NEWS

19 Nov 2024 - Glenmore Asset Management - Market Commentary

|

Market Commentary - October Glenmore Asset Management November 2024 Globally, equity markets were weaker in October. In the US, the S&P 500 declined -1.0%, the Nasdaq fell -0.52%, whilst in the UK was down -1.54%. In Australia, the All Ordinaries Accumulation index declined -1.33%. On the ASX, the top performing sector was gold, supported by a +5% rise in the gold price. Banks also performed well in the month. Consumer staples were the worst performer, impacted by index heavyweight Woolworths (WOW) falling -10% following a weaker than expected 1H25 trading update. In bond markets, the US 10 year government bond yield rose +50 basis points (bp) to close at 4.28%, whilst its Australian counterpart increased +53bp to end the month at 4.51%. The main driver of the higher bond yields was market expectations of less interest rate cuts from the Federal Reserve. Funds operated by this manager: |

18 Nov 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Carrara Global Opportunities Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Carrara Credit Portfolio | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Woodbridge Secured Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Minotaur Global Opportunities Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 850 others |

18 Nov 2024 - Macro Research - AUD Outlook

15 Nov 2024 - Hedge Clippings | 15 November 2024

|

|

|

|

Hedge Clippings | 15 November 2024 Last week's Hedge Clippings noted that Donald Trump's election victory would lead to some predictably unpredictable outcomes. Earlier this week we met with Richard Grace, ex CBA economist, now principal of PinPoint Macro Analytics, who has kindly agreed to provide some economic muscle and rigour to our weekly view of the world. Richard's contribution is included below as a Fund Monitor's Insights Article, part of which is summarised below. We mentioned to Richard that Newton's Third Law tells us that for every action, there is an equal and opposite reaction--a concept that generally provides a sense of predictability. But Richard pointed out that economics and politics doesn't work the way of physics and that the effects of Trump's presidency is likely to be anything but predictable: Each of his actions is bound to provoke a reaction, but the direction and magnitude of that reaction remains anyone's guess. Since Donald Trump was re-elected on November 5th, the Australian dollar (AUD) has slipped about 3% against the U.S. dollar, now hovering around 0.6450. For those who remember Trump's 2016-2020 term, this drop might feel like déjà vu. His announced tariffs on Chinese and European goods back then strengthened the USD and put downward pressure on the AUD, and history seems to be repeating itself. Trump's proposed economic policies this time around are designed to boost the U.S. economy, but not without shaking up global trade relationships. He's planning to significantly increase tariffs on Chinese imports to 60% and on all U.S. imports from around 3% to 20%. If Congress allows these measures, the impact on global growth could be profound, especially as China struggles with a sluggish property market. For Australia, the road ahead may be bumpy, with the AUD facing further downside into 2025. The graph below illustrates the effect Trump's tariffs had on a handful of currencies during his last term in office - Meanwhile, over in Washington, Trump has assembled a headline-grabbing cabinet. His appointment of Robert F. Kennedy Jr. to head the Department of Health and Human Services is contentious, given Kennedy's scepticism towards vaccines. The potential ramifications for U.S. health policy could create market uncertainty, especially in sectors like pharmaceuticals and healthcare. Adding another layer of unpredictability, Trump has put Elon Musk at the helm of a newly formed Department of Government Efficiency--tasked with slashing bureaucracy. Musk's call for "high-IQ revolutionaries" willing to work 80+ hour weeks for zero pay might seem like a joke, but it underscores the aggressive belt-tightening Trump is pursuing. Investors will be watching for signs that this approach could create a more efficient U.S. administration, but for now, it seems more noise than concrete benefits. In yet another controversial move, Trump appointed Matt Gaetz as the new attorney general. Gaetz, who has faced his share of controversies, including a past Justice Department sex trafficking investigation, now leads the very institution that once scrutinised him. This, much like Trump's broader cabinet reshuffle, introduces reactions that are difficult to foresee, adding to the overall unpredictability of the administration. As always, in uncertain times, there are opportunities. Trump's renewed focus on U.S. industry may boost certain sectors--infrastructure, for example--and that could provide selective investment opportunities. But for those watching from Australia, the emphasis should be on managing FX risk and monitoring how the dust settles, especially regarding China and resource exports. News & Insights New Funds on FundMonitors.com Macro Research - AUD Outlook | PinPoint Macro Analytics News & Views: Tariffs - the impact on infrastructure | 4D Infrastructure Megatrends for 2025 and beyond... | Magellan Asset Management October 2024 Performance News Bennelong Concentrated Australian Equities Fund Quay Global Real Estate Fund (Unhedged) Glenmore Australian Equities Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

