NEWS

Performance Report: Equitable Investors Dragonfly Fund

The Equitable Investors Dragonfly Fund rose by +2.69% in November. Top contributors included Intelligent Monitoring (IMB) and Geo (NZ: GEO), while Redflow (RFX) and Spacetalk (SPA) detracted from performance. Equitable noted that, while...

Read more...

Performance Report: Insync Global Quality Equity Fund

The Insync Global Quality Equity Fund rose by +5.76% in November, an outperformance of +1.06% compared with the All Countries World (AUD) benchmark which rose by +4.7%. Since inception in October 2009, the fund has returned +12.25% per...

Read more...

Performance Report: Insync Global Capital Aware Fund

The Insync Global Capital Aware Fund rose by +5.59% in November, an outperformance of +0.89% compared with the All Countries World (AUD) benchmark which rose by +4.7%. Since inception in October 2009, the fund has returned +10.34% per...

Read more...

Performance Report: Digital Asset Fund (Digital Opportunities Class)

The Digital Asset Fund (Digital Opportunities Class) rose by +0.08% in November. Since inception in May 2021, the fund has returned +22.5% per annum, a difference of +39.67% relative to the S&P Cryptocurrency Broad Digital Market benchmark...

Read more...

Performance Report: PURE Resources Fund

The PURE Resources Fund rose by +1.94% in November, a difference of -1.15% compared with the S&P/ASX Small Resources TR benchmark which rose by +3.09%. Since inception in May 2021, the fund has returned +8.56% per annum, a difference of...

Read more...

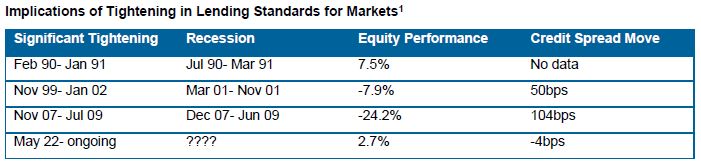

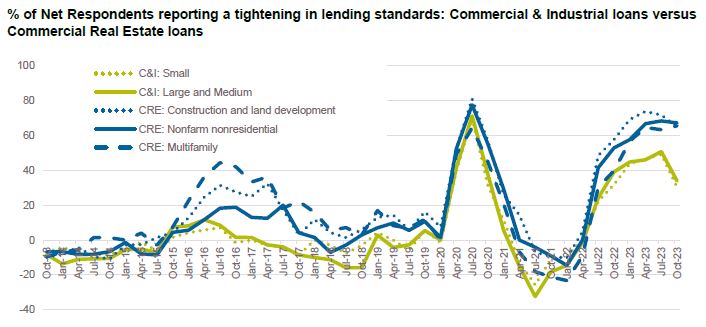

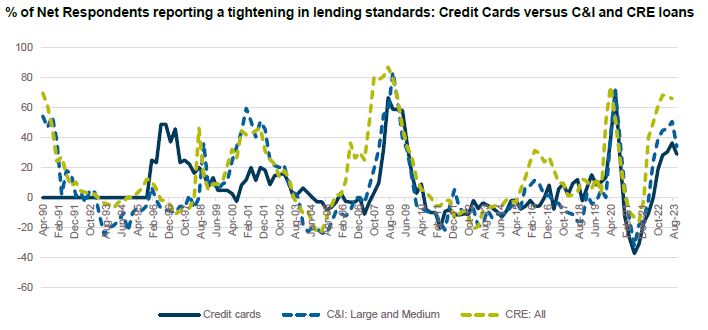

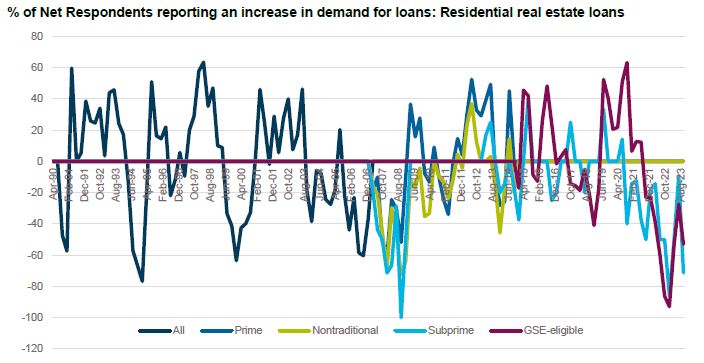

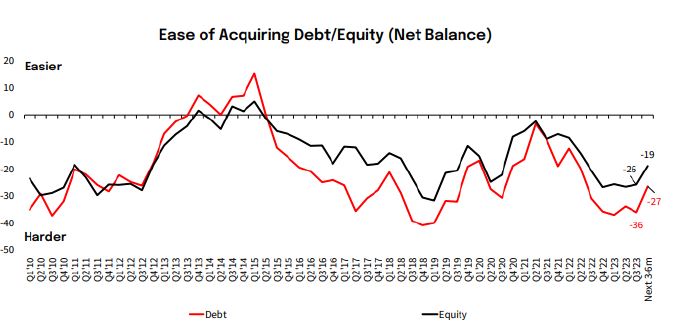

What is the Fed's Senior Loan Officer Survey and what is it telling us?

The financial system of the United States is unique. Unlike Australia where households and institutions are at the mercy of the four major banks, the US banking system is highly dispersed. There are over 4,000 commercial banks and over 500...

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +1.16% in November. Since inception in April 2018, the fund has returned +11.01% per annum, an outperformance of +4.69% relative to the RBA Cash Rate + 5% benchmark which has returned +6.32% on an...

Read more...

Performance Report: PURE Income & Growth Fund

The PURE Income & Growth Fund rose by +0.65% in November. Since inception in December 2018, the fund has returned +10.71% per annum, a difference of +7.75% relative to the S&P/ASX Small Industrials TR benchmark which has returned +2.96% on...

Read more...

Performance Report: Kardinia Long Short Fund

The Kardinia Long Short Fund returned +3.68% in November. Since inception in May 2006, the fund has returned +6.95% per annum, an outperformance of +0.8% relative to the ASX 200 Total Return benchmark which has returned +6.15% on an...

Read more...

Investment Perspectives: 12 surprising charts for your Christmas stocking

As we near the end of a volatile macroeconomic year, we look at some of the interesting trends in global real estate and consider what's to come.

Read more...