NEWS

29 Nov 2021 - The benefits of scale for private debt investors

|

The benefits of scale for private debt investors Metrics Credit Partners 22 November 2021 In private debt funds - unlike in boutique equity funds - there is a big payoff for investors from having a bigger loan book. Scale makes private debt providers more relevant to borrowers and investors, says Metrics Managing Partner Andrew Lockhart. Conventional wisdom says that by staying small, boutique managers can deliver superior returns. They are nimble and can move in and out of stocks without the burden of having to invest, even when conditions are not favourable. But what is true of equity managers does not hold for private debt providers. Increased scale makes a private debt manager more relevant to both the borrowers and the investors and provides more consistent returns. In this article we look at the reasons why, using the Metrics Credit Partners experience to illustrate the benefits. Metrics was established ten years ago, a pioneer in non-bank lending in Australia, by a team of three partners who worked at NAB and who had extensive experience in lending and portfolio risk management. Since then, Metrics has grown to a team of ~100 people with AUM of ~$10 billion. Metrics has not grown just for the sake of getting bigger, but because there are clear benefits for investors. Having scale makes Metrics more relevant to borrowers because access to non-bank debt finance can help them grow. With increased funding, Metrics can lend larger volumes to clients to help realise their plans. A smaller lender may not always have the capacity to match the needs of some borrowers and they don't have the certainty of capital that a larger lender provides. Metrics is not a bank. It is a minnow compared to the balance sheets of any of the Big Four. But it does not have their cost structure or rigid business practices, either. As one of the largest non-bank providers of debt finance to Australian businesses Metrics has the capability to match the needs of borrowers in a way that banks cannot. There are regulatory restrictions which impose a higher level of capital to be retained on balance sheets for banks that lend to business compared with lending for consumer purposes where the loan is secured against a residential property. This reduces the returns that a bank can generate from lending to companies which reduces their appetite to do so. But Metrics is focused on business and real estate lending. It has a highly skilled and a professional team with a deep understanding of each borrower, which means they can assess risk and price it accordingly. Through the recent wave of lockdowns that began in June 2021 Metrics again demonstrated its commitment to business borrowers. In the September quarter alone, Metrics financed in excess of $1.2 billion. By December, as the economy re-emerges from lockdowns, Metrics expects to finalise another $2 billion. It's unlikely any of our non-bank fund competitors can provide this volume of finance to Australian companies. All through this period Metrics has further added depth and breadth of expertise, increasing its team ~100 people. By resourcing teams in origination and risk assessment it has a larger more diverse team to consider more lending opportunities. That in turn delivers more attractive returns and capital preservation for investors. Contrast that with small private debt providers who claim to have the same benefits of a boutique equity investor. Their small scale means they can only do a handful of loans for a small number of clients before they reach capacity. That limits the potential of their borrowers. It also limits the managers ability to create diversified portfolios for their investors, increasing concentration and single large counterparty credit risk. The big global credit players setting up shop in Australia have a similar scale problem. On the face of it they have huge resources and big, well-known brand names to offer the local market. But the reality is that their local teams are small and lack the capacity to originate many good lending opportunities. When they do find one, the credit decisions are usually taken offshore, away from the relationships and understanding of local nuances that a larger, local private debt manager like Metrics provides. Being more relevant to borrowers has several important benefits for investors. Scale provides access to better deal flow, giving Metrics a better understanding of the market and the ability to focus on the best quality lending opportunities coming through. Having the ability to lend in larger size also means more negotiating power when determining the terms and conditions on the financing. It allows Metrics to tap sources of income - such as origination fees - that those smaller players cannot, generating better returns for investors. Scale also provides important risk management capabilities for investors, by allowing diversification across a wide range of industries and sectors. A larger portfolio of loans, where each exposure represents less than 1% of the total, provides cover against any one loan having an outsized impact on the returns to investors. This is also important in preserving investor capital, reducing concentration risk from any one borrower. Scale is only useful when it delivers better outcomes for borrowers and investors. Metrics' continued growth and performance reinforces this. This year alone, both listed funds have undertaken significant capital raisings to expand their capacity and continue to trade at a premium to their NAV. New additions to the Metrics suite of funds have and will continue to come to market to ensure those benefits of scale are realised for borrowers and investors alike. Funds operated by this manager: MCP Income Opportunities Trust (ASX: MOT), MCP Master Income Trust (ASX: MXT), Metrics Credit Partners Credit Trust, Metrics Credit Partners Direct Income Fund, Metrics Credit Partners Diversified Australian Senior Loan Fund, Metrics Credit Partners Real Estate Debt Fund, Metrics Credit Partners Secured Private Debt Fund II, Metrics Credit Partners Wholesale Investments Trust |