15 Nov 2024 - Performance Report: Altor AltFi Income Fund

[Current Manager Report if available]

15 Nov 2024 - Performance Report: Glenmore Australian Equities Fund

[Current Manager Report if available]

15 Nov 2024 - Making Millions In The Market 1987 Crash!

|

Making Millions In The Market 1987 Crash! Marcus Today October 2024 |

37 Years! Where Has That Gone!I started as a back-office clerk in the UK before transitioning to a trainee dealer role on the floor of the London Stock Exchange. It didn't take long to discover that I had a knack for it and developed a passion for the market. The early 80s brought significant changes under Thatcher, including the Big Bang in the City. These changes eventually led to my becoming a member of the London Stock Exchange in 1985 - two years before the crash. By that point, I had already spent eight years gaining experience in the market leading up to that fateful October.I had moved from broking to trading and became a senior option trader on the floor for a company called Smith Brothers, a venerable old Jewish stockjobbing firm. Smith Brothers eventually became Smith New Court and was later bought out by Merrill Lynch. As a senior trader, I was especially skilled at first-day trading in the recently privatised UK companies like Jaguar, British Airways, British Gas, and Rolls Royce. Shouting, screaming, and being quick with arithmetic was my forte, and I loved it..png)

The Calm Before the StormWe all knew that one day the game would be up and that all the fun we were having would have to be paid for. The piper always takes his wages. And talking of wages, the Big Bang in the City created yuppies. I was a Yuppie. Filofax in hand and even a Motorola Mobile phone. Yes, for those that can remember them they resembled a brick.Building Tension and Optimism in the MarketThat summer leading up to the crash worries started to emerge. We had the odd spasm but nothing more that tremors before the big eruption in October. Now at the time it was a heady party in the market and there was a belief that it was never going to go down. Every pullback was another buying opportunity. As an option trader it was money for jam. All the institutions did was sell us puts which ultimately went out worthless.We bought puts by the bucket load. Thousands of them. Now if you know option hedging if you buy a put you buy the stock to hedge it. You buy with a delta ratio. Not wishing to get too complicated, but the stock we bought kept going up and covered the loss from the puts that we had been buying. It was a simple strategy. Everyone was happy. Institutions figured that if the market slipped back and they had the stock 'put' on them they would be happy to be buying. After all the market only ever goes up, doesn't it?The Yuppie Boom and Soaring SalariesSo, the game continued. The instos earned extra income and looked very clever in the brave new world and option traders like me took on the risk and bought the stock. Salaries soared as profits rolled in. Privatisation gave everyone a stake in the new stock market bubble. My salary went from GBP1701 to GBP40,000 over that period.1700 pounds did not even cover my car loan when I started. Didn't even cover my season ticket so I worked for my father during the holidays on building sites and weekends to earn enough to eat and play in the City. With the increase in our salaries came a belief that we were invincible. We were early 20s and Masters of the Universe. All that was to end..png)

The Dutch ConnectionAt that time there were a lot of international traders in the London Traded Option Market (LTOM). The Dutch were there in force and I was pretty tight with my Dutch friends. They liked to party and had huge expense accounts to boot plus they knew options. They practically invented them. Think tulips. Anyway, the Friday before the Black Monday crash I was in Amsterdam having flown through the Hurricane that hit London the night before. Needless to say, I had a fabulous weekend in a great city with some lovely people. Sunday night I flew home and knew that we were in for a serious week. The market had been closed on the Friday as people struggled to work and tried to get through the physical carnage that had hit London.The Crash BeginsSo, there we were at Smith Bros, a bunch of young traders who owned all the puts. A lot of them were October puts (if the crash had happened week later things would have been different). We had a huge equity trading operation. It was not a big firm and the company was long. Seriously long going into the crash. With the new computerised trading that had just been brought in adding to the complications. After some crisis meetings, we were ready to take the floor like gladiators entering the arena. We knew it would be make or break for the company. And so, it began.The falls were mind numbing. We did not have computers in those days, so it was impossible to make prices on options and know your positions from minute to minute. The only thing we knew was that we were all very short. As prices plunged through the strike prices were got shorter and shorter. We had to buy stock to re-hedge our delta exposure and buy lots of it.You would think that buying stock would be easy in a crash. Just stand there with a buy pad and write out the slips. No such luck. Under our company rules we were only allowed to trade with our own equity market makers. So, a phone call, yes, they were phone calls, to the dealing desk in equities to buy 1m Rolls Royce shares was followed with a short sharp two-word sentence one of which was 'off'. We could not buy enough stock to cover our shorts.The equity market makers did not have the capacity to sell as much as we wanted and believed that a rally was imminent and there was no value in selling a spotty option trader 1 million Rolls Royce at the bottom. Of course, it turned out that it wasn't the bottom. FTSE 100 fell by 10.8% on Black Monday itself, and 12.2% on the following day.Profiting in the PanicWe made millions that week. Puts that were worthless were suddenly worth fortunes, everybody was buying puts to cover or we were buying as much stock as we could to hedge our position. It was frantic. I lost my voice and couldn't talk properly for the following week. Fortunes were made and lost that week and as usual we washed them down with the yuppie drink of choice, Bollinger. We were heroes. Just for one day.When the option trading team finished the first day, we walked up to the equity trading floor (remember it had all gone electronic by then) and were given a standing ovation. It was like winning the world cup. We walked amongst our peers swapping war stories and offer congratulations and sympathy. The upshot was the option traders had made a profit of GBP9.5m on that day. The rest of the firm had lost GBP9m. Smith Brothers was still in business. We had saved the firm. Bonuses all round.The Calm After the StormAnd so, the week unfolded. Day after day a similar story. My girlfriend at the time was away on business and a nightly phone call really didn't do it justice. Besides I was usually in the Arbitrageur Bar drinking and dancing on the ceiling.The only problem seemed to be that after the crash, no one else wanted to play anymore. Wounds were being licked. Traders were being let go and the world of the yuppie changed. 'Wall Street' came out and we had 'Bud Fox' and 'Gordon Gecko' to model ourselves on but it wasn't the same. For the following two years option traders in London came in every day and twiddled their thumbs me included. If someone wanted to trade the competition was so fierce that we also jumped on a buyer or a seller with enthusiasm. After two years of holding out and playing dumb games, I saw an ad in the FT for traders to come and trade options and derivatives in Sydney. My way out. And here I am 35 years later.What Lessons Can Be Learnt from All This?And how does it relate to the current market? (Updated slightly!)Well, it is pretty fully valued. Complacency is rife and we have some serious irrational behaviour going on. Trump Media But it does not feel like 1987. Things had got really out of control by then. Corporate leverage and balance sheets were stretched to the hilt and takeovers using scrip were rife. Deals were everywhere. Since then, of course we have had other crashes, mini crashes and the mother of all crashes the GFC. What differs from 1987 to 2008 was that the '87 crash was confined to the stock market primarily. It really didn't spill over to the real economy or jobs. It threatened to, but never really did. We had a recession we had to have (some years later) and house prices became the bubble and then crashed. Interest rates went through the roof. In the GFC everything was infected. The banks nearly collapsed and we were on the brink of another great recession. Luckily central banks stepped in and saved the day. Record low interest rates have saved us but have enslaved us through massive household debts. We are paying the price for that currently but house prices remain massively elevated!Final ThoughtsSo, will we see another crash? Yes of course we will. History does repeat. Will it be soon? I suspect that is unlikely given the low rates and the lack of alternatives. Will some bubble markets crash? Yes. Chip stocks may crash one day. Who knows? The one lesson that I learnt from that crash, and the subsequent ones, is avoid over leverage and have some cash around for those opportunities. The GFC and other crashes are rare events and when they happen, fortune favours the brave and the market gets irrational and traders throw everything out in the search for liquidity. It will happen again. That is why you must keep a buffer and have cash ready to be deployed to snap up those once in a lifetime opportunities. The investors that got seriously hurt were those that had massive leverage and had to sell at any price. The smart money bought. It is easy in these heady times to throw caution to the wind. Fear of missing out is real. Stick to your plan. Have discipline. Buy quality companies and have funds ready just in case. And finally, don't believe your own hype. Hubris is a dangerous thing. Pride does come before a fall. Everybody looks good in a full-on bull market but it's when the tide goes out, that we see who is not wearing any clothes as they say. Incidentally during the crash our index futures trader had a huge punt on the market bouncing and bought back all the short exposure we collectively had. He didn't tell anyone and hid his trade until Christmas Eve. Somewhat of a shock to find a massive multi-million-dollar loss that carried our bonuses down the Thames but that is a whole different story and one for another day. In there somewhere! Author: Henry Jennings |

|

Funds operated by this manager: |

.png)

