NEWS

24 Apr 2020 - Hedge Clippings | 24 April 2020

|

|||||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

24 Apr 2020 - Performance Report: Ark Global Fund - Class B AUD Hedged

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The investment objective of the Fund is to achieve long-term capital appreciation with low correlation to global equity markets through investment in the Underlying Fund. Fund One is a global macro fund that utilises quantitative research including machine learning techniques and fully automated trading algorithms which will aim to generate positive uncorrelated returns relative to any significant equity benchmark. The traded instruments are either major FX pairs or the most liquid exchange traded stock index, bond, and commodity futures across North America, Europe and Asia Pacific. The algorithm backtests over 10 years of tick data and in order to do so effectively requires machine learning to filter noise and identify meaningful signals, which results in statistically significant prediction of price movements. In production this processing is done in real time and the portfolio reacts to asset movements by rebalancing automatically to the desired risk exposure through the market impact optimised execution logic. Risk management layers built into the algorithm have been developed using the experience the team has gained from their decades in highly liquid fast-moving markets in the proprietary High Frequency Trading world. This allows the system to trade autonomously but safely to all trading opportunities and potential system issues, and to alert the team to any behaviour outside of strictly controlled bounds. The Fund is a 'feeder fund' which indirectly gains exposure to the underlying assets by investing all or substantially all of its assets in the Underlying Fund. The Fund may retain a certain amount of cash from the investment in the Fund for the purpose of payment of costs, fees, hedging and expenses. |

| Manager Comments | The best performing assets for the month were: 10 year Canadian Government bond futures (+3.17% of NAV), TOPIX futures (+2.34% of NAV), and E-mini Russell 2000 future (+2.16% of NAV). The worst performing assets were: E-mini NASDAQ 100 future (-1.22% of NAV), Euro Stoxx 50 future (-4.07% of NAV) and ASX200 Index future (-4.97% of NAV). |

| More Information |

23 Apr 2020 - Beware when the market and the economy are out of sync

23 Apr 2020 - Performance Report: Bennelong Kardinia Absolute Return Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund's discretionary investment strategy commences with a macro view of the economy and direction to establish the portfolio's desired market exposure. Following this detailed sector and company research is gathered from knowledge of the individual stocks in the Fund's universe, with widespread use of broker research. Company visits, presentations and discussions with management at CEO and CFO level are used wherever possible to assess management quality across a range of criteria. Detailed analysis of company valuations using financial statements and forecasts, particularly focusing on free cash flow, is conducted. Technical analysis is used to validate the Manager's fundamental research and valuations and to manage market timing. A significant portion of the Fund's overall performance can be attributed to the attention and importance given to the macro economic outlook and the ability and willingness to adjust the Fund's market risk. |

| Manager Comments | In March, the Fund's short book and low net market exposure protected the portfolio from the significant coronavirus-induced market decline. The Short Book contributed +600 basis points to performance. Other positive contributors included Fisher & Paykel, Fortescue, Jumbo Interactive and Rio Tinto. Key detractors included Macquarie, CBA, Aristocrat Leisure, Charter Hall and CSL. Net equity market exposure was increased from -5.6% to +28.4% (36.1% long and 7.7% short) during the month. Key changes to the portfolio included the closure of most of the Fund's individual stock shorts and a significantly reduced short position in Share Price Index Futures, partially offset by the sale of a significant portion of the long book. Kardinia also added a number of new long positions including Fortescue Metals, Fisher & Paykel Healthcare and JB Hi-Fi. |

| More Information |

22 Apr 2020 - New Funds on Fundmonitors.com

|

New Funds on Fundmonitors.com |

|

|

||||

| Levitas Capital Absolute Return VIX Fund (ARVIX) | ||||

|

||||

| View Profile |

|

||||

| The Airlie Australian Share Fund | ||||

|

||||

| View Profile |

|

||||

| Darling Macro Fund | ||||

|

||||

| View Profile |

|

||||

| Longlead Absolute Return Fund | ||||

|

||||

| View Profile |

| Longlead Market Neutral Fund | ||||

|

||||

| View Profile |

| Want to see more funds? |

|

Subscribe for full access to these funds and over 400 others |

22 Apr 2020 - Performance Report: Insync Global Capital Aware Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Insync employs four simple screens to narrow the universe of over 40,000 listed companies globally to a focus group of high quality companies that it believes have the potential to consistently grow their profits and dividends. These screens are size of the company, balance sheet performance, valuation and dividend quality. Companies that pass this due diligence process are then valued using dividend discount models, free cash flow yield and proprietary implied growth and expected return models. The end result is a high conviction portfolio of typically 15-30 stocks. The principal investments will be in shares of companies listed on international stock exchanges (including the US, Europe and Asia). The Fund may also hold cash, derivatives (for example futures, options and swaps), currency contracts, American Depository Receipts and Global Depository Receipts. The Fund may also invest in various types of international pooled investment vehicles. At times, Insync may consider holding higher levels of cash if valuations are full and it is difficult to find attractive investment opportunities. When Insync believes markets to be overvalued, it may hold part of its resources in cash, or use derivatives as a way of reducing its equity exposure. Insync may use options, futures and other derivatives to reduce risk or gain exposure to underlying physical investments. The Fund may purchase put options on market indices or specific stocks to hedge against losses caused by declines in the prices of stocks in its portfolio. |

| Manager Comments | In March, Insync sold down all remaining index put positions as volatility measured by the VIX index approached all-time highs mid-month, reflecting extreme fear and panic by investors. They also hedged a portion of the Fund's USD exposure back into Australian dollars as the Australian dollar fell significantly against the USD. Insync believe the portfolio is well positioned for the recovery in markets. Their view is that large-scale operations with the strongest balance sheets, a long runway for growth due to global megatrends and effective capital allocators are going to be the greatest beneficiaries as global economies start to recover. Insync noted the Fund's global megatrend companies are less sensitive to the economic cycle or crisis and have therefore not had to make significant changes to the portfolio. |

| More Information |

21 Apr 2020 - Performance Report: DS Capital Growth Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The investment team looks for industrial businesses that are simple to understand; they generally avoid large caps, pure mining, biotech and start-ups. They also look for: - Access to management; - Businesses with a competitive edge; - Profitable companies with good margins, organic growth prospects, strong market position and a track record of healthy dividend growth; - Sectors with structural advantage and barriers to entry; - 15% p.a. pre-tax compound return on each holding; and - A history of stable and predictable cash flows that DS Capital can understand and value. |

| Manager Comments | The Fund's capacity to protect investor capital in falling markets is highlighted by the following statistics (since inception): Sortino ratio of 1.15 versus the Index's 0.39, down-capture ratio of 45.22%, and an average negative monthly return of -2.06% versus the Index's -3.12%. DS Capital expect the current downturn to present many opportunities to the patient investor with a long-term view. They believe the evolution of the crisis will feature a total reset of earnings expectations and operating conditions along with many capital raisings. They noted every bear market lays the seeds for the next bull market and they are excited by the number of opportunities being worked on by the investment team. |

| More Information |

- Dynamic vs Static risk management

- Reviewing 1 year of the Darling Macro Fund

- Managing liquidity risk

- Contractual uncertainty

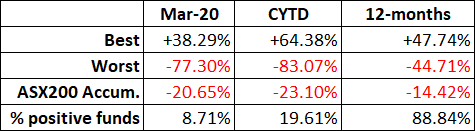

20 Apr 2020 - March 20 Insights

20 Apr 2020 - Performance Report: Loftus Peak Global Disruption Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The investment process involves a combination of top-down analysis with fundamental bottom-up qualitative and quantitative research to derive a risk-adjusted discounted cash flow (DCF) valuation of companies in the target universe. The investment team will generally buy stocks from the pool of securities that are trading below Loftus Peaks' valuation and sell them when they are trading above Loftus Peak's valuation. The approach allows for both fundamental accounting information as well as market-oriented inputs to be factored into the portfolio construction process. Loftus Peak's model typically does not rely on leverage to deliver investment returns and specifically takes into account risk in the valuation process. Capital preservation can be managed by holding up to 50% cash. Index and currency options and futures may also be used to manage risk. |

| Manager Comments | Top contributors in March included Apple, Netflix, Amazon and Tencent. Key detractors were Google, Qualcomm and Roku. The Australian dollar depreciated -5.1% over the month against the US dollar, which meant the value of the Fund's US dollar positions increased. As at 31 March 2020, the Fund carried a foreign currency exposure of 93%, giving it the ability to participate in any Australian dollar rebound from its decade-low levels. At month end, the Fund was 89% invested in 24 holdings with the balance in cash. |

| More Information |

17 Apr 2020 - Hedge Clippings | 17 April 2020

|

|||||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|