NEWS

1 Apr 2022 - Semiconductors - transforming our lives

|

Semiconductors - transforming our lives Alphinity Investment Management 21 March 2022 That's not a peak……I still remember the time I thought I'd hit "peak technology". I had a new Nokia 3310 in my hand and after making a call and sending an SMS I found a game called Snake that helped to pass time in the cab while the driver fumbled through a UBD street directory to try and find my hotel. I was also carrying a new digital camera to document my trip and an MP3 player with music I'd burned from my existing CD's. And when I hit my destination all I needed to find was a telephone port to be able to connect back to the work files I needed to finish a presentation for the morning. What a time to be alive….…

It would have been impossible at that time for me to envisage what life would look like 20 years later. The phone I use is now a phone, internet, camera, music and TV device all in one, with the capability to run my entire life off a 6 inch by 3 inch screen. That cab I was in? Well now the guidance systems mean never pulling into a McDonalds to work out directions ever again, let alone the incredible advances in safety features and entertainment. Then we stand at the front edge of the electric vehicle migration while peering at autonomous driving looming on the horizon. Those files I need? Well now I can access them from anywhere and on any device as data migrates to the cloud. The changes to the way we live, and work have been astonishing and are accelerating.

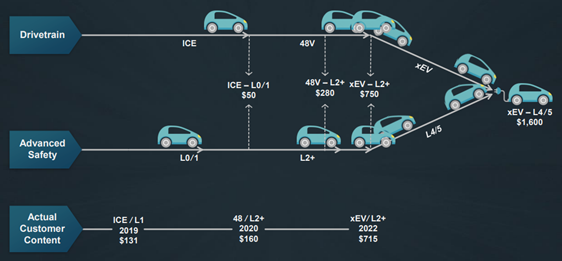

While it is almost impossible to imagine what the next 20 years may look like, one thing we do know is that as technology marches ever forward, so does the required intensity of computing power. It is quite a leap from having a "snake" made of clunky pixels moving on a basic screen to cars that need to observe and assess all factors around them then calculate and execute the best course of action in fractions of a second. Let alone what other currently unimaginable technology extensions will emerge. Imagination and semiconductors - driving technological advancementUnderpinning this march in computational advancement have been semiconductors. It is advances in semiconductor technology that facilitates this rapid escalation in compute power while also keeping a restraint on device size. And it isn't just the complexity of the compute but the expansion in use cases that underpins the importance of semiconductors in the technology supply chain. Taking auto as an example, not only are the semis more advanced, but they have proliferated into almost every element of the car, from power to entertainment to guidance systems. The semiconductor company ONSemi estimate the content value of semis has lifted from $50 for an internal combustion engine with no advanced driver assist systems, to a future state of $1,600 for an electric vehicle approaching full autonomy.

Source: ONSemi Investor Day (Aug 21) This expansion of content value is occurring across a range of industries. From cars to phones to datacentres and our homes, content per unit is expected to lift by 50-100% when moving from 2020 to 2025. Smartphones are continually adding more functionality, datacentres are adding capacity to underpin advances such as AI, machine learning and the metaverse while compressing speed, and our homes are moving towards a degree of connