Read the full article here: REITs and inflation - where is the sweet spot?

NEWS

Higher inflation can be a friend to real estate investors

8 Sep 2021 - Quay Global Investors

When investing in real estate, higher inflation is more likely to be a friend than a foe, helping protect investment from supply side issues and driving up the residual value of improvements, says Justin Blaess, portfolio manager at Quay...

Read more...

8 Sep 2021 - Higher inflation can be a friend to real estate investors

By: Quay Global Investors

|

Higher inflation can be a friend to real estate investors Quay Global Investors August 2021 |

|

When investing in real estate, higher inflation is more likely to be a friend than a foe, helping protect investment from supply side issues and driving up the residual value of improvements, says Justin Blaess, portfolio manager at Quay Global Investors.

"Indeed, we believe real estate - and thereby listed real estate - is a good inflation hedge. Land is tangible, and well-located land has an intrinsic value; it can be used as a place to build shelter or as a place to do business or access services. "Because of supply constraints, well-located land will generally appreciate over time. In addition, the cost of replacing any improvements built on the land will also increase through inflation. This is significant, because if there is excess demand for a type of real estate, the market will have to accept rising costs and thereby the rents required to economically justify construction - regardless of the inflation environment. "Investors in real estate - both direct and listed - can therefore benefit from a higher inflation environment, particularly compared to global equities investments." Mr Blaess says it's worth understanding how listed real estate has performed in previous periods where inflation has been elevated. "Some questions for investors to consider include: at what levels of inflation does real estate perform best? Can there be too much inflation? Not enough inflation? What if the current US bond yields are correct (currently 1.2 per cent per annum) and we are headed for sustained low inflation?" To answer these questions, Quay analysed US REIT and S&P500 real and nominal returns by constructing indices for when headline CPI was both less than and greater than 3 per cent and in increasing increments of 1 per cent. From these indices the average monthly nominal and real returns could be calculated for the purpose of comparison. "Our analysis shows that listed real estate is an excellent hedge for inflation and has historically delivered strong positive nominal and real returns in higher inflationary environments. It also offers a better relative return when compared to general equities. "This is especially so when inflation is in the moderate 3 to 6 per cent range, where listed real estate has historically generated more than double the real return relative to equities. Even with very high inflation (6 per cent and above), listed real estate continues to outperform equities (albeit at a lower relative level than in a moderate inflation scenario). "It's also interesting to note that over the past 50 years, inflation has been above 3 per cent more often than below. When it has been below 3 per cent, listed real estate nominal and real returns have been quite a bit lower than in a moderate inflation environment. And contrary to common belief, in lower inflation settings listed real estate returns actually tend to lag equities. "So as someone with a vested interest in the performance and outlook for real estate, when it comes to inflation, we say 'take a long view and don't be fearful'," Mr Blaess says. |

|

Funds operated by this manager: Quay Global Real Estate Fund |

Reporting Season Insights | Cyan Investment Management

7 Sep 2021 - Australian Fund Monitors

Chris Gosselin, CEO of Australian Fund Monitors, speaks with Graeme Carson, Director & Portfolio Manager at Cyan Investment Management.

The Cyan C3G Fund has a track record of 7 years and has outperformed the ASX Small...

Read more...

7 Sep 2021 - Reporting Season Insights | Cyan Investment Management

By: Australian Fund Monitors

|

Chris Gosselin, CEO of Australian Fund Monitors, speaks with Graeme Carson, Director & Portfolio Manager at Cyan Investment Management. The Cyan C3G Fund has a track record of 7 years and has outperformed the ASX Small Ordinaries Total Return Index since inception in July 2014, providing investors with a return of 15.58% per annum, compared with the index's return of 9.42% p.a. over the same period. The manager has delivered this outperformance while maintaining a down-capture ratio since inception of 52%, indicating that, on average, it has only fallen half as much as the market during the market's negative months.

|

Is your fund manager skilful or just lucky?

7 Sep 2021 - Andrew Mitchell, Ophir Asset Management,

In this article we outline how investors can try to tell which funds managers have 'skill' - and can be expected to keep outperforming for a long time -- and those that are simply 'lucky' and likely to disappoint when markets change.

Read more...

7 Sep 2021 - Is your fund manager skilful or just lucky?

By: Andrew Mitchell, Ophir Asset Management,

|

Is your fund manager skilful or just lucky? Andrew Mitchell, Ophir Asset Management August 2021 |

|

There is no doubt in the world of sport that the likes of 20-time tennis Grand Slam winner Roger Federer outperforms because of skill, not luck. When investors evaluate the performance of equity funds, however, it's not as obvious which funds are skilled or have just been lucky. Fund manager league tables were recently released for the last financial year, and the media, as usual, trumpeted funds with hot performance. But now is a particularly difficult time for investors to assess fund managers. With markets rising, some funds have just been lucky and ridden strong gains. There is now a danger that investors chase these hot, lucky funds and become saddled with poorly performing investments for years. In this article we outline how investors can try to tell which funds managers have 'skill' - and can be expected to keep outperforming for a long time - and those that are simply 'lucky' and likely to disappoint when markets change. If investors can spot the difference, they are significantly more likely to choose the right fund for them, a fund that delivers sustained performance, and a fund that ultimately helps them reach their financial and lifestyle goals. The skilled few The big problem for investors is that few funds are truly skilled. In a 2014 report on equity investing, Willis Towers Watson, the global investment consulting firm, argued that only 10 per cent of fund managers could be considered genuinely skilled over the long term, while 70 per cent show mediocre performance and 20 per cent are inferio The fact that so few managers were deemed truly talented is a product of the multiple forces which influence portfolio performance, such as:

Obviously, managers that perform via the first four should be avoided. But how can we tell who has the right qualities to be considered genuinely talented managers? 4 attributes of the skilled Although no specific rule book exists on how this should be judged, we believe that skilled investors have four characteristics in common. 1. They perform through time The number one attribute of skilled investment managers is their performance over time. By studying this, we can observe if performance has aligned with their intended investment style. For example, if they are a "Growth" style manager have they tended to perform well when that style is in favour? If they are an "all -weather" manager, have they been able to perform well through all different kinds of market environments? We can also measure how persistent returns have been across different stages of the market cycle. 2. They have a high number of winning bets One should also study the number of bets made over time. A manager who makes many bets over time, and wins a reasonable number of them, deserves to be rated far higher than a manager whose success is solely attributable to one or two knockouts. The former manager has been tested more times, and hence we can be more confident in their ability to replicate that success in the future. 3. They are on a quest for "better" Besides just looking at each manager's track record of returns, those with skill at investing have an attitude to their craft that combines intensity, flexibility, and humility. These managers have a passion for investing and are constantly striving to put in the work to become more skilled investors. 4. They accept the role of chance At the same time, best-in-class investors are aware of the role of chance in their investment outcomes and don't try to paint their success as pre-ordained. By contrast, fund managers who don't realise how much chance impacts their results can end up being painfully stubborn or arrogant. And when the environmental variables that help outperformance eventually stop, a humble manager is more likely to adapt and evolve their process commensurately. The harsh reality is that even a skilled investment manager will underperform at times, and an unskilled manager can outperform, potentially even for years. Still, the longer the period over which a given investment manager delivers superior performance, and the larger the investment base involved, the more likely the results reflect skill rather than luck. To put this another way, over time as an investor becomes more skilful, their performance should become more consistent. Like medical research So how do professional fund manager selectors statistically test whether a fund manager's performance is truly different from their benchmark, or the market? They perform tests similar to the type medical researchers use to test whether a drug's treatment of a condition is statistically different from a placebo. A simplified example of this test is below: Where:

T = the so-called 'test statistic' X = is a measure of the outperformance (if positive) or underperformance (if negative) of the fund versus the benchmark. (Note: providing the benchmark is 'risk-equivalent' to the Fund) N = is a measure of how long the fund has been going for S = is a measure of the volatility of the outperformance or underperformance of the manager through time A 'test statistic' greater than about 2 means you have 95%+ confidence that the manager's outperformance or underperformance is different to zero. This level of confidence is the most commonly used to determine if something is truly different from its comparator or baseline. 3 takeaways What you can quickly see is that both the greater the size of the outperformance and the longer the manager's track record are both positive attributes. Also, the lower the volatility of the outperformance, the more likely that outperformance is 'statistically significant' (different to zero) and due to skill rather than luck. Some takeaways from this are:

Secretly skewing to small caps More sophisticated statistical tests also exist to help ensure managers aren't simply outperforming by taking more risk than is embedded in the benchmark or market they are trying to outperform. A manager, for example, might claim outperformance during a bull market, but they only outperformed because they used leverage in their fund to increase its risk, and hence returns, in that market environment. Finally, we need to question whether a fund's investment returns represent exposure that could be obtained at a much lower cost by investing through passive-type products. In such instances, there is no need to pay fees to a skilful investment manager to access these returns. For example, small-cap equities, which is our space, have tended to outperform large-caps across many different equity markets over long periods of time. Investors should turn their nose up at large-cap managers who skew their funds to small caps, and where their small cap holdings have accounted for a meaningful share of their outperformance over their large-cap benchmarks. Sorting the skilled from the plain lucky To summarise, it is clear there is much to think about when trying to determine whether a manager's returns have been due to skill rather than luck. Hopefully we have dissuaded you though from putting too much weight on a manager's short term annual returns reported in the so-called 'leagues tables' in the press! At Ophir we judge the performance of our funds, and our analysts who contribute to it, primarily on its size, duration, consistency, and number of unrelated positions that have led to the result. We also seek to control for excessive risks that could jeopardise absolute performance over the long run. As long-time readers will know, we think there are two other key criteria that help the skill of any manager shine through:

There are of course many other factors to consider as well when trying to disentangle the skilled from the unskilled, but the above is what we consider to be some of the most important here at Ophir. |

|

Funds operated by this manager: Ophir High Conviction Fund (ASX: OPH) |

Reporting Season Insights | DS Capital

6 Sep 2021 - Australian Fund Monitors

Chris Gosselin, CEO of Australian Fund Monitors, speaks with Rodney Brott, CEO & Executive Director of DS Capital.

The DS Capital Growth Fund has a track record of 8 years and has consistently outperformed the ASX 200 Total...

Read more...

6 Sep 2021 - Reporting Season Insights | DS Capital

By: Australian Fund Monitors

|

Chris Gosselin, CEO of Australian Fund Monitors, speaks with Rodney Brott, CEO & Executive Director of DS Capital. The DS Capital Growth Fund has a track record of 8 years and has consistently outperformed the ASX 200 Total Return since inception in January 2013, providing investors with a return of 16.77%, compared with the index's return of 9.94% over the same period. DS Capital has delivered these returns with -2.44% less volatility than the index, contributing to a Sharpe ratio which fallen below 1 once and currently sits at 1.31 since inception.

|

High-margin, asset-light businesses are the best defence against inflation

6 Sep 2021 - Claremont Global

With the latest US CPI reading over 5%, we have been receiving a number of questions from investors about what this means for the future composition of our portfolio.

Read more...

6 Sep 2021 - High-margin, asset-light businesses are the best defence against inflation

By: Claremont Global

|

High-margin, asset-light businesses are the best defence against inflation Bob Desmond, Claremont Global August 2021 |

|

With the latest US CPI reading over 5%, we have been receiving a number of questions from investors about what this means for the future composition of our portfolio. Well, the simple answer is not that much ― and here's why.

The difficulty with economic forecasts As regular readers of our articles will know, we believe that accurate and consistent economic forecasts are exceptionally difficult, and it is even more difficult to successfully construct a portfolio to express such a view. We received a very good example of this in March as the US 10-year Treasury bond yield moved above 1.70 per cent on stronger economic growth and fears of higher inflation. One view accompanying this move was that now was an opportune time to sell "growth" businesses and buy their "value" counterparts. The narrative was that growth companies will suffer disproportionately as the market attaches a higher discount rate to their future profits - which are longer duration than their more cyclical value counterparts. In addition, more cyclical companies can expect to see a recovery in their profitability due to stronger economic growth. At a basic level, you can edit the "sell growth, buy value" argument to "sell technology, buy financials". In June we wrote an article where our advice was - and continues to be - don't sell great businesses based on an uncertain economic forecast! And once again, recent events have turned out to be somewhat different than consensus expectations. Bond yields have since retreated to 1.2% ― which when combined with some exceptional "big tech" earnings over the last two quarters has seen a strong rally in many of their share prices.

Another quarter of big tech earnings growth To illustrate this, let's take our portfolio's two technology companies - Alphabet and Microsoft - which saw their revenue rise by 62% and 21% respectively, an astonishing result for companies of their size. Admittedly Alphabet was up against an easy comparison last year, as COVID-19 cut advertising revenue ― however, even on a two-year basis revenue is still up by 26% a year. In contrast, JP Morgan - one of the world's most respected banks - saw their revenue fall by 8% year-over-year.

Or, even if we look at the events of the last 18 months - an authority no less than the Reserve Bank forecasted that the Australian economy would shrink by 20% as a result of COVID-19, whilst the reality is an economy that is actually larger than pre-pandemic. But to the point of this article … let's assume that the macro forecasters are correct and inflation rises materially in coming years. What type of businesses would you want to own?

Lessons from Zimbabwe I do have some experience in this regard, having spent the early part of my career in Zimbabwe under hyperinflationary conditions. While this is an obviously extreme case, it's still worth trying to draw some lessons from that experience. Intuitively, one's immediate response (and one you often see in the media) is to "buy assets". However, my experience was that the best businesses to own in inflationary periods are asset-light ones, and more obviously those with pricing power and high margins. As inflation rises, so do the capital demands of the business you own. This includes the capital that needs to be invested in working capital and fixed assets, with the inevitable impact that has on free cash flow. In Zimbabwe, it was not uncommon to see companies report exceptional profits, as inventory and depreciation was expensed through the income statement at much lower historical prices. In contrast, free cash flow was far lower than profit, as new inventory and fixed assets are replaced at much higher prices. Warren Buffett described this aptly when writing about inflation in the 1970s:

In our companies, two key metrics we focus on are gross margin and capital expenditure to sales. Companies that have a high gross margin are often blessed with a low cost/high-value ratio from a client perspective. This means they are a very small part of a customer's cost but are essential to running that business and have few substitutes. Microsoft provides immense value relative to the cost A clear example in our portfolio is Microsoft. What company can afford to turn their subscription off to save on costs and how much cost would they really save anyway? The monthly subscription to Office 365 is only $29 a month for an enterprise customer. There is an immense value provided relative to the cost. The worst business to own is one that has:

The first thing a CFO is going to do when costs are rising, is look at the list of the largest suppliers and ask them to reduce costs ― just at a time when those suppliers own costs are rising. Good luck trying to ask Microsoft to reduce prices! The combination of limited pricing power and asset intensity can be particularly pernicious. A business cannot raise prices in line with inflation, whilst simultaneously its own capital needs are accelerating as the "tapeworm" of inflation requires more dollars to be spent just to maintain unit volume and its capital base. If things get bad enough, free cash flow turns materially negative. And in this scenario, the company takes on debt (at ever-higher interest rates as inflation rises) or is forced to issue equity at depressed prices ― resulting in permanent value destruction.

Allocate your capital as a CEO would Across our portfolio, the weighted gross margin is 55% and this compares to 35% for the S&P 500, which demonstrates the competitive advantage and the inherent pricing power of our businesses. Our capital expenditure to sales ratio is 5% versus the market at 7.9%. As such, our businesses have a collective gross margin that is more than 57% higher than the market, with capital expenditure needs that are 37% lower. It makes no business sense to us to sell some of the best businesses in the world to buy slower growing, lower margin and more cyclical businesses on the basis that inflation is just around the corner. After all, which CEO do you know who would sell the highest margin, most asset-light, cash generative, competitively advantaged divisions to reinvest capital in the lower margin, capital intensive ones on a view that higher inflation is on the way? To quote Warren Buffett again:

High conviction investing Claremont Global is a high conviction portfolio of value-creating businesses at reasonable prices. |

|

Funds operated by this manager: Claremont Global Fund |

Hedge Clippings | 03 September 2021

3 Sep 2021 - Australian Fund Monitors

Last week we flagged the record second quarter earnings season in the US. By any measure the Australian reporting season just ended will also go down as one of the strongest on record, no doubt justifying market valuations which are also...

Read more...

3 Sep 2021 - Hedge Clippings | 03 September 2021

By: Australian Fund Monitors

|

|||||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

Investment Perspectives: REITs and inflation - where is the sweet spot?

3 Sep 2021 - Quay Global Investors

To examine the impact that different levels of inflation have had on listed real estate, we have looked at the returns over the last 50 years in absolute and real terms, and relative to general equities. Because global real estate indices...

Read more...

3 Sep 2021 - Investment Perspectives: REITs and inflation - where is the sweet spot?

By: Quay Global Investors

|

Investment Perspectives: REITs and inflation - where is the sweet spot? Quay Global Investors August 2021 |

|

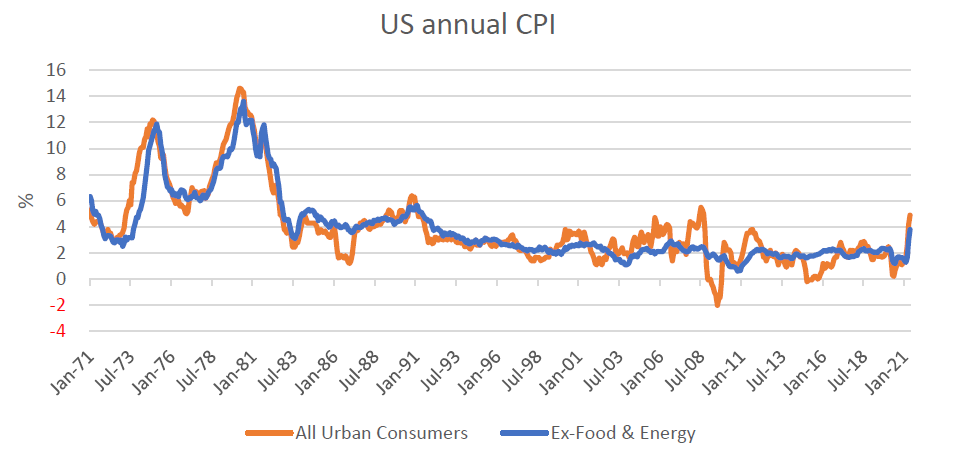

We've often stated that real estate (listed and direct) tends to outperform equities during periods of high inflation and have previously cited the following chart as evidence of this dynamic. Source: NAREIT, Bloomberg, Quay Global Investors What is not clear is whether listed real estate outperforms during moderate (say between 3-6%) or higher levels of inflation (say +7%). While these levels of inflation may seem rare, the fact is that over the last 50 years US inflation has been above 3% more times than below. And during such periods, the nominal returns for listed real estate have been higher than low inflationary environments; and relative to equities, higher in both nominal and real terms. The rise and rise of CPI Anecdotally, we believe real estate - and thereby listed real estate - to be a good inflation hedge. Land is tangible, and well-located land has an intrinsic value in that it can be used as a place to build shelter or as a place to do business or access services. Because of supply constraints, well-located land will generally appreciate over time. In addition, the cost of replacing any improvements built on the land will also increase through inflation. This is important, because if there is excess demand for a type of real estate, the market will have to accept rising costs and thereby the rents required to economically justify construction - regardless of the inflation environment. Last month saw the US Bureau of Labour Statistics (BLS) release CPI for June (see following chart). For the last 4 months it has continued to rise and is now at a 5.4% 12-month increase, which is the largest such increase since the heady days before the GFC in August 2008. And if we exclude volatile food and energy prices from this headline number, while the absolute level is lower it is now the highest CPI print for this adjusted series since November 1991. Discussion around the impact of rising inflation on investment returns is now firmly on everyone's lips. Source: US Bureau of Labor Statistics There are pundits that believe this is cause for concern for the bond market, the stock market and the US dollar. All three could have an impact on our portfolio returns, but a lot will depend on whether this inflation is transitory in nature or not. We have previously published our thoughts on the debate here. Regardless, it is worth understanding how listed real estate has performed in previous periods where inflation has been elevated. More specifically, at what levels of inflation does real estate perform best? Can there be too much inflation? Not enough inflation? What if the current US bond yields are correct (currently 1.2% per annum) and we are headed for sustained low inflation?

What it means for real estate To examine the impact that different levels of inflation have had on listed real estate, we have looked at the returns over the last 50 years in absolute and real terms, and relative to general equities. Because global real estate indices don't go back this far, we have instead used US REIT data and compared it to the S&P500. In our opinion, this represents a good proxy for listed global real estate given the large size and diversity of the US REIT market and also that it represents greater than 50% of the global sector. The methodology was to analyse US REIT and S&P500 real and nominal returns by constructing indices for when headline CPI was both less than and greater than 3% and in increasing increments of 1%. From these indices the average monthly nominal and real returns could be calculated for the purpose of comparison. A summary of this output is highlighted below. Source: US Bureau of Labor Statistics, NAREIT, Bloomberg LLC The results show that listed real estate is an excellent hedge for inflation and has historically delivered strong positive nominal and real returns in higher inflationary environments. It also offers a better relative return when compared to general equities. This is especially so when inflation is in the moderate 3-6% range, where listed real estate has historically generated more than double the real return relative to equities. Even with very high inflation (>6% and above), listed real estate continues to outperform equities (albeit at a lower relative level than in a moderate inflation scenario). It's also interesting to note that over the last 50 years, inflation has been above 3% more often than below. When it has been below 3%, listed real estate nominal and real returns have been quite a bit lower than in a moderate inflation environment. And contrary to common belief, in lower inflation settings listed real estate returns actually tend to lag equities.

Concluding thoughts What can we conclude from this analysis? Don't fear inflation. In fact, when investing in real estate, inflation can be your friend. Higher inflation will protect your investment from supply issues (and therefore competition for tenants) and will drive up the replacement cost and residual value of your improvements. We have long argued that for most real estate, the ultimate anchor for value is replacement cost - and rising replacement costs are good for real estate. It is why replacement cost analysis is an important part of our process. What is equally important is that a low inflation environment (<3%) tends to be relatively more favourable for equities (compared to listed real estate). This data cuts against the common narrative that low interest rates, and therefore low inflation, are better for property. |

|

Funds operated by this manager: Quay Global Real Estate Fund |

Insync Monthly Adviser July 2021 Update

2 Sep 2021 - Insync Fund Managers

Insync delivered a strong positive return for the month outperforming the benchmark and maintaining the consistency of outperformance since inception. Whilst monthly, quarterly, or even yearly numbers are too short as useful success...

Read more...

2 Sep 2021 - Insync Monthly Adviser July 2021 Update

By: Insync Fund Managers

Big Tech's success incites a backlash

2 Sep 2021 - Michael Collins, Magellan Asset Management Limited

The critics said the platforms enjoy monopoly powers bestowed by the 'network effect' - when each additional user makes something more valuable for other users. They say these companies were allowed to buy, imitate and crush threats. They...

Read more...

2 Sep 2021 - Big Tech's success incites a backlash

By: Michael Collins, Magellan Asset Management Limited

|

Big Tech's success incites a backlash Michael Collins, Magellan Asset Management Limited August 2021 |

|

Theodore Roosevelt, the 26th US president who was in office from 1901 to 1909, is ranked among the greats.[1] Among achievements, Roosevelt won the Nobel Prize in 1906 for efforts to resolve the Russo-Japanese war and ensured the Panama Canal was built under US control. The Republican protected natural wonders such as the Grand Canyon, welcomed Oklahoma as the 46th state, founded the Department of Commerce and Labor (since split) to oversee the economy and, by expanding the navy, hastened the US's rise as a global power. And he was a 'trust buster'. Roosevelt was president of a feeble state during a 'Gilded Age' when "the power of big business alarmed public opinion because its leaders behaved as if they were above the law", according to one biographer.[2] On assuming office in September 1901 after his predecessor was assassinated, Roosevelt challenged the business czars who sat atop trust structures. In 1902, he used the Sherman Antitrust Act of 1890 to prevent J.P. Morgan-controlled Northern Securities from establishing a western railway monopoly, the first time any president confronted a big company.[3] Northern was soon dissolved after a court battle. Moves followed against other 'bad trusts' such as the Beef Trust, the Sugar Trust and the giant Standard Oil under the control of John D Rockefeller. Such steps are recalled today as people ponder the emergence of powerful technology companies; foremost, Alphabet (owner of Google), Amazon, Apple and Facebook. Many people want to curb the influence of these billion-plus-user-strong 'net states'.[4] The critics said the platforms enjoy monopoly powers bestowed by the 'network effect' - when each additional user makes something more valuable for other users. They say these companies were allowed to buy, imitate and crush threats. They claim the platforms are conflicted because they act as gatekeeper and competitor to rivals such as other online sellers. The overarching complaint is the internet giants have too much influence in a Gilded Age they created. They want Big Tech's power reduced, even if that means breaking up these titans. Amid these calls, US President Joe Biden's administration is flexing against Big Tech. House Democrats have introduced six antitrust bills[5] including the Republican-supported Ending Platform Monopolies Act that seeks to ban takeovers and limit conflicts of interest.[6] Biden has appointed tech foes to head regulatory bodies and advise him. Biden named as his special assistant for competition policy Tim Wu, a law professor who has called for the dismantling of Facebook and who blames monopoly power for the rise of fascism in the 1930s.[7] He chose Jonathan Kanter, designer of the EU's antitrust case against Google, to run the Justice Department's Antitrust Division. He selected Lina Khan, an academic famous for highlighting Amazon's conflicts of interest, to head competition watchdog, the Federal Trade Commission. Already under Khan, the FTC has rescinded a 2015 policy that limited its enforcement abilities[8] and approved procedural changes to capitalise on a 1975 statute that lets it write tougher regulations.[9] Another sign of Biden's resolve is a far-reaching executive order on July 9 to promote competition across the US economy.[10] The antitrust push comes after decades when the antitrust focus was based on the tangible goal of protecting consumers. This meant preventing price gouging. Free services such as Facebook and Google are insulated from the charge of rigging prices; so too is Amazon that is celebrated for lowering prices. For Biden's efforts to succeed Roosevelt-style, regulators need to reframe the antitrust focus to the intangible goal it had in Roosevelt's day. Back then, regulators sought to curb the political and economic power flowing from market dominance, even though economies of scale were allowing these titans to reduce prices for consumers. Even without much of a pivot, Biden's actions will likely help consumers. The 'right to repair' is being enforced, which means tech companies will need to make models that can be repaired and supply relevant parts. Amazon in July gave complainants the right to take court action against the company, a move that exposes the e-retailer to liability.[11] Regulators will impose fines on platforms for even minor competition breaches and target conflicts of interest. Amazon could be forced to shed AmazonBasics that sells Amazon-branded goods and might be forced to allow rival sellers to offer wares at lower prices on other sites. Ditto for Google when promoting search results that benefit the Alphabet group. Apple faces scrutiny about pre-installed apps for Apple services on iPhones. Regulators will take a harsher view of takeovers, especially by Big Tech. Government antitrust action in June that prompted Aon to abandon its US$30 billion takeover of rival insurer Willis Towers Watson showed the higher hurdle for takeovers.[12] But even if antitrust swivels to focus on intangible threats to society, much won't change. Breaking up companies is hard because liberal democracies enshrine property rights by limiting government power. Big Tech will thus use the courts as a shield against the antitrust push. These companies have the resources to prolong and win court action. Legal moves by Amazon and Facebook in June to force Khan to recuse herself from FTC decisions revealed Tech's resolve to protect gains.[13] The FTC's failure in a federal court in June to prove Facebook is a monopoly shows how hard the legal battle will be to win. That follows a unanimous ruling of the Supreme Court in April that stripped the FTC of its long-used power to seek restitution from businesses guilty of abusive practices.[14] Away from the legal system, a polarised Congress won't toughen antitrust laws too much when unravelling the network effect would result in outsized damage to popular tech services offered free by companies. Big Tech might be crimped here and there but the internet giants will remain as dominant as ever; perhaps even too powerful for society's good. To be sure, the internet giants reject accusations they are 'robber barons', claiming they have succeeded through ingenuity and effort, not by rigging markets. The antitrust pursuit precedes Biden by years - the FTC action that seeks to reverse Facebook's purchases of Instagram and WhatsApp, for instance, began under the administration of Donald Trump.