26 Nov 2021 - Hedge Clippings | 26 November 2021

|

|||||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

26 Nov 2021 - Performance Report: Equitable Investors Dragonfly Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund is an open ended, unlisted unit trust investing predominantly in ASX listed companies. Hybrid, debt & unlisted investments are also considered. The Fund is focused on investing in growing or strategic businesses and generating returns that, to the extent possible, are less dependent on the direction of the broader sharemarket. The Fund may at times change its cash weighting or utilise exchange traded products to manage market risk. Investments will primarily be made in micro-to-mid cap companies listed on the ASX. Larger listed businesses will also be considered for investment but are not expected to meet the manager's investment criteria as regularly as smaller peers. |

| Manager Comments | Equitable Investors noted Dragonfly Fund continued to make advances in the month of October in an environment where top 100 ASX listings and Small Industrials struggled but some elements of the microcap segment found investor demand. Last month the commented that an increase in volatility early in October was reflective more of shifting sentiment than any change in fundamentals. At the time of writing their October performance report, their view is that it is more of the same in November as bond yields remain volatile while investors digest higher inflation numbers and second guess central banks. |

| More Information |

26 Nov 2021 - Fund Review: Bennelong Long Short Equity Fund October 2021

BENNELONG LONG SHORT EQUITY FUND

Attached is our most recently updated Fund Review on the Bennelong Long Short Equity Fund.

- The Fund is a research driven, market and sector neutral, "pairs" trading strategy investing primarily in large-caps from the ASX/S&P100 Index, with over 19-years' track record and an annualised returns of 14.35%.

- The consistent returns across the investment history highlight the Fund's ability to provide positive returns in volatile and negative markets and significantly outperform the broader market. The Fund's Sharpe Ratio and Sortino Ratio are 0.85 and 1.34 respectively.

For further details on the Fund, please do not hesitate to contact us.

The contrarian approach to investing is not a new concept. If you want to generate returns better than the crowd, you need to be different.

26 Nov 2021 - Big and boring - when playing it safe pays off

|

Big and boring - when playing it safe pays off Forager Funds Management 05 November 2021 When it comes to investing, does being boring ever pay off? The contrarian approach to investing is not a new concept. If you want to generate returns better than the crowd, you need to be different. Against the backdrop of a tumultuous past year and a half, the easiest thing was to play it safe in the light of uncertainty. That's exactly what many people did, including some high-profile professional investors who converted their portfolios to cash in March 2020. For us, being agile, open-minded and willing to be contrarian was more important than ever last year. It allowed us to invest in a collection of unloved businesses at once-in-a-lifetime prices. And it paid off. The 2021 financial year was the best on record for Forager across both our Australian Shares Fund and International Shares Fund. That was then, what about now?The current environment reminds me a lot of 2017. We had had a wonderful few years of outperformance leading up to that year, with many of our contrarian investments paying off handsomely. The following two years, however, were our two worst on record. When I reflect on that 2018-2019 period, our biggest mistake was to keep being contrarian simply for the sake of it. I wrote an article at the end of 2017 that identified 10 blue chip stocks that made for a nice defensive portfolio in a generally expensive market. Not only did those 10 stocks perform well over the subsequent year, on average they outperformed our Australian Shares Fund by some 20%. There is a time and place for contrarian bets. And there's a time for playing it safe. Right now, interest rates remain at record lows, stock markets are trading at all-time highs, people are inventing new metrics like revenue multiples to justify absurd prices for growth stocks, inflation is becoming a serious concern and COVID resurgences are weighing on the economic recovery. More importantly, there are very few pockets of undue pessimism. It is time, once again, to be thinking about the benefits of safe and boring. Once again, like 2017, investor obsession with hyper growth and high returns has left some of these stocks neglected. The beauty of being big and boringLet's take a look at two big and boring stocks currently in our Australian Shares Fund: Downer EDI and TPG Telecom. Employing some 52,000 people in Australia and New Zealand, Downer Group is one of the antipodes' largest industrial services companies. Its operations range from maintaining buildings and railway lines through to building roads and runways for the defence force. If that sounds boring, that's the whole point. After a number of slip-ups in recent years, the company has been focussing on making itself as boring as possible. It has been winding down its higher-risk construction business, has offloaded most of its mining services businesses and sold its laundries operations for a tidy sum. By 2024, we estimate 80-90% of revenue will come from government-related entities. This transformation has gone largely unrewarded by investors. Up until its latest results were released in August, the share price was languishing at 2016 levels. We think it can generate an 8-9% cash return from these prices, is committed to sharing most of that cash with shareholders and should be able to generate growth in line with the wider economy. In a world of expensive assets, that adds up to just fine. Telcos out of fashionTPG is earlier in its transformation journey. The original TPG was a popular founder-led business which David Teoh built from the ground up and created a huge amount of shareholder value. His final act was to merge with Vodafone, much to Rod Sims ire. The ACCC Chairman didn't like the impact this merger could have on competition and the deal ended up in the courts. TPG won, the ACCC lost and the combined company is now a significant player with more than five million mobile subscribers and two million fixed broadband subscribers. Teoh has now left the business and the days of rapid growth are well behind TPG. But we think the concerns Sims had about competition suggest a brighter future ahead for the sector. On the fixed side of the business, margins have been compressed by the transition from reselling ADSL to lower margin NBN contracts. From here on, there is upside in potential NBN price cuts and the networks themselves are starting to bypass the NBN with home 5G wireless devices (my household uses one, it's super fast and was the easiest installation I have ever experienced). And in mobile all three large players are talking about a "better" pricing environment, with all of them selling new contracts at better than the current average. Sims won't like that, but it is good news for shareholders. We think all of this adds up to a business that can generate a cash return of roughly 8% on today's market capitalisation. Unlike Downer, we might need to wait a few years while TPG repays some debt, but shareholders should see most of that paid out as dividends from the 2023 financial year. The telco sector is mature, boring and stable, but we will take 8% over most of the opportunities we are seeing today. The lesson: you don't always need to be differentForager's motto is "opportunity in unlikely places". It's an approach that has served us well over the past decade. Despite the odd year of poor performance, our clients are still well ahead of the index since our Australian Fund's inception in 2009. We have learned an important lesson from those difficult years, though. You don't always need to be doing better than the crowd. Keeping it simple is not always easy. Especially when, like us, you have a reputation for being contrarian. To turn to our loyal client base and say "you know how we look for opportunity in unlikely places?". Well, we just bought Downer EDI. That doesn't sit well with how we view ourselves or what our clients have come to expect. And that's what makes it so hard. But we know how important it is. The contrarian's time will come again. And, while we wait, boring stocks like Downer and TPG can give us some perfectly sensible returns. Written by Chief Investment Officer Steve Johnson Funds operated by this manager: Forager Australian Shares Fund (ASX: FOR), Forager International Shares Fund |

26 Nov 2021 - Australian Big Banks are Back!

|

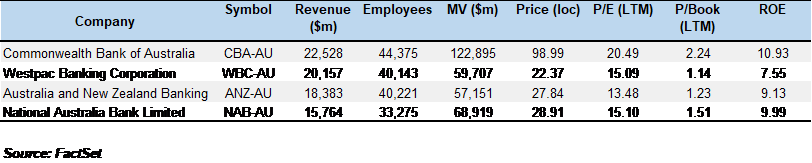

Australian Big Banks are Back! Arminius Capital 17 November 2021 The three banks with September financial years - ANZ, NAB and Westpac - are almost back to normal. Cash profits and return on equity are still below FY19 levels, but it is clear that the COVID-19 crisis has not left any scars on the banking system. Most importantly, the banks' capital positions are once again "unquestionably strong": an average Common Equity Tier 1 (CET1) ratio of 12.7%, up from 11.4% in FY20, means that all the banks can afford share buybacks.

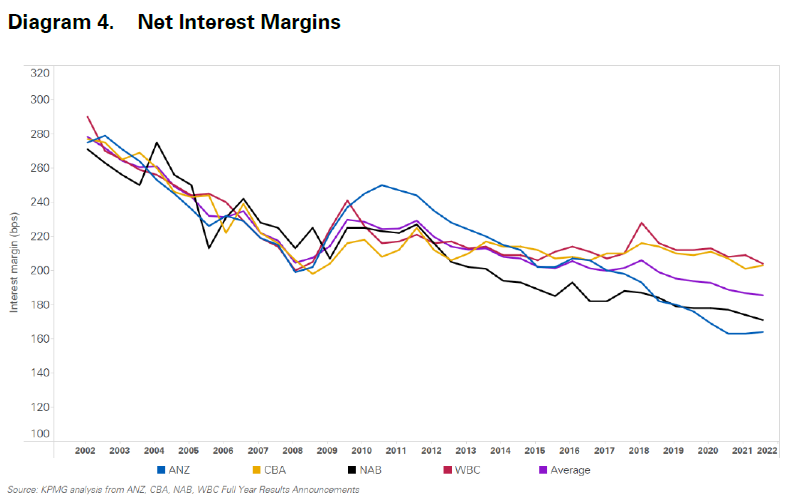

So far, however, organic growth is modest. Most of the recovery in cash earnings came from the $820m writeback of provisions built up last year. The banks are still paying "customer remediation costs" for their crimes of fees for no service and other horrors revealed by the Hayne Royal Commission, but these should end in FY22. The ratio of operating costs to income is still too high, and the banks will need another two to three years to achieve their cost reduction targets. The fundamental problem is that banking is no longer as profitable as it used to be, thanks to increased competition, tighter regulation, and higher capital requirements. The KPMG chart below shows how the banks' average net interest margin (NIM) has slid steadily downward, from 3.0% two decades ago to only 1.86% now.

In order to preserve their margins, the banks need to simultaneously cut their operating costs and increase their capital spending to improve their processes. CBA is leading the pack in both of these objectives, which is why it is the only one of the Big Four to have returned to its 2016 share price. Shareholders of the other three banks are well aware of the size of their capital losses over the last five years. This is also why CBA's dividend yield is less than 4.0% while the other three yield between 4.5% and 5.0%. FY22 results are likely to be similar to this year - modest organic growth, with profits buoyed by provision writebacks. But there will be complications. The first is that wholesale funding costs will increase as US and Australian interest rates rise, and the banks will lose some of the deposit inflow which was triggered by the COVID-19 panic. The second is that the Australian regulators will probably impose macroprudential controls to slow the pace of house price rises and to discourage borrowers from taking on excessive debt. The third is that the rise in CPI inflation will affect different sectors of the Australian economy in different ways, and may put an end to the improvement in loan delinquency rates. Our analysis suggests that the banks are fairly priced at present, as a sector with low earnings growth but also low risk. In the long run, the recent changes in industry structure will mean that bank earnings will grow more slowly than most companies in the S&P/ASX200 Index, making the banks attractive for income rather than capital growth. ANZ's cash profit of $6.2bn (218c per share) slightly exceeded market expectations, because stronger markets income offset a 4% increase in costs as well as ongoing customer remediation costs. The full-year dividend of 142c was higher than 60c in FY20 but still below 160c in FY19. During the latest half-year, ANZ's residential loan book declined by 1% against system growth of 4%. This disparity highlights the inadequacies of ANZ's mortgage processing systems, which the bank has acknowledged and is devoting capex to improving. FY22 earnings and dividends are expected to be flat, but ANZ is trading on a lower P/E than the other three, so the medium term may see some price gains through re-rating. Commonwealth Bank's trading update for the September quarter disappointed the market, with the CBA share price falling 8%. Despite above-system loan growth, cash profit for the quarter was flat at $2.2bn and net interest margin fell significantly. A single quarter is not necessarily an indicator of the 2022 result, but it does reinforce our view that the banks face a difficult competitive environment. NAB reported a $6.6bn cash profit (199c per share) and lifted its full-year dividend to 127c (a 64% payout ratio), which was better than 60c in FY20 but still below 166c in FY19. The result was free of notable items and other one-offs. Management indicated that future dividends would be 65% to 75% of cash earnings. During the half-year, NAB grew its gross loans and advances (GLA) as fast as system growth or faster. The bank has simplified and automated its mortgage approval process: 30% of Simple Home Loans are expected to be approved in one hour, and 60% within one day. Westpac is lagging behind the other three big banks. FY21 cash earnings of $5.4bn (146c per share) are equivalent to a return on equity of 7.6%, well behind the Big Four average of 9.9%. Westpac's cash earnings suffered from a notable items charge of $1.6bn, and the September 2021 half year was disappointing, with expenses rising and margins falling. The FY22 dividend of 118c (an 81% payout ratio) was better than 31c in FY20 but well below 174c in FY19. The share price has fallen 9% since the result - the market clearly does not believe that Westpac will achieve its announced cost reduction targets on time. Funds operated by this manager: |

