NEWS

28 Jul 2020 - Performance Report: Harvest Lane Asset Management Absolute Return Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Harvest Lane Asset Management employs a conservative, highly selective and opportunistic approach. Using their extensive knowledge in the area of corporate actions, the Fund's managers assess each opportunity based on a thoughtful, diligent and disciplined process and invest where they believe an opportunity exists to generate above average investment returns relative to the risk incurred. Investment decisions are made without speculating on market direction, with rigid risk controls enforced to minimise the risk of large losses of investor capital. The Fund invests in securities that are predominantly listed on the ASX and occasionally in those listed in other developed markets. Equity swaps and other derivatives may be used at times to reduce risk. The fund typically holds high levels of cash in the absence of sufficiently attractive opportunities to deploy investor capital in accordance with its objectives. |

| Manager Comments | Harvest Lane saw a resurgence of M&A activity in the first three days of June alone, while successful completion in some legacy holdings came as welcome news (much to the portfolio's benefit). They noted that, at the same time, some much needed confidence has been reinjected back into the domestic M&A market, however, they added that deal spreads continue to remain elevated reflecting the market's cautionary bias. The deal breaks Harvest Lane saw in recent months have largely been backed by private equity; Abano Healthcare, Metlifecare, CML Group, Olivers' Real Foods and Village Roadshow have all had bidders that are either entirely or majority backed by private equity, whereas completed deals in the last few months have typically come from strategic/corporate buyers. Harvest Lane noted they now view 'binding' transactions with the same level of suspicion as they have long viewed 'non-binding and indicative' approaches from private equity. Harvest Lane remain active with each new opportunity that presents itself. They believe current market conditions warrant an increased focus on risk management, however they noted they won't hesitate to transact where they recognise a favourable risk/reward opportunity. |

| More Information |

27 Jul 2020 - Performance Report: Insync Global Capital Aware Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Insync employs four simple screens to narrow the universe of over 40,000 listed companies globally to a focus group of high quality companies that it believes have the potential to consistently grow their profits and dividends. These screens are size of the company, balance sheet performance, valuation and dividend quality. Companies that pass this due diligence process are then valued using dividend discount models, free cash flow yield and proprietary implied growth and expected return models. The end result is a high conviction portfolio of typically 15-30 stocks. The principal investments will be in shares of companies listed on international stock exchanges (including the US, Europe and Asia). The Fund may also hold cash, derivatives (for example futures, options and swaps), currency contracts, American Depository Receipts and Global Depository Receipts. The Fund may also invest in various types of international pooled investment vehicles. At times, Insync may consider holding higher levels of cash if valuations are full and it is difficult to find attractive investment opportunities. When Insync believes markets to be overvalued, it may hold part of its resources in cash, or use derivatives as a way of reducing its equity exposure. Insync may use options, futures and other derivatives to reduce risk or gain exposure to underlying physical investments. The Fund may purchase put options on market indices or specific stocks to hedge against losses caused by declines in the prices of stocks in its portfolio. |

| Manager Comments | Insync noted the key to the Fund's outperformance over FY20 has been its downside risk management as well as the selection of stocks with long growth runways that aren't closely linked to prevailing economic conditions. The Fund's downside protection (Put options) is being rebuilt after the options were fully exercised in March when volatility reached closed to all-time highs. Insync maintains a positive view for the medium to long-term. Their view is that very low interest rates are making quality sustainable growth companies extremely valuable. They also expect the Megatrends in which they invest are likely to resist a severe recession and a pandemic. At month-end, the portfolio's top holdings included PayPal, Visa, Microsoft, Adobe, JD Sports Fashion, Walt Disney, Accenture, Facebook, S&P Global and Domino's Pizza. The top three Megatrends in the portfolio by weight were the 'Age Related Health Solutions' and 'Digitisation' megatrends (both at 14% of the portfolio), followed by the 'Cashless Society' megatrend (13% of the portfolio). |

| More Information |

27 Jul 2020 - Performance Report: Bennelong Concentrated Australian Equities Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The overriding objective of the Concentrated Australian Equities Fund is to seek investment opportunities which are under-appreciated and have the potential to deliver positive earnings, while satisfying our stringent quality criteria. Bennelong's investment process combines bottom-up fundamental analysis together with proprietary investment tools which are used to build and maintain high quality portfolios that are risk aware. The portfolio typically consists of 20-35 high-conviction stocks from the S&P/ASX 300 Index. The Fund may invest in securities listed on other exchanges where such securities relate to ASX-listed securities. Derivative instruments are mainly used to replicate underlying positions and hedge market and company specific risks. |

| Manager Comments | The main contributors to performance over the quarter were James Hardie, Breville Group, Fortescue Metals Group and IDP Education. The main detractors were CSL, Fisher & Paykel Healthcare and Afterpay. Bennelong maintain a reasonably balanced outlook for the market, trying not to be either too bullish or too bearish. They noted that, in this context, they continue to see good prospects for a continued recovery in the economy and market. |

