priorities, and local councils must accelerate approvals and unlock land. At the same time, institutional capital - particularly from local government pension schemes (LGPS) -must be mobilised to support long-term, scalable development. Developers also have a pivotal role to play in delivering housing and responding to shifting demand dynamics. With urbanisation driving housing demand, the BtR sector stands out as a key delivery mechanism that's capable of providing high-quality, professionally managed housing at scale. A step-change in delivery is not optional, it's essential. Unlocking land, streamlining planning, and mobilising long-term capital must now become national priorities. Local versus national housing targetsNational housing targets are coordinated by central government policy; they're based on broad long-term growth rates and affordability ratios. The government aims to tackle the housing crisis by building 1.5 million homes by 2030. It will use planning reforms to unlock greyfield and brownfield land[1], while significantly expanding affordable and social housing. One challenge of a predominantly national approach is that housing targets are often set using broad criteria, which may not fully capture local nuances and needs. Over the long term, they can fail to consider the economic and social impacts that well-targeted and appropriate levels of housebuilding can have at a local level. Some regions can be left behind. Focusing on local needsIn contrast, local housing delivery is led by local authorities and region-specific entities. These are much more concentrated on local city, town and regional housing needs, often considering local economic growth and regeneration agendas. Perhaps the most powerful point about locally anchored strategies is that they don't have to be mutually exclusive with national targets. In fact, central policy is already working to empower local authorities to deliver social housing, using national targets as a framework[2]. Local authorities can come under considerable pressure to meet these targets, leading to tensions when national expectations don't align with local needs or capacities. Therefore, local targets can more effectively leverage the motivations of local authorities, who can be the foremost institutional investors[3], given the scale and influence of LGPS. LGPS can be the firepower that housing needsThe 86 local authority pension funds in England and Wales now invest through eight main LGPS (ACCESS Pool, Border to Coast, Brunel, LGPS Central, LPP, London CIV, Northern LGPS, and Wales Pension Partnership). With these pools soon consolidating from eight to six, this shift will deliver even greater concentrated firepower. It will be possible to mobilise large-scale investment with enhanced professional oversight and strategic focus. Through this collective strength, current total LGPS assets of nearly £400 billion are set to grow to £1 trillion by 2040[4]. As these pools look to invest more into housing, this approach could support the delivery of up to 80,000 homes across the UK, according to research by Savills[5]. This represents around 60% of current BtR stock, which suggests the speed of delivery could really accelerate. Chart 2: Cumulative delivery of Build-to-Rent units from 2013 to 2025

How can LGPS help the housing crisis?Not only do LGPS pools have considerable financial firepower, they also have traits that make them uniquely suited to national housing initiatives. Working in partnership for BtR housingWhile LGPS pools possess critical mass, there is substantial value and capability to be added from private capital. Aberdeen can use the scale of LGPS pools to deliver high-quality rental housing that supports both local communities and national policy targets. Leaning on our existing relationships, we can comingle additional funding, use our own sector-specialists, and bring in operational expertise, all while improving resource efficiencies. We can then use this scale to diversify and deploy capital into smaller catchments, which would otherwise be unreachable by institutional investment. Working with the John Lewis Partnership, we can go one step further by unlocking well-located city-centre locations for redevelopment. This will deliver much-needed housing in urban markets through a nationally recognised and trusted brand. By adding existing BtR assets across local authorities, we can cement local goals while servicing national housing targets. Final thoughts...The net result of partnering with local authorities means that locally driven housing initiatives can be delivered at scale across regions. We can blend fiduciary duty with social outcomes that neither local authorities nor the private sector could fully accomplish alone. By helping to facilitate public-private partnerships, we can increase collaboration among pension pools and make national-level housing targets more achievable. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) |

