NEWS

Performance Report: Canopy Global Small & Mid Cap Fund

The Canopy Global Small & Mid Cap Fund saw positive contributions from Visional, HEICO and Dollarama in June, while Moncler, Hemnet and Wise weighed on performance. Canopy remains constructive on its holdings, citing strong fundamentals...

Read more...

Performance Report: Bennelong Long Short Equity Fund

The Bennelong Long Short Equity Fund rose by +4.14% in June, outperforming the ASX 200 Total Return benchmark by +2.73%. Since inception in February 2002, the fund has returned +12.48% per annum, an outperformance of +4.09% relative to the...

Read more...

Glenmore Asset Management - Market Commentary

Globally equity markets rallied strongly in June. In the US, the S&P 500 increased +5.0%, the Nasdaq rose +6.6%, whilst in the UK, the FTSE fell -0.1%

Read more...

Performance Report: Seed Funds Management Hybrid Income Fund

The Seed Funds Management Hybrid Income Fund rose by +0.49% in June. Since inception in October 2015, the fund has returned +6.34% per annum, an outperformance of +1.57% relative to the Solactive Australian Hybrid Securities (Net)...

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund rose by +1.87% in June, outperforming the ASX 200 Total Return benchmark by +0.46%. Since inception in November 2017, the fund has returned +20.06% per annum, an outperformance of +10.99% relative to...

Read more...

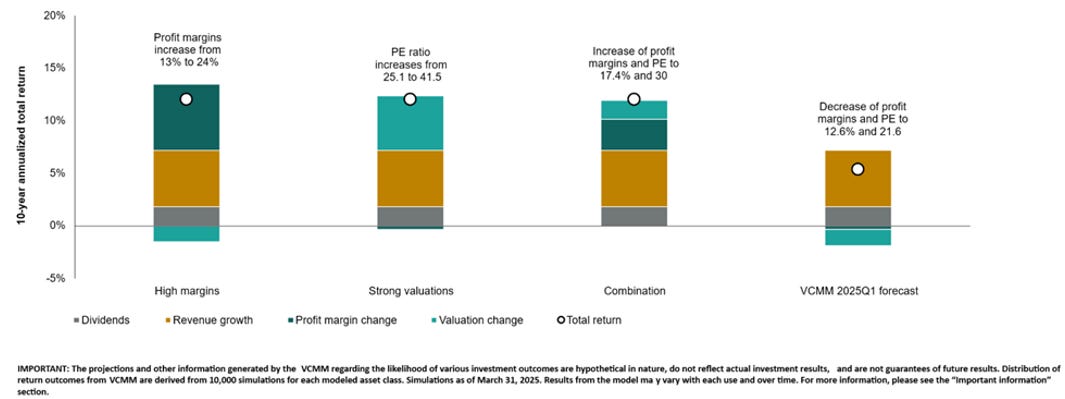

10k Words | July 2025

We get a bit fixated on US equity valuations, with Vanguard highlighting the high hurdles required to achieve another decade of >12% returns; even as the 10 year bond yield has been more competitive and tariffs drive negative earnings...

Read more...

Performance Report: ECCM Systematic Trend Fund

The ECCM Systematic Trend Fund rose by +1.19% in June. Since inception in January 2020, the fund has returned +11.23% per annum, an outperformance of +6.25% relative to the SG Trend benchmark which has returned +4.98% on an annualised...

Read more...

Performance Report: Quay Global Real Estate Fund (Unhedged)

The Quay Global Real Estate Fund (Unhedged) returned -0.25% in June, outperforming the FTSE EPRA/ NAREIT Developed NET TR benchmark by +0.69%. Since inception in January 2016, the fund has returned +7.00% per annum, an outperformance of...

Read more...

Trade deals and stimulus: the key drivers for stock returns

In the past year, investors have had to grapple with trade wars, military conflicts, rate cuts and recession fears. Nevertheless, global stocks returned 17% in the past 12 months in USD terms1, compared to 20% p.a. returns over the...

Read more...

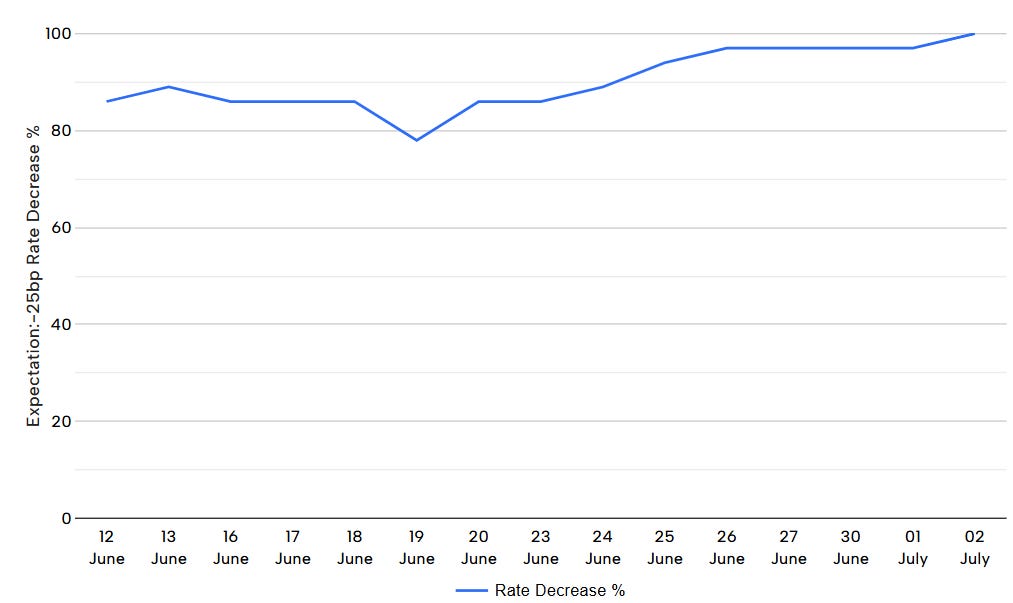

Hedge Clippings | 11 July 2025

According to the AFR, 32 out of the 36 economists that they surveyed prior to this week's RBA board meeting got it wrong. That's not very encouraging if you're making decisions based on their advice, and certainly not good for your bonus...

Read more...