NEWS

24 Sep 2025 - Investment Perspectives: Riding the silver tsunami

23 Sep 2025 - Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

[Current Manager Report if available]

23 Sep 2025 - Australian Secure Capital Fund - Market Update

|

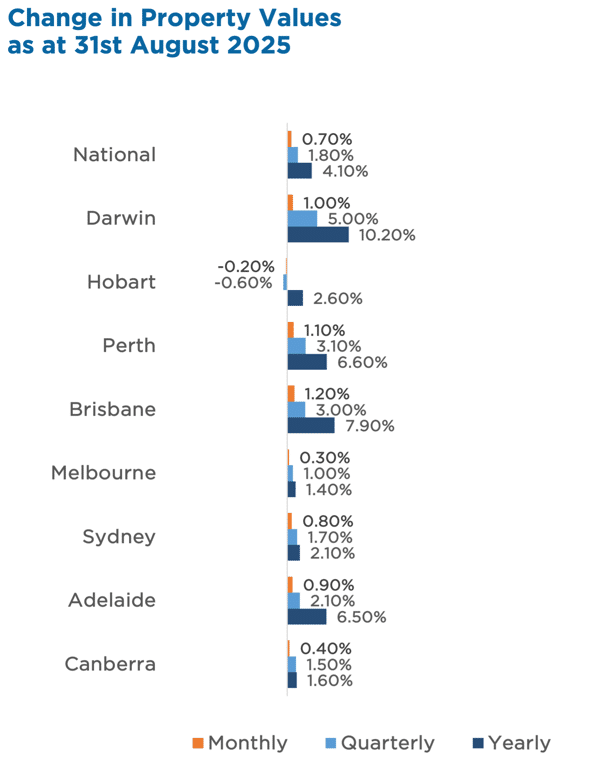

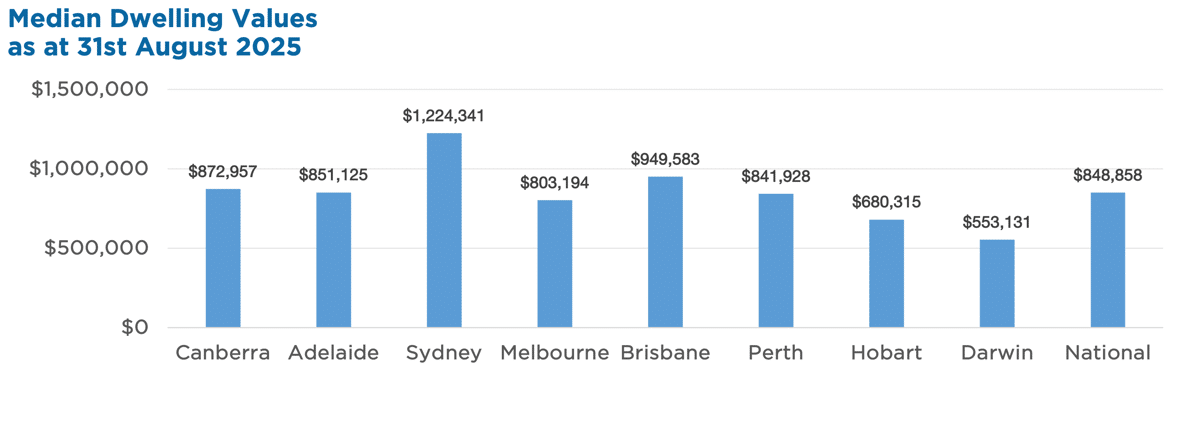

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund September 2025 Australia's housing market extended its run in August, with values up 0.7%. This is strongest monthly gain since May 2024. Annual growth now sits at 4.1%. Tight supply (listings 20% below average) and strong buyer demand pushed auction clearance rates to 70%. This is the highest since early 2024. Vendors are entering spring in a strong position, with low competition and broad-based price growth across the capitals. Highlights:

Property Values as at 31st of August 2025

|

22 Sep 2025 - Performance Report: DAFM Digital Income Fund (Digital Income Class)

[Current Manager Report if available]

22 Sep 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Arrowstreet Global Small Companies Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Arrowstreet Global Equity Fund (Hedged) | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Arrowstreet Global Equity Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Allan Gray Australia Balanced Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

19 Sep 2025 - Hedge Clippings |19 September 2025

|

|

|

|

Hedge Clippings | 19 September 2025

Hedge Clippings - All about the Donald! The US Federal Reserve did what markets had been anticipating - and Donald Trump has been crying out for - cutting rates by 25 bps and flagging that two more are on the way. Trump will claim the credit no doubt, and his new FED appointee Stephen Miren - direct from his day job at the White House - voted against the move, instead arguing for a .50% cut. However, Jerome Powell stuck to his guns, and it went by the numbers, 11-1 in favour of 0.25%. The move came off the back of weaker employment numbers as job growth has slowed, partly due to Trump's immigration policy, and despite stronger inflation, which Powell described as "somewhat elevated". But the complication is tariffs. While Trump won't admit it, his trade barriers are acting as a tax on consumers, pushing up the cost of goods and feeding through to inflation. So, while the Fed is easing with one hand, they're fighting a tariff policy that is tightening the screws with the other. For investors, it's a case of celebrating cheaper money while simultaneously wondering what it says about the health of the US economy - and whether tariff-induced inflation could yet bite harder. Still on Trump, across the Atlantic, the UK was busy polishing the silverware for his visit to Windsor Castle. King Charles, who has seen his fair share of world leaders, rolled out a stunningly lavish welcome. The photo-ops were dutifully staged, but one can't help speculating what was said behind closed doors once the motorcade departed. Did Charles turn to Camilla and mutter, "Thank goodness that's over", or perhaps, "Best to count the cutlery." Sadly, we'll never know. Jokes aside, markets remain in the uncomfortable space between policy and politics. Rate cuts are meant to provide reassurance, but they also underline fragility. Trade barriers are meant to project strength, but they tend to hurt the very economies that impose them, and the people who voted for them. And while royal pageantry makes for colourful headlines, investors would do well to tune out the theatre. As we often say, "let the numbers do the talking". Right now, in the US those numbers point to an uneasy mix: slowing growth, stubborn inflation risks, and the hope that monetary stimulus buys enough time for the economy to adjust. Whether it does so depends less on the pomp at Windsor, and more on how long consumers and businesses can shoulder the contradictions of easy money, and expensive trade. What's next on the local front? Albo's off to New York, where he's hoping to have a more successful time persuading Donald to see his point of view than he did this week while trying to keep PNG and Vanuatu out of the clutches of Beijing. Hopefully (not that hope is a reliable strategy), Trump, fresh from Windsor, will still have his warm and fuzzy side on show. News | Insights New Funds on FundMonitors.com 10k Words | Equitable Investors Australian Equities Reporting Season Update | Airlie Funds Management August 2025 Performance News |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

19 Sep 2025 - Performance Report: Canopy Global Small & Mid Cap Fund

[Current Manager Report if available]

19 Sep 2025 - Why the Gold Price Keeps Rising

|

Why the Gold Price Keeps Rising Marcus Today August 2025

|

|

Why does the gold price go up? Let me tell you the main reason the gold price goes up. All the gold dug up in the world is a lump of metal: 20.4m by 20.4m by 20.4m. That's all the gold ever dug up in the world. It grows about 2% per annum with production, and it shrinks about 2% per annum with consumption in things like electronics. So you've got this inert lump of metal, 20.4m square, sitting there -- earning nothing, doing nothing, looking pretty if it can -- and a whole load of people are running around it deciding what the price is. In the last couple of decades, two things have happened. One is exchange traded funds came along and bought. If it bought three metres by three metres by three metres, it completely changed the supply dynamics of this inert piece of metal. It's an amazing thought that if you could create an exchange traded fund backed by physical gold and start selling it, then as you sell you've got to find the gold. So you go into this inert, stable 20.4m cube and start buying chunks of it so that people invest in gold. It was self-fulfilling really. When exchange traded funds started in 2003, people started buying gold as an investment. It shoved demand up. Consequently, the gold price went from between $200 and $500 an ounce to $3,500. Now it's 20 years later and it's still going on. Exchange traded funds are buying gold, and when gold has a run it's a squeezy commodity to get hold of. That is backed by physical gold. So gold is being squeezed -- and squeezed again. Add on top of that currency. If you've got an inert piece of metal and everyone's running around it wondering what price it should be, and it's priced in US dollars, then because of a global financial crisis you print twice as many US dollars, the US dollar is worth half as much. For one thing it was the GFC, then Covid for another. Print twice as many US dollars and the currency is worth half as much. So the price of gold, and anything else priced in US dollars, doubles -- not because gold is worth any more, but because the currency is worth less. That's what's driven the gold price as well. One of the biggest drivers for the gold price is when the US dollar goes down. You'll find the gold price goes up. At the moment the US has a lot of debt. That weakens the currency. A currency is really a reflection of how strong an economy is. If they put tariffs in and it slows the US economy down, the US dollar goes down. If they start to cut interest rates, which it looks like they're going to, the currency goes down because it doesn't yield as much. All this is pushing towards a weaker US dollar. And a weaker US dollar is going to cause the gold price to go up again. So combined with the risk of "The Big One", a falling US dollar, exchange traded fund buying -- the gold price goes up. And that's what's going on at the moment. DISCLAIMER: This content is for general information purposes only and does not constitute personal financial advice. Please consider your own circumstances or seek professional advice before making investment decisions. |

|

Funds operated by this manager: |

18 Sep 2025 - Performance Report: Cyan C3G Fund

[Current Manager Report if available]

