NEWS

Performance Report: Collins St Value Fund

The Collins St Value Fund rose by +4.11% in November. Since inception in February 2016, the fund has returned +13.25% per annum, an outperformance of +4.32% relative to the ASX 200 Total Return benchmark which has returned +8.93% on an...

Read more...

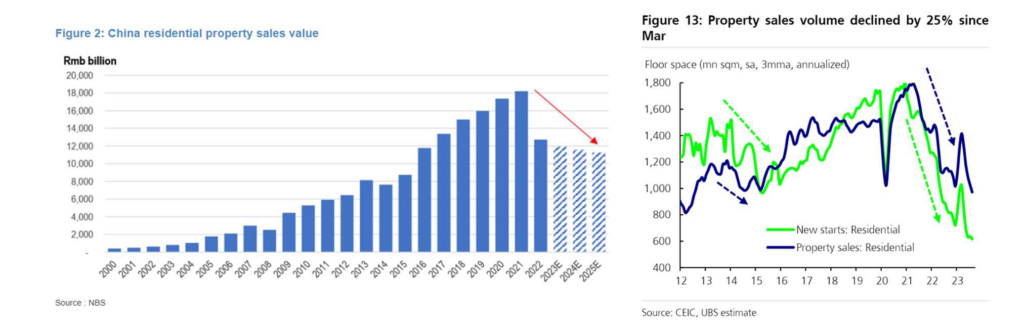

China Property: Has the "Grey Rhino" been tamed?

Stabilization of property market in sight = Time to buy quality growth stocks in China.

Relative to most governments in the world, the Chinese authorities proactively controlled and deflated the property

market bubble to...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +5.52% in November, outperforming the ASX 200 Total Return benchmark by +0.49%. Since inception in January 2013, the fund has returned +12.22% per annum, an outperformance of +3.86% relative to the...

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund rose by +6.6% in November, outperforming the ASX 200 Total Return benchmark by +1.57%. Since inception in November 2017, the fund has returned +16.6% per annum, an outperformance of +9.37% relative to...

Read more...

Why government bonds remain a natural choice

As we approach the eagerly anticipated end of the rate hiking cycle, investors are considering how to position portfolios for what comes next, while trying to navigate the current higher rate, higher inflation environment.

Read more...

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund rose by +8.14% in November, outperforming the ASX 200 Total Return benchmark by +3.11%. Since inception in June 2017, the fund has returned +17.58% per annum, an outperformance of +10.04% relative to...

Read more...

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) rose by +7.53% in November, outperforming the S&P Global Infrastructure TR (AUD) benchmark by +3.06%. Since inception in March 2016, the fund has returned +9.15% per annum, an outperformance of...

Read more...

Investing Essentials: Diversification - The shield against investment volatility

Are you putting all your eggs in one basket?

As any investor will tell you, investing can be a rollercoaster.

Not all investments behave in the same way - different types of investments behave differently under...

Read more...

Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

The Skerryvore Global Emerging Markets All-Cap Equity Fund rose by +1.94% in November. Since inception in August 2021, the fund has returned +2.19% per annum, an outperformance of +6.13% relative to the MSCI Emerging Markets (MMEF) AUD...

Read more...

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund rose by +6.21% in November, outperforming the ASX 200 Total Return benchmark by +1.18%. Since inception in June 2018, the fund has returned +9.58% per annum, an outperformance of +2.41% relative to the...

Read more...