NEWS

16 Aug 2019 - Hedge Clippings | 16 August 2019

|

||||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

16 Aug 2019 - Fund Review: Bennelong Kardinia Absolute Return Fund July 2019

BENNELONG KARDINIA ABSOLUTE RETURN FUND

Attached is our most recently updated Fund Review. You are also able to view the Fund's Profile.

- The Fund is long biased, research driven, active equity long/short strategy investing in listed ASX companies with over ten-year track record.

- The Fund has significantly outperformed the ASX200 Accumulation Index since its inception in May 2006 and also has significantly lower risk KPIs. The Fund has an annualised return of 9.26% p.a. with a volatility of 7.03%, compared to the ASX200 Accumulation's return of 6.54% p.a. with a volatility of 13.19%.

- The Fund also has a strong focus on capital protection in negative markets. Portfolio Managers Mark Burgess and Kristiaan Rehder have significant market experience, while Bennelong Funds Management provide infrastructure, operational, compliance and distribution capabilities.

For further details on the Fund, please do not hesitate to contact us.

15 Aug 2019 - Commonwealth Bank's FY19 Result: Trench Warfare Ahead

15 Aug 2019 - Fund Review: Bennelong Twenty20 Australian Equities Fund July 2019

BENNELONG TWENTY20 AUSTRALIAN EQUITIES FUND

Attached is our most recently updated Fund Review on the Bennelong Twenty20 Australian Equities Fund.

- The Bennelong Twenty20 Australian Equities Fund invests in ASX listed stocks, combining an indexed position in the Top 20 stocks with an actively managed portfolio of stocks outside the Top 20. Construction of the ex-top 20 portfolio is fundamental, bottom-up, core investment style, biased to quality stocks, with a structured risk management approach.

- Mark East, the Fund's Chief Investment Officer, and Keith Kwang, Director of Quantitative Research have over 50 years combined market experience. Bennelong Funds Management (BFM) provides the investment manager, Bennelong Australian Equity Partners (BAEP) with infrastructure, operational, compliance and distribution services.

For further details on the Fund, please do not hesitate to contact us.

14 Aug 2019 - Performance Report: Glenmore Australian Equities Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The main driver of identifying potential investments will be bottom up company analysis, however macro-economic conditions will be considered as part of the investment thesis for each stock. |

| Manager Comments | Top contributors included Phoslock Environment Technologies, Magellan Financial Group, Dicker Data, People Infrastructure, AP Eagers, Alliance Aviation Services and Fiducian Group. Key detractors included Stanmore Coal and Jumbo Interactive. Glenmore noted they were surprised by the magnitude of the rebound in 2019. They believe the most likely driver of the rebound is the view that we will have continued low inflation and low interest rates for the foreseeable future. Glenmore's approach in this environment has been to sell or trim holdings where they believe valuations have become stretched and remain very selective with regards to the quality of businesses they are invested in. |

| More Information |

14 Aug 2019 - Performance Report: NWQ Global Markets Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | This is achieved through active allocations to a select number of liquid alternative managers that employ a variety of strategies. The Fund places emphasis on managers who demonstrate a rigorous and repeatable investment process that has delivered a strong track record. |

| Manager Comments | The portfolio comprises funds that invest in FX (47.3%), global macro (32.7%) and managed futures (32.7%). The contribution from each strategy to the portfolio's July return (before fees) was +2.58%, -2.03% and +2.69% respectively. |

| More Information |

13 Aug 2019 - Performance Report: Cyan C3G Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Cyan C3G Fund is based on the investment philosophy which can be defined as a comprehensive, clear and considered process focused on delivering growth. These are identified through stringent filter criteria and a rigorous research process. The Manager uses a proprietary stock filter in order to eliminate a large proportion of investments due to both internal characteristics (such as gearing levels or cash flow) and external characteristics (such as exposure to commodity prices or customer concentration). Typically, the Fund looks for businesses that are one or more of: a) under researched, b) fundamentally undervalued, c) have a catalyst for re-rating. The Manager seeks to achieve this investment outcome by actively managing a portfolio of Australian listed securities. When the opportunity to invest in suitable securities cannot be found, the manager may reduce the level of equities exposure and accumulate a defensive cash position. Whilst it is the company's intention, there is no guarantee that any distributions or returns will be declared, or that if declared, the amount of any returns will remain constant or increase over time. The Fund does not invest in derivatives and does not use debt to leverage the Fund's performance. However, companies in which the Fund invests may be leveraged. |

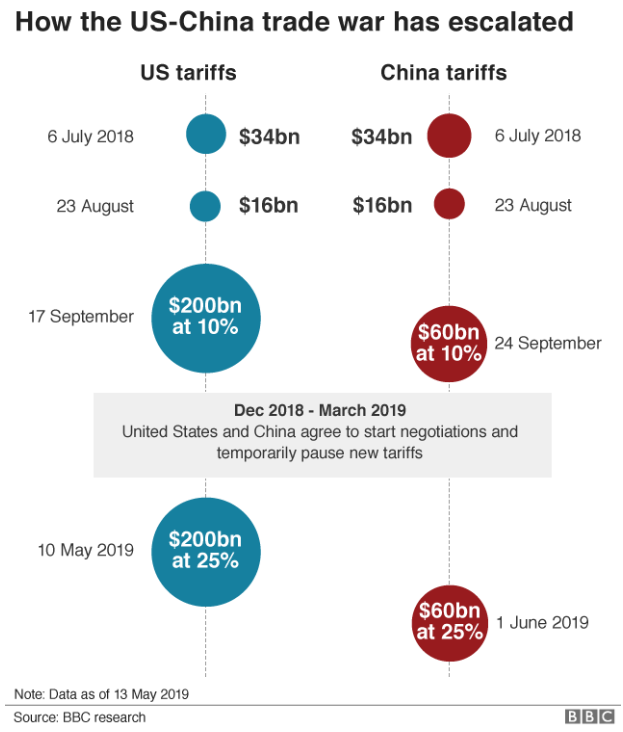

| Manager Comments | Top contributors during the month included Alcidion, Quickfee, Readcloud, Atomos and PSC Insurance. Cyan noted very few of the Fund's holdings performed poorly in July. Cyan believe ongoing trade wars and associated currency fluctuations are likely to continue to drive sentiment in the short term. They noted that, rather than trying to pick short-term trading directions, they continue to invest on a stock specific basis through a well-diversified portfolio of around 30 companies. Cyan expect the market to focus more fully on individual company performance rather than macro events and short-term sentiment during reporting season. |

| More Information |

13 Aug 2019 - Fund Review: Bennelong Long Short Equity Fund July 2019

BENNELONG LONG SHORT EQUITY FUND

Attached is our most recently updated Fund Review on the Bennelong Long Short Equity Fund.

- The Fund is a research driven, market and sector neutral, "pairs" trading strategy investing primarily in large-caps from the ASX/S&P100 Index, with over 16-years' track record and an annualised returns of 15.17%.

- The consistent returns across the investment history highlight the Fund's ability to provide positive returns in volatile and negative markets and significantly outperform the broader market. The Fund's Sharpe Ratio and Sortino Ratio are 0.91 and 1.48 respectively.

For further details on the Fund, please do not hesitate to contact us.

12 Aug 2019 - Performance Report: Bennelong Kardinia Absolute Return Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund's discretionary investment strategy commences with a macro view of the economy and direction to establish the portfolio's desired market exposure. Following this detailed sector and company research is gathered from knowledge of the individual stocks in the Fund's universe, with widespread use of broker research. Company visits, presentations and discussions with management at CEO and CFO level are used wherever possible to assess management quality across a range of criteria. Detailed analysis of company valuations using financial statements and forecasts, particularly focusing on free cash flow, is conducted. Technical analysis is used to validate the Manager's fundamental research and valuations and to manage market timing. A significant portion of the Fund's overall performance can be attributed to the attention and importance given to the macro economic outlook and the ability and willingness to adjust the Fund's market risk. |

| Manager Comments | July's return was driven by gold, industrials and key healthcare stocks. Top contributors included A2 Milk, Evolution, Northern Star, Magellan Financial Group, CSL and Polynovo. Detractors included Next Science, Nearmap, Rio Tinto and Audinate Group. The largest detractors were a short position in Share Price Index Futures and the individual short book. Net equity market exposure was increased from 24.9% to 40.5% (73.3% long and 32.8% short), with the key changes being a new long position in Westpac and increased weightings in Commonwealth Bank, James Hardie, Xero, A2 Milk and Macquarie Group. This was partly offset by the sale of NAB and Next Science and four new individual stock shorts in the financials and resources sectors. |

| More Information |

9 Aug 2019 - Hedge Clippings | 09 August 2019

|

|||||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|