16 Sep 2025 - 10k Words |September 2025

|

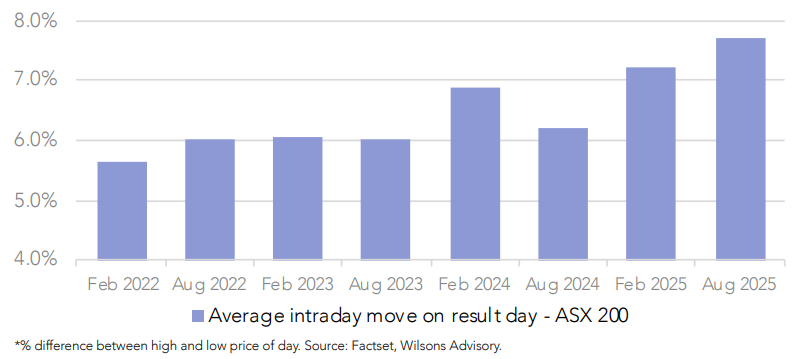

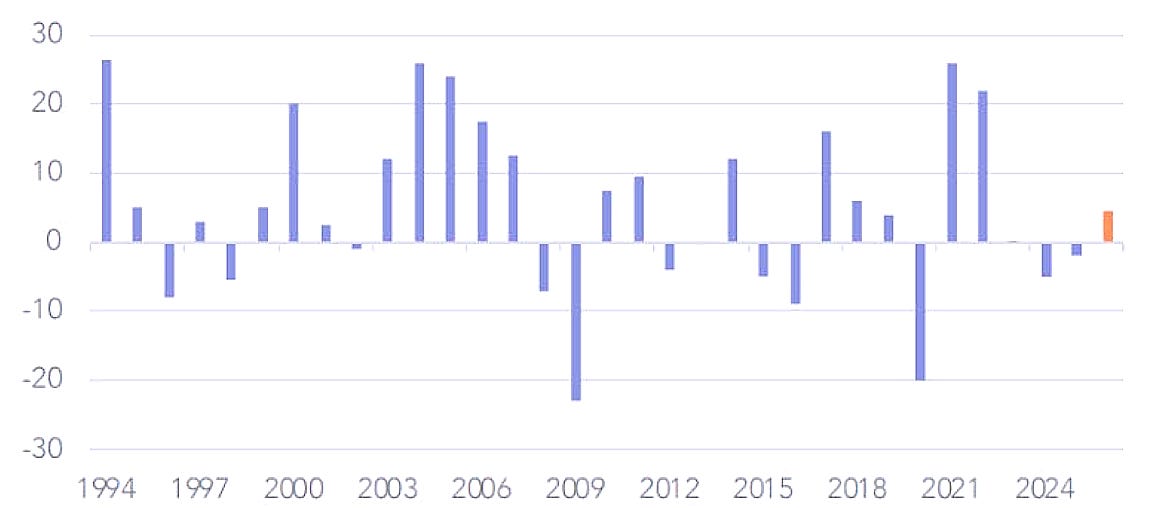

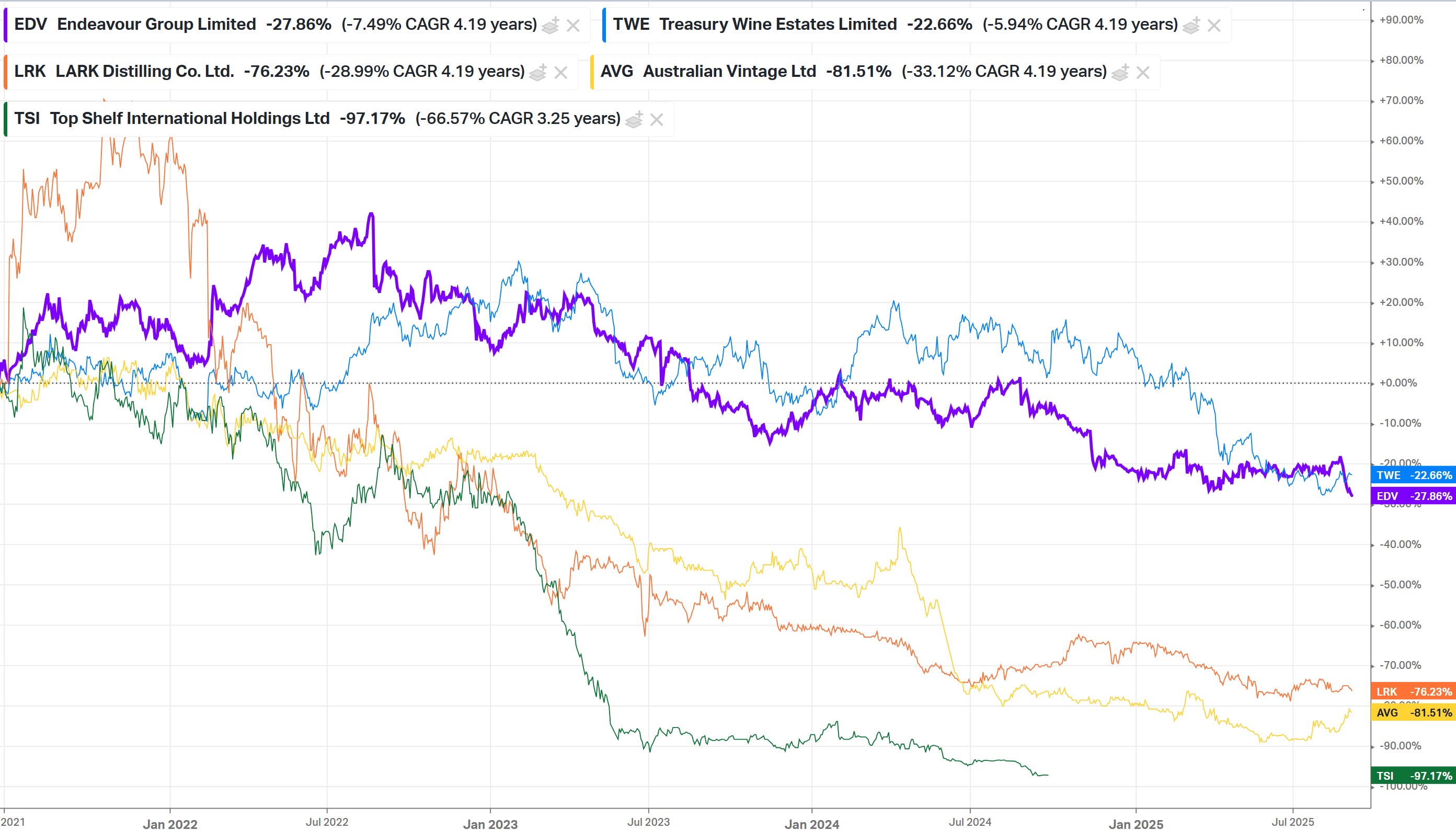

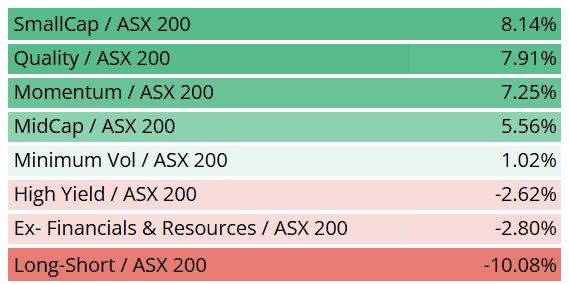

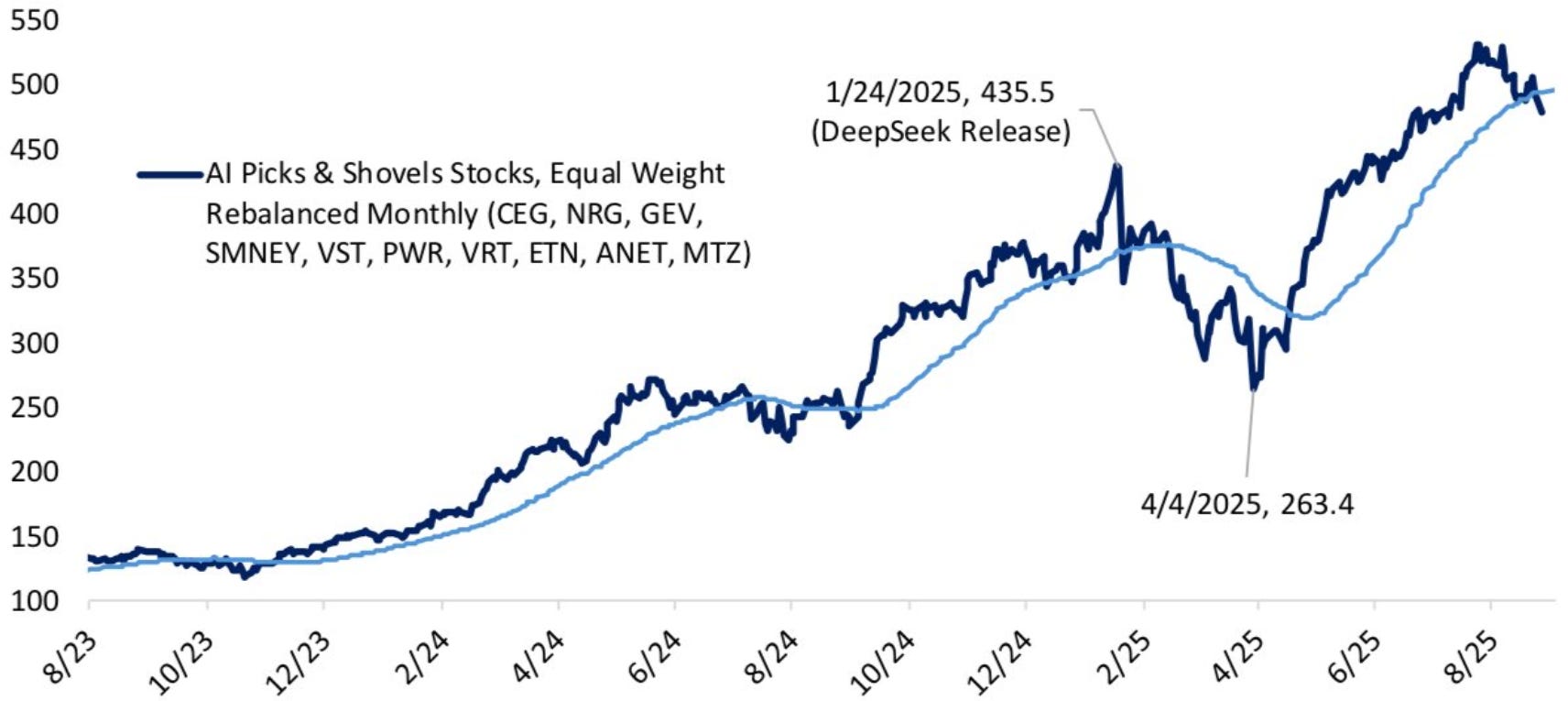

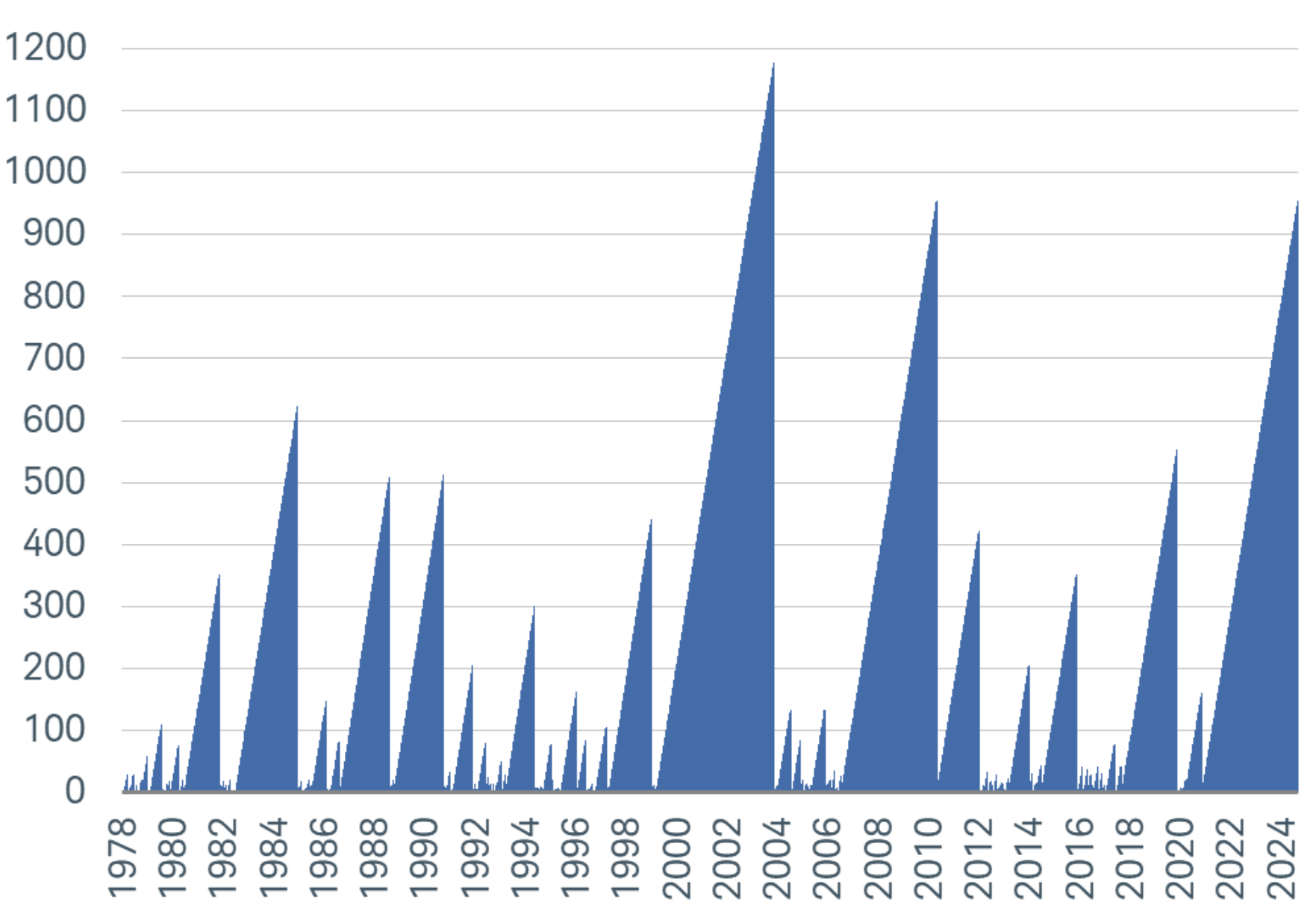

10k Words Equitable Investors September 2025 Record volatility amid an ASX reporting season delivering another year of flat-to-negative growth. Australian GDP in the June quarter compared well with peers but on a per capita basis things have been going backwards since Q4 2022. Things have been going more backwards for the Alcohol & Tobacco space (and related ASX listings). Back on equities, large cap and momentum were leading factors in the US over the past 12 months (the AI theme having a bit to do with that) but in Australia it is small caps out in front. US smalls - and also bonds - remain in lengthy drawdown periods. Looking more broadly, delinquencies in the US office CMBS sector have been on the rise, while a large portion of private equity buy-out holdings are in breach of leverage caps. Finally, take a look at the price of diamonds falling away. September 2025 Edition

ASX reporting season featured record result-day share price volatility

Source: Wilsons Three years of flat-to-negative earnings growth in Australia projected to end in FY2026

Source: Wilsons Advisory Australian gross operating profits: mining industry v the rest

Source: IFM Investors, ABS June 2025 quarter GDP growth - quarterly change annualised

Source: Macrobond, AMP Real & real per capita growth in GDP

Source: IFM Investors Australian household spending - alcohol & tobacco has been in decline for ~24 months

Source: Evans & Partners Performance of ASX-listed alcohol stocks

Source: Koyfin, Equitable Investors US factor ETF performance / S&P 500 ETF performance over past 12 months

Source: Koyfin ETFs tell a bit of a different story on the ASX over the past 12 months

Source: Equitable Investors AI "Picks & Shovels" Equal Weight Index - rebalanced monthly

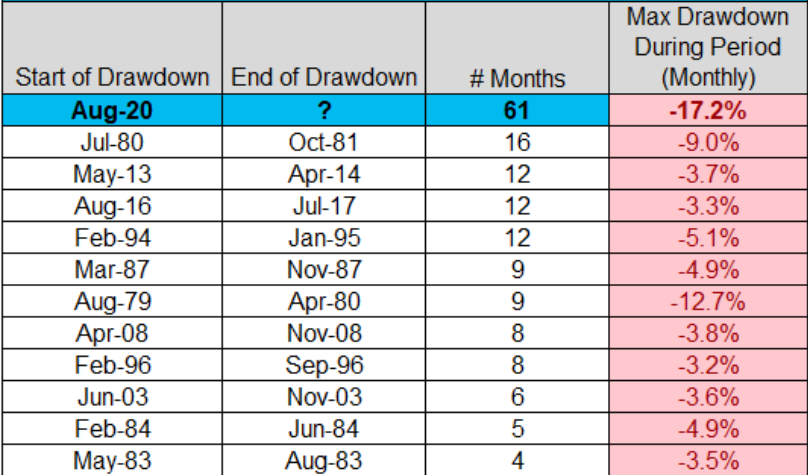

Source: Bespoke Number of says since Russell 2000 (US small cap index) last surpassed its prior high (drawdown)

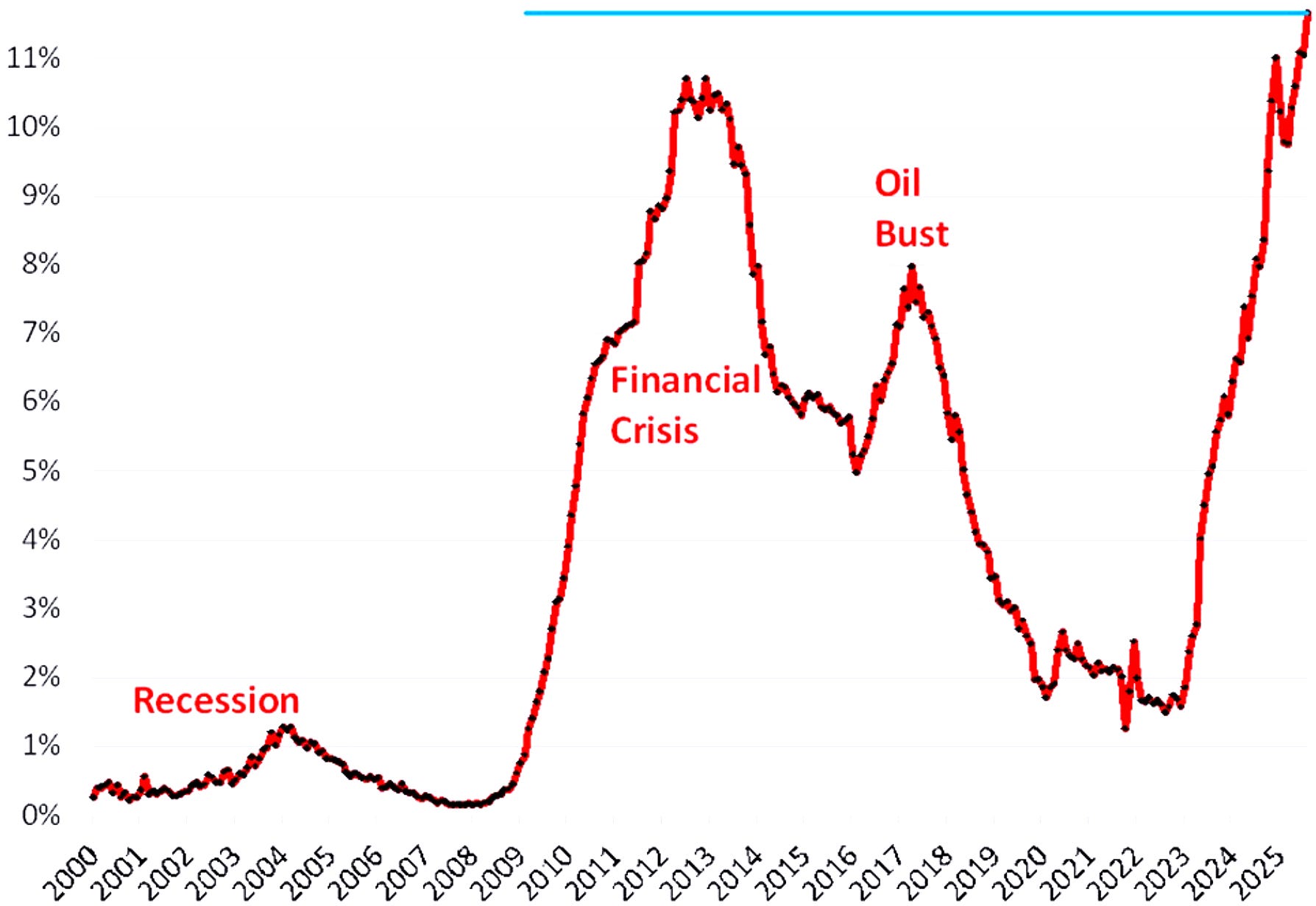

Source: Charles Schwab Number of months since Bloomberg Aggregate Bond Index last surpassed its prior high (drawdown)

Source: Creative Planning, @CharlieBilello US Office CMBS delinquency rate (%)

