NEWS

31 Mar 2020 - Performance Report: Wheelhouse Global Equity Income Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | To pursue this objective, the Investment Manager is responsible for actively managing, monitoring and tailoring the integration of derivative contracts alongside the Morningstar Portfolio, while taking into account changing market and stock specific conditions. The Investment Manager is responsible for maximising the structural benefits of short option positions (lowered Volatility, improved capital preservation, higher income generation), whilst mitigating, minimising and monitoring the structural negatives (variable market exposure, option expiries, collateral management and asymmetric return profiles). In addition, long derivatives positions are also used to enhance the capital preservation characteristics of the Fund in more extreme market movements. As a consequence of the integration of Derivatives, returns of the strategy, intra-cycle, are expected to vary from the underlying Morningstar Portfolio due to these characteristics. For example in weak markets, or in extended sideways markets, the Fund is expected to outperform relative to the Morningstar Portfolio. Conversely in strong positive markets the Fund is expected to underperform. |

| Manager Comments | The Fund's February return comprised -5.56% from the portfolio (in USD) and a positive return of +3.61% from the weakening of the Australian dollar versus the US dollar. Top contributors included Schneider Electric, Kerry Group, Tyler Technologies, Adobe and Sanofi. Key detractors included Western Union, Intel Corp, GlaxoSmithKline, Bank of America and United Technologies. |

| More Information |

30 Mar 2020 - Finding Defensive Funds in a Disorderly World | Insync Fund Managers

|

Australian Fund Monitors' CEO, Chris Gosselin, speaks with Monik Kotecha, CEO of Insync Fund Managers. Monik is the Chief Investment Officer of both the Insync Global Capital Aware Fund and the Insync Global Quality Equity Fund and in this video discusses his views on current market conditions and how he expects his funds to perform. Year to date (as at the end of February 2020), the Insync Global Capital Aware Fund and the Global Quality Equity Fund are up +4.48% and +2.14% respectively against AFM's Global Equity Benchmark which is down -2.05%. |

30 Mar 2020 - Performance Report: Datt Capital Absolute Return Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Our investment objectives are: 1) To minimise the risk of permanent capital loss 2) Generate a net return of 10% through the economic cycle An unconstrained, concentrated approach focused on superior risk-adjusted returns. The investment strategy: - targets long-term capital growth in a prudent manner, with an emphasis on capital preservation and low volatility in returns - aims to outperform in markets where equities are down - diversifies investments across asset classes and duration to reduce risk while maintaining relatively concentrated exposure to attractive investment opportunities - is an application of the Manager's investment process, that has no institutional constraints and is completely benchmark unaware |

| Manager Comments | In February the Fund's equity performance was negative, driven by the fall in their two largest exposures - Adriatic Metals and Alkane Resources. Datt Capital exited their holding in Whitehaven and added to their position in Alkane Resources. The manager continues to monitor a number of fixed income instruments in the distressed and special situation space. The Fund has no current derivative exposure. Current equity exposures are Afterpay, Adriatic Metals, Alice Queen, Alkane Resources, Argonaut Resources, Valmec and Yandal Resources. |