14 Nov 2024 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

14 Nov 2024 - Performance Report: Airlie Australian Share Fund

[Current Manager Report if available]

14 Nov 2024 - Have ASX iron ore stocks found their floor?

|

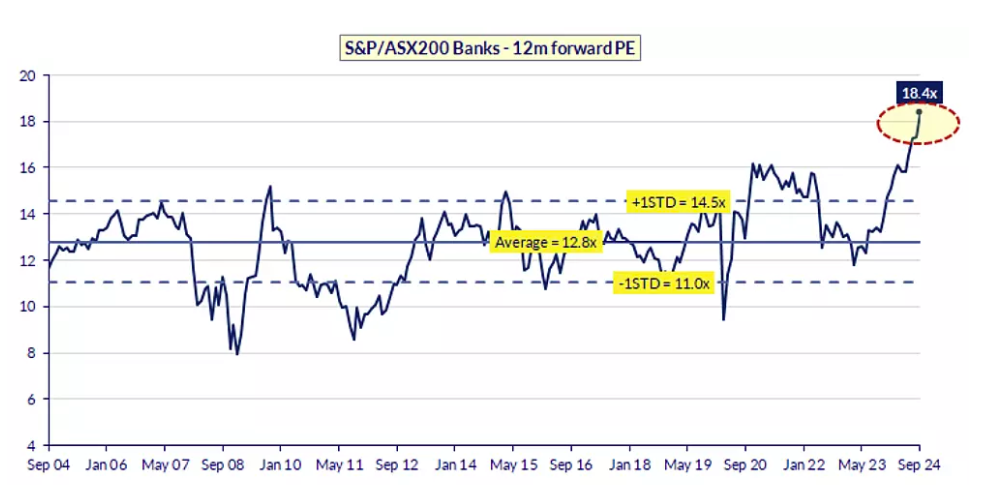

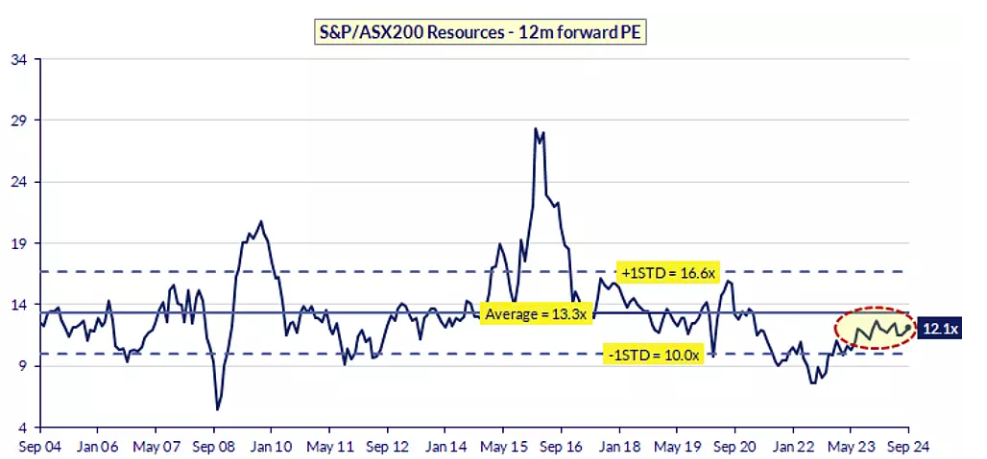

Have ASX iron ore stocks found their floor? Tyndall Asset Management October 2024 Iron ore prices may have finally found some stability moving forwardRecently, the People's Bank of China (PBOC) rolled out its most significant set of monetary easing policies since 2015. These measures were designed to address China's ongoing property sector challenges and provide a broader boost to economic growth. Interest rates and reserve requirement ratios have been cut to historically low levels, signalling the government's commitment to maintaining liquidity and preventing a deeper slowdown. While this has spurred a rally in both Chinese equities and Australian resource stocks, the question remains: Is this a short-term sentiment-driven bounce, or the start of something more sustainable? While opinions may vary on the longevity of this rally, one thing is clear: China's looser monetary policy has created an environment ripe for further fiscal and property policy adjustments. The current positioning of the market is quite negative on China and thus underweight stocks that are exposed to China such as Australian Resources. This helps explain the recent strong market reaction. Have iron ore stocks found their floor?The common reaction to China's slowdown often involves calls to sell big miners like BHP (ASX: BHP) and Rio Tinto (ASX: RIO). However, that kind of knee-jerk reaction doesn't align with a value-based investing approach. While sentiment undeniably influences short-term market movements, the real question is: How much steel is the global economy demanding, and what is the marginal cost of supply? At current prices, iron ore is likely sitting at a support level, hovering around US$95/t, which is underpinned by break-even costs. Prices have dipped below US$95/t for only 16 days this year, compared to 50 days over the last three years. The cost curve supports this level, as many producers would be unprofitable at lower prices. Additionally, trader mentality tends to kick in once prices break the US$100/t threshold, adding further support to this range. On a more fundamental level, we believe there is currently around 120mt of supply in the market that requires a price of over So, the question we have to ask is whether China's economic weakness is severe enough to remove another 120Mt of iron ore demand from the market. We don't think so. While the Chinese government has signalled its willingness to address demand concerns through coordinated policies, the China Iron & Steel Association (CISA) has projected that crude steel production will remain flat year-on-year in 2024. This suggests stability moving forward at current levels. Supply-side adjustments: Rebalancing the marketOn the supply side, significant cuts in iron ore production from both India and China have already done much to rebalance the market. India's output has fallen from 70Mtpa earlier this year to 30Mtpa due to price sensitivity, while China's domestic production has similarly dropped from 200mtpa to 80mtpa on a 62% Fe basis. In Australia, we have seen Mineral Resources (ASX: MIN) shut down the Yilgarn operations (8Mt) and the Sino Iron Project decreased from 21Mt to 14mt. These adjustments further underscore the market's price elasticity. The greatest long-term supply risk remains the Brazilian mining giant, Vale. Although Vale has increased its production guidance for the year, Brazilian exports typically flatten out in the final quarters of the year due to seasonality, so massive increases in output are unlikely. Longer term, another potential supply-side disruptor that has long spooked the market is the Simandou project in Guinea. The rail line is expected to be operational by Q1 2026, with the port to be staged thereafter. The complexity of the project poses a significant risk of delays. We expect the operation to ramp up through 2028. Additionally, the wet season in Guinea introduces challenges with stockpile management and moisture control. For now, the risk of an oversupply glut in the iron ore market seems overplayed by the bears in the market. Seasonality and SentimentAnother factor working in iron ore's favour is seasonality. Historically, iron ore prices have shown strength from December through February, as China's domestic production falls during the winter months. This forces the country to rely more on seaborne supply, which is often disrupted by wet weather conditions in Brazil and the Pilbara region in Australia. Port inventories are currently sitting at 150Mt, which is on the higher end of the seasonal average. However, this doesn't pose a significant threat to the market, as a portion of these inventories are now controlled by major iron ore players for blending purposes. Moreover, low-grade discounts have narrowed, and rebar spreads have rebounded from their September lows, signalling that much of the bearish sentiment may already be priced in. It is also difficult to assess the full supply chain inventories in China including stockpiles at steel mills. Recent discussions with China companies suggest that this inventory may be at the lower end of history. Where is the opportunity in iron ore equities?In terms of equities, Fortescue Metals Group (ASX: FMG) is a recent addition to the portfolio. It offers an attractive entry point, and its lack of gearing makes it a pure play on a rebound in iron ore prices while paying an attractive fully franked distribution. BHP and Rio Tinto offer more diversified exposure, with their base metals businesses providing some downside protection. While the market remains cautious due to weak Chinese sentiment, the fundamental factors supporting iron ore prices--cost support and seasonality--paint a more optimistic picture. As long as demand holds and supply remains in check, iron ore prices are likely to stabilise around current levels, if not rise slightly through the remainder of the year. Given this, an overweight position in iron ore equities, particularly FMG, appears to be a solid investment in the months ahead. Is this the start of a larger rotation out of the banks into the miners?We are seeing a significant valuation gap between the Bank and Resource sectors. The Banks sector has surged to an all-time high P/E of 18.4x (refer to Figure 1), well above its historical average of 12.8x, even exceeding the +1 standard deviation level of 14.5x, indicating stretched valuations. Figure 1: ASX200 Banks - trading at 18.4x forward concensus earnings (all-time high) |