NEWS

12 May 2025 - Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

[Current Manager Report if available]

12 May 2025 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

12 May 2025 - The Resurgence of Nuclear Energy

|

News & Views: The Resurgence of Nuclear Energy 4D Infrastructure May 2025 Nuclear energy is undergoing a renaissance. While it has long been associated with images of devastation and disaster, it is now increasingly recognised as a crucial part of the global energy transition, offering a reliable solution to rising energy demand and decarbonisation efforts. In this edition of News & Views we examine the decline of nuclear energy, the catalysts behind its resurgence and how the 4D investment strategy captures exposure to this evolving theme. Why did nuclear decline?1. Public fearAt its peak in the late 1990s to early 2000s, nuclear energy accounted for nearly 17% of global electricity generation, compared to around 9% today. Incidents like Three Mile Island in the US in 1979 and Chernobyl in 1986 increased public anxiety around nuclear energy. While both these incidents resulted in greatly increased safety regulations and oversight, the stigma remained. The 2011 Fukushima disaster in Japan reignited safety concerns, resulting in several countries scaling back or halting their nuclear programs. The US for example increased regulatory scrutiny while Germany decided to exit nuclear power altogether. 2. High costs and complex constructionHigher safety standards and regulatory obligations have made nuclear projects increasingly expensive. The need for more advanced safety systems, robust containment structures and ongoing design and regulatory changes have all increased the cost to build, operate and maintain nuclear power plants. Project management complexities have also been detrimental. With less nuclear plants being built, the industry experienced a loss of skilled labour and expertise in nuclear construction. This, coupled with the incredible complexity yet lack of standardisation in plant build, has also led to increased inefficiencies and costs. As a result, many of the more recent nuclear power plant projects have seen significant delays and cost overruns. Examples include:

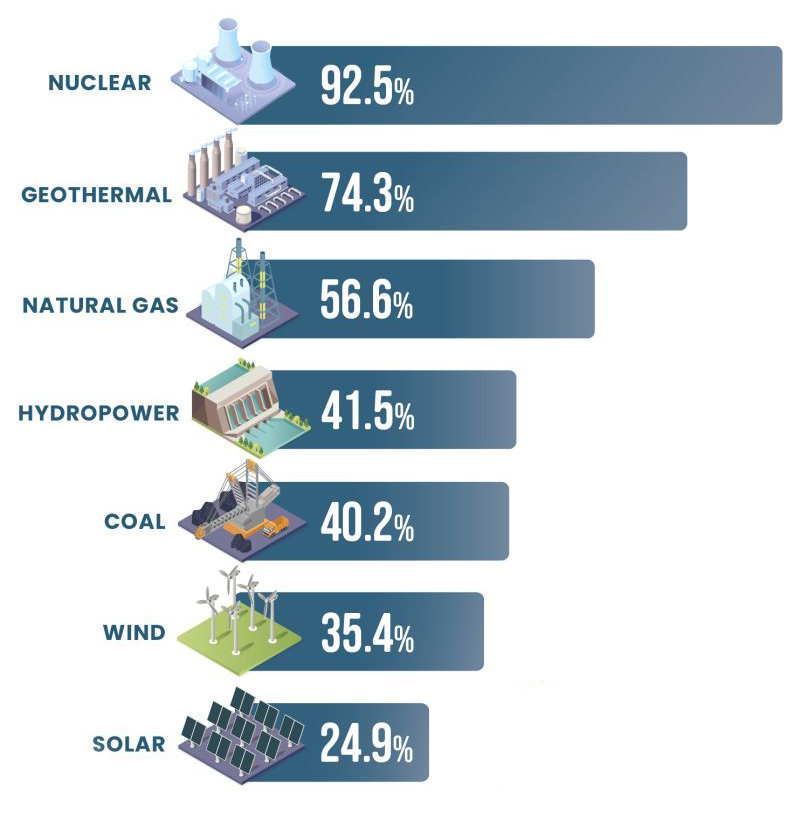

What's driving nuclear's revival?1. Reliable, carbon-free baseload powerNuclear energy offers continuous, emissions-free power -- a valuable complement to intermittent renewables like wind and solar. While wind and solar energy are expanding, they remain intermittent, generating electricity only when the wind blows or the sun shines. Managing this intermittency requires energy storage to store excess energy during high-output periods and release it during high-demand or low-generation periods. Even though storage technology and deployment has grown rapidly, costs remain too high to implement at scale. At the same time supply pressures are increasing as coal and gas-fired power plants being phased out or growing more slowly. This is why nuclear energy stands out as the only large-scale baseload power source that can reliably bridge the supply gap, combat climate change and avoid the intermittency challenges of other renewables. Capacity Factors across various energy sources

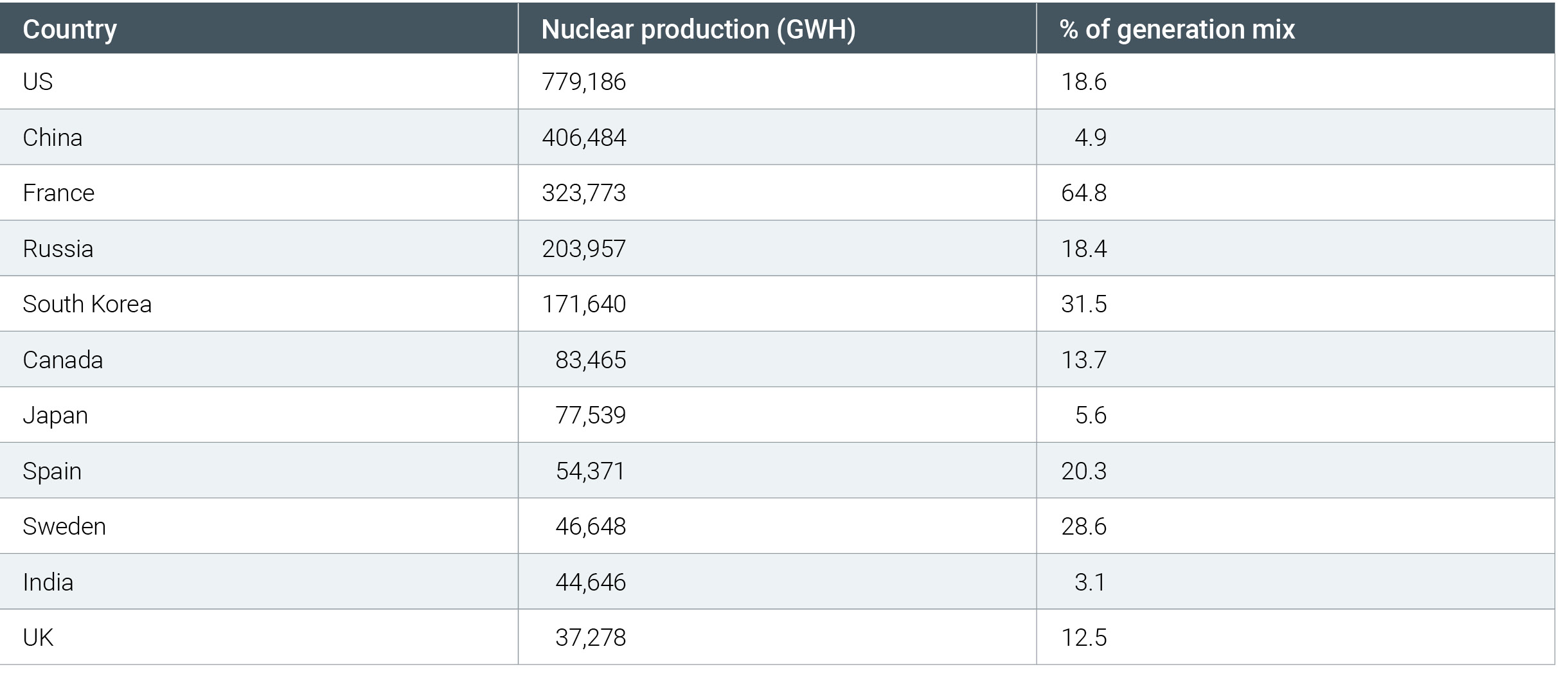

It is important to note that even with safety and cost concerns, nuclear continues to be a pivotal component of the electricity generation mix for many countries. For example, in France, where nuclear accounts for approximately 65% of the generation mix, power prices have remained relatively low compared to other European countries. The relatively low cost of nuclear power generation has also contributed to France becoming one of the world's largest net exporters of energy, bringing in €5bn in revenues in 2024.1 Recognising the value of nuclear power assets, France plans to replace its aging nuclear fleet with six new reactors by 2050, with an option for an additional eight. Nuclear Production 2023 and Proportion of Generation Mix

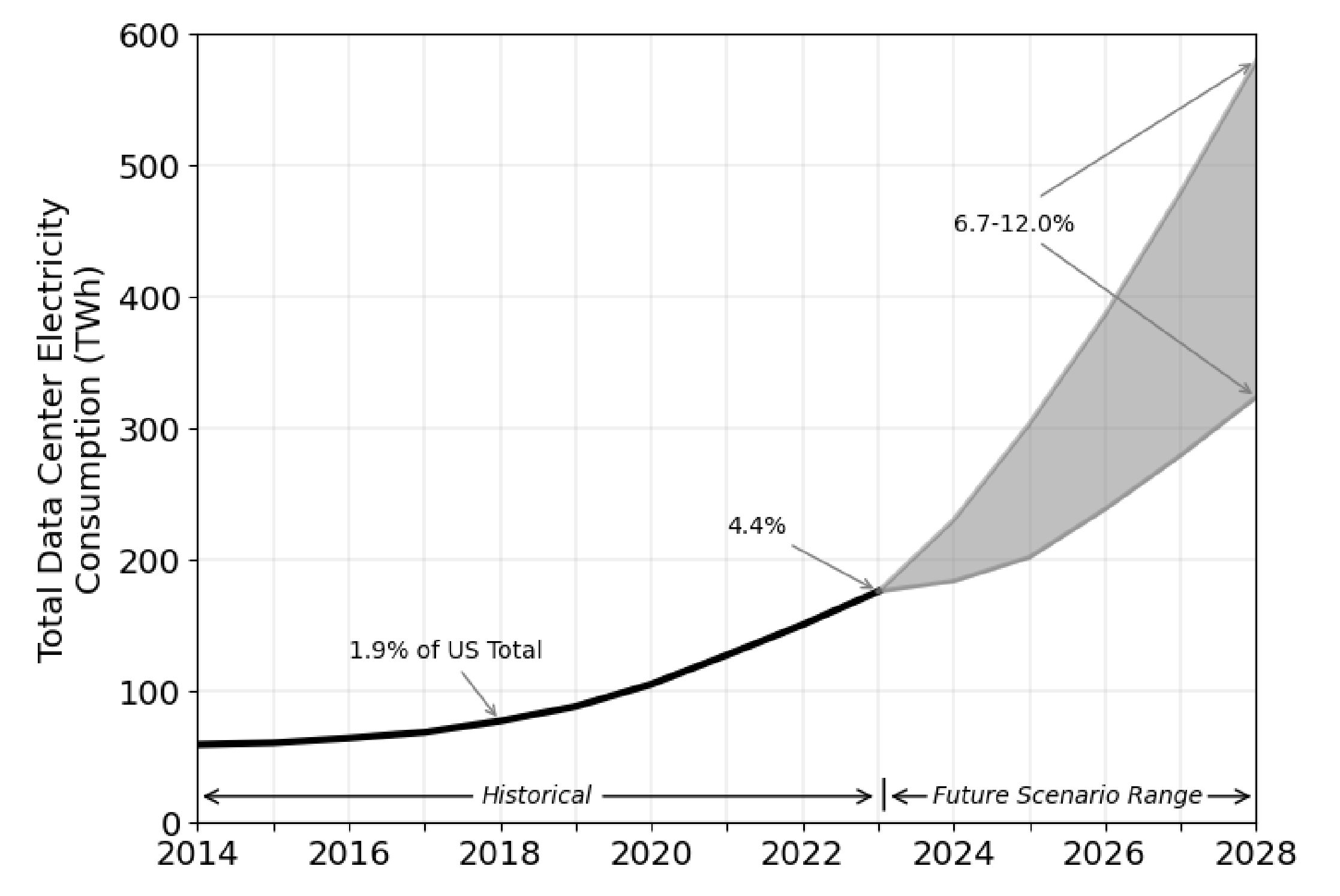

2. Rising demand from electrification and AIElectricity demand, previously growing modestly (~1% per year in the US), is now accelerating due to manufacturing onshoring, electrification and surging AI data centre usage. While estimates of demand growth are difficult to quantify, it is estimated that over the next five years the US will see load growth of at least 3%3, with further upside potential as data centre demand increases alongside demand for AI computing. Government reports project US data centre demand leaping from 176TwH in 2023 to 325-580TwH in 2028.4 This equates to between 6.7% and 12% of total US electricity consumption - up from 4% currently.5 Estimated data centre consumption growth

3. Hyperscaler investment'Hyperscalers' (large technology companies using data centres for cloud computing and data management services) are turning to nuclear energy due to its ability to provide 24/7 secure base load power for data centres while also aligning with their significant carbon reduction goals. The main drawback of nuclear power for hyperscalers is build time: with planning and construction times of over 10 years along (notwithstanding time and cost blowouts (as set out above). These long lead times conflict with hyperscalers' ambitions to deliver nascent high-profile AI technologies as soon as possible. As an alternative, hyperscalers have focused on leveraging existing nuclear capacity and exploring innovative reactor designs to mitigate cost and construction times. This is demonstrated through examples from key hyperscalers including:

4. Policy supportGovernment policy is increasingly supportive. The US Inflation Reduction Act (IRA) is the most prominent example, with the Act containing several tax credit provisions that serve to boost nuclear's financial viability. Examples include:

Nuclear's investment caseWe anticipate continued growth in nuclear demand, driven by AI-related consumption, supportive policies and decarbonisation mandates. Given the long lead times and high costs of new build, leveraging existing capacity remains the focus. Translating this to investment decisions4D supports the nuclear theme as part of the Energy Transition. However, for us to take exposure the underlying assets must meet our infrastructure definition by either being 'regulated' or 'contracted'. One or both of these arrangements serves to secure the investment and operating costs of the plant as well as the return to the shareholder. At 4D we have nuclear power generating exposures across multiple US utility investments, but most prominently through our investment in Dominion Energy (D). Dominion owns regulated nuclear facilities in Virginia and South Carolina, as well as the Millstone Nuclear Power Station in Connecticut, which the company is exploring contracting opportunities for. We also have exposure through European utilities including Iberdrola [IBE] who have some legacy nuclear exposure in Spain. We are also closely monitoring nuclear-exposed Independent Power Producers (IPPs) like Constellation Energy, Talen and Vistra. While these stocks appeal in different ways, they currently either lack the cash flow visibility we require in our investments or lack a compelling enough risk-reward proposition amid stretched valuations. Case Study: Millstone nuclear power plantOwned by Dominion Energy, the Millstone Nuclear Power Plant (Millstone) is based in Connecticut, US, and has an operating capacity of 2GW across units 2 and 3. The power station began operating in 1975 and has an operating license from the US Nuclear Regulatory Commission (NRC) until July 2037 and November 2045 for Units 2 and 3 respectively. The power station provides around 47% of Connecticut's power needs, more than 90% of the state's carbon-free power and employs around 4,000 people. Until March 2019, Millstone sold 100% of its capacity into the ISO New England merchant energy market in the northeast of the US. Prior to the Covid-19 recovery, benign growth in power demand from customers (around 1% annual demand growth for the previous decade), combined with cheaper forms of alternative energy generation (such as renewables and natural gas), meant the merchant price of power earned by Millstone was uneconomic compared to the running costs of the facility. The load-weighted average prices achieved in 2016, 2017 and 2018 were $34.62/MWh, $37.45/MWh and $52.27/MWh respectively. Dominion management lobbied Connecticut legislators and regulators, stressing they would have to decommission Millstone if the state didn't provide some form of financial support as low and volatile market prices meant the facility was loss making. In response, the Connecticut regulator, PURA, signed a fixed price agreement with Dominion for approximately half of Millstone's capacity, for a maturity of 11 years (to 2029). The price within the contract was $49.99/MWh, well above the prevailing market price achieved for the facility. This contract supported the financial viability of Millstone and incentivised Dominion to continue operating the facility. Fast forwarding to the current environment, the northeast US power market is now in short supply, driven by the aforementioned strong demand growth from data centres, onshoring of manufacturing and wider electrification efforts. This has resulted in much higher market prices with capacity contracts agreed with data centre companies at prices rumoured in excess of $100/MWh. The carbon-free, firm power capacity provided by nuclear facilities like Millstone are particularly sought after by tech companies. Dominion management are now considering options of what to do with the uncontracted capacity of the facility, and potential utilisation of capacity post expiry of the agreement with PURA in 2029. 1 https://energynews.pro/en/france-reaches-a-record-e5-billion-in-electricity-exports-in-2024/ The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. Funds operated by this manager: 4D Global Infrastructure Fund (Unhedged), 4D Global Infrastructure Fund (AUD Hedged) |

Source: US Energy Information Administration

Source: US Energy Information Administration Source: NEI, IAEA-PRIS 2

Source: NEI, IAEA-PRIS 2 Source: Berkeley Lab - 2024 United States Data Center - Energy Usage Report

Source: Berkeley Lab - 2024 United States Data Center - Energy Usage Report Source: U.S. Department of Energy

Source: U.S. Department of Energy

9 May 2025 - Hedge Clippings | 09 May 2025

|

|

|

|

Hedge Clippings | 09 May 2025 Although last week's Hedge Clippings described the election campaign as boring, disappointing and uninspiring, the outcomes and after-effects have been anything but. Anthony Albanese's victory was decisive and well deserved, even if he was ably assisted by Peter Dutton and Adam Bandt, who each contributed to Albo's success, and their own eventual demise. To what extent Dutton was supported (probably the wrong term) by the Liberal party hierarchy, or the executive and his inner circle, we'll no doubt have to wait to find out when the inevitable post-mortem is held or books are written. Treasurer Jim Chalmers summed it up on election night when he said he "couldn't believe his luck" when his opposite number announced they would vote against his across-the-board tax cuts, even though in actual dollar terms it amounts to $268 in 2026-27, and $536 in 2027-28. That's enough for one cup of coffee a week next year, and two cups the year after. We can't wait! Where the Libs go from here is anyone's guess, but if they continue to listen to the right wing of the party (or Gina Rinehart, who'd like them to be more like Trump), they're going to remain where they are, or worse, for the foreseeable future. Which, sadly, is not good for democracy. As it is, we have to hope that success will not go to Albo's and the loony left's head, and that ideas such as taxing unrealised capital gains won't spread beyond super balances above $3 million. Our guess, however, is that they will. Bottom line, congratulations to Albanese. He's only 62, so short of another Hawke/Keating type deal, Jim Chalmers will have to wait at least three years, and possibly six. So back to the real world, where they probably couldn't give a fig to Australian's antics of the past few weeks. As pointed out by PinPoint Economics' latest report (and chart pack), tariffs and trade wars are the focus of economic and political debate at present. To quote PinPoint's Executive Summary, the parameters shift on an almost daily basis, such that there's a need to cut through to the underlying fundamentals and work out what to watch.

However, the most pertinent aspect is PinPoint's view that the parameters shift on an almost daily basis. Trump's style is to come out all guns blazing in an attempt to get the upper hand - or to achieve maximum exposure, or both. What the final outcome will be once he's chopped and changed his terms on a country-by-country basis remains to be seen. First cab off the rank is the UK - (The Donald's obviously keen to make sure his invitation to Buckingham Palace is still secure), where he's kept a 10% tariff in place in spite of the US enjoying a trade surplus (like Australia) with the UK. He's also hinted that the 145% tariffs on China will be watered down, and that the White House is in talks with dozens of other countries. Trump has been less successful buying Canada and Greenland (so far), nor has he stopped the war in Ukraine or Palestine. Everything remains uncertain, making Australia a relative oasis of calm! News & Insights 10k Words | Equitable Investors Market Commentary | Glenmore Asset Management April 2025 Performance News Seed Funds Management Hybrid Income Fund Bennelong Australian Equities Fund Bennelong Long Short Equity Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

9 May 2025 - Performance Report: Quay Global Real Estate Fund (Unhedged)

[Current Manager Report if available]

9 May 2025 - Performance Report: Bennelong Long Short Equity Fund

[Current Manager Report if available]

9 May 2025 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

9 May 2025 - Are You In The Matrix?

|

Are You In The Matrix? Marcus Today April 2025 |

|

Have you been told to "buy and hold"? "It'll be fine in the long run"? "You can't time the market"? You might be in the matrix. In this video, Marcus breaks down the truth behind the mantras the finance industry repeats - not to help you, but to keep you quiet. If you've ever felt like the advice doesn't quite match reality... you're not alone. DISCLAIMER: This content is for general information purposes only and does not constitute personal financial advice. Please consider your own circumstances or seek professional advice before making investment decisions. |

|

Funds operated by this manager: |

7 May 2025 - Sustainability: Is this the end for sustainable investing?

|

Sustainability: Is this the end for sustainable investing? abrdn April 2025 This is a crucial year for sustainable investing. With a heady mix of regulatory change, political backlash and changing sentiment, we ask whether it's over for sustainable investment? Investors who have set interim climate targets for 2030 have less than five years to achieve them. But even with an increase in the regularity and severity of extreme weather events, many investors have faced a political backlash against climate change and sustainable investing. These developments have accelerated in recent months with a drastic shift in the US political climate. This has led to big-name US asset managers and companies abandoning climate commitments and rushing to roll back on diversity, equity and inclusion (DEI) pledges. But behind the headlines, we see a more nuanced evolution of the sustainable investing world - one in which demand for sustainability strategies remains strong. This is being driven by institutional investors demanding bespoke solutions to meet specific goals and these asset owners are backing up their talk with action. Transatlantic splitThe US and Europe are heading in opposite directions. Political pressures have led to a retreat from sustainable investment in the US, while Europe largely remains committed. President Donald Trump plans to dismantle the previous US administration's measures to promote sustainability and wants to increase coal, oil and gas exploration on federal land - his recent executive orders demonstrating his intent. He has weakened the Environmental Protection Agency and pulled the US out of the Paris climate agreement. Some US asset managers, facing legal challenges, have turned their backs on climate targets and withdrawn from international climate initiatives, such as the Net Zero Asset Managers and the Climate Action 100+ initiatives. But across the Atlantic, it's almost business as usual for a region that has long been at the vanguard of international efforts to promote sustainability and sustainable investing. Last December, regulators there started applying the European Union's (EU) Green Bonds regulation. These rules aim to clarify eligibility criteria on what qualifies in the EU as a 'green bond'. The goal is to improve investor protection by preventing 'greenwashing'. It's not all plain sailing even in the EU. In a bid to boost competitiveness, Europe's Omnibus package rolls back flagship sustainable investment policies including the Corporate Sustainability Reporting Directive and the Corporate Sustainability Due Diligence Directive, amid proposals to dilute the region's Sustainable Finance Disclosure Regulation. This divergence in philosophy amid pressures to weaken existing measures complicate global operations for asset managers and asset owners alike. It is simply no longer possible to operate with a one-size-fits-all approach. Big investors lead the wayThat said, many institutional investors continue to demand sustainable investing strategies. This isn't always obvious, but it is a critical component of the current investment landscape. In February, a group of 27 asset owners - primarily from the UK but also representing European, Australian and US investors - signed the 'Asset Owner Statement on Climate Stewardship' to reinforce their support for sustainability principles and to spell out what they expect from fund managers. There is growing demand for tailored investment solutions. While these are predominantly focused on asset owners looking to meet their climate targets, there is also interest in deploying strategies to protect natural environments in bespoke, or 'segregated', mandates. In our own assets under management, those we classify as 'sustainable' investments, grew to £87 billion (US$112.4 billion) by end-2024 from £55 billion a year earlier. This increase was largely attributable to segregated sustainable investment mandates. We are also seeing cases in which asset managers who turn away from sustainability goals may be punished by some asset owners. For example, both the UK's People's Pension and Denmark's Akademiker Pension pulled mandates from one US fund manager amid disagreements over climate stewardship. DEI requires diverse solutionsCompanies employ DEI policies for reasons including employee wellbeing, legal compliance and enhancing brand image. But critics equate DEI with the prioritisation of identity over competence. Many US companies have been diluting or scrapping their DEI policies in response to Trump's executive order on DEI and to avoid litigation. DEI-related quotas and affirmative-action programs have been under particular scrutiny. Opponents say they are discriminatory and that employees hired through these initiatives have not been chosen on merit. Some firms have removed gender quotas on boards, for example. The response from asset managers has been mixed amid a growing number of DEI cases going to court. While some have gone quiet on DEI, other fund managers continue to engage with companies and deepen long-term relationships to drive improvements in this area. The changes companies are making with regards to DEI, as a result of navigating new pressures and expectations, is yet another facet of the evolving nature of sustainability investing in a complex world. Final thoughtsMany recent headlines have painted a grim picture for sustainable investing, with phrases like 'sustainability in crisis' making the rounds. There's no doubt that the honeymoon for sustainable investing is over. However, a closer look reveals a more nuanced story. A hostile political environment in the US makes it more difficult to follow sustainable investment principles there. However, the demand for sustainability strategies remains strong, especially from institutional investors who remain committed to achieving sustainability targets and need customised investment solutions. Once the marketing hype is stripped away, sustainable investing has always been fundamentally about financially-material issues. These issues continue to be critical regardless of the political whims of the day. This is why asset owners, as long-term investors, remain committed. This is why there are opportunities for those investors who can navigate this complex landscape. Sustainable investment is not dead - it is reforming and evolving to meet the demands of a changing world. It took over 100 years to secure agreement on globally-accepted accounting principles. We are trying to achieve the same thing with less time and as the world gets hotter each year. Is it any wonder there are a few bumps along the road? |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund, abrdn Emerging Opportunities Fund, abrdn Global Corporate Bond Fund (Class A), abrdn International Equity Fund, abrdn Multi-Asset Income Fund, abrdn Multi-Asset Real Return Fund, abrdn Sustainable International Equities Fund |

7 May 2025 - Tim Hext: Art of the deal or new world order?

|

Tim Hext: Art of the deal or new world order? Pendal April 2025 |

|

PRESIDENT TRUMP's "reciprocal" tariffs caught many - me included - by surprise last week. Until then, I mistakenly believed tariffs were all part of the art of the deal. Tariff talk, which was seen as a tactical ploy to get a better deal for the US, suddenly seemed to have larger ideological aims. How else can you explain the ridiculous calculation method for reciprocal tariffs? There is still a lot of water to go under the bridge in the weeks and months ahead as negotiations go bilateral - but understanding Trump (always a difficult exercise) will help navigate markets. When China entered the World Trade Organisation in 2001, the US trade deficit with China was $84 billion. The US had a $300 billion deficit overall in manufacturing. Over next two decades, the manufacturing deficit grew $1 trillion to $1.3 trillion by 2022. China accounted for almost $600 billion of this growth. Overall, this was seen as a win/win. China got to develop on the back of hard work and exporting to the US. And US consumers got plenty of cheap goods from China, protecting a standard of living in the face of slow wage growth. The bonus for the US was that in an attempt to keep its currency lower, the Chinese government bought US dollars and became huge buyers of US Treasuries. Its FX reserves went from $300 billion to over $3 trillion during this period. Let's not forget the most important thing: since 2000, around 500 million Chinese people have emerged from poverty to middle incomes. By 2018, however, geopolitics started to kick in. As China started to flex its muscle globally, not all in the US were happy. The narrative began to change. In his first term, Trump launched a trade war with China, causing negative equity returns. Helping the Chinese economy was now seen as a negative, not a positive. That trade war now seems tame. It seems the narrative from Trump is effectively that the US can handle some pain if it means achieving a longer-term new world order. The US will retreat back to some supposed golden age. Time will tell. Implications for bond marketsAs evidenced this week, all these actions from Trump are a mixed bag for US bonds. Firstly, economic weakness should mean Fed cuts and rallies in bonds. However, tariffs will mean higher inflation - at least near term. Throwing more confusion into the picture is foreign buying (or more likely selling) of US bonds. Smaller trade deficits mean smaller capital surpluses and therefore, at best, smaller inflows into US capital markets. Where it gets more interesting, though, is the weaponisation of financial flows - not just trade flows. Rumours have been circling that China is dumping part of its US Treasury holdings. Other countries may follow - after all, like any investments, you want to know the CEO knows what they are doing, and simply put, credibility and confidence has evaporated. Who would want to lend money to an entity that is acting so aggressively against your interests? Therefore, the flight to quality is more of a flight to cash and short bonds, not long bonds. Yield curves are steepening faster than economic fundamentals suggest. It was only late last year when US exceptionalism became the investment theme for this decade. That exceptionalism remains but is quickly being redefined from a positive to a negative. Implications for our portfoliosWe have been leaning into duration for a number of months, but are very disappointed by the lack of a reaction from our long end. Short-end duration has worked, but unlike Covid and the GFC, the long end has been left behind. The RBA will also be cautious. The expected low CPI print on 30 April will give the central bank cover to cut at its 20 May meeting, but unless it keeps getting worse, its recent form suggests only a 25-basis-point (bps) cut. It will then adopt a wait-and-see approach for how it all impacts Australia. But given there are six weeks till then, markets are right to price some risk of a larger cut - though, current levels of 40bps of cuts looks a little too much. The random nature of announcements mean we are generally keeping risk close to home. Our caution around credit means we are avoiding the major drawdowns that will be hitting more aggressive investors. Now is not the time to charge in. However, we are still looking for relative value opportunities in a volatile market to keep adding value in these stressed times. LiquidityAnd just like that - liquidity in many sectors dries up in a puff of smoke. Our portfolios at Pendal Income and Fixed Interest have always operated at the more liquid end of markets. We leave the less-liquid, high-yield chasing to others. Government bonds remain highly liquid. Semi-government bonds are hanging in there though bid/offers are widening. You can transact senior bank paper assuming manageable size and paying a wider spread. However, as we have often warned, beyond there it gets very tricky. Everything is liquid in good times, but it is a shortlist in a time of crisis. The RBA sets the liquidity rules and its world is one of cash, bank bills/NCDs and government bonds (all known as High Quality Liquid Assets). These remain open for business, but beyond that point, it is buyer-beware for liquidity. Author: Tim Hext |

|

Funds operated by this manager: Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Multi-Asset Target Return Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Pendal Sustainable Australian Share Fund, Regnan Credit Impact Trust Fund, Regnan Global Equity Impact Solutions Fund - Class R |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |