NEWS

China is Recovering

Economic patient zero is recovering, but no-one is immune to a relapse.

China is recovering, not only from COVID-19, but also from the GDP collapse caused by its lockdown. We know this because the central government has begun to...

Read more...

Where to Invest in a Post-Lockdown World

Now that governments are talking about re-opening the economy, investors can start thinking about the businesses that might provide the best returns as we emerge from economic hibernation. Here, I give a quick appraisal of the investment...

Read more...

The 'Beginning of the End', or the 'End of the Beginning'?

After a strong rebound in risk assets and some signs of a relaxation of the lock downs, we are now entering 'phase 2'. The actual damage done will become clear and fears about a viral resurgence are likely. Consequently, we expect a...

Read more...

Hedge Clippings | 01 May 2020

An article published in the UK's FT last week highlights an ongoing issue in the debate between Active and Passive investing. When it comes to analysing managed fund, and active funds in particular, it is worth remembering the old Castrol...

Read more...

A simple investing framework

With the number of headlines hitting the newswires on what feels like a minute-by-minute basis, it's easy to get lost in chasing data points. Instead, I believe that having a well-defined and broadly applicable framework to assess the...

Read more...

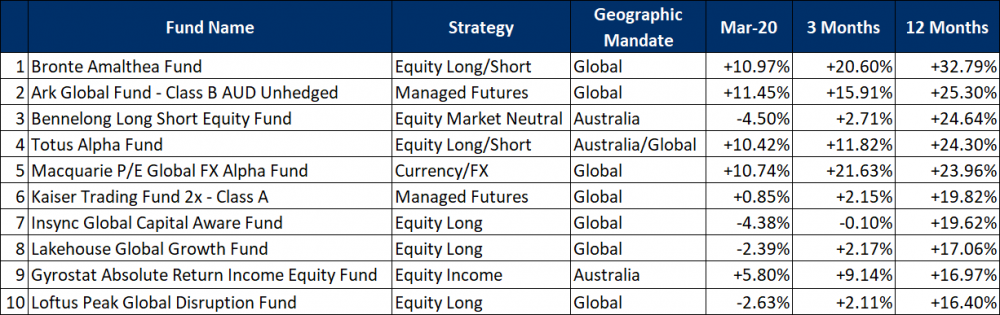

Performance Report: Ark Global Fund - Class B AUD Unhedged

The Ark Global Fund (unhedged) rose +11.45% in March, outperforming AFM's Global Equity Index by +19.52% and taking annualised performance since inception to +18.45% versus the Index's +8.92%.

Read more...

Performance Report: Wheelhouse Global Equity Income Fund

The Wheelhouse Global Equity Income Fund outperformed AFM's Global Equity Index by +7.48% in March, returning -0.59%. Over the quarter the Fund rose +2.17%, outperforming the Index by +12.13%. Since inception in May 2017, the Fund has...

Read more...

Performance Report: Delft Partners Global High Conviction

The Delft Global High Conviction strategy outperformed AFM's Global Equity Index by +0.88% in March. Since inception in July 2011, the strategy has returned +14.85% p.a. versus the Index's annualised return of +12.97% over the same period.

Read more...

Performance Report: Insync Global Quality Equity Fund

The Insync Global Quality Equity Fund has returned +14.63% over the past 12 months against AFM's Global Equity Index's +2.72%. Since inception in October 2009, the Fund has returned +12.74% p.a. versus the Index's +10.23%.

Read more...

Oklahoma - Where Oil Futures Go to Die

The day oil died was Monday the 20th of April 2020 - for the first time in history the price of a novated futures contract CL00 for Crude Oil WTI went negative ("CLK20" ticker on the CME for May 2020). It got buried -$37.63 below ground,...

Read more...