NEWS

9 Apr 2025 - Performance Report: Glenmore Australian Equities Fund

[Current Manager Report if available]

9 Apr 2025 - Performance Report: Bennelong Long Short Equity Fund

[Current Manager Report if available]

9 Apr 2025 - Everyone has a plan until they get punched in the face

|

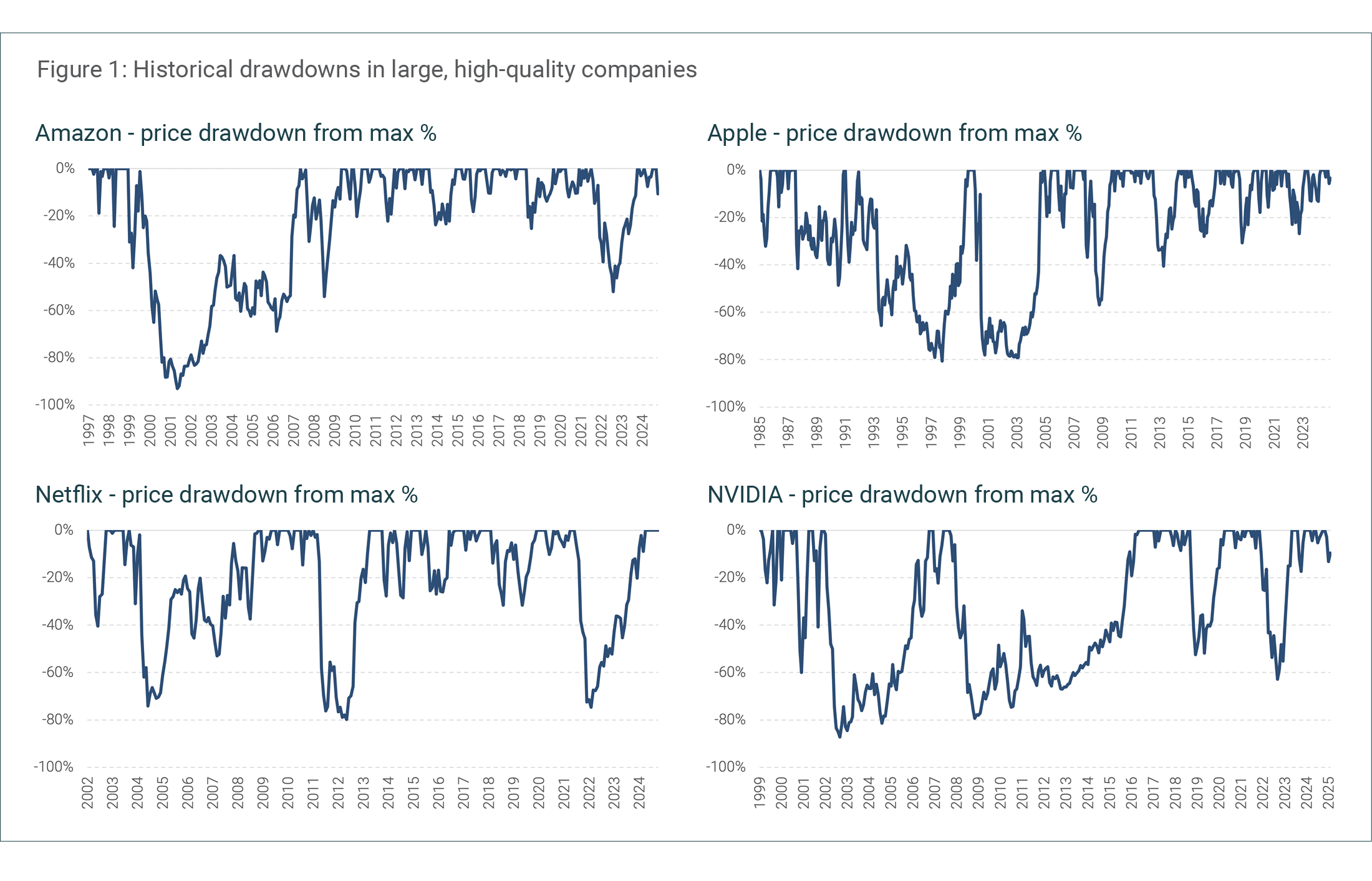

Everyone has a plan until they get punched in the face Canopy Investors March 2025 "Know what you own and know why you own it." Long-term investment success requires differentiated thinking supported by genuine conviction. At Canopy, we believe conviction cannot be borrowed or assumed; it must be built through detailed research and a deep understanding of the businesses we invest in. When markets turn volatile and uncertainty reigns, the strength of our conviction can be the difference between seizing opportunity and capitulating at precisely the wrong moment. The challenge of maintaining conviction Maintaining conviction through market volatility is one of the toughest challenges investors inevitably face. As shown in the charts below, even the largest and highest quality companies can experience significant price declines that test investor resolve. Amazon's share price fell 93% between December 1999 and September 2001, took eight years to regain its prior high, and then dropped more than 50% again during the Global Financial Crisis. Similarly, Apple, Netflix and NVIDIA have each weathered multiple declines exceeding 70% on their paths to becoming some of the world's most valuable companies.

This pattern isn't limited to a few notable exceptions. In a study of the top 100 most successful companies of each decade since 1950, Bessembinder (2020) found that even these exceptional investments experienced average drawdowns of 32.5%, lasting 10 months. Volatility has real consequences for realized investment returns. A long-running analysis by market research firm DALBAR (2022) found that, over the last three decades, the average US equity fund investor has underperformed the S&P 500 by 3-4% annually - primarily because of buying high and selling low during volatile periods. When share prices decline and negative sentiment builds, many investors abandon sound investments precisely when they should maintain or increase their positions. As Cullen Roche put it, "The stock market is the only store where, when everything is on sale, people run away." At the root of this behaviour is what we call 'borrowed conviction' - investment theses adopted from respected investors, the financial media or popular sentiment rather than developed through independent research. When negative headlines accumulate and prices fall, borrowed conviction can crumble in the face of mounting pressure to sell. Only by developing one's own conviction - built on a deep understanding of a business, its competitive advantages, its long-term prospects and cash flow generation - can investors maintain confidence in the face of market pessimism or temporary setbacks. Being different and right "To achieve superior investment results, you have to hold views that are different from the consensus and be right." - Howard Marks. Being different alone is not sufficient; contrarianism without insight typically leads to poor results. Detailed research reveals opportunities where the market's understanding is incomplete or incorrect. These opportunities often arise in several ways:

Strong conviction must be balanced with intellectual flexibility. As Charlie Munger observed, "Part of what you must learn is how to handle mistakes and new facts that change the odds." This balance helps distinguish between appropriate persistence and mere stubbornness - knowing when to hold firm in your thesis and when to adapt to new evidence. Our approach At Canopy, we have developed a structured research process designed to build knowledge, test assumptions and size positions based on conviction levels:

Investing with conviction We believe conviction built on detailed research is essential for long-term investment success. Our structured research process develops this conviction through comprehensive business analysis, clear investment theses, collaborative team input and systematic position sizing. This disciplined approach enables us to identify opportunities amid volatility and maintain positions when others capitulate. |

|

Funds operated by this manager: Canopy Global Small & Mid Cap Fund |

Source: FactSet, Canopy Investors.

Source: FactSet, Canopy Investors.

8 Apr 2025 - Performance Report: 4D Global Infrastructure Fund (Unhedged)

[Current Manager Report if available]

8 Apr 2025 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

8 Apr 2025 - Australian Secure Capital Fund - Market Update

|

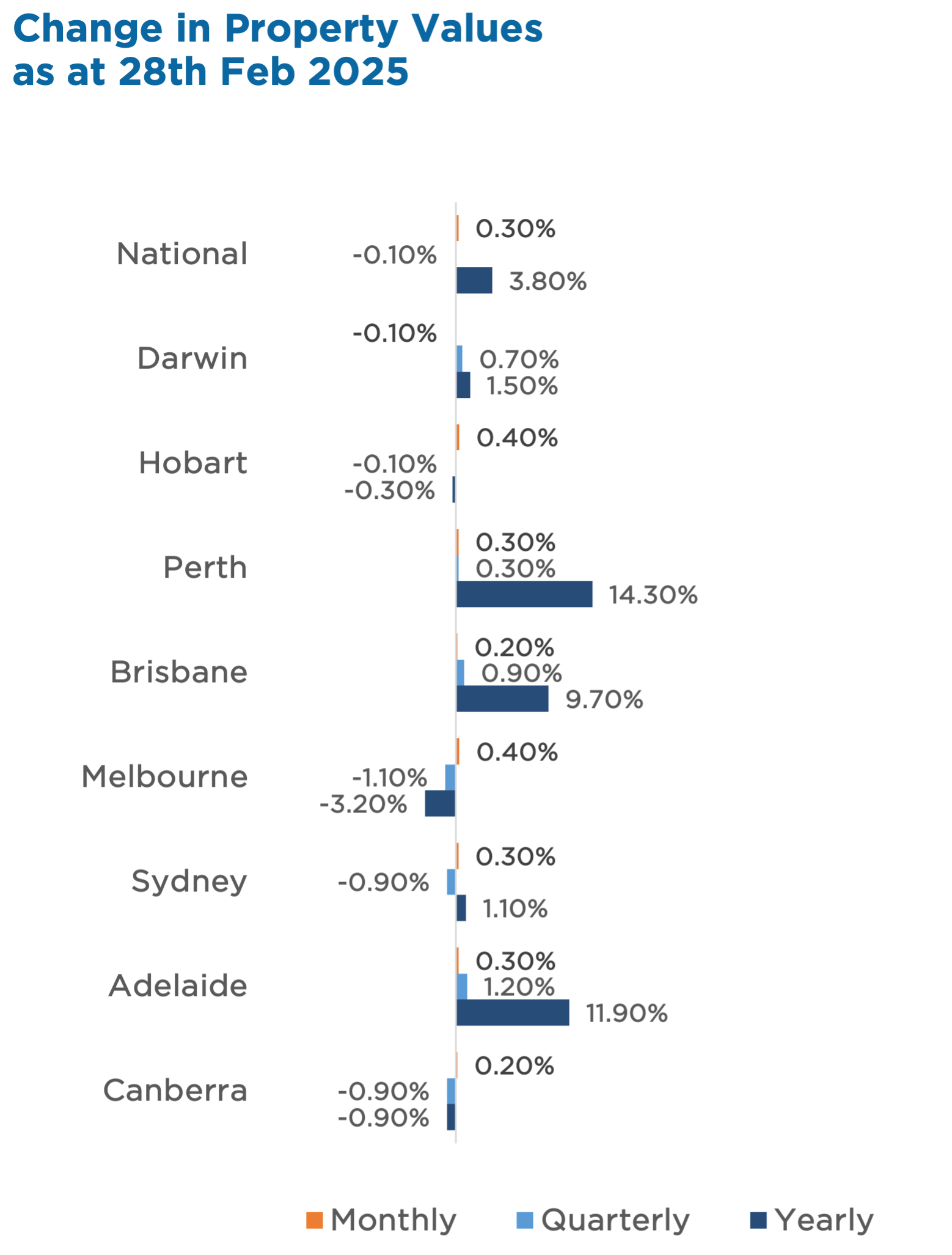

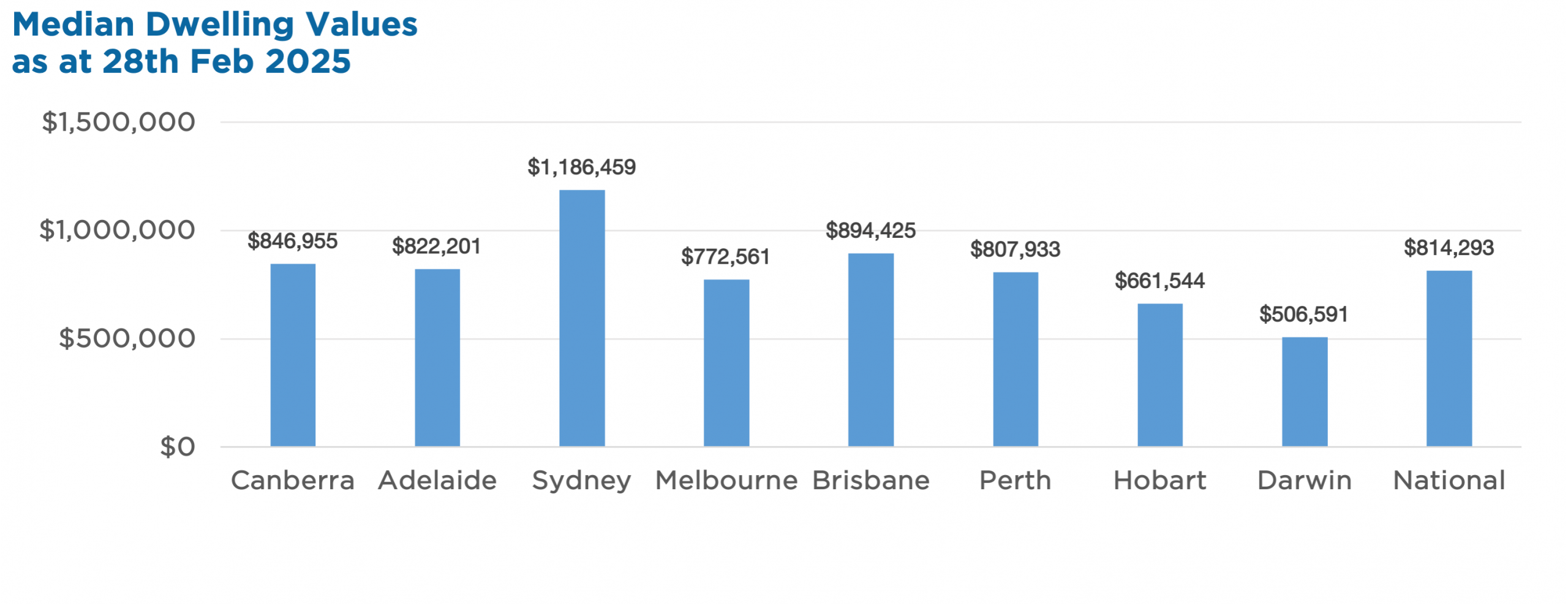

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund March 2025 February marked a shift in Australia's housing market, with national home values rising 0.3%, ending a three-month downturn. Gains were widespread, with Melbourne and Hobart leading at +0.4%, while regional markets continued to outperform, rising 0.4% for the month and 1.0% over the quarter. This renewed momentum aligns with improving buyer sentiment, supported by tighter housing supply and a slowdown in new listings, which remain 4.7% lower year-on-year. Auction clearance rates have also strengthened, reflecting growing confidence in the market. While affordability remains a challenge, supply constraints and positive sentiment could support continued price growth in the coming months. Investors monitoring market trends should note the shifting dynamics, particularly in premium housing markets, which have historically been the first to respond to changing economic conditions. Property Values

|

7 Apr 2025 - Manager Insights | Euree Asset Management

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Winston Sammut, Property Director at Euree Asset Management. They discuss the global market reaction to Donald Trump's tariff announcements, as investors shift to safer assets amid rising uncertainty, falling interest rates, and fears of a trade war, with flow-on effects for REIT valuations and broader market sentiment.

|

4 Apr 2025 - Hedge Clippings | 04 April 2025

|

|

|

|

Hedge Clippings | 04 April 2025 It's difficult to add anything new to the commentary about Donald Trump's "Liberation Day" that hasn't already been said or written. Outside his immediate circle of acolytes, seemingly led by Commerce Secretary Howard Lutnick, we have struggled to find any positive commentary from any corner of the world, (including the economic powerhouse of Norfolk Island) or in any language that supports Trump's upending of the world's economy. Except two: Russia and North Korea. Go figure? Ronald Reagan and every other US president since WWII would be turning in their grave. To be fair, although Norfolk Island was singled out in Trump's Rose Garden ramble, by the time the official list was released, someone had realised there's stupid, and then there's plain dumb, and thus Fletcher Christian's descendants were spared - yet again. One assumes that in due course the results of Trump's "genius" (his words, not ours nor it seems anyone else's) will come back to bite him where it hurts most - his ego and the ballot box. Unfortunately his self esteem/adoration is such that he probably won't notice when it does, and in spite of his best efforts, a third term seems out of reach. Not that the US constitution will stop him from trying. So Australia, and the rest of the world, (except as above, Russia and North Korea) are left to try to decide how to respond to the US directly, and, at the same time, try to fathom how every other country's response will change the overall global economic landscape. One factor to consider is that Trump is obsessed with the trade of goods, where the US operates a deficit. In today's technological and service orientated world, the US has a services trade surplus - admittedly not sufficient to even the score, but he's quiet on that front. Trump will try to pick off individual targets. Maybe the world's best reaction is to coordinate their responses? It worked in 1939 (just, after a shaky start) when dealing with another predictably self-obsessed adversary, even if it did take the US a couple of years to join the fray, and only then when they had no other option, or possibly saw the tide turning. In the meantime, everyone else - along with the RBA - is left to ponder their reaction in uncertain times. For the record, if you can remember as far back as last Tuesday, the newly formulated board left rates on hold on April Fool's Day, just before Trump's Liberation Day. However, they did mention "uncertain" no less than five times, as well as devoting more than 50% of their media release to a section on the "Uncertain Outlook", before returning to the more familiar ground of "returning inflation to target" being the priority. Markets, and as a result, many fund performances, were negative in February and March, and April is certainly heading that way. We spoke with Euree Asset Management's Winston Sammut just before going to press, (see video below) and it is fair to say that with all his experience, he views the immediate outcome as "uncertain" (that word again) but not overly positive. News & Insights Manager Insights | Euree Asset Management Making sense of the banking sector | Airlie Funds Management |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

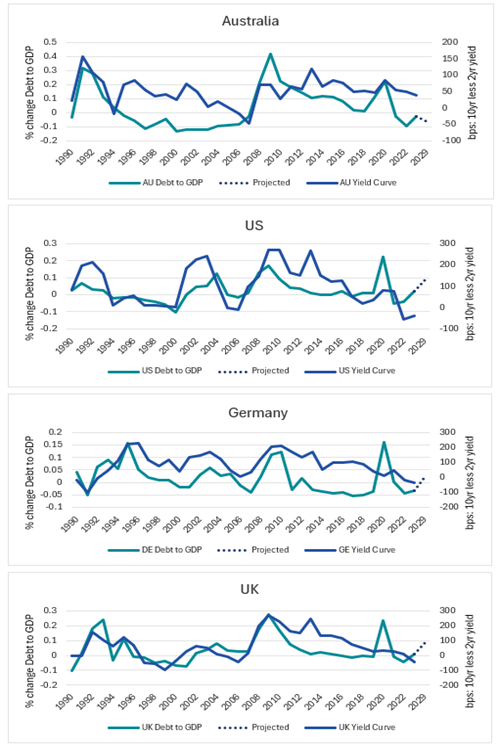

4 Apr 2025 - Spurious Correlations

|

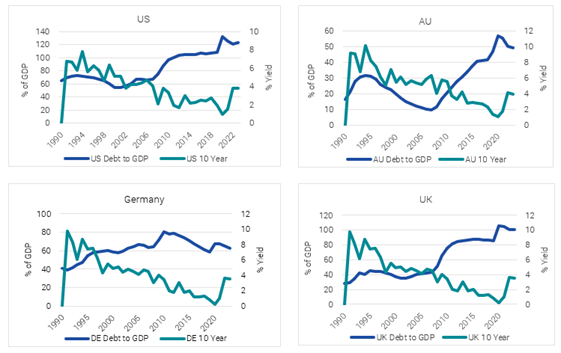

Spurious Correlations Yarra Capital Management March 2025 Debt size doesn't seem to matter!Major government borrowing events have typically been triggered by one-off crisis like the Global Financial Crisis (GFC) and COVID-19, not by interest rates. Before 2008, debt-to-GDP ratios were stable or even declining in many economies, suggesting governments borrow based on necessity, not borrowing costs. Looking at the US, Australia, Germany, and the UK (refer Chart 1), debt levels have risen, yet interest rates haven't followed suit. Germany, for instance, has kept debt-to-GDP in check, yet its bond yields have moved in line with other developed economies. Chart 1 - Debt-to-GDP vs. 10-year yields

|

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

3 Apr 2025 - Trumponomics: What tariffs could mean for small caps

|

Trumponomics: What tariffs could mean for small caps abrdn March 2025 The recent wave of tariffs imposed by President Trump, along with retaliatory measures from affected nations, has created a complex environment for businesses worldwide. While these trade disputes pose risks, they also present unique opportunities for certain US small-cap companies. At the core of Trump's tariff policies is the goal of protecting American industries and reducing trade deficits. Measures that will undoubtedly disrupt global supply chains, drive up the cost of imported goods, and create challenges for businesses reliant on foreign materials. They are expected to, however, incentivize domestic production, potentially benefitting small-cap companies that can step in to replace diminished imports. While not all firms will benefit, we believe companies with resilient business models, pricing power, and strong balance sheets will be best positioned to navigate these economic shifts. Reshoring and supply chain reconsiderationsOne of the primary ways tariffs could benefit small-cap companies is through the reshoring of manufacturing capacity. As tariffs make foreign goods more expensive, many US firms are adapting supply chain strategies to increase domestic sourcing and production. This shift presents new opportunities for smaller companies across a variety of sectors. For instance, reshoring projects will drive demand for local construction crews, concrete suppliers, and equipment rental firms. Regional banks will play a key role in financing these initiatives. Meanwhile, new semiconductor facilities will require specialised HVAC systems with nearby maintenance and repair services. By positioning themselves within these expanding domestic supply chains, small-cap companies stand to benefit from stronger revenue and earnings growth. Tariff-driven innovation and efficiencyAdditionally, tariffs have spurred innovation and efficiency improvements among small-cap companies. Many businesses are investing in automation, advanced manufacturing techniques, and other innovations to offset rising material costs to enhance productivity. These efforts help maintain margins and better position small-cap companies for long-term success. This is especially relevant for technology and industrial companies leveraging innovation to reduce dependence on foreign inputs and strengthen their competitive position. Reshaping the competitive landscapeCounter-tariffs imposed by other nations in response to Trump's policies have also played a role in shaping the competitive landscape. Countries like China have targeted US exports, impacting industries such as agriculture and automotive. While some small-cap exporters face headwinds, others have successfully pivoted to alternative markets. We believe companies that can adapt to shifting trade dynamics and diversify their customer base will be best positioned to thrive. The economic environment remains supportiveWhile we are mindful of the risks associated with recent policy actions, the broader economic environment remains supportive of high-quality small-cap stocks. Despite geopolitical uncertainty, GDP growth is expected to remain in positive territory. Also, many companies have already strengthened operations in response to past disruptions, such as the pandemic and volatility during Trump's first term. These efforts, such as diversifying supply chains and implementing efficiency initiatives, have better-positioned businesses to navigate potential tariffs and raw material inflation. Overall, the US economy is expected to continue expanding, albeit at a more modest pace. This environment allows resilient small-cap companies to capitalise on the new administration's 'America First' agenda while leveraging recent operational enhancements to mitigate near-term risks. ... Along with earnings growthAs we move through 2025, small-cap stocks are gaining attention for several reasons. Investors are increasingly looking to diversify, given the growing concentration of "Big Tech" in large-cap indices. The shift is timely, as small-cap companies are expected to deliver stronger earnings growth relative to their large-cap counterparts (Chart 1). This is an important development as small-cap growth rates have lagged large-caps for several years. Chart 1. Russell 2000 Index (RTY) vs. S&P 500 Index (SPX) positive EPS growth ... And attractive valuationsFurthermore, small-cap stocks are trading at attractive valuations, with their discount to large-caps near historic lows (Chart 2). Chart 2. Small cap relative to large cap forward price/earnings (PE) ratio While multiple factors have contributed to this valuation gap, earnings growth differentials have been key drivers. As small-cap earnings accelerate, this discount should begin to narrow, presenting a compelling opportunity for investors. Final thoughts...Trump's latest tariffs and the retaliatory measures from affected nations are reshaping the competitive landscape for US small-cap companies. While risks remain, the push towards domestic production, supply chain diversification, and innovation can drive earnings growth for many firms over the long term. Coupled with resilient economic conditions and historically attractive valuations, high-quality small-cap stocks present a strong investment opportunity for those looking to capitalise on evolving trade dynamics. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund, abrdn Emerging Opportunities Fund, abrdn Global Corporate Bond Fund (Class A), abrdn International Equity Fund, abrdn Multi-Asset Income Fund, abrdn Multi-Asset Real Return Fund, abrdn Sustainable International Equities Fund |