NEWS

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund rose by +2.28% in May. Since inception in February 2009, the fund has returned +12.14% per annum, an outperformance of +2.14% relative to the ASX 200 Total Return benchmark which has...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +3.72% in May. Since inception in January 2013, the fund has returned +12.63% per annum, an outperformance of +3.34% relative to the ASX 200 Total Return benchmark which has returned +9.29% on an...

Read more...

Glenmore Asset Management - Market Commentary

Globally equity markets rallied strongly in May. In the US, the

S&P 500 increased +6.2%, the Nasdaq rose +9.6%, whilst in

the UK, the FTSE was up +3.3%.

S&P 500 increased +6.2%, the Nasdaq rose +9.6%, whilst in

the UK, the FTSE was up +3.3%.

Read more...

Hedge Clippings | 13 June 2025

Following the overnight attack on Iran's nuclear facilities by Israel, the world has become a more dangerous place, although there are those who will claim that in the longer run, for Iran not to have a nuclear capacity (energy or arms)...

Read more...

Performance Report: ECCM Systematic Trend Fund

The ECCM Systematic Trend Fund has returned +11.17% per annum, an outperformance of +6.40% relative to the SG Trend benchmark which has returned +4.77% on an annualised basis over the same period.

Read more...

Performance Report: Seed Funds Management Hybrid Income Fund

The Seed Funds Management Hybrid Income Fund rose by +0.90% in May, outperforming the Solactive Australian Hybrid Securities (Net) benchmark by +0.82%. Since inception in October 2015, the fund has returned +6.34% per annum, an...

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +0.77% in May, outperforming the RBA Cash Rate + 5% benchmark +0.06%. Since inception in April 2018, the fund has returned +11.46% per annum, an outperformance of +4.53% relative to the benchmark which...

Read more...

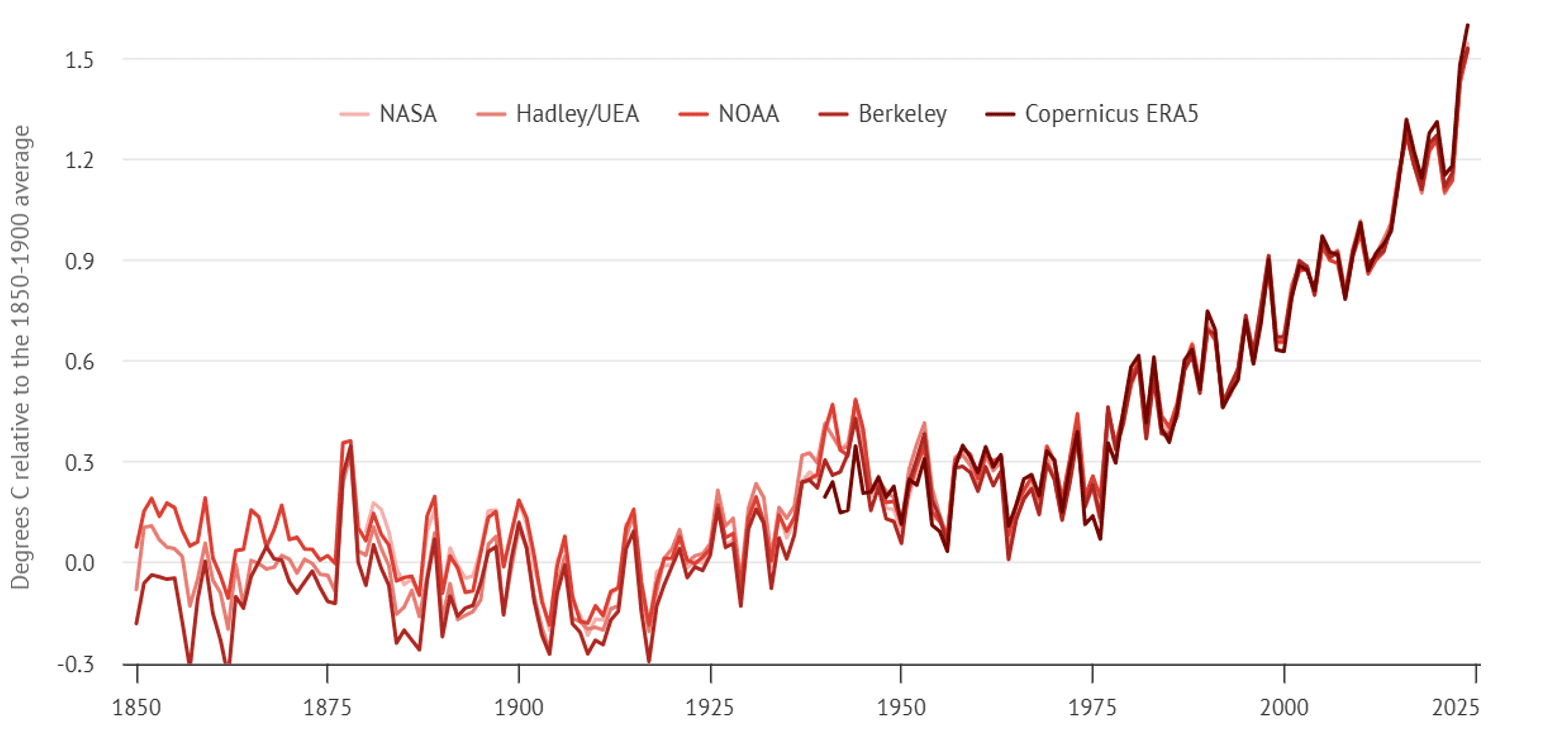

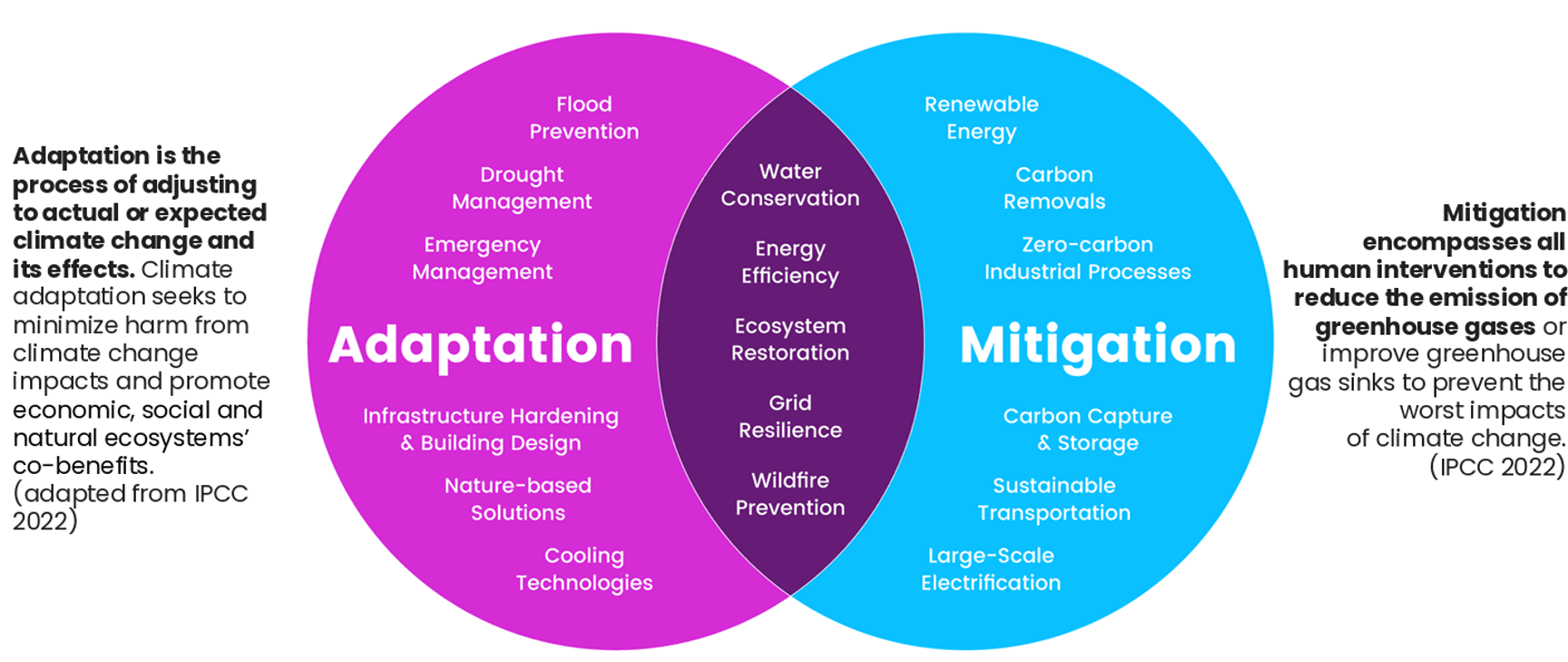

Reframing Net Zero: Investing in a >2°C World

The global climate trajectory has fundamentally shifted. We are moving beyond 'net zero pathways' to model how climate outcomes - not just targets - affect value and risk. In this latest paper, Dr Erin Kuo-Sutherland (Chief Sustainability...

Read more...

Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

The Skerryvore Global Emerging Markets All-Cap Equity Fund has returned +5.94% per annum since inception in August 2021, an outperformance of +2.48% relative to the MSCI Emerging Markets (MMEF) AUD benchmark which has returned +3.46% on an...

Read more...

Performance Report: Bennelong Australian Equities Fund

The Bennelong Australian Equities Fund rose by +2.58% in May. Since inception in February 2009, the fund has returned +10.90% per annum, an outperformance of +0.90% relative to the ASX 200 Total Return benchmark which has returned +10.00%...

Read more...