| More Information |

24 Jul 2020 - Hedge Clippings | 24 July 2020

|

|||||||||||||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

24 Jul 2020 - Manager Insights | Spatium Capital

|

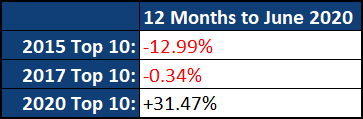

Damen Purcell, COO at Australian Fund Monitors, speaks with Jesse Moors and Nicholas Quinn from Spatium Capital. Jesse and Nicholas manage the Spatium Small Companies Fund, a long-only fund that invests in a portfolio of 25 - 40 ASX300 listed companies. Since the strategy's inception in July 2018, it has returned +15.52% p.a. against the ASX200 Accumulation Index's annualised return over the same period of +1.48%. Over FY20 the Fund rose +29.16%, outperforming the Index by +36.84%. |

24 Jul 2020 - Performance Report: Bennelong Emerging Companies Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund may invest in securities expected to be listed on the ASX within 12 months. The Fund may also invest in securities listed, or expected to be listed, on other exchanged where such securities relate to ASX-listed securities |

| Manager Comments | Over the June quarter the Fund outperformed the Index by +31.54% as the micro and small-cap stocks held by the Fund recovered even harder than the broader market. However, Bennelong reiterate that, while micro and small-cap stocks can deliver larger returns, they also come with significantly greater risk. This is highlighted by the fund's annualised volatility since inception of 36.54% against the Index's 17.40%. Top contributors included Viva Leisure, BWX, Baby Bunting, EML Payments and Mader. While each of these companies operate in very different industries, Bennelong noted they are all high quality and believe they have very promising growth prospects. As a result of the volatility seen so far in 2020, particularly in the micro and small-cap end of the market, Bennelong have made a number of changes to the portfolio. They believe the portfolio is currently well positioned for attracted returns over the long-term, regardless of the market's short-term movements. |

| More Information |

24 Jul 2020 - Performance Report: Frazis Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The manager follows a disciplined, process-driven, and thematic strategy focused on five core investment strategies: 1) Growth stocks that are really value stocks; 2) Traditional deep value; 3) The life sciences; 4) Miners and drillers expanding production into supply deficits; 5) Global special situations; The manager uses a macro overlay to manage exposure, hedging in three ways: 1) Direct shorts 2) Upside exposure to the VIX index 3) Index optionality |

| Manager Comments | Of the top 10 ASX stocks over FY20, the Frazis Fund had 3 - Afterpay (#1), Mesoblast and Polynovo. Frazis noted companies with brilliant products and broad customer support are faring significantly better than mature incumbents. Frazis believe there is a strong chance Afterpay will enter the Chinese market with Tencent, or at the very least, Hong Kong, which they expect would add years to the company's current growth runway. Other positive contributors over the quarter included Pinduoduo, Carvana, Tesla, Twist Bioscience and Moderna. Frazis believe the multiples of many technology stocks need to compress by 25-50% to re-enter normal valuation ranges. They noted this could happen quickly tomorrow or slowly over time. With this in mind, they are selectively holding companies that they expect to have 300 - 500% larger revenues in 3 - 5 years. Looking forward, the Fund will continue to be invested across its usual themes: Software, Solar & Renewables, Online Retail, Life Sciences, Fintech, Digital Health and companies that change the way people live. |

| More Information |

24 Jul 2020 - Stimulus Fuels Breakdown Between Markets and Economic Reality

23 Jul 2020 - The Rise of Restoration: A Focus on Oil and Gas Abandonment

23 Jul 2020 - Performance Report: Bennelong Australian Equities Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Bennelong Australian Equities Fund seeks quality investment opportunities which are under-appreciated and have the potential to deliver positive earnings. The investment process combines bottom-up fundamental analysis with proprietary investment tools that are used to build and maintain high quality portfolios that are risk aware. The investment team manages an extensive company/industry contact program which helps identify and verify various investment opportunities. The companies within the portfolio are primarily selected from, but not limited to, the S&P/ASX 300 Index. The Fund may invest in securities listed on other exchanges where such securities relate to the ASX-listed securities. The Fund typically holds between 25-60 stocks with a maximum net targeted position of an individual stock of 6%. |

| Manager Comments | Over the June quarter the Fund returned 21.90% against the Index's +16.48%. The main positive contributors to quarterly performance were James Hardie, Breville Group and Fortescue Metals Group. Bennelong noted that, while these stocks were sold off in the market downturn in the previous quarter, their operating businesses have held reasonably well despite covid-related headwinds. The main detractors included CSL and Fisher & Paykel Healthcare, both of which are defensive stocks that significantly outperformed during the previous quarter's downturn but which subsequently underperformed during the June quarter's recovery. Bennelong maintain a reasonably balanced outlook for the market, trying not to be either too bullish or too bearish. They noted that, in this context, they continue to see good prospects for a continued recovery in the economy and market. |

| More Information |