NEWS

15 Jan 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|||||||||||||||||||||

| T. Rowe Price Global Equity (Hedged) Fund - I Class | |||||||||||||||||||||

|

|||||||||||||||||||||

| View Profile | |||||||||||||||||||||

| T. Rowe Price Dynamic Global Bond Fund S Class | |||||||||||||||||||||

|

|||||||||||||||||||||

| View Profile | |||||||||||||||||||||

| T. Rowe Price Dynamic Global Bond Fund I Class | |||||||||||||||||||||

|

|||||||||||||||||||||

| View Profile | |||||||||||||||||||||

|

|||||||||||||||||||||

| Perpetual Balanced Growth Fund | |||||||||||||||||||||

|

|||||||||||||||||||||

| Perpetual ESG Real Return Fund | |||||||||||||||||||||

|

|||||||||||||||||||||

| Perpetual Diversified Real Return Fund - Class Z | |||||||||||||||||||||

|

|||||||||||||||||||||

| View Profile | |||||||||||||||||||||

|

Want to see more funds? |

|||||||||||||||||||||

|

Subscribe for full access to these funds and over 790 others |

21 Dec 2023 - What is the Fed's Senior Loan Officer Survey and what is it telling us?

|

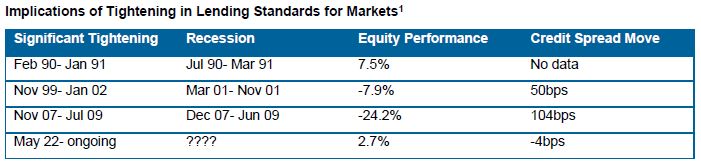

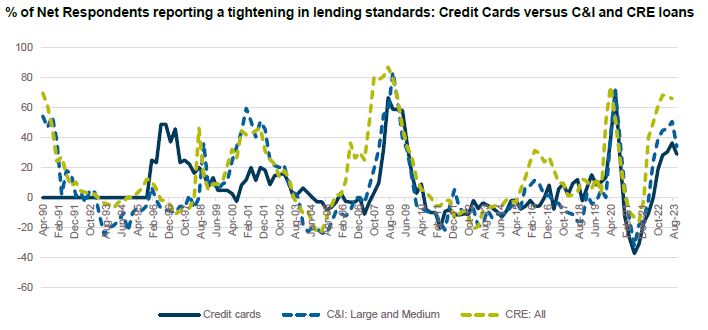

What is the Fed's Senior Loan Officer Survey and what is it telling us? Challenger Investment Management November 2023 The financial system of the United States is unique. Unlike Australia where households and institutions are at the mercy of the four major banks, the US banking system is highly dispersed. There are over 4,000 commercial banks and over 500 savings and loan associations. The top 4 banks represent less 50% of total assets in the banking system; in Australia this figure is over 70%. With so many individual lenders, the Federal Reserve Board (the Fed) conducts a quarterly survey to gauge the degree to which financial conditions are changing. This is called the SLOOS, the Senior Loan Officer Opinion Survey on Bank Lending Practices. The survey polls up to 80 large domestic banks and 24 branches of individual banks. The questions address the degree to which banks are tightening lending standards, how the demand for credit is evolving as well as how the pricing of credit risk is changing. The results of the survey are reported to the Federal Open Market Committee (FOMC) and feed into monetary policy decision making. The survey has been repeatedly shown to have high predictive content with a tightening in lending standards being strongly correlated with a slowing in GDP growth. In this month's "What We're Watching" we take a closer look at the Senior Loan Officer Survey in an attempt to identify the degree to which standards are tightening and where the tightening is most acute. Observation 1: Previously when banks tightened by as much as they have done to date, a recession has followed A challenge in interpreting the survey data is that the questions asked of the banks have binary responses with the measure tracking the net percentage of respondents answering in the affirmative. It gives no indication as to the degree to which standards were tightened or pricing increased. There are also small biases in responses; for example, a bias towards tightening of credit standards with an average 6% of net respondents indicating tightening for C&I loans since 1990. Since 1990 there have been 4 periods of significant tightening in credit standards (which we define as 4 consecutive quarters where 20% or more of net respondents reporting tightening in standards for C&I loans). All 3 previous periods of significant tightening in credit standards were followed by a recession and in two of the 3 a selloff in credit and equity markets.

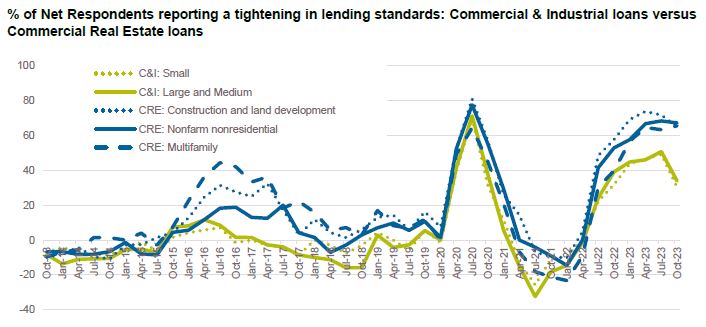

There have also been several periods where banks have meaningfully loosened credit standards. The mid 1990s (mid 93 to mid 95) and mid 2000s (early 04 to mid 06) saw extended periods of loosening lending standards. More recently banks loosened lending standards from early 2021 to mid 2022 including the most negative net percentage of respondents reporting tightening on record; -32.4% for the quarter ended Jul-21 (although it is arguable that some of this loosening was a reversal of the sharp tightening we saw when COVID hit). Our take is that the tightening in lending standards is not over. While standards were not excessively loose in 2022, we think the tightening will eventually weigh on risk markets. Observation 2: pricing on C&I loans is increasing The SLOOS also asks banks whether they are increasing spreads of loans over the Banks' cost of funds. Historically banks have had a slight bias towards tightening pricing albeit with responses being far more volatile than responses around lending standards. Interestingly the correlation between tightening in lending standards and changing spreads is only around 60%. Banks tend to reach a point where they are unwilling to loosen lending standards any further but are still willing to compete on price. For example, banks tightened pricing on C&I loans for longer periods than they loosened credit standards; from early 1993 to mid 1998 and from mid 2003 until mid 2007, respectively. In contrast, when standards tighten banks tend to also widen pricing concurrently. The widening in pricing has two effects - it further exacerbates credit pressure on borrowers, especially when combined with the significant increase in base interest rates. Secondly it creates opportunities for alternative lenders to disintermediate the banks. Observation 3: CRE lending standards are far tighter than C&I lending standards Commercial real estate (CRE) lending standards have tightened by far more than commercial and industrial loans. Demand for credit has also declined to levels not seen since the Global Financial Crisis (GFC). Even sectors such as Multifamily which are performing relatively well in a fundamental sense are experiencing a sharp tightening in lending standards.

To date, non-farm non-residential CRE lending has experienced 5 consecutive quarters where more than 50% of net respondents have tightened lending standards. The longest such period on record was the GFC with 7 quarters. No other period since 1990 has seen more than 2 consecutive quarters of >50% net respondents tightening credit standards. Observation 4: The consumer is still okay The survey data for credit cards implies a far less severe tightening in credit standards. The leadup is similar with the 2020 tightening and 2021 loosening in credit standards tracking closer to C&I and CRE loans but paths diverge in late 2022. New and used auto loans have experienced even less of a tightening in standards than credit cards.

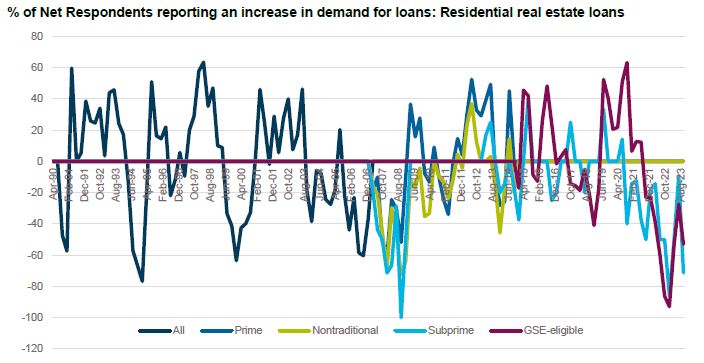

Residential mortgages, the epicentre of the GFC, have also not experienced a material amount of tightening in credit standards. Demand for consumer credit, both secured and unsecured has also not picked up materially with a reduction in demand being reported for auto loans and consumer loans ex credit cards and auto loans. However, demand for mortgages has fallen to GFC lows, in large part due to mortgage rates which are around 8%, levels not seen for more than 20 years.

Domestic survey data While APRA does not collate consolidated survey data on lending conditions, several banks conduct their own surveys. NAB completes a quarterly survey on commercial property markets where borrowers have reporting difficulties in accessing credit with availability in line with pre-COVID levels. This suggests that while credit standards for real estate lending are tightening in Australia, they are not tightening at the same pace as in the United States.

In conclusion... Despite the relatively benign indications in Australia, the SLOOS implies a far sharper tightening in credit conditions especially in commercial real estate lending markets. Pricing of risk is also heading higher. While we don't necessarily expect tighter lending conditions in the US to flow directly to Australia (in aggregate our banks are in a stronger capital and liquidity position than the US banking system), we do think the tighter conditions in the US may precipitate an increase in risk premiums across markets. After all, when the US sneezes, the rest of the world catches a cold. Funds operated by this manager: Challenger IM Credit Income Fund, Challenger IM Multi-Sector Private Lending Fund For Adviser & Investors Only [1] All the data in this report is sourced from the SLOOS which is produced by the Federal Reserve. https://www.federalreserve.gov/data/sloos.htm |

20 Dec 2023 - Investment Perspectives: 12 surprising charts for your Christmas stocking

19 Dec 2023 - The 'low emissions' megatrend: Is it too early to invest in green hydrogen?

|

The 'low emissions' megatrend: Is it too early to invest in green hydrogen? Insync Fund Managers December 2023 The 'low emissions' megatrend is decarbonising business models, driving long term value for investors and helping corporates and countries attain climate related goals. Insync Funds Management CIO, Monik Kotecha said, 'The main levers of the low emissions megatrend are cost competitive renewables that have experienced massive drops in their establishment, then production costs, compared to their fossil fuel and nuclear peers.' This, he said, is what is driving the 'electrification of everything' including transportation, heating, industrial operations, etc. 'More than just clean energy generation, it also encompasses digitally optimised energy efficiency systems, decentralised energy generation and overhauling entire electricity grids.' Half of the world's demand for energy is projected to be served by 'clean molecule' sources by 2050 and hydrogen, the first, lightest and most abundant element in the universe, is set to play a vital role. 'Electrification alone won't get us to net zero,' Mr Kotecha said. 'Hydrogen as part of an energy mix could supply sectors not suited to electricity, such as heavy machinery and heavy industries, in lieu of fossil fuels.' Seen as a potentially environment-friendly transformative force Mr Kotecha said hydrogen is an enticing prospect for investors, green hydrogen in particular. 'However, it is vital to temper enthusiasm with a dose of realism, given the hurdles on the path to profitability.' At the heart of the challenge, he said, lies competition with fossil fuels. 'Currently, they are more cost-effective and often heavily subsidised by governments, which means green hydrogen is dependent on external private financial support. Subsidised carbon economics continues to dominate over environmental concerns, and this will remain a challenge until subsidies, scale, infrastructure, and technology advances for green hydrogen level up the current 'unlevel' playing field.' Most hydrogen today is produced by extracting it from oil, coal or natural gas. In order to justify substantial capital investment for an environment-friendly production source, high-capacity utilisation is essential. 'Green hydrogen is made by splitting the water molecule via electrolysis to create hydrogen. This demands a stable green power source, which is no small feat - although this complex issue is rapidly being overcome.' A variation to green hydrogen is pink hydrogen (electrolysis powered from nuclear energy). New salt based nuclear reactors already under construction could proffer a cost effective and far safer and environmentally friendly power source than today's typical fission reactors, thus meeting the need for stability of supply. However, it is likely that the green hydrogen sector will require a more extended investment horizon to realise its full potential or until new technology breakthroughs like those encountered in solar impact the economics. 'In other words, unfortunately, we don't think green hydrogen has yet reached an essential economic tipping point to be a profitable component of the low emissions megatrend, nor produce companies that meet our high profitability criteria, but we will continue to watch and see.' Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

18 Dec 2023 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||

| Firetrail S3 Global Opportunities Fund (Hedged) | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| Firetrail Australian Small Companies Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| Firetrail S3 Global Opportunities Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

|

||||||||||||||||||||

| India 2030 Fund | ||||||||||||||||||||

|

||||||||||||||||||||

|

||||||||||||||||||||

| UBS Emerging Markets Equity Fund | ||||||||||||||||||||

|

||||||||||||||||||||

|

||||||||||||||||||||

| OAM Select Income Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||

|

Subscribe for full access to these funds and over 750 others |

18 Dec 2023 - Glenmore Asset Management - Market Commentary

|

Market Commentary - November Glenmore Asset Management December 2023 Globally equity markets recovered strongly in November. In the US, the S&P 500 rose +8.9%, the Nasdaq increased 10.7%, whilst in the UK, the FTSE 100 was more muted, rising +1.8%. The key driver of the rally was data points showing cooling inflation, which in turn saw bond yields fall materially. The US 10-year bond rate declined -58 basis points to close at 4.26%. Its Australian counterpart fell +52bp to close at 4.41%. The weaker inflation data provided hope that the restrictive interest rate hikes of the last 18 months may be nearing an end. In Australia, the All-Ordinaries Accumulation Index rose +5.2% in November. Top performing sectors were healthcare and real estate (a clear beneficiary of lower bond rates), whilst energy was the worst performing sector, driven by a fall in oil and gas prices. Positively for the fund, small cap stocks outperformed large caps as investor risk appetite improved with falling bond rates. Given the material underperformance of small cap stocks vs large caps in the last 18 months, we believe the next few years should be positive for the fund given its skew to small caps, where we are seeing quality companies across numerous sectors priced very attractively. Funds operated by this manager: |

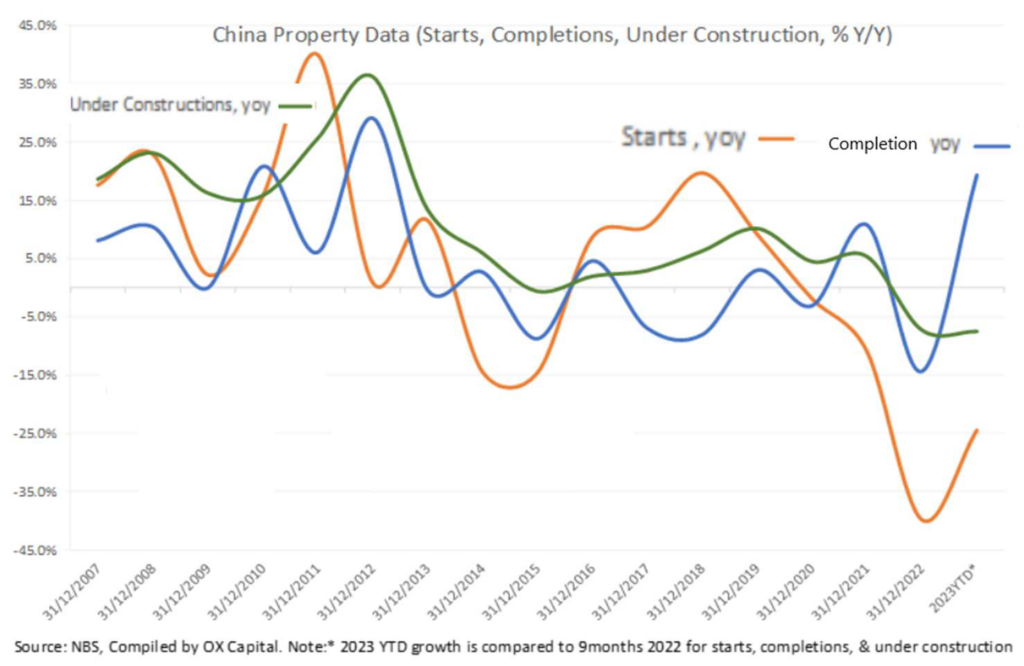

15 Dec 2023 - China Property: Has the "Grey Rhino" been tamed?

|

China Property: Has the "Grey Rhino" been tamed? Ox Capital (Fidante Partners) December 2022 Stabilization of property market in sight = Time to buy quality growth stocks in China. Relative to most governments in the world, the Chinese authorities proactively controlled and deflated the property 2) Housing starts have declined over 60% from peaks to 2023 YTD. Urbanization rate in China is only ~60%,

3. Stimulating growth: The Chinese authorities have started to stimulate the economy, showing an intention to boost growth, increase consumer sentiment and investor confidence. We believe further reforms are likely to mitigate risks to the broader economic recovery. Notably, our base case for China is that of continual policy easing and continued government stimulus, an environment ripe for improving economic activity. Funds operated by this manager: |

14 Dec 2023 - Why government bonds remain a natural choice

|

Why government bonds remain a natural choice JCB Jamieson Coote Bonds November 2023 As we approach the eagerly anticipated end of the rate hiking cycle, investors are considering how to position portfolios for what comes next, while trying to navigate the current higher rate, higher inflation environment. Perhaps now, more than in any other cycle, the role of bonds in portfolios is being questioned after negative annual returns were experienced in 2022. In this article, we discuss why 2022 was such a difficult year for investors across the board, why higher rates aren't necessarily a bad thing for active bond investors and why the valuable role bonds play in a diversified investment portfolio hasn't changed. 2022 - AN EXCEPTION RATHER THAN THE RULEWhen it comes to making the case for bonds, perhaps the biggest objection comes from those who saw 2022 as a serious flaw in the argument. Bonds traditionally play the role of what many refer to as 'portfolio insurance' - offsetting equities' losses during market upheaval - but in 2022 they failed to perform this function. SO, WHAT HAPPENED?Bond returns have two main enemies, inflation, which erodes their value, and rising interest rates, which reduces the value of existing bonds because higher rates of income are available elsewhere. In 2022, we had both inflation and higher rates in tandem, as central banks aggressively hiked rates in a bid to bring inflation back to tolerable levels. As active bond investors, we've managed portfolios through a number of crises, and to put 2022 in context, this was one of the biggest bond market sell-off events since the great depression. We see this as an exception to the rule, rather than a 'new normal'. While financial market downturns typically see equity markets sell off and bond markets surge, rapid rate rises and inflation result in both asset classes suffering. The history books are punctuated by market crises, and while history doesn't repeat, looking to a previous episode of severe negative returns in 1994, interestingly this was followed by a period of outperformance in 1995. 2023 hasn't been a turnaround year like 1995 was, but we remain of the view that 'boring bonds' can quickly turn around in a correction event and that timing the market is impossible. The old adage of 'time in the market, not timing the market' holds true in bonds also. Chart 1: Australian Government Bond Market and Equity Market Annual Returns since 1993

Source: Bloomberg AusBond Treasury 0+ Yr Index vs S&P ASX 200 Accumulation Index. As at 27 November 2023. HIGHER RATES AREN'T ALL BADIncreasing interest rates in the context of an actively managed bond portfolio invested over the medium to long term is not necessarily bad. Higher rates restore their value and defensive properties relative to equities and active management enables bonds to be traded on the secondary market, before they mature, meaning that the negative effects of rising rates can be managed. In the post GFC period of ultra-low interest rates and bond yields, the ability of bonds to deliver meaningful returns and their defensive characteristics were much more limited than they are today in a higher interest rate regime. In essence, the cushions have now been re-inflated and bonds are now in better shape than they have been for years. If anything, the case for holding bonds has strengthened, particularly if rates have risen too high, too quickly and an economic downturn looks imminent. A TRIED AND TRUSTED DIVERSIFIER

Regardless of the path ahead for cash rates, bonds remain a vital diversifier. Whichever way an investor constructs a portfolio, a diversified range of return sources across asset classes can help mitigate risk. The top left quadrant of the chart above illustrates events where bonds have provided positive returns, during crises where equity markets were strongly negative. This shows the value of diversification and the traditional portfolio defence role of government bonds in action. CONCLUSIONLooking ahead, we believe the delayed impact of the rapid rise in interest rates on the economy could result in an economic downturn, with central banks cutting interest rates well into 2024 to stimulate economies. In that scenario, allocations to government bonds are typically sort after, driving bond prices and returns higher. About once every decade bond investors are rewarded for their patience and time in the market and we believe that the cyclical nature of the economy, and our analysis suggests that this time is coming.

Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) |

13 Dec 2023 - Investing Essentials: Diversification - The shield against investment volatility

|

Investing Essentials: Diversification - The shield against investment volatility Bennelong Funds Management November 2023 |

|

As any investor will tell you, investing can be a rollercoaster. Not all investments behave in the same way - different types of investments behave differently under certain economic and market conditions. Some may go up while others go down. Some may be entirely negatively correlated. This is where diversification comes in. Essentially, diversification means investing across a range of different investment types that behave differently across a full investment market cycle. While nothing will give you an absolute guarantee against loss, spreading your investments across different investment categories and types of assets limits your exposure to individual related risks. Risks can be in the form of market risks, where the market may become less valuable for assets within a particular class due to external factors, like interest rate changes, war, or weather events. Or, they can be asset-specific risks, which come from the performance of investments or companies themselves, often dependent on management's performance, operational activities or competitor actions, for example. There are all sorts of ways to diversify your portfolio to mitigate these risks. Diversification can occur across asset classes (e.g. equities, property, cash), industries (e.g. telecommunications, agriculture, financial services), or regions (e.g. countries, markets, economies). Diversifying by asset class For example, commodities like gold may not have a correlation to real estate. Diversifying by industry For example, if you decide to invest all your money into one type of agricultural crop such as wheat, then adverse weather conditions could wipe out the crop rendering your entire investment worthless. But if you had invested across other industries that aren't impacted by weather, such as healthcare or financial services, only a portion of your savings would be impacted by this weather event. Diversifying by region For example, one region may be in economic expansion while another is in contraction. Exposure to different currencies, and to different political and regulatory environments can have an impact on an investment. Having your investment diversified across asset classes, industries and regions is important for investment success, and helps to ensure that your range of investments don't all perform in the same way at the same time. Therefore, overall investment returns may be achieved in a less volatile way, relative to holding only one or two different assets. In determining the right asset allocation for your portfolio, you'll need to consider the overall risk and return of each asset, and how different assets correlate with each other. It's also important to determine your own risk and return level that you are comfortable with and able to tolerate. Diversification serves as somewhat of a safety net, capturing the potential benefits of various investments while mitigating the risks associated with market fluctuations. It's always important to remember that any decisions you make should be in line with your own financial objectives, as each person's investment needs will be different. |

|

For more insights visit www.bennelongfunds.com Disclaimer The content contained in this article represents the opinions of the author/s. The author/s may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the author/s to express their personal views on investing and for the entertainment of the reader. |

12 Dec 2023 - The real risk of wildfires to US infrastructure investors

|

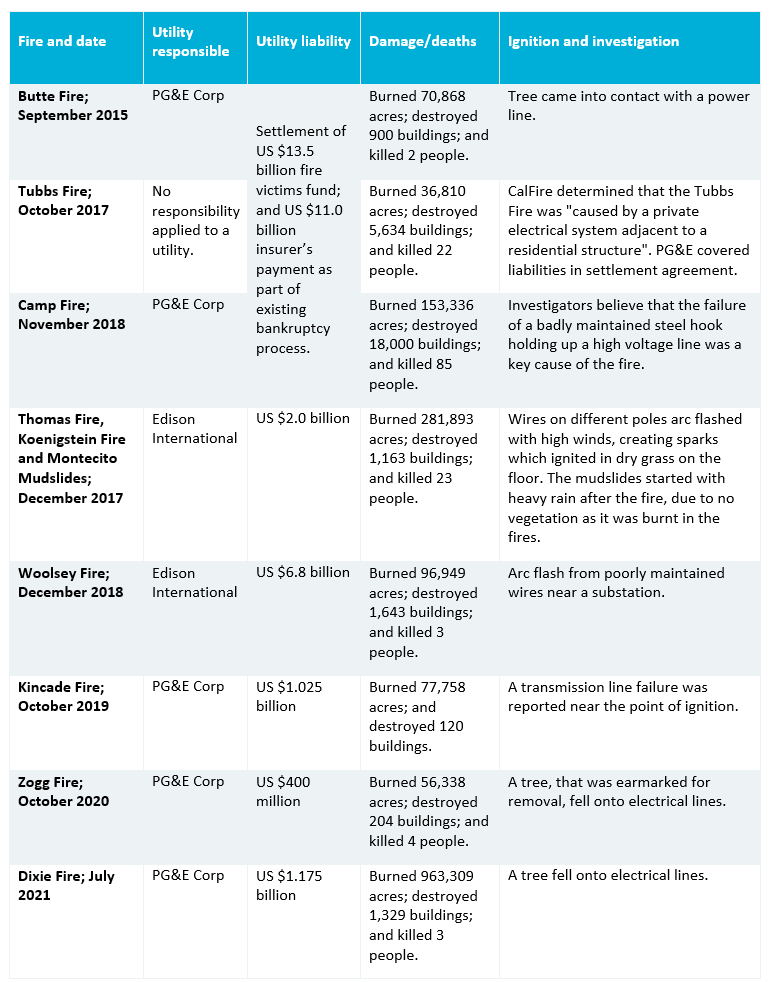

The real risk of wildfires to US infrastructure investors 4D Infrastructure November 2023 This article focuses on wildfires in the US, and their impact on utility companies in our universe. Five of the ten most destructive US wildfires since records began in the mid-to-late 1800s have occurred since 2013[1]. Climate change driven by human intervention has, through attribution analysis, been proven to be a key contributor to the increased frequency and ferocity of fires in the US. These fires are a real risk for utility companies and their investors, and with global temperatures continuing to rise, it seems the issue could intensify going forward. In our recent Global Matters article, Extreme weather risks and their impact on investors, we outlined the observed link between extreme weather events and climate change globally. Here, we'll focus specifically on wildfires and their impact on US utilities. Wildfire ignitionsWildfires are somewhat unique compared to extreme weather events - even though conditions are exacerbated by global warming, wildfire ignition is usually started by lightning strikes, human intervention (accident, negligence or intent), or electric utility equipment. There have been numerous examples in the US where electric utility company assets have ignited wildfires, which have gone on to cause significant third-party damage. The utility therefore faced billions of dollars in litigation liabilities, well in excess of their insurance protection. This has resulted in significant financial losses, cash liability payments, and increased probability of corporate financial distress, which itself has social ramifications. It started in CaliforniaThe detrimental shareholder impact of wildfire liabilities experienced by Californian utilities is well known. PG&E Corp (PCG-US) and Edison International (EIX-US) were most negatively affected by wildfires ignited by company assets over the period 2017-2021. Courts in California have adopted a unique application of the legal concept, inverse condemnation. It applies legal liability on electric utilities for all third-party damages caused by a fire which the utility's assets are found to have ignited. The courts' application of inverse condemnation removes the legal requirement to prove negligence on behalf of the utility in order to enforce third-party liabilities, which is required in other states. The courts have assumed the utility will recover these third-party property damages from customer bills, but the Californian utility regulator has been reticent to allow this. A number of fires were found to be ignited by utility assets in the state, incurring significant third-party property damages, as well as civil, regulatory and criminal penalties.

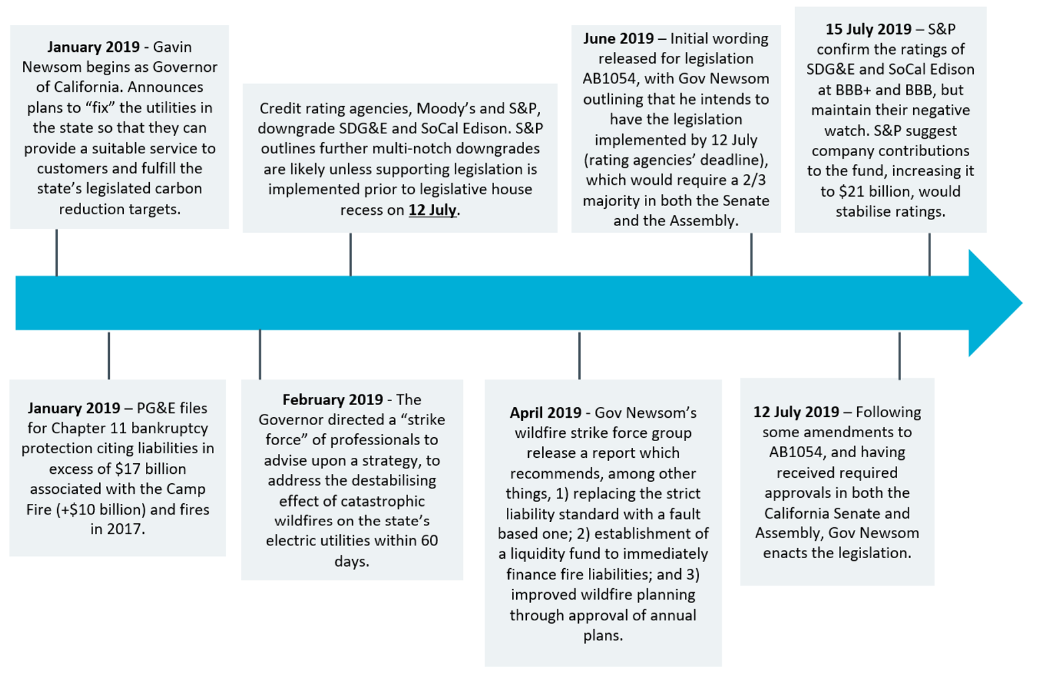

Source: California Board of Forestry and Fire Protection (CAL Fire) PG&E filed for bankruptcy protection in January 2019, due to the quantum of liabilities facing the company at the time. This process rendered the remaining equity value in the company zero. As part of PG&E coming out of bankruptcy, the company negotiated with legal representatives of uninsured wildfire victims and insurance companies of the Butte, Tubbs and Camp Fires to make payment of $24.5 billion (partially through an established fund) for property damages. However, it became clear that the situation for the utilities in the state was untenable. In 2019, Governor Newsom began his gubernatorial tenor in California. He identified wildfire risk as a key risk to the state, and understood that properly functioning and sustainably financed utilities were needed to deliver the energy prerogatives of California. He went about establishing a framework to mitigate wildfire liabilities for utilities which are prudently operated, in order to improve their credit assessment and ability to finance themselves. The below timetable summarises legislative steps taken, and the corresponding credit rating agency response.

Legislation SB 1054 not only established a wildfire liquidity fund which would finance wildfire legal liabilities sustained by the utilities, but it also established a process of ensuring that the utilities were prudently operating their electricity assets and were taking reasonable steps to mitigate the ignition of wildfires. If classified as a prudent operator under an annual certification, the utility can recover any fire liabilities in customer bills or from the established liquidity fund. Since 2018/19, companies have significantly reviewed their operational management of fires, and invested billions of dollars in 'hardening' their networks to avoid future fires. Key initiatives include:

The major electric utilities in California experienced significant share price corrections associated with the wildfires, and only recently have started to recover. The market seems to appreciate steps taken by the companies and state legislators in mitigating future fires, combined with the liquidity fund and pre-prudency test in avoiding future legal liabilities when fires do occur. But recent developments suggest wildfire risk is not specific to California... More recent experiences of wildfire riskInvestors thought that debilitating financial damages from wildfire risk was limited to Californian utilities because of the state's unique application of inverse condemnation. The requirement in other states, to prove utilities have acted negligently, was perceived as a mitigant against them incurring similar legal liabilities, unless negligent. That view may be changing. PacifiCorp litigationIn June 2023, unlisted electric utility, PacifiCorp, received an Oregon court decision relating to its alleged involvement in five major fires which burned across the state in October 2020. The fires burnt 850,000 acres of land, causing damage to around 4,000 homes, and killing at least 11 people[2]. Despite PacifiCorp not having been found responsible for ignition of the fires by any formal body at the time of writing, a jury court made a number of decisions including:

The jury found PacifiCorp negligent in failing to shut-off power to its 600,000 customers during a windstorm, despite warnings from officials. The company did not have any established power shut-off process, and argued the ramifications of cutting power would have broader and serious ramifications. The decision that PacifiCorp was liable for the fires also means that the company is likely to incur further actual and punitive damages associated with approximately 2,500 householders under a separate class action lawsuit. A very basic assessment suggests PacifiCorp could be liable for billions of dollars associated with this class action lawsuit. There is a clear risk of financial distress for the company. Maui fires of 2023The Maui fires that started on 8 August 2023 destroyed more than 2,700 structures, and killed 97 people, with 31 unaccounted for as of 18 September 2023. An investigation is ongoing into the cause of the fire, but Maui County has already filed a lawsuit against a subsidiary of the utility company, Hawaiian Electric Industries (HE-US), based on suspicions that the fire was ignited by the utility equipment (uninsulated wire contacted dry grassland when strong winds downed a wooden power pole). Hawaiian Electric has suggested that the lawsuit is imprudent in pre-empting the outcome of the formal investigation into causation. The share price of HEI fell from the closing price of $37.36 on 7 August, to $12.85 as at 17 October 2023 (a 65% decrease) based on legal risk associated with the fire. There is conjecture as to the prudent operation of the network on behalf of Hawaiian Electric, but the findings in the PacifiCorp case clearly show a high legal risk being faced by the company. Other exposed companiesA number of other companies are also exposed to wildfire risk in the US including:

4D's approach to mitigating the riskThere is no doubt that the environmental conditions for wildfires are being exacerbated by climate change. In doing nothing, utilities will be at greater risk of wildfire liabilities (physical and legal) as global temperatures increase. Many utilities are enhancing their operational preparedness and investing in 'hardening' the network to mitigate the risk of fire ignition. Governments and fire authorities are also focused on reducing the fuel for fires, being able to respond effectively to fires after ignition, and protecting prudently operated utilities from legal liabilities. At 4D, we undertake significant due diligence to understand utilities' operational preparedness and investment plans in hardening their networks against wildfires. We also keep abreast of legal and regulatory developments in utility operating jurisdictions to ensure the companies aren't exposed to risks that they cannot mitigate through prudent operation of their networks. This due diligence flows through our capex modelling and values, as well as our quality assessment of the utilities' jurisdiction, asset quality and management. We will exit a position, or rule a stock uninvestable, if there is a real risk of unquantifiable liability. |

|

Funds operated by this manager: 4D Global Infrastructure Fund (Unhedged), 4D Global Infrastructure Fund (AUD Hedged), 4D Emerging Markets Infrastructure Fund For more information about 4D Infrastructure, visit https://www.4dinfra.com/ The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. [1] https://earth.org/worst-wildfires-in-us-history/ |