News

26 Mar 2026 - Performance Report: DAFM Digital Income Fund (Digital Income Class)

[Current Manager Report if available]

26 Mar 2026 - Becoming wary of software

|

Becoming wary of software Challenger Investment Management March 2026 (9-minute read) Many of you will have seen news over the past few weeks regarding the US Private Credit sector's exposure to software and flow on concerns regarding the impact of AI on the software businesses. Investor concerns have centred around those managers who are most exposed with most press articles focussed on Blue Owl Capital as amongst the largest players in the private credit market they have the highest exposure.

Turning to the domestic private credit market we think the following is important:

The constant challenge for investors which is especially true in this environment is that the assessment of the risk of a fund is not just about the assets, it's not just about the manager and not just about their governance practices. A major determinant of outcomes will be how other investors respond. This is a much tougher proposition for investors to assess - size and scale matters here, access to institutional capital, transparency and approach to governance. A private credit firm with one open ended fund, poor valuation discipline, external leverage and lack of scale is far more exposed than the alternative. Challenger IM Credit Income Fund , Challenger IM Multi-Sector Private Lending Fund For Adviser & Investors Only Disclaimer: This material has been prepared by Challenger Investment Partners Limited (Challenger Investment Management or Challenger), ABN 29 092 382 842, AFSL 329 828. This document does not relate to any financial or investment product or service and does not constitute or form part of any offer to sell, or any solicitation of any offer to subscribe or interests and the information provided is intended to be general in nature only. This should not form the basis of, or be relied upon for the purpose of, any investment decision. This document is not available to retail investors as defined under local laws. This document has been prepared without taking into account any person's objectives, financial situation or needs. Any person receiving the information in this document should consider the appropriateness of the information, in light of their own objectives, financial situation or needs before acting. This document is provided to you on the basis that it should not be relied upon for any purpose other than information and discussion. The document has not been independently verified. No reliance may be placed for any purpose on the document or its accuracy, fairness, correctness, or completeness. Neither Challenger Investment Management nor any of its related bodies corporates, associates and employees shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of the document or otherwise in connection with the presentation. |

25 Mar 2026 - Performance Report: DS Capital Growth Fund

[Current Manager Report if available]

25 Mar 2026 - Emerging Markets: How AI concerns are impacting India

|

Emerging Markets: How AI concerns are impacting India Pendal March 2026 (5 minutes read time) |

|

Fears that rapid advances in artificial intelligence could slow global IT spending have weakened investor confidence in Indian software stocks. Pendal's Global Emerging Markets Opportunities team investigates the implications for India's growth and current account balance. THE explosion in capability of AI models in recent months has led some equity market participants to become more cautious about the outlook for various service sector industries, leading to selloffs in sectors from software to financial planning. As investors who approach the asset-class primarily through top-down, country-level developments, the GEMO team has been thinking about what this might mean for India. India is one of a group of emerging markets that tend to run current account deficits. "These are countries that have significant latent domestic demand but where, for various historical, geographical or institutional reasons, domestic production falls short. These markets tend to have higher beta to global liquidity and risk appetite," says James Syme, senior fund manager, JOHCM. "Most pertinently for India, the growth cycles of these countries tend to be constrained by inflation and external deficits, with both vulnerabilities reflecting demand running too far ahead of supply." Since the end of 2010, India's current account deficit has averaged 1.7 per cent of GDP, although the maximum deficit was 5.1 per cent of GDP. The structure of the current account balance has developed through time, and changed with India's economic cycle, but some components remain structurally important. In 2025, India ran a deficit in non-oil goods of US$189 billion (4.9 per cent of GDP). Net oil imports were US$122 billion (3.2 per cent of GDP). The resultant trade deficit of US$311 billion (8 per cent of GDP) was substantially offset by a net positive services balance of US$210 billion (5.4 per cent of GDP). Notably, the surplus in IT services was US$227 billion (5.9 per cent of GDP). India also ran a positive income balance of US$85 billion (2.2 per cent of GDP), for an overall current account deficit of US$17 billion (0.4 per cent of GDP). Syme says this relationship between IT service exports and oil imports is key for India's economy, and the two have grown together. In fiscal year 2019, net IT service exports were US$85 billion, and oil imports were US$93.9 billion. "The varying cycles in global IT service spending and the oil price are key for the health of the Indian economy," explains Syme. At a time of higher oil prices, what does the downturn in sentiment towards software and IT service stocks mean for India? In the first two months of 2026, the MSCI India IT Index has fallen over 20 per cent in USD terms. "This is concerning, because the aggregate revenue of India's listed IT companies has a high correlation with the economy's IT service exports," says Syme. If the negative outcome that stocks are pricing in comes to pass, particularly with higher oil prices, India's growth may be constrained by the current account balance. "However, it is important to note that the 12-month forward consensus estimates for both the revenues and profits of the constituents of MSCI India IT Index have increased by 3.4 per cent year to date," notes Syme. "This steady growth in the fundamental outlook for these companies suggests both opportunity in the sector, where we remain overweight, and ongoing support for the Indian economic growth story, although we remain underweight the country on valuation grounds. "We do not feel that share price moves alone constitute a macro-level signal for India at this time." |

|

Funds operated by this manager: Pendal MicroCap Opportunities Fund , Pendal Global Select Fund - Class R , Pendal Sustainable Australian Fixed Interest Fund - Class R , Pendal Focus Australian Share Fund , Pendal Horizon Sustainable Australian Share Fund , Regnan Credit Impact Trust Fund , Pendal Sustainable Australian Share Fund , Pendal Sustainable Balanced Fund - Class R , Pendal Multi-Asset Target Return Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

24 Mar 2026 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]

24 Mar 2026 - Australian Secure Capital Fund - Property Update

|

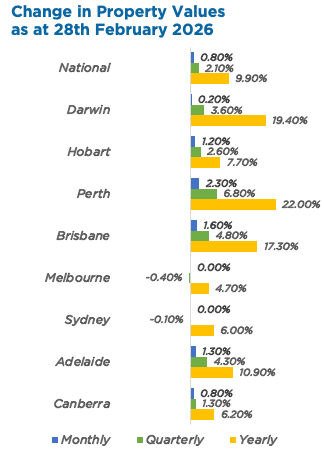

Australian Secure Capital Fund - Property Update Australian Secure Capital Fund March 2026 (1-minute read) February was another strong month for Australian property values, posting a national rise of 0.8% for the second consecutive month. Perth (+2.3%) again led the way with a second straight monthly rise of greater than 2%, adding more than $22,500 to the median dwelling value over the month. Similarly, Brisbane (+1.6%) and Adelaide (+1.3%) again saw monthly increases of greater than 1%. Conversely, values in Melbourne and Sydney were flat over February, with both cities notching slight rolling quarterly decreases of -0.4% and -0.1%, respectively. As a result, regional areas continue to outperform the capital cities, rising by 1.1% month-on-month, compared to 0.6% for the capitals. Nationally, rents increased 1.7% over the three months to February 2026, denoting the highest rolling quarterly increase since April 2025.

Source: Cotality HVI, 02 March 2026 February Edition Funds operated by this manager: ASCF Select Income Fund , ASCF High Yield Fund , ASCF Premium Capital Fund , ASCF Private Fund

|

23 Mar 2026 - Performance Report: Bennelong Twenty20 Australian Equities Fund

[Current Manager Report if available]

February due to reporting season, persistent AI disruption

fears and ongoing geopolitical tension. (2-minute read)

23 Mar 2026 - Glenmore Asset Management - Market Commentary

|

Market Commentary - February Glenmore Asset Management March 2026 (2-minute read) The volatility of the last few months was amplified in February due to reporting season, persistent AI disruption fears and ongoing geopolitical tensions. Domestically, large caps materially outperformed small/mid caps, resulting in the All Ordinaries Accumulation Index rising +3.3% compared to a -2.6% decline in the ASX Small Ordinaries Accumulation Index. The ASX50 had an extremely strong month, increasing by +7.9%, whilst at the smaller end, the Small Ords Industrials declined -4.5%. Capital light businesses, such as software and technology companies fell sharply due to investor fears around disruption from AI, whilst resources and mining services outperformed. In comparing the fund's performance versus the benchmark in February, it should be noted the fund has a strong small/mid cap focus. Over the long term, there is clear evidence that these companies deliver superior returns to large caps, however during periods of investor risk aversion (such as the current environment where the RBA is raising interest rates to combat inflation), investor funds typically move out of small caps to the perceived safety of large cap companies. In the US, the tech heavy NASDAQ was weighed down by similar factors, resulting in a -3.4% decline in the month, underperforming the S&P 500 which fell -0.9%. Outside of the US, the Euro Stoxx 50 and FTSE 100 maintained their recent momentum, rising +3.2% and +6.7%, respectively. As we have discussed, the expectation of further RBA rate hikes has continued to drive a rotation back into large caps. Bluechip names rebounded in February, including CBA (+17%), NAB (+13%), BHP (+16%) and Woolworths (+16%). Whilst the market continues to expect 1-2 more RBA rate hikes over the next 12 months, past cycles have shown that the underperformance of small/mid caps tends to bottom well before the end of a rate hiking cycle. In bond markets, the US 10-year bond yield recorded a sharp decline, falling -30 basis points (bp) to 3.94%, whilst its Australian counterpart fell -16bp to 4.65%. The Australian dollar continued to rise, increasing +2.2% to US$0.71, implying an increase of 1.5 cents. Funds operated by this manager: |

20 Mar 2026 - Hedge Clippings |20 March 2026

|

|

|

|

Hedge Clippings | 20 March 2026 It's been a volatile week for markets, interest rates, and above all, the politics of war. In Australia, the RBA raised rates for the second month in a row after cutting three times last year, including as recently as August. That suggests the Board may have moved too far, too soon on the way down, and there is now a real risk it may be jumping too quickly on the way back up. With inflation still stubborn and global uncertainty rising, and inflation with it, the RBA was clearly stuck between a rock and a hard place, which was reflected in the narrow 5-4 vote in favour of a hike. Hedge Clippings' experts Nick Chaplin and Renny Ellis, who argued against last year's cuts, were equally emphatic this week when we spoke to them that the Board could well have - and should have - held their nerve. With the next meeting only five or six weeks away, there was a strong case for waiting, and allowing February's increase more time to work through the economy, for February's inflation data to land, and for the fallout from the closure of the Strait of Hormuz -- and the likely duration of the conflict -- to become clearer. As Jerome Powell said after this week's Fed meeting when they kept rates steady, "we just don't know what comes next". Fair point. Right now, neither do markets, central banks, nor anyone trying to price risk with a straight face. And for that, investors can once again send a silent thank you (or maybe some other message) in Donald Trump's direction. News | Insights Expert Analysis of the RBA's March 17 Rate Decision | Seed Funds Management & Arculus Funds Management 10k Words | Equitable Investors February 2026 Performance News Bennelong Emerging Companies Fund Glenmore Australian Equities Fund Seed Funds Management Financial Income Fund Insync Global Capital Aware Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

20 Mar 2026 - Performance Report: Cyan C3G Fund

[Current Manager Report if available]