18 Sep 2025 - Build-to-rent housing: igniting the firepower of local pension funds

|

Build-to-rent housing: igniting the firepower of local pension funds abrdn September 2025 The UK is at a critical juncture in addressing its long-standing housing undersupply. While the challenge of meeting housing demand is not breaking news, the scale of the shortfall keeps making headlines. In 2024, a shake-up in how housing need is calculated pushed the government's annual target to a bold 370,000 homes - a 20% jump from the previous benchmark. Ambitious? Absolutely. But let's be clear: the UK hasn't built at this pace since the late 1960s. If we're serious about unlocking economic growth and making housing more accessible, we need a smarter, more scalable strategy. That means building where demand is surging - and today, that's in our cities. With urban living on the rise, the build-to-rent (BtR) sector is perfectly positioned to lead the charge. Chart 1: Annual housing completions Investing and planning to meet housing targetsMeeting national housing targets requires action across all tiers of governance and investment. National policy must provide the enabling framework, regional authorities must align infrastructure and planning priorities, and local councils must accelerate approvals and unlock land. At the same time, institutional capital - particularly from local government pension schemes (LGPS) -must be mobilised to support long-term, scalable development. Developers also have a pivotal role to play in delivering housing and responding to shifting demand dynamics. With urbanisation driving housing demand, the BtR sector stands out as a key delivery mechanism that's capable of providing high-quality, professionally managed housing at scale. A step-change in delivery is not optional, it's essential. Unlocking land, streamlining planning, and mobilising long-term capital must now become national priorities. Local versus national housing targetsNational housing targets are coordinated by central government policy; they're based on broad long-term growth rates and affordability ratios. The government aims to tackle the housing crisis by building 1.5 million homes by 2030. It will use planning reforms to unlock greyfield and brownfield land[1], while significantly expanding affordable and social housing. One challenge of a predominantly national approach is that housing targets are often set using broad criteria, which may not fully capture local nuances and needs. Over the long term, they can fail to consider the economic and social impacts that well-targeted and appropriate levels of housebuilding can have at a local level. Some regions can be left behind. Focusing on local needsIn contrast, local housing delivery is led by local authorities and region-specific entities. These are much more concentrated on local city, town and regional housing needs, often considering local economic growth and regeneration agendas. Perhaps the most powerful point about locally anchored strategies is that they don't have to be mutually exclusive with national targets. In fact, central policy is already working to empower local authorities to deliver social housing, using national targets as a framework[2]. Local authorities can come under considerable pressure to meet these targets, leading to tensions when national expectations don't align with local needs or capacities. Therefore, local targets can more effectively leverage the motivations of local authorities, who can be the foremost institutional investors[3], given the scale and influence of LGPS. LGPS can be the firepower that housing needsThe 86 local authority pension funds in England and Wales now invest through eight main LGPS (ACCESS Pool, Border to Coast, Brunel, LGPS Central, LPP, London CIV, Northern LGPS, and Wales Pension Partnership). With these pools soon consolidating from eight to six, this shift will deliver even greater concentrated firepower. It will be possible to mobilise large-scale investment with enhanced professional oversight and strategic focus. Through this collective strength, current total LGPS assets of nearly £400 billion are set to grow to £1 trillion by 2040[4]. As these pools look to invest more into housing, this approach could support the delivery of up to 80,000 homes across the UK, according to research by Savills[5]. This represents around 60% of current BtR stock, which suggests the speed of delivery could really accelerate. Chart 2: Cumulative delivery of Build-to-Rent units from 2013 to 2025

How can LGPS help the housing crisis?Not only do LGPS pools have considerable financial firepower, they also have traits that make them uniquely suited to national housing initiatives. Working in partnership for BtR housingWhile LGPS pools possess critical mass, there is substantial value and capability to be added from private capital. Aberdeen can use the scale of LGPS pools to deliver high-quality rental housing that supports both local communities and national policy targets. Leaning on our existing relationships, we can comingle additional funding, use our own sector-specialists, and bring in operational expertise, all while improving resource efficiencies. We can then use this scale to diversify and deploy capital into smaller catchments, which would otherwise be unreachable by institutional investment. Working with the John Lewis Partnership, we can go one step further by unlocking well-located city-centre locations for redevelopment. This will deliver much-needed housing in urban markets through a nationally recognised and trusted brand. By adding existing BtR assets across local authorities, we can cement local goals while servicing national housing targets. Final thoughts...The net result of partnering with local authorities means that locally driven housing initiatives can be delivered at scale across regions. We can blend fiduciary duty with social outcomes that neither local authorities nor the private sector could fully accomplish alone. By helping to facilitate public-private partnerships, we can increase collaboration among pension pools and make national-level housing targets more achievable. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) |