NEWS

US, the S&P 500 increased +1.6%, the Nasdaq rose +1.0%,

whilst in the UK, the FTSE100 declined -1.3%.

20 Feb 2024 - Glenmore Asset Management - Market Commentary

|

Market Commentary - January Glenmore Asset Management February 2024 Globally equity markets performed strongly in January. In the US, the S&P 500 increased +1.6%, the Nasdaq rose +1.0%, whilst in the UK, the FTSE100 declined -1.3%. In Australia, the ASX All Ordinaries Accumulation Index rose +1.1%. Energy and Financials were the best performing sectors, whilst resources was the weakest performer, as sentiment towards the Chinese economy weakened. Inflation data both domestically and offshore continues to moderate, which in our view indicates the bulk of the heavy lifting by central banks in terms of interest rate hikes has now been done. The US economy appears to be ahead of Australia in terms of getting on top of inflation, hence we expect the US will see interest rate cuts before Australia over the next 12-18 months. In bond markets, following two months of very material declines in bond yields, January saw a slight increase as economic data pointed to a still strong global economy (despite the aggressive tightening by central banks). In the US, the 10-year bond rate climbed +17 basis points (bp) to close at 4.01%, whilst in Australia the 10-year bond rate rose +6 bp to also finish at 4.01%. As always, February is a very busy month with the vast majority of the fund's holdings reporting results for the six months to 31 December 2023. The upcoming reporting season will provide visibility into how the companies are performing operationally. Whilst we have seen a recovery in equity markets in recent months, we continue to be very optimistic about the outlook for small/mid cap stocks on the ASX given their cheap valuations and material underperformance over the last two years. To reiterate, our focus in 2024 will be identifying quality businesses trading on attractive valuations, where we believe material earnings upside exists. Funds operated by this manager: |

19 Feb 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Aura Core Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| MA Sustainable Future Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Aquasia Short Term Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| Eley Griffiths Group Mid Cap Fund - Class A | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| EAM Global Small Companies Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Auscap Ex-20 Australian Equities Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 800 others |

16 Feb 2024 - Murray Ackman: Ignore the billionaires - diversity, equity and inclusion are good for investors

|

Murray Ackman: Ignore the billionaires - diversity, equity and inclusion are good for investors Pendal February 2024 |

|

AMERICAN billionaires seem to be picking fights with big brands and civil rights groups over whether corporate diversity, equity and inclusion (DEI) policies are discriminatory. Or even whether they cause aircraft malfunctions. If you've been following the "woke backlash", you'd be familiar with recent flash points such as the campaign against Harvard's first Black female president Claudine Gay. Tesla's Elon Musk, hedge fund manager Bill Ackman and Lululemon founder Chip Wilson have all been engaging in civil discourse on social media recently, expressing anti-DEI views. Musk went as far as suggesting that Boeing, fresh from having a fuselage panel fall off mid-flight last month, was prioritising diversity over safety. That drew a swift rebuke from civil rights groups. "DEI must DIE," Musk said recently on his X social network. "The point was to end discrimination, not replace it with different discrimination." This week the Tesla CEO erased mention of DEI in the electric vehicle maker's corporate filings. Do DEI critics have a point? And what does that mean for investors and companies? What are the concerns about DEI?Musk's criticism of Boeing centred around the impact and unintended consequences of connecting executive pay to diversity targets and ESG metrics. At the start of 2022 Boeing altered its bonus scheme, rewarding executives who hit certain climate and DEI targets. Boeing is certainly not alone here. In 2011, just 1 per cent of listed companies had such a policy. By 2021 it was 38 per cent, and the trend continues. Supporters argue this is positive for companies and shareholders. The idea is that such policies safeguard future economic results from risks while aligning the managerial objectives with shareholder interests. Sharemarket analysts look for such policies as a sign that a business cares about a particular issue. Who's right?Does linking executive pay to diversity improve a business? Or are such corporate DEI policies a sign of excess? There are plenty of studies - including from Pereptual's Regnan sustainable investing business - suggesting DEI can drive business outperformance. A 2021 study from sustainable investing leader Regnan found that DEI - and especially equity and inclusion - can drive business outperformance. Yet Regnan also found many businesses think about diversity and inclusion in a flawed way. For example, DEI policies often focus on the needs of minority groups, while majorities are not always adequately considered. For investors and companies alike, we believe organisational settings should allow all talent to flourish - including 'majority talent' as well as talent that is traditionally under-represented. These are essential pre-requisites for an equitable and inclusive workplace. Businesses benefit from fair employment practices, supportive cultures and open decision-making. What it means for investorsWhile there is now a lot of ESG measurement going on inside companies, it's fair to say there could be a deeper discussion about how inclusive culture can be good for a business. But is Elon Musk right to say there is undue focus placed on DEI? The billionaire's complaints could make sense in the context of a boot-strapped start-up operating from the proverbial garage. But it feels provocative coming from the CEO of a business with one of the highest market caps in history. Based on our experience at Pendal, businesses clearly demonstrate what they care about by what they report. And that is useful for investors. Investors should expect to see comprehensive DE&I plans from companies. And take caution with companies that ignore these responsibilities. And they should look beyond the reported diversity numbers to understand if a business has the right structure to allow for diversity and growth. While it's entertaining to see billionaires argue among themselves, investors must understand how a company thinks about diversity and inclusion if they want to understand whether it is managing risks. Author: Murray Ackman |

|

Funds operated by this manager: Pendal Focus Australian Share Fund, Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Regnan Global Equity Impact Solutions Fund - Class R, Regnan Credit Impact Trust Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

15 Feb 2024 - A few charts from our Micro Caps CY2024 Overview

|

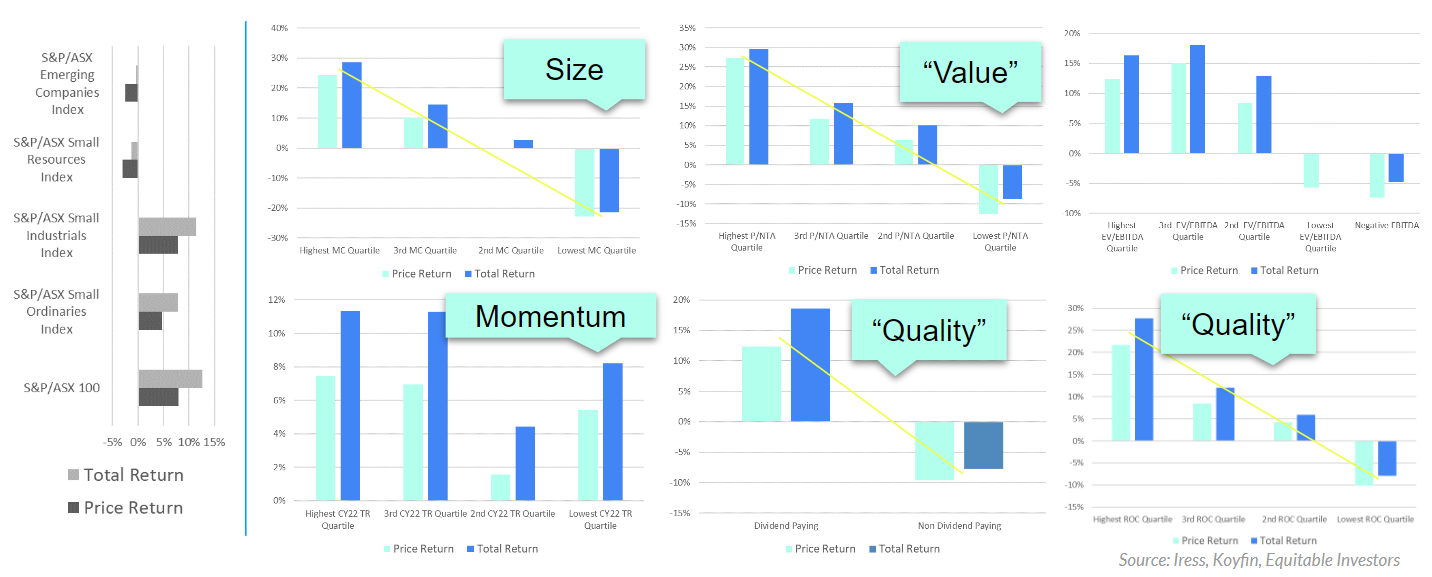

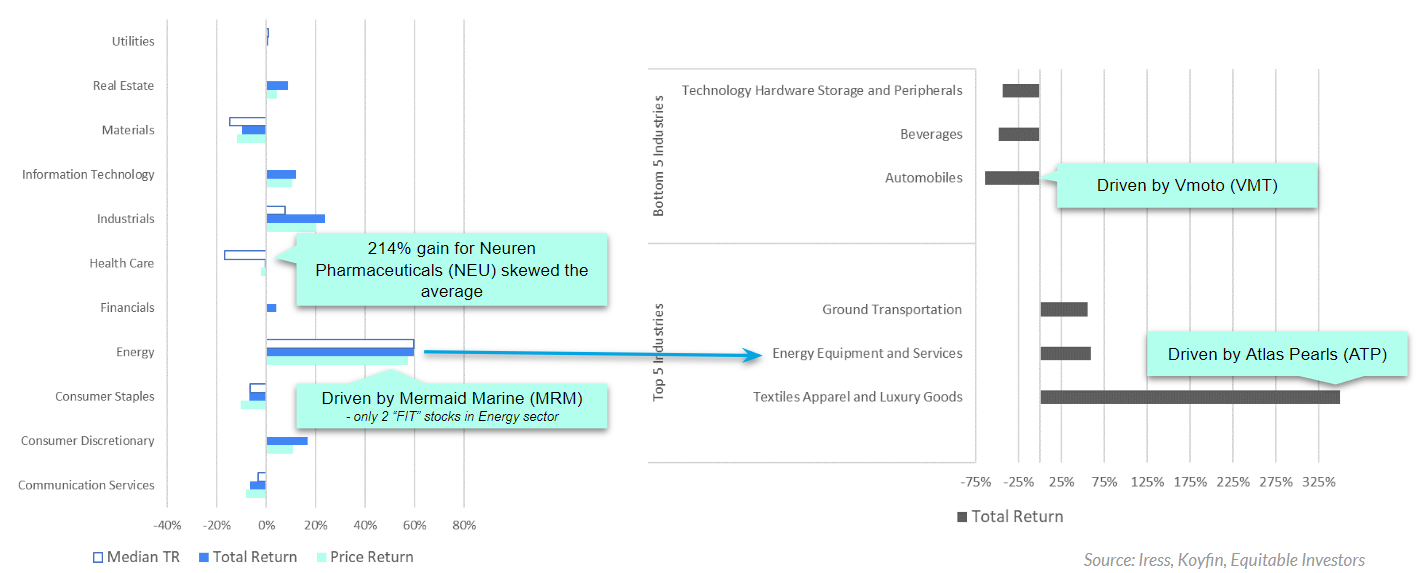

A few charts from our Micro Caps CY2024 Overview Equitable Investors February 2024 CY2023 Review

Stocks on higher multiples did better than those in "value" territory as investors chased "quality" (if you define that as top quartile return on capital or companies paying dividends) but the most clear cut divide in ASX listings in CY2023 was simply size as investors shunned the perceived heightened risk of micro caps. Below we analyse CY2023 performance of our ASX "FIT" (Financials, Industrials & Technology) micro-to-mid cap universe, alongside the S&P/ASX benchmarks. All FIT returns presented are averages of the stocks that meet the relevant criteria. CY2023 Sector & Industry Review

The Materials sector, covering chemicals, packaging and paper, was the most beaten-down in CY2023 with an average decline of 10% and a median decline of 15%. Health was an interesting space, where the average return was -1% but the median was -17% as the median biotech, pharmaceutical and health care stock fell by more than 20% BUT one stock surged 214%. Interesting to note that Consumer Discretionary stocks strongly outperformed Consumer Staples.

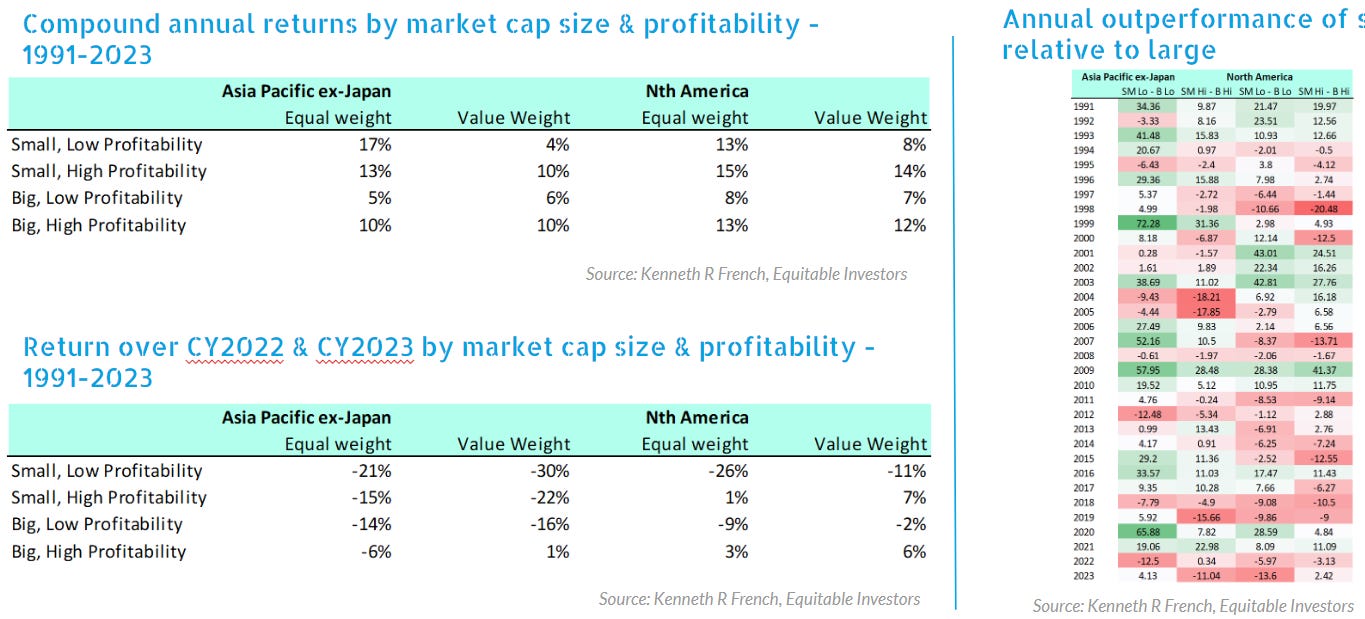

Returns by Size - Broader International Perspective

On an equal-weighted basis, the smallest 10% of stocks by market cap have outperformed the larger 90% in North America and in Asia Pacific ex-Japan (Australia, Hong Kong, NZ & Singapore) over the past 30+ years. But returns over CY2022 and 2023 have favoured the largest and most profitable businesses.

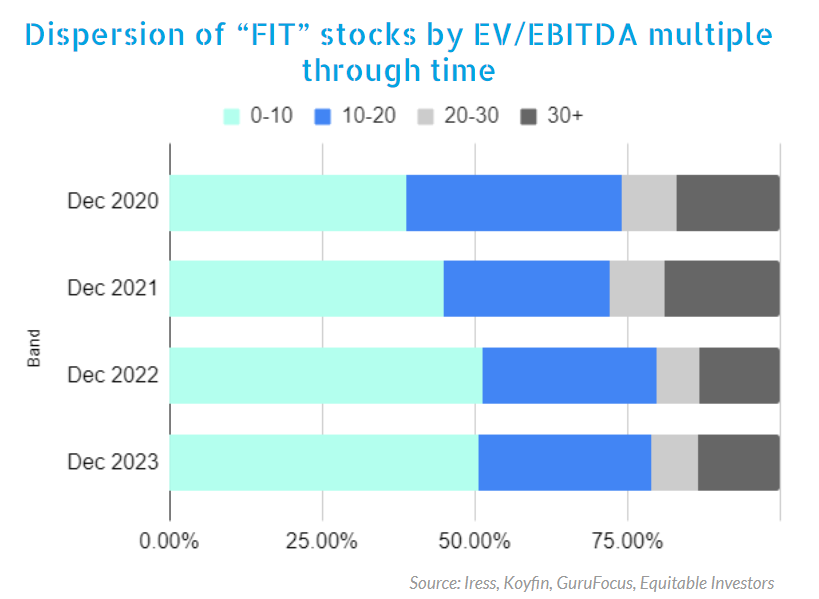

We began tracking the dispersion of trailing (historical) EV/EBITDA multiples when we launched the weekly "Small Talk" publication in 2020. There has been a tangible shift downwards in multiples, with 51% of companies on 10x or less in 2022 and 2023, compared to just 39% at the end of 2020. Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

13 Feb 2024 - Investment Perspectives: Global real estate - the outlook and themes for 2024

12 Feb 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Contrarius Global Equity Fund (Australia Registered) - Retail Class | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Contrarius Global Balanced Fund (Australia Registered) - Retail Class | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Lazard Australian Equity Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Lazard Global Equity Franchise Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Lazard Global Small Cap Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Lazard Global Digital Health Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 800 others |

Resilient growth and moderating inflation in the US reflect positive supply shocks that are almost exhausted. A slowdown followed by a mild recession in 2024 is the most likely scenario.

9 Feb 2024 - Private markets house view for 2024

|

Private markets house view for 2024 abrdn January 2024 What's in store for private assets?Resilient growth and moderating inflation in the US reflect positive supply shocks that are almost exhausted. A slowdown followed by a mild recession in 2024 is the most likely scenario. European economies are already weak and we expect them to remain so until the middle of next year - although positive real income growth should limit the size of the downturn. Most central banks have finished hiking rates and should begin cutting in 2024, as inflation fades further. Chinese policy easing is now stabilising activity, but there are long-term headwinds. Emerging markets are benefiting from moderating inflation and they are entering a policy-easing cycle. As we analyse the private markets landscape, it is important to consider the latest trends in key sectors and to address the evolving macro backdrop. Private equityIn a high-interest-rate environment, persistent inflation continues to draw down deal appetite in both Europe and the Americas, particularly regarding exit strategies. Many General Partners continue to extend out their exit horizons, avoiding lower valuations in anticipation of better market conditions in the future. The latest third-quarter valuation multiples suggested that valuations are correcting at a modest pace across North America and Europe. In terms of sectors, financials and consumers have suffered the worst peak-to-trough declines while energy valuations are still rising. Technology multiples held up well heading into 2023 but have been hit since. However, they are still at a premium relative to other sectors. We continue to see mid-market companies in Europe and the Americas contributing to consumption growth in urban centres. Therefore, we will focus on opportunities to invest in recession-proof industries like healthcare and information technology that capture global long-term trends. It is crucial to focus on upper-quartile managers who have a proven track record of unlocking value in portfolio companies' balance sheets. Private creditDemand for private credit continues to remain robust as traditional lenders pull back. Given the elevated returns, expanded spreads, and protection from a low correlation to gross domestic product, the risk-return dynamics of private credit have become extremely appealing. Careful deal selection for assets with downside risk remains crucial. Default rates remain low by historical standards, but they are anticipated to rise in private credit as many private credit managers have not been fully tested since the Global Financial Crisis (GFC). In addition, the market dynamics are fundamentally different from the previous cycle. Dislocation in the market is creating good opportunities, and lenders are in a position to demand stronger covenants and to execute deals at attractive risk-adjusted returns. Selectivity remains key. And with signs of distress and increasing default rates, high-quality deals are vital. InfrastructureGlobal infrastructure markets grappled with several shock factors over the year. These stemmed from macro and micro drivers, with a slower fundraising environment, increased financing costs, geopolitical risks, and valuation pressures (to name a few). Despite facing volatility, core private infrastructure assets showed resilience. They provided inflation protection, cost pass-through mechanisms, and robust cashflow generation. The energy transition sectors, for example, continued to grow and large deals still closed. The US Inflation Reduction Act (IRA) provides a strong tailwind for investing in infrastructure spending. For example, technologies such as hydrogen, carbon capture and transport are attractive structural opportunities. Europe is positioning itself to increase domestic commodity supply and energy autonomy by expanding investments in renewable energy. Globally, digital and telecom infrastructure continues to ride a long boom, bolstered by macro headwinds and rising opportunities in digitisation. Real estateThe global real estate market is progressing steadily through this current downturn. Capital markets (yields) have been recalibrating in response to higher interest rates and higher debt costs, which have been much faster than the correction following the GFC. In most regions, values have fallen between 15% and 30% in just two-to-three quarters, but we believe this revaluation phase is close to the end. Real estate yield spreads remain tight versus the risk-free benchmark, but spreads are improving slowly - although they have yet to offer enough illiquidity premia. In Europe, logistics have repriced most aggressively but with more to go for secondary offices. In North America, we are observing cap-rate expansion starting to slow down across sectors. Office defaults are becoming more visible in the US and several high-profile valuations are bringing expectations down to more realistic levels. Meanwhile, across industrials and logistics, renewal activity has remained robust, hence values have held up with a strong macro backdrop. In Asia-Pacific, yields in most markets have barely moved since end-2021. As such, we think there are likely more outward yield shifts that need to take place in the next year. While logistics properties in many markets will likely see higher yields, the negative impact on capital values is expected to be mitigated by further rental upside. Natural resourcesActivity across natural resources is heavily driven by the global energy market. Energy prices continue to be the driving force of investment across the asset class, which is set to continue. The recent conflict in the Middle East has caused further uncertainties, which had started to fall in June. As the renewable energy transition continues to play out, metal and mining strategies have also seen increasing demand, given some metals are also essential in generating renewable energy. While growth in renewables fundraising continued, it is a multi-year push toward decarbonisation. Interestingly, investment flows in North America renewables seem to be catching up with Europe. This can be largely explained by the IRA. In Europe, government infrastructure spending is expected to increase to reflect its transition to a low-carbon economy. Going into 2024, it's likely that the demand for energy will be sustained, but there is uncertainty about how long this could last. However, investment opportunities across natural resources will continue, with the emergence of low-cost renewable power and the growth of carbon markets. This includes the role of timber in the global transition to net zero and lower emissions. Author: Lulu Wang, Portfolio Strategist, Private Markets |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund Source: |

8 Feb 2024 - Bond Market Insights and Outlook for 2024

|

Bond Market Insights and Outlook for 2024 JCB Jamieson Coote Bonds January 2024 Bonds finished 2023 strongly following the market categorically rejecting the 5.00% level in US and Australian 10-year bonds in October. This has provided a solid base for bonds in 2024 following the global peak in yields and the end to the global central bank hiking cycle. The market was comforted with the lower inflation readings and the weaker set of economic data. Bond supply dynamics also played a part when the narrative of increasing government deficits was alleviated with US Treasury projections in the order of 100 billion less than the market was expecting. Markets have moved to more aggressively price in easing from the US Federal Reserve (US Fed), Bank of England and European Central Bank given declining inflation with goods inflation the driver. While time will tell whether November's cash rate hike from the Reserve Bank of Australia (RBA) was the last in the cycle, our view is that we are either at, or at least very near, the peak in cash rates. If history is a guide, cash rates tend to remain on hold at the peak for an average of eight months. While this is certainly not an exact science, based on what we currently know about the economic outlook and market pricing, we anticipate that the RBA will start to loosen monetary policy in 2024 following in the slipstream of its global central bank counterparts. Predicated on this view, any back up in yields will provide a decent opportunity to increase duration exposure, particularly in the 3-to-5-year sector where historically the curve steepens as markets approach their first rate cut. The monetary tightening has pushed the global credit impulse to its weakest level since the Global Financial Crisis, which implies weaker demand growth moving forward placing pressure on the jobs market. High delinquency rates and credit card balances currently support anemic consumer confidence and may begin testing both consumer resilience and the ability of employers to maintain employment with margins under pressure. The job market in 2024 will be the main determinant of whether we travel down the path of a 'hard landing' with the commensurate aggressive easing of short-term interest rates and much higher bond prices with the recent rally into year-end just an entrée to what can be served up. MARKET OUTLOOK: ARE RECESSIONARY SIGNAL LIGHTS STILL FLASHING RED?US recessionary indicators are all signaling a code red alert. An inverted yield curve persisting for 18 months, coupled with a 19-month sequential decline in the Leading Indicator Index, has an infallible record in predicting a US recession. In a soft-landing scenario, the US Fed will need to make approximately a 300 basis points cut just to reach a neutral rate setting. However, in the event of a full-blown recession, we are anticipating a need for around 500 basis points of easing. The December US Fed meeting validated the end of the hiking cycle in short term rates with US Fed Chairman, Powell commenting that "you want to cut rates well before inflation is at 2%" otherwise it would be too restrictive. The US Fed also downgraded its inflation forecast and alluded to three cuts in 2024 as Powell showed concern over keeping rates too high for too long. The inflation trajectory continues a downward path and heading into 2024 this is expected to persist - we still have some hefty inflation prints dropping out of the index so we should get inflation falling on a year-on-year basis for the first five months of the year if we continue to print similar numbers that have been recorded lately. Continued weakness in energy prices and lower wage growth through a deteriorating employment market would also be supportive of the slowing inflation period. The picture in Australia is also encouraging with the inflation story lagging the global softening prices thematic. Given the transmission mechanism of Australian interest rates, we would anticipate this to play catch up in the first quarter of next year. As the new year commences, 2024 is ripe for geopolitical developments with 40 national elections on the calendar from Taiwan at the start of the year through to the US presidential election in November. The potential for a changing of the guard in foreign policy heightens the chances of an escalation or aggravation amongst countries and should fly in the face of the complacency that currently prevails in risk markets and encourage a flight-to-quality demand for sovereign bonds. After an extended period of ultra-low bond yields, followed by some painful years of adjustment higher, bonds are arguably in better shape now than they have been in several years, offering a sense of stability and optimism for investors in the current financial landscape. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) |

5 Feb 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

||||||||||||||||||||||

| Clearbridge RARE Infrastructure Value Fund - Hedged | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| ClearBridge RARE Infrastructure Value Fund - Unhedged | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| ClearBridge RARE Emerging Markets Fund - Unhedged | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| ClearBridge RARE Infrastructure Income Fund - Hedged | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| ClearBridge RARE Infrastructure Income Fund - Unhedged | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

|

||||||||||||||||||||||

| Contrarius Australia Balanced Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Contrarius Australia Equity Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 800 others |

Unless that is, you have been invested in the US Magnificent Seven. It has been a year of extraordinary moves in things we never saw coming.

1 Feb 2024 - A Fairytale of New York (NYSE and the Nasdaq)

|

A Fairytale of New York (NYSE and the Nasdaq) Marcus Today December 2023 |

2023 has been a year that most Australian investors would like to forget.

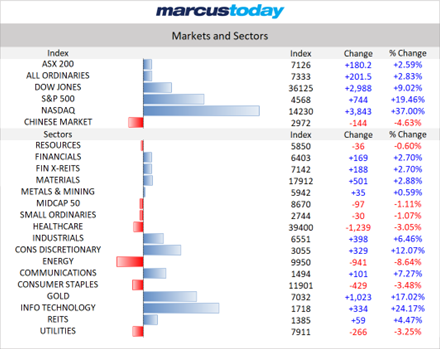

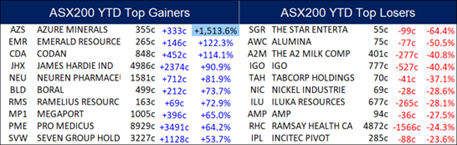

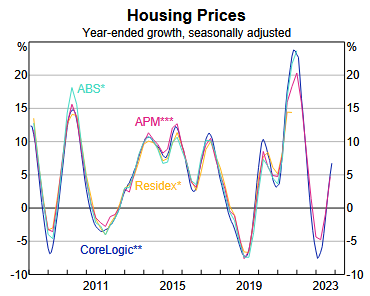

Source: Marcus Today . Source: Marcus Today. Unless that is, you have been invested in the US Magnificent Seven. It has been a year of extraordinary moves in things we never saw coming. Bitcoin is the best performing 'asset' - and I use that term loosely. US Bond markets have staged an extraordinary rally in the last month or so, as yields spiked and then collapsed. Iron ore has defied gravity and hit $200 in AUD terms, almost back to the halcyon days during CV-19, or the big gains we saw before the GFC - and all this without the bazooka stimulus we have come to expect from the Chinese. In fact, Chinese property seems to have gotten worse over the year. Here, the retailers have had a great year despite all the rate rises. Where was that mortgage cliff that traumatised markets? It's coming apparently. Many have suffered, but we now have a pause in the inflation offensive. Rates are normalising. The last decade was abnormal! What happened to house prices? They just kept going higher.

Source: ABS, APM, CoreLogic, Residex. Trophy homes changed hands at record prices. Young people have given up on the Great Australian Dream. The Bank of Mum and Dad took a pounding this year - if you could find them on their holiday in Europe that is. This time last year, lithium was riding high at extraordinary levels, and now we have gone from rooster to feather duster. Much like another white powder craze in milk powder! White line fever. Remember that? A2 Milk (ASX: A2M) hit 20 bucks - madness. Plenty of that around. Gone now though. Some brokers were sounding the warning bell on lithium prices and were 'pooh-poohed' for their view. As General Melchett once said in Blackadder, you should never pooh-pooh a pooh-pooh. Wise words darling, eh? At one stage this year, we had billionaires fighting to keep lithium assets Australian-owned. Hats off to you Gina. You succeeded. Unfortunately, it was at a cost. Quite a big cost. For everyone. In hindsight, it looks like two bald men fighting over a comb. Origin Energy (ASX: ORG) saw off the 'Brookfield Mounties' after a rear-guard defence from Australian Super, though several other icons fell - Newcrest is no longer and OZ Minerals (ASX: OZL) fell to BHP (ASX: BHP). Is the ASX shrinking to greatness? Then there are the gold miners. Who would have 'thunk' that gold would hit an all-time high whilst rates were going higher? Gold pays no dividends and actually costs money to store. It has always puzzled me why we spend so much time and money digging it up, making it into a nice bar shape, and then burying it again in an underground vault. The sector is up 17%. Still, many things in life puzzle me. I struggled with The Book of Mormon! Was that just me? This year we had the rise of AI and the machine. I thought Nvidia was a skin care product until this year! Even AI didn't see that one coming. We also had a year where GLP-1 drugs offered a 'miracle cure' for obesity, and killed CSL (ASX: CSL) and Resmed (ASX: RMD) in the process. More iconic falls. The consensus last year was that the US economy would experience a recession. The question was whether we were going to get a soft landing or a hard landing. Well, no recession. The experts got that wrong too. In fact, there is not much the experts got right. Oil was supposed to hit $100 due to Ukraine, and then Gaza. Nope. Oil is struggling, even if the Saudis are cutting production. What to expect in 2024.Firstly, experts have no monopoly on making daft predictions. Just because they are on TV or interviewed in the media, I think 2023 shows how wrong they can be. There is one certainty in 2024 that even the experts will get right. The US Presidential Election. Everything to play for, and everything to lose. Are we really headed back to the chaos of the Trump era? It seems a distinct possibility. We are not talking about it yet - but we will. The US Election cycle kicks off early in 2024. The experts are still forecasting a recession and a landing of some sorts in 2024. Hard or soft. Similar arguments triggered a war in Lilliput. Which end of the egg to crack? The markets are now pricing in quite savage rate cuts in the US in 2024. The reason is the US economy is crashing. Is it? I am not sure the Fed will be that aggressive. The economy is slowing, but crashing in an election year seems unlikely. Powell will want to keep his job and the Fed independent. Trump is an agent of change. There are two themes that I think will manifest in 2024. Both out of favour. Both troubled, and both seeing serious negativity. The first one is lithium. At some stage, and we are not there yet, the price will have fallen so much that all that supply coming on stream will struggle to get funding. Plenty of it will be uneconomic. All those gold miners who switched to lithium may have to switch back to gold! Remember the dot-com boom? The miners became web-masters and then had to switch back! When was the last time that we saw a high-profile off-take agreement? Yep, I can't remember one. My 'go-to' would be Pilbara Minerals (ASX: PLS). It still has 20% shorted. A market cap of around $10bn with a cash stash and no problems with the US, as far as Chinese ownership is concerned. Remember when Liontown (ASX: LTR) was valued at nearly $7bn for a project still under construction? We are not at peak bearishness in the sector as yet, but at some stage in 2024, there will be a huge bounce. The other one which has been taken out the back is the oil and gas sector. BHP is looking pretty smart with its jettison of the oil and gas assets to Woodside (ASX: WDS). If you had said there would be a war in the Middle East and interest rates would be at 4.35%, there would not be many experts who would have predicted consumer discretionary stocks would be out partying, and oil and gas stocks suffering from a serious hangover. Yet here we are. I think the sell-down in oil has been overdone. WDS is the premier way to go with this, and I still like Karoon (ASX: KAR), which has de-risked from a one-trick pony with the recent Gulf of Mexico acquisition. Both a big and a smaller one are buys for a better 2024. Finally, I was asked to pick a stock for an Advent Calendar segment recently. I had two that I liked: Treasury Wine (ASX: TWE) for a reopening of China year, and Zip (ASX: ZIP). I know. Crazy, but the US consumer is still spending, just finding different ways to pay. I think we are all guilty of that. Regulation is coming here, and that will provide some certainty. The key is the US, the growth of BNPL, and the pesky ZIP balance sheet. Could 2024 be the year we are talking BNPL again? Maybe, but then again, I have been wrong many times before. Why should this year be any different? The good news is that next year, ChatGPT will be writing a similar article, and I will be redundant. You can blame it then. Author: Henry Jennings, Senior Market Analyst, and Media Commentator |

|

Funds operated by this manager: |