25 Nov 2021 - Performance Report: Laureola Australia Feeder Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Life Settlements are resold life insurance policies and can be thought of as a form of finance extended to an individual backed by the person's life insurance policy. This financing is repaid upon maturity by collecting the death benefit from the insurance company. Risk mitigation measures implemented by Laureola include science-driven due diligence of policies, active monitoring of insured through a vertically integrated operation, and investor aligned fund design. |

| Manager Comments | The Laureola Master Fund has a track record of 8 years and 7 months and has consistently outperformed the Bloomberg AusBond Composite 0+ Yr Index since inception in May 2013, providing investors with a return of 15.37%, compared with the index's return of 3.52% over the same time period. On a calendar basis the fund has never had a negative annual return in the 8 years and 7 months since its inception. Its largest drawdown was -4.9% lasting 10 months, occurring between December 2018 and October 2019. The Manager has delivered higher returns but with higher volatility than the index, resulting in a Sharpe ratio which has never fallen below 1 and currently sits at 2.44 since inception. The fund has provided positive monthly returns 97% of the time in rising markets, and 100% of the time when the market was negative, contributing to an up capture ratio since inception of 167% and a down capture ratio of -258%. |

| More Information |

25 Nov 2021 - Fund Review: Bennelong Twenty20 Australian Equities Fund October 2021

BENNELONG TWENTY20 AUSTRALIAN EQUITIES FUND

Attached is our most recently updated Fund Review on the Bennelong Twenty20 Australian Equities Fund.

- The Bennelong Twenty20 Australian Equities Fund invests in ASX listed stocks, combining an indexed position in the Top 20 stocks with an actively managed portfolio of stocks outside the Top 20. Construction of the ex-top 20 portfolio is fundamental, bottom-up, core investment style, biased to quality stocks, with a structured risk management approach.

- Mark East, the Fund's Chief Investment Officer, and Keith Kwang, Director of Quantitative Research have over 50 years combined market experience. Bennelong Funds Management (BFM) provides the investment manager, Bennelong Australian Equity Partners (BAEP) with infrastructure, operational, compliance and distribution services.

For further details on the Fund, please do not hesitate to contact us.

25 Nov 2021 - The Long and The Short: The tide of inflation

|

The Long and The Short: The tide of inflation Kardinia Capital 08 November 2021 |

|

Inflation looking less transitory Signs continue to indicate that inflation is creeping into the system. Central and global banks don't tend to agree, but we think the tone will shift. In the face of a constant inflation rhetoric, the global consensus continues to push back on the structural shift in inflation. However, evidence of price inflation and supply chain disruptions are now showing up at every corner.

The Fed still sees inflation as temporary, with upticks in inflation explained away as simply the economy normalising after the pandemic shock and supply chain bottlenecks causing temporary disruption. But our US contacts note that those bottlenecks could last until 2022 or later. US Transportation Secretary, Pete Buttigieg, suggested in a recent interview that US supply chain issues may last 'years and years'[1]. Both Dubai Ports and Singapore-based Ocean Network Express, which carries more than 6% of the world's containerised freight, have suggested an easing in supply chain disruption may not come until as late as 2023. Listening to the key metrics

The UN's Food Price Index is up 33% year on year. The index measures the global monthly price change in a basket of five food commodities, with vegetable oils up 61%, sugar up 53%, cereals up 27%, meat up 26% and dairy up 15%.

Rising fears about supply and energy security have also pushed Brent to above US$80/bbl, up 40%, and spot Asian LNG prices to US$35mmbtu, up 600% since 2019 Meanwhile, the USA labor market is already tightening. The drop in unemployment to 4.8%, and rapid 0.6% month on month wage growth, is indicative of a structural shortage of workers. We expect the US experience to be repeated in Australia as our two largest economies emerge from lockdowns. We're paying close attention to wage inflation in this country, given the Reserve Bank of Australia has indicated it is unlikely to raise interest rates while this metric remains subdued. Is history repeating itself?

We believe what we're seeing today is remarkably similar to the experience in the 1970s. Back then, food and energy supply 'shocks' led the decade's inflationary surprises. Firstly, bad weather saw CPI for food up 20% in 1973 and 12% in 1974; then came the Middle East conflict in 1973, which drove a rapid spike in the oil price. History may not repeat itself, but it can rhyme. Today it is fuel prices, unfavourable weather and the impact of coronavirus on supply chains leading to food inflation. For the oil market, it's the rapid move towards 'green' renewable energy (coupled with strong demand as the world emerges from the ravages of coronavirus) and freight costs that has led to a 70% surge in global oil prices this year. Why does it matter?

Today, as inflationary pressures continue to build, several advanced economies have already increased rates, including the Norges Bank, the Reserve Bank of New Zealand and the Monetary Authority of Singapore, with the Bank of England potentially moving shortly. The recent Australian quarterly CPI release (3.0% year on year) has ensured that inflation will remain a heated debate into 2022. At the very least: if inflation expectations build, interest rates launch sooner and bond prices continue to fall, then we should expect higher volatility in equities. Individual sector returns will diverge with winners and losers. Equity returns historically beat inflation, within which commodities and energy sectors tend to do well. Banks and sectors which exhibit monopolistic pricing powers and hard assets, such as property, also perform strongly; whereas rate-sensitive sectors such as IT and loss-making stocks tend to underperform. We have seen this before and have positioned the Kardinia portfolio accordingly. |

|

Funds operated by this manager: Bennelong Kardinia Absolute Return Fund |

|

[1] Buttigieg: Some Supply Chain Issues May Last 'Years and Years', Bloomberg, 8 October 2021 |

24 Nov 2021 - Performance Report: 4D Global Infrastructure Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The fund is managed as a single portfolio including regulated utilities in gas, electricity and water, transport infrastructure such as airports, ports, road and rail, as well as communication assets such as the towers and satellite sectors. The portfolio is intended to have exposure to both developed and emerging market opportunities, with country risk assessed internally before any investment is considered. The maximum absolute position of an individual stock is 7% of the fund. |

| Manager Comments | The 4D Global Infrastructure Fund has a track record of 5 years and 8 months and has outperformed the S&P Global Infrastructure TR Index (AUD) since inception in March 2016, providing investors with a return of 9.42%, compared with the index's return of 7.87% over the same time period. On a calendar basis the fund has had 1 negative annual return in the 5 years and 8 months since its inception. Its largest drawdown was -19.77% lasting 1 year and 8 months, occurring between February 2020 and October 2021 when the index fell by a maximum of -24.67%. The Manager has delivered these returns with -0.48% less volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times and currently sits at 0.72 since inception. The fund has provided positive monthly returns 95% of the time in rising markets, and 11% of the time when the market was negative, contributing to an up capture ratio since inception of 105% and a down capture ratio of 95%. |

| More Information |