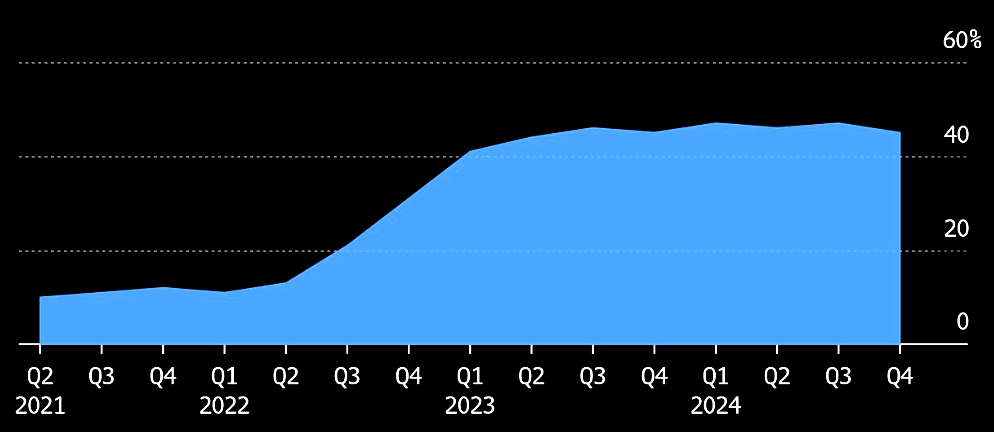

Source: Trepp, The Kobeissi Letter % of private equity buyout holdings in breach of leverage caps

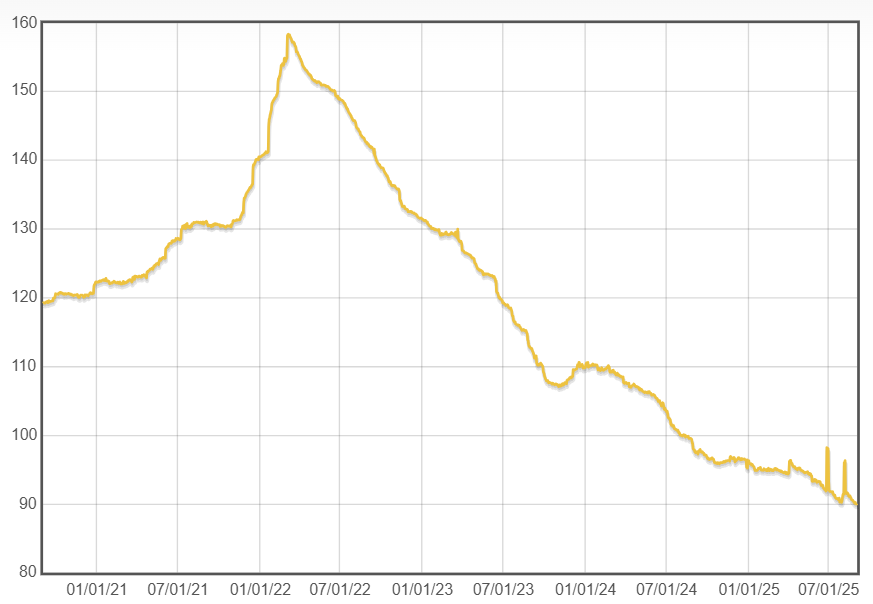

Source: MSCI, Bloomberg via Advisor Perspectives Diamond prices in decline

Source: IDEX Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

15 Sep 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| iPartners Property Credit Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| iPartners Bond Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Partners Group Global Value Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Pendal Sustainable Balanced Fund - Class R | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| Laser Beam Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

12 Sep 2025 - Turning Turbulence into Triumph: Two Stocks Mastering Market Themes

|

Turning Turbulence into Triumph: Two Stocks Mastering Market Themes Alphinity Investment Management June 2025 6 minutes read time |

|

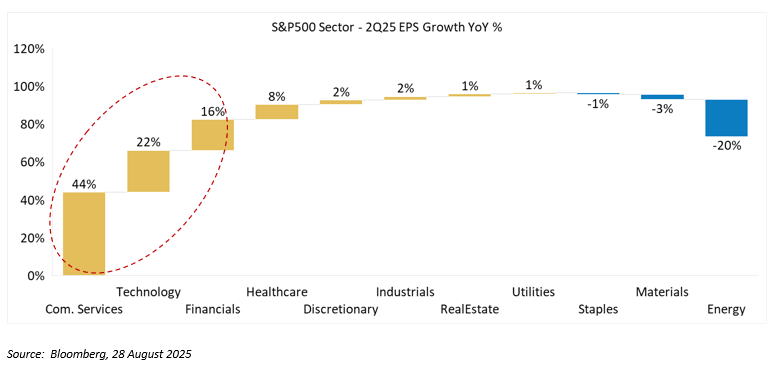

Five powerful themes are reshaping the investment landscape, creating winners and losers across global markets. The AI revolution stands as the defining narrative, driving fundamental shifts in capital allocation and valuation frameworks. Lower interest rate expectations and regulatory reform have reignited investor confidence, while Trump's tariff agenda injects supply chain uncertainty and continues to impact both corporate margins and consumer spending power. Meanwhile, geopolitical tensions fuel unprecedented defence spending and strategic consolidation as companies position for an increasingly fragmented world. These converging forces created a tale of two markets during 2Q25 earnings season. On the surface, the numbers appeared robust: over 80% of US companies beat earnings expectations, guidance upgrades accelerated to double the 1Q25 rate, and consensus pushed earnings growth forecasts to an impressive 11% and 13% for 2025 and 2026 respectively. Yet beneath this veneer of strength lay a more complex reality. Earnings growth concentrated heavily within just three sectors and performance diverged sharply among industry peers. This bifurcated landscape has created an unforgiving environment where execution excellence separates winners from casualties. Companies skilfully navigating these themes are thriving, while those stumbling face harsh consequences. Two high quality companies with underappreciated earnings potential that exemplify this successful navigation are Amphenol and O'Reilly Automotive, transforming market complexity into competitive advantages and turning potential headwinds into powerful tailwinds through exceptional strategic execution. US 2Q25 Reporting Season - Strong overall growth of 12%, but largely driven by 3 sectors

Five Themes Defining Corporate PerformanceThe recent reporting season once again highlighted these five powerful themes that continue to reshape the investment landscape and define how companies are adapting to the current environment. Below, we examine how these themes have evolved and intensified through the latest earnings cycle:

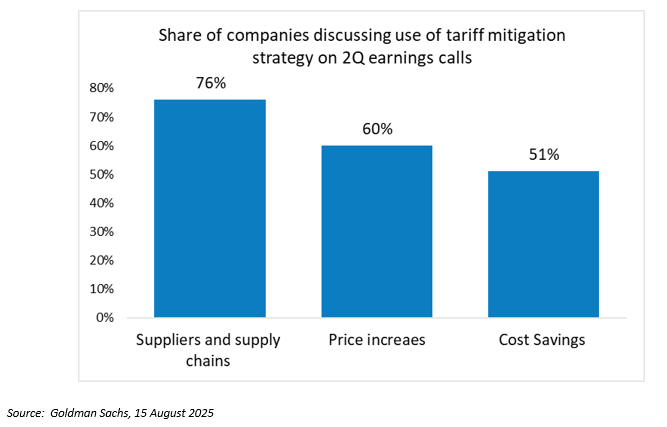

Increased confidence in corporates' ability to mitigate tariff headwinds

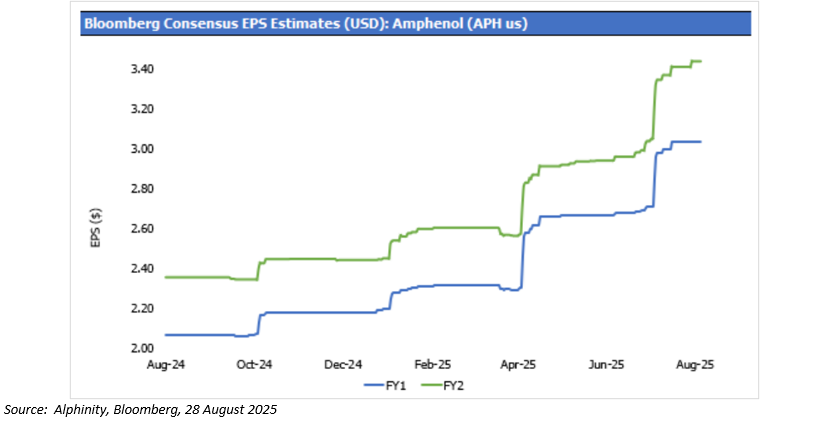

Quality in Action: Two Exceptional OperatorAmong the winners emerging from this challenging environment, two companies showcase exceptional strategic positioning across multiple themes. Amphenol and O'Reilly Automotive have not merely survived current market forces--they have actively leveraged them to strengthen their competitive moats, accelerate growth, and deliver consistent outperformance through disciplined execution and opportunistic capital deployment. Amphenol: Wired for AI, Armed for Defence, Primed for M&AAmphenol, a leading connector and fibre optics supplier with 12% global market share, sits perfectly at the intersection of three key themes: AI infrastructure buildout, defence spending acceleration, and strategic M&A activity. AI Content Multiplication Amphenol expects to grow at 2x their end markets due to significant content uplift in AI applications. Unlike traditional data centres , AI requires every chip to be interconnected, creating multiples of connections. This structural advantage delivered exceptional Q2 2025 results--revenue beat expectations by 11% and EPS by 21%. Management noted AI customers "continue to spend with no one slowing down investments." Strategic M&A Execution The $10.5 billion CCS acquisition exemplifies Amphenol's disciplined M&A approach in today's active dealmaking environment. Acquired at a reasonable 11x EBITDA, CCS brings $3.6 billion in expected 2025 sales at 26% EBITDA margins. The deal adds complementary fibre capabilities with minimal overlap to existing operations. With leverage remaining under 2x and management's proven integration track record (13% annual revenue growth over five years, 2x their end markets), this represents smart capital deployment in an M&A-friendly market. Defence Expansion The $300 million acquisition of Narda-MITEQ, a leading provider of active RF and microwave components, expands Amphenol's existing defence exposure. This positioning capitalizes on unprecedented global defence spending increases driven by geopolitical tensions and deglobalization trends. Structural Margin Expansion Management raised conversion margin targets from 25% to 30%, citing better pricing power as technology complexity increases. This adds a new earnings growth lever beyond their traditional organic growth, M&A, and buyback strategy. Attractive Valuation Trading at 30x CY26 EPS versus the S&P 500's 21x, Amphenol's market premium sits at the lower end of its historical 40-85% range despite earnings growing 40-50% above average years. The combination of AI content multiplication, strategic M&A execution, and defence market expansion positions Amphenol as a clear beneficiary of three of today's dominant investment themes. Amphenol - Strong earnings upgrade cycle underpinned by multiple growth levers and pricing power

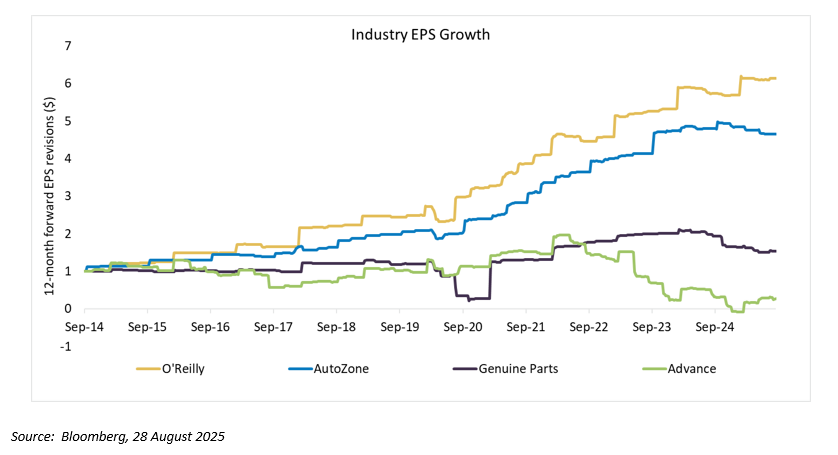

O'Reilly's Wide Consumer Moat Meets Supply Chain MasteryO'Reilly demonstrates how best-in-class operators are able to turn challenging conditions into competitive advantages. As a leader in the automotive aftermarket industry with 6,200 stores, the company benefits from non-discretionary vehicle maintenance demand while demonstrating superior tariff navigation. A Resilient Industry The automotive aftermarket's structural advantages shine during uncertainty. Vehicle repairs remain essential regardless of economic pressures, with aging U.S. vehicle fleets and rising light truck penetration driving sustained demand. O'Reilly's dual-market strategy serves both DIY consumers (52% of sales) and professional mechanics (48% of sales), providing diversified exposure to recession-resistant spending. Tariff Management Excellence With 20-30% of costs sourced from China and 10-15% from Mexico, O'Reilly faces meaningful tariff exposure but has demonstrated exceptional pass-through ability. Same-SKU inflation accelerated from 0.5% in Q1 to 1.5% in Q2 2025, with management seeing "substantially more" pricing power potential than currently embedded in guidance. Solid Execution O'Reilly delivered strong second-quarter 2025 earnings, growing comparative sales by 4.1% (beating expectations of 3.7%) and expanding its gross margin by 70 basis points. Despite elevated SG&A spending, management raised full-year comparative growth guidance to 3-4.5% from prior 2-4%, suggesting conservative positioning with upside potential. Widening Competitive Moat O'Reilly's unrivalled distribution network--30 distribution centres and 385 hub stores enabling 5-night weekly delivery--provides superior service versus struggling competitors. With NAPA facing operational challenges and Advance Auto Parts in financial restructuring, O'Reilly is well positioned to continue capturing market share in a consolidating industry. The combination of defensive demand, tariff-induced pricing tailwinds, and market share opportunities positions O'Reilly for sustained outperformance as macro headwinds become competitive advantages. O'Reilly enjoying superior earnings growth relative to key peers over the last decade

Navigating Complexity Through Strategic SelectionToday's investment landscape rewards execution excellence while punishing missteps, as these five forces--AI implementation, defence modernisation, tariff adaptation, strategic M&A, and consumer resilience--create clear winners and losers even within sectors. Success requires identifying companies that transform these forces into competitive advantages. Amphenol capitalizes on AI content multiplication and executes disciplined defence acquisitions, while O'Reilly turns tariff headwinds and consumer pressure into earnings and market share gains. As earnings dispersion widens and market patience diminishes, broad sector exposure is insufficient. Investors must focus on best-in-class operators with proven execution capabilities and structural competitive advantages. In this bifurcated environment, owning quality companies like Amphenol and O'Reilly provides both defensive characteristics and offensive growth potential, positioning portfolios to benefit from, rather than merely endure, the forces reshaping the global economy. Editorial Note: |

|

Funds operated by this manager: Alphinity Australian Share Fund , Alphinity Concentrated Australian Share Fund , Alphinity Sustainable Share Fund , Alphinity Global Equity Fund , Alphinity Global Sustainable Equity Fund This material has been prepared by Alphinity Investment Management ABN 12 140 833 709 AFSL 356 895 (Alphinity). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed. |