[15] The issue of monopoly or oligopoly power extends beyond tech.[16] Even the internet giants deserve protection from capricious politicians - Trump's attempt to block AT&T's takeover of Time Warner in 2018 was seen as politically motivated.[17] Truth be told, Western politicians and regulators are flummoxed on how to regulate such complex creations as platforms. While that could result in poorly designed regulation, the more likely result is that authorities refrain from mounting an aggressive tilt against the internet titans that would be hard to beat in court anyway. The upshot is that the tech superstars are likely to retain, if not extend, their dominance in coming years. Their critics will keep longing for another Roosevelt for a while yet. Unwinding the Chicago twist John Sherman (1823 to 1900) was a Republican senator from Ohio who gave his name to the act that is regarded as the foundation of attempts to regulate competition. At its core, the act, which Sherman described as "a bill of rights, a charter of liberty"[18] made it illegal for competitors to collude on prices, to divide markets, and outlawed monopolies if they relied on unfair competition.[19] The act's significance was to consider the interests of workers, smaller competitors and wider society over the long term. US Congress soon passed two more laws to strengthen the Sherman Act. As trusts were dismantled and companies formed, the Clayton Act of 1914 was designed to block mergers and takeovers that would have cemented control over prices. The other was the Federal Trade Commission Act of 1914 that created an agency to scrutinise businesses. The intent of these three acts and subsequent amendments[20] spread to US states and other countries such that it forms the basis of government control over business around the world today. In the US, the efforts to police competition peaked in the 1950s and 1960s. After World War II, Congress and the Supreme Court introduced and enforced antitrust measures that protected smaller businesses against larger ones by cracking down on predatory pricing, looked askance at 'vertical integration' and consistently considered social and political issues, not just economic ones. The focus, however, changed from the 1970s when University of Chicago professors (dubbed the Chicago School) argued that antitrust laws should focus only on what mattered to consumers; namely, prices, output and efficiency. The Chicago School argued that firms survived only if they pleased consumers so there was no need for the government to protect firms from more dominant competitors or take a wider view of their influence in society. The Chicago view was encapsulated in the paradox named after Yale professor Robert Bork who said in his book of 1978 The antitrust paradox that efforts to protect consumers only lead to higher prices by protecting inefficient firms.[21] The Bork paradox, which essentially said government regulation of competition did more harm than good, took hold and antitrust enforcement largely lapsed during the 1980s and has been patchy since.[22] As the rise of the digital platforms revived interest in antitrust efforts, Amazon became the prime antitrust focus because a company that started selling books online in 1995 now has interests that extend beyond ecommerce to advertising, artificial intelligence assistants, book publishing, bookstores, cloud services, delivery, electronics, express post, entertainment, gaming, groceries, logistics, money lending, music, publishing, streaming, videos and warehousing. This issue is not just Amazon's power within an industry but the company's influence across the economy and society. Khan, when at Yale University in 2017, wrote perhaps the most influential paper that has argued that today's narrow approach to antitrust allows Amazon's unfettered rise to the detriment of wider consumer welfare. In Amazon's antitrust paradox Khan said measuring Amazon's dominance on short-term benefits to consumers misses the potential longer-term harm to market structures and competition and underappreciates the risk of predatory pricing. Khan said the narrow antitrust focus misjudges how integration across distinct business lines may prove anticompetitive because the platforms serve as infrastructure for rivals and the economics of platforms promotes growth over profits. Thus predatory pricing is rational, she said, when today's narrow antitrust doctrine treats it as irrational and implausible. Another consequence is that platforms can exploit information collected on companies using their services to undermine them as rivals.[23] Her solution was to restore the traditional broader antitrust and competition policy principles or apply common carrier obligations and duties on the platforms, proposals Khan and others of her ilk now have the regulatory power to pursue. Flawed solutions In 2012, Facebook paid US$1 billion for Instagram when the photo-sharing app employed just 13 people, had only 30 million users and earned no revenue.[24] The US regulator voted 5-0 to allow the deal[25] while the UK supervisor approved the purchase because Instagram was in no position to compete against Facebook "as a potential social network or as a provider of advertising space".[26] Regulators missed that Facebook was buying a rival that might divert people from its platform, the same motive that prompted Facebook in 2013 to bid unsuccessfully for Snapchat[27] and in 2014 to buy WhatsApp for US$19 billion with regulatory approval.[28] Alphabet, Amazon, Apple and Facebook, by the count of The Washington Post owned by Amazon's Jeff Bezos, have bought at least 607 companies in their rise to monopolistic or oligopolistic control over their tech spheres that have become central to daily life.[29] Suggestions for curbing Big Tech are plentiful. Their implementation, however, often looks problematic. Some have argued, for instance, that Amazon should be subject to common carrier obligations (ensure other businesses have equal and fair access to the platform) to curb its power in retail and be prevented from favouring its products. But why would Amazon be treated like a utility when it only accounted for just below 5% of US retail sales in 2020, hardly monopoly control? Why would online and offline competitors be able to favour their products and not Amazon? For those who suggest that the platforms be regulated like utilities, many propose the 'regulated asset base' model of oversight. Under this model, utilities earn a return akin to what they would earn competing against an imaginary competitor that was meeting its cost of capital. Valuing the intellectual capital of the platforms would be just one hurdle.[30] Others propose that users own their behavioural data, connections or search history. But apathy might prevent much changing. Stronger privacy laws would dim Big Tech's sway but this would inhibit innovation. Some say Facebook should be made interoperable - when data can be shared with other sites - akin to how AOL was forced to make its Instant Messenger interoperable in 2001.[31] Would people bother switching? Others suggest that Facebook be forced to become a subscription service.[32] But politicians might baulk at making users pay for something a company is offering at no charge. Another solution is tougher regulations on how algorithms target and sort information and people and steep penalties for their misuse.[33] A more-radical proposal would be for governments to set up publicly owned platforms to compete against the established privately owned platforms. But no one in the US is serious about this path. Another radical proposal is to dismantle the platforms. But that would diminish the network effect for users, nullify economies of scale, Amazon A might eventually dominate Amazon B, C, D and E anyway, and such a path presages years of court battles with no guarantee of success for antitrust forces. Perhaps pertinent for those intent on breaking up Big Platforms are the unintended consequences of Roosevelt's successful battle to dissolve Rockefeller's Standard Oil. In 1911, Rockefeller was playing golf when he was given the news the Supreme Court had ordered Standard Oil to be split into 34 companies. He asked his golf partner, a Catholic priest, if he had any money. The priest said no and asked why. "Buy Standard Oil," was Rockefeller's response. It was sound advice for, in one biographer's view, "it was the luckiest stroke of his career". Only three years after Henry Ford produced his first Ford Model T, Rockefeller now owned about 25% in 34 oil companies that soared in value when investors could glimpse the assets in listed companies that had previously been largely privately held.[34] And didn't Roosevelt know he had made Rockefeller the world's richest person. In 1912, Roosevelt re-entered presidential politics by creating the Bull Moose party. At one stop during his failed campaign, Roosevelt roared: "Rockefeller and his associates have actually seen their fortunes doubled. No wonder that Wall Street's prayer now is: Oh Merciful Providence, give us another dissolution."[35] [1] Roosevelt has come fourth in the past four C-SPAN surveys of historians where they rank the US presidents. The past four surveys were conducted in 2021, 2017, 2009 and 2000. In the past three, Abraham Lincoln came first, George Washington second and Franklin D. Roosevelt third. c-span.org/presidentsurvey2021/?page=overall [2] Kathleen Dalton. 'Theodore Roosevelt. A strenuous life.' Vintage Books. 2002. Page 204. [3] Dalton. Op cit. Pages 224 to 226. [4] WIRED. 'Net states rule the world; we need to recognise their power.' Alexis Wichowski from Columbia University's School of International and Public Affairs. 4 November 2017. wired.com/story/net-states-rule-the-world-we-need-to-recognize-their-power/ [5] House Committee of the Judiciary. 'Markups'. 23 June 2021. The six bills are H.R. 3843, the Merger Filing Fee Modernization Act of 2021; H.R. 3460, the State Antitrust Enforcement Venue Act of 2021; H.R. 3849, the Augmenting Compatibility and Competition by Enabling Service Switching Act of 2021 or the ACCESS Act of 2021; H.R. 3826, the Platform Competition and Opportunity Act of 2021; H.R. 3816, the American Choice and Innovation Online Act; and H.R. 3825, the Ending Platform Monopolies Act. judiciary.house.gov/calendar/eventsingle.aspx [6] House of Representatives. 'H.R. 3825 - Ending Platform Monopolies Act.' Entered 11 June 2021. congress.gov/bill/117th-congress/house-bill/3825/text. See release by Congressman Lance Gooden, who introduced the bill. 'Congressman Gooden introduces the Ending Platform Monopolies Act.' 11 June 2021. gooden.house.gov/media/press-releases/congressman-gooden-introduces-ending-platform-monopolies-act [7] Tim Wu. 'Be afraid of economic 'bigness'. Be very afraid.' 10 November 2018. The New York Times. nytimes.com/2018/11/10/opinion/sunday/fascism-economy-monopoly.html. See also, 'Tim Wu explains why he thinks Facebook should be broken up.' WIRED. 5 July 2019. wired.com/story/tim-wu-explains-why-facebook-broken-up/ [8] Federal Trade Commission. 'FTC rescinds 2015 policy that limited its enforcement ability under the FTC act.' 1 July 2021. ftc.gov/news-events/press-releases/2021/07/ftc-rescinds-2015-policy-limited-its-enforcement-ability-under [9] Federal Trade Commission. 'FTC votes to update rulemaking procedures sets stage for stronger deterrence of corporate misconduct.' 1 July 2021. ftc.gov/news-events/press-releases/2021/07/ftc-votes-update-rulemaking-procedures-sets-stage-stronger [10] The White House. 'Fact sheet: Executive order on promoting competition in the American economy.' 9 July 2021. whitehouse.gov/briefing-room/statements-releases/2021/07/09/fact-sheet-executive-order-on-promoting-competition-in-the-american-economy/ [11] See "Amazon ends use of arbitration for customer disputes.' 22 July 2021. nytimes.com/2021/07/22/business/amazon-arbitration-customer-disputes.html [12] See US Department of Justice Antitrust Divisions 'Complaint' filed against Aon and Willis Towers Watson. Filed to the US District Court for the District of Columbia. 16 June 2021. justice.gov/opa/press-release/file/1404951/download. The EU had approved the takeover. Berkshire Hathaway, fearing FTC pushback, in May/June abandoned the purchase of pipeline assets from Dominion Energy. See 'Wall Street and Warren Buffett miss the good old days.' 27 July 2021. Bloomberg News. bloomberg.com/opinion/articles/2021-07-26/wall-street-and-warren-buffett-miss-the-good-old-days [13] 'Amazon seeks recusal of FTC chair Khan, a longtime company critic.' 30 June 2021. The Washington Post. The newspaper is owned by Amazon founder Jeff Bezos. washingtonpost.com/technology/2021/06/30/amazon-khan-ftc-recusal/. 'Facebook seeks recusal of FTC chair Lina Khan amid high-profile antitrust case.' 14 June 2021. The Washington Post. washingtonpost.com/technology/2021/07/14/facebook-seeks-recusal-ftc-chair-lina-khan/ [14] Supreme Court of the US. Ruling. 'AMG Capital Management, LLC et all v Federal Trade Commission.' 22 April 2021. supremecourt.gov/opinions/20pdf/19-508_l6gn.pdf. See also, Mike Davis, founder Article III Project. 'Congress must empower the FTC to fight tech's abuses.' Newsweek. 29 July 2021. newsweek.com/congress-must-empower-ftc-fight-big-techs-abuses-opinion-1614105 [15] See Axios. 'Judge dismisses FTC's antitrust complaint against Facebook.' 28 June 2021. axios.com/judge-dismisses-ftcs-antitrust-complaint-against-facebook-b4612f7a-2f82-4462-91d3-36612c56416e.html. See also Federal Trade Commission. 'FTC sues Facebook for illegal monopolisation.' 9 December 2020. ftc.gov/news-events/press-releases/2020/12/ftc-sues-facebook-illegal-monopolization. More than 40 state attorneys were involved in the case. [16] Some parts of tech seem safe from antitrust efforts. See WIRED. 'Biden's antitrust revolution overlooks AI - at Americans' peril.' 27 July 2021. wired.com/story/opinion-bidens-antitrust-revolution-overlooks-ai-at-americans-peril/ [17] The allegation is that Trump ordered Gary Cohn, then the director of the National Economic Council, to pressure the Justice Department to block AT&T's takeover of Time Warner (now known as Warner Media) out of spite of CNN. The allegation was made by Jane Mayer in 'The making of the Fox News White House'. The New Yorker. 4 March 2019. newyorker.com/magazine/2019/03/11/the-making-of-the-fox-news-white-house [18] Senator John Sherman speaking in the US Senate. Congressional Record. Senate 1890. Page 2,461. appliedantitrust.com/02_early_foundations/3_sherman_act/cong_rec/21_cong_rec_2455_2474.pdf [19] US Federal Trade Commission. 'FTC fact sheet: Antitrust laws: A brief history." Undated. consumer.ftc.gov/sites/default/files/games/off-site/youarehere/pages/pdf/FTC-Competition_Antitrust-Laws.pdf. Federal Trade Commission. 'The antitrust laws.' ftc.gov/tips-advice/competition-guidance/guide-antitrust-laws/antitrust-laws [20] The Robinson-Patman Act of 1936 amended the Clayton Act to ban certain discriminatory prices, services, and allowances in dealings between merchants. The Clayton Act was amended again in 1976 by the Hart-Scott-Rodino Antitrust Improvements Act to require companies planning large mergers or acquisitions to notify the government of their plans in advance. See the Federal Trade Commission 'The antitrust laws.' ftc.gov/tips-advice/competition-guidance/guide-antitrust-laws/antitrust-laws [21] See Robert Bork. 'The antitrust paradox. A policy at war with itself.' The Free Press. 1978. The introduction, chapter 1 and epilogue can be found at: amazon.com/Antitrust-Paradox-Robert-H-Bork/dp/0029044561 [22] See Maurice E. Stucke and Ariel Ezrachi. 'The rise, fall, and rebirth of the US antitrust movement.' Harvard Business Review. 15 December 2017. hbr.org/2017/12/the-rise-fall-and-rebirth-of-the-u-s-antitrust-movement [23] Lina M. Khan. 'Amazon's antitrust paradox.' The Yale Law Journal. Volume 126 2016-2017. Number 3. January 2017. yalelawjournal.org/note/amazons-antitrust-paradox [24] UK Office of Fair Trading. Release. 'Anticipated acquisition by Facebook Inc of Instagram Inc.' 14 August 2012. webarchive.nationalarchives.gov.uk/20140402232639/http://www.oft.gov.uk/shared_oft/mergers_ea02/2012/facebook.pdf [25] Federal Trade Commission. 'FTC closes its investigation into Facebook's proposed acquisition of Instagram photo-sharing program.' 22 August 2012. ftc.gov/news-events/press-releases/2012/08/ftc-closes-its-investigation-facebooks-proposed-acquisition [26] UK Office of Fair Trading. Op cit. [27] The Wall Street Journal. 'Messaging service Snapchat spurned $3 billion Facebook bid.' 13 November 2013. wsj.com/articles/messaging-service-snapchat-spurned-facebook-bid-1384376628 [28] See Federal Trade Commission. Release. 'FTC notifies Facebook, WhatsApp of privacy obligations in light of proposed acquisition.' 10 April 2014. ftc.gov/news-events/press-releases/2014/04/ftc-notifies-facebook-whatsapp-privacy-obligations-light-proposed. See European Commission. Press release. 'Mergers: Commission approves acquisition of WhatsApp by Facebook.' 3 October 2014. europa.eu/rapid/press-release_IP-14-1088_en.htm [29] The Washington Post. 'How Big Tech got so big. Hundreds of acquisitions.' 21 April 2021. washingtonpost.com/technology/interactive/2021/amazon-apple-facebook-google-acquisitions/ [30] See The Economist. Schumpeter. 'What if large tech firms were regulated like sewage companies?' 23 September 2017. economist.com/business/2017/09/23/what-if-large-tech-firms-were-regulated-like-sewage-companies [31] Mark Stoller. Fellow at the Open Markets Institute. Tweet. 'We know one way to regulate Facebook. DOJ forced AOL messenger interoperability in 2001. It worked.' 6 October 2017. twitter.com/matthewstoller/status/916316360807985153 [32] Roger McNamee, managing director of Elevation Partners. 'How to fix Facebook: Make users pay for it.' 21 February 2018. washingtonpost.com/opinions/how-to-fix-facebook-make-users-pay-for-it/2018/02/20/a22d04d6-165f-11e8-b681-2d4d462a1921_story.html [33] See Martin Sandbu. Financial Times. 'Free Lunch' columnist. 'Civilising the digital economy. Ownership rights and algorithmic accountability.' 24 February 2018. ft.com/content/a245e882-1882-11e8-9e9c-25c814761640 [34] 'Titan. The life of John D Rockefeller Sr.' Ron Chernow. Warner Books. 1998. Page 545. By one count the largest federal antitrust suit of the day against the biggest empire of the day, it entailed 444 witnesses who delivered 11 million words of testimony. Add on 1,374 exhibits, and the proceedings filled 12,000 pages in 21 volumes. On top of that were another 21 state antitrust suits. [35] Chernow. Op cit. Pages 556 and 557. Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. A copy of the relevant PDS relating to a Magellan financial product or service may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to be implemented and its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund |

New Funds on Fundmonitors.com

2 Sep 2021 - Australian Fund Monitors

Here are some of the latest additions to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research,...

Read more...

2 Sep 2021 - New Funds on Fundmonitors.com

By: Australian Fund Monitors

|

New Funds on Fundmonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

||||||||||||||||||||||||

|

||||||||||||||||||||||||

|

||||||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||

|

||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||

|

||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||

|

||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||

|

||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||

|

||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||

|

||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||||

|

Subscribe for full access to these funds and over 600 others |

||||||||||||||||||||||||