| More Information |

27 Mar 2020 - Hedge Clippings | 27 March 2020

|

|||||||||||||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

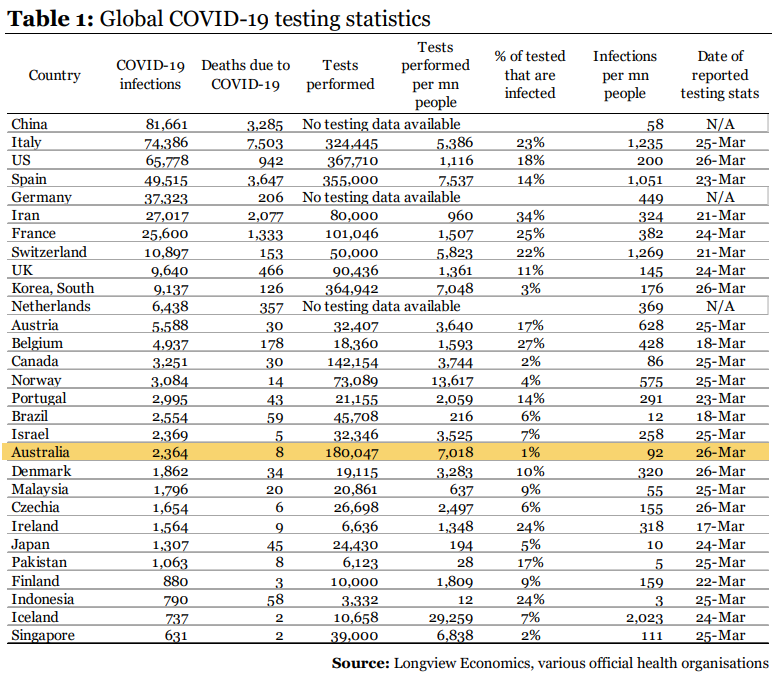

27 Mar 2020 - COVID-19 | Analysis from Longview Economics

27 Mar 2020 - Performance Report: Bennelong Twenty20 Australian Equities Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund is managed as one portfolio but comprises and combines two separately managed exposures: 1. An investment in the top 20 stocks of the markets, which the Fund achieves by taking an indexed position in the S&P/ASX 20 Index; and 2. An investment in the stocks beyond the S&P/ASX 20 Index. This exposure is managed on an active basis using a fundamental core approach. The Fund may also invest in securities expected to be listed on the ASX, securities listed or expected to be listed on other exchanges where such securities relate to ASX-listed securities.Derivative instruments may be used to replicate underlying positions and hedge market and company specific risks. The companies within the portfolio are primarily selected from, but not limited to, the S&P/ASX 300 Accumulation Index. The Fund typically holds between 40-55 stocks and thus is considered to be highly concentrated. This means that investors should expect to see high short-term volatility. The Fund seeks to achieve growth over the long-term, therefore the minimum suggested investment timeframe is 5 years. |

| Manager Comments | Bennelong's view is that the volatility currently plaguing markets is telling of markets' fear of uncertainty. At this stage, Bennelong believe the virus is a short-term disruption and that it could pass within the next few months. Once it has passed, they expect the outlook for equities to be favourable; markets will be looking ahead with the benefit of low interest rates, possible fiscal stimulus and some pent-up demand. Looking beyond the short-term view of the market, Bennelong have taken the opportunity to selectively up-weight their position in holdings that were heavily sold off but in which they continue to see long duration growth that will resume in time. They are also proactively managing risk by focusing on quality, and in particular, durable businesses with strong balance sheets. |

| More Information |

27 Mar 2020 - Performance Report: DS Capital Growth Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The investment team looks for industrial businesses that are simple to understand; they generally avoid large caps, pure mining, biotech and start-ups. They also look for: - Access to management; - Businesses with a competitive edge; - Profitable companies with good margins, organic growth prospects, strong market position and a track record of healthy dividend growth; - Sectors with structural advantage and barriers to entry; - 15% p.a. pre-tax compound return on each holding; and - A history of stable and predictable cash flows that DS Capital can understand and value. |

| Manager Comments | The Fund's focus on protecting investors' capital in falling markets is highlighted by the following statistics (since inception): Sortino ratio of 2.96 versus the Index's 1.01, down-capture ratio of 26.05%, largest drawdown of -8.80% versus the Index's -13.73%, and average negative monthly return of -1.43% versus the Index's -2.59%. |

| More Information |

26 Mar 2020 - Finding Defensive Funds in a Disorderly World | Kardinia Capital

|

Continuing the theme of "Defensive Funds in a Disorderly World", Australian Fund Monitors' CEO, Chris Gosselin, speaks with Kristiaan Rehder, Portfolio Manager of the Bennelong Kardinia Absolute Return Fund. Kristiaan shares his views on the current economic climate and how he expects the Fund to perform. To highlight the Fund's defensive nature, its largest drawdown throughout the GFC was -6.02% versus the ASX200 Accumulation Index's -47.19%. As at 29 February 2020, the Fund had returned +4.50% YTD against the Index's -3.08%. |

26 Mar 2020 - Loftus Peak building on 'Disruptive Innovation'

26 Mar 2020 - Performance Report: Cyan C3G Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Cyan C3G Fund is based on the investment philosophy which can be defined as a comprehensive, clear and considered process focused on delivering growth. These are identified through stringent filter criteria and a rigorous research process. The Manager uses a proprietary stock filter in order to eliminate a large proportion of investments due to both internal characteristics (such as gearing levels or cash flow) and external characteristics (such as exposure to commodity prices or customer concentration). Typically, the Fund looks for businesses that are one or more of: a) under researched, b) fundamentally undervalued, c) have a catalyst for re-rating. The Manager seeks to achieve this investment outcome by actively managing a portfolio of Australian listed securities. When the opportunity to invest in suitable securities cannot be found, the manager may reduce the level of equities exposure and accumulate a defensive cash position. Whilst it is the company's intention, there is no guarantee that any distributions or returns will be declared, or that if declared, the amount of any returns will remain constant or increase over time. The Fund does not invest in derivatives and does not use debt to leverage the Fund's performance. However, companies in which the Fund invests may be leveraged. |

| Manager Comments | The Fund returned -11.9% in February. Mid-month Cyan cut positions in three companies that they considered would be directly impacted by COVID-19: Atomos, McPhersons and Webjet. In the latter days of February and early March after further share price weakness they took the opportunity to add slightly to existing positions in Alcidion, Kelly Partners, Quickstep, Schrole and Vita Group. Cyan noted all of these businesses are well funded, enjoy growing revenue streams and in the case of Kelly Partners and Vita Group, enjoy dividend yields above 6%. Whilst the Fund is continuing to be impacted by the continued weakness in global markets, Cyan noted it has been holding reasonable amounts of cash for some time which is hugely beneficial in the current conditions. They are taking this opportunity to deploy some of this cash by increasing some existing positions and finding entry points for a number of new companies. They expect markets could see a swift and considerable upturn even before the current uncertainty clears. |

| More Information |