News

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund has risen by +9.92% over the past 12 months. Since inception in February 2009, the fund has returned +13.12% per annum, an outperformance of +3.34% relative to the ASX 200 Total Return...

Read more...

Performance Report: Cyan C3G Fund

The Cyan C3G Fund rose by 3.28% in April, outperforming the ASX Small Ordinaries Total Return Index by 6.34%. Top contributors during the month included Vinyl, Wisetech, Readcloud, Alcidion, Touch Ventures and Acusensus, while Playside,...

Read more...

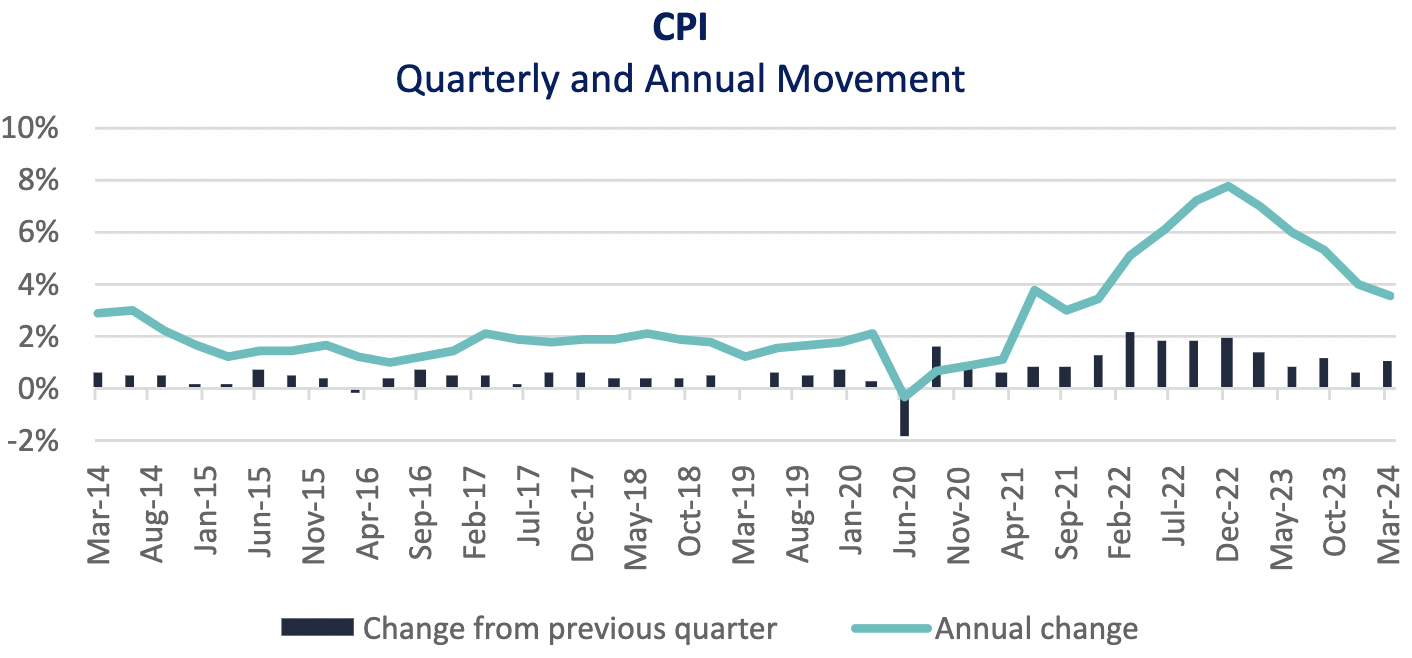

Quarterly consumer price index update

The long-awaited quarterly consumer price index (CPI) figure was reported weeks ago. Over the March quarter, CPI rose by 1.0 per cent, which follows the previous 0.6 per cent December quarter increase.

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +0.74% in April. Since inception in April 2018, the fund has returned +11.83% per annum, an outperformance of +5.3% relative to the RBA Cash Rate + 5% benchmark which has returned +6.53% on an annualised...

Read more...

JH Explorer in Charleston: Power cabling the energy transition

During a research trip to the US, Portfolio Manager Tal Lomnitzer spends some time at a high-end cable manufacturer - a company that is vital for the transmission of clean energy from production to consumption points.

Read more...

Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

The Skerryvore Global Emerging Markets All-Cap Equity Fund returned -0.39% in April. Since inception in August 2021, the fund has returned +4.73% per annum, an outperformance of +4.97% relative to the MSCI Emerging Markets (MMEF) AUD...

Read more...

Magellan Global Quarterly Update - April 2024

Nikki Thomas and Arvid Streimann discuss key themes impacting the markets and providing opportunities for investors. Arvid discusses his recent trip to Washington which provided valuable insights into the future growth of AI innovation and adoption.

Read more...

Performance Report: Bennelong Long Short Equity Fund

The Bennelong Long Short Equity Fund rose by +1.57% in April, outperforming the ASX 200 Total Return benchmark by +4.51%. Since inception in February 2002, the fund has returned +12.61% per annum, an outperformance of +4.49% relative to...

Read more...

Performance Report: Collins St Value Fund

The Collins St Value Fund rose by +2.31% in April, outperforming the ASX 200 Total Return benchmark by +5.25%. Since inception in February 2016, the fund has returned +13.9% per annum, an outperformance of +4.22% relative to the benchmark...

Read more...

Manager Insights | Euree Asset Management

Chris Gosselin, CEO of FundMonitors.com, speaks with Winston Sammut, Director Property at Euree Asset Management.

Read more...