NEWS

Invest in Your World

Are investors missing out on the value created from their increasing digital screen time?

It won't come as a surprise that over the last decade the average daily time spent on screens, which used to be restricted to television...

Read more...

Positive developments likely from the Retirement Income Review

The Australian Government Treasury (Treasury) discussion papers on retirement income highlight the increasing focus on a more comprehensive risk assessment of retirement income products.

The recently announced Retirement Income...

Read more...

Performance Report: Touchstone Index Unaware Fund

The Touchstone Index Unaware Fund rose +2.62% in September, outperforming the ASX200 Accumulation Index by +0.78% and taking annualised performance since inception in April 2016 to +11.91% with an annualised volatility of 9.79%.

Read more...

Hedge Clippings | 25 October 2019

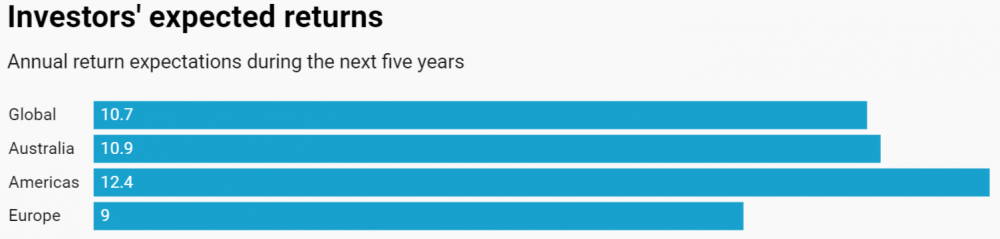

Equity Returns - are investors expecting too much?

An article published in the business section of the ABC News website on Thursday provided an insight and research into investor's expectations of annual returns from the share...

Read more...

Performance Report: Paragon Australian Long Short Fund

The Paragon Australian Long Short Fund has returned +10.48% p.a. since inception in March 2013. By contrast, the ASX200 Accumulation Index has returned +8.88% p.a. over the same period.

Read more...

Fund Review: Bennelong Long Short Equity Fund September 2019

Latest Fund Review for the Bennelong Long Short Equity Fund is now available. The Fund is a research driven, market and sector neutral, "pairs" trading strategy investing primarily in large-caps from the ASX/S&P100 Index...

Read more...

Why Cyan has sold out of Afterpay

Afterpay (APT) has been one of Cyan's most successful investments, having risen 30-fold from our initial investment at the $1 IPO in April 2016 to our exit on the 9th October at $33.50. In the 3.5 years since then, whilst we have made...

Read more...

Fund Review: Bennelong Twenty20 Australian Equities Fund September 2019

The latest Fund Review on Bennelong Twenty20 Australian Equities Fund is now available. The Fund invests in ASX listed stocks, combining an indexed position in the Top 20 stocks with an actively managed portfolio of ex-20 stocks.

Read more...

Performance Report: Quay Global Real Estate Fund

The Quay Global Real Estate Fund returned +0.9% in September, including a -0.1% return from currency. Since inception in January 2016, the Fund has returned +11.73% p.a. with an annualised volatility of 10.31%.

Read more...

Performance Report: Bennelong Australian Equities Fund

The Bennelong Australian Equities Fund rose +2.23% in September, outperforming the ASX200 Accumulation Index by +0.39% and taking annualised performance since inception in February 2009 to +13.74% versus the Index's +11.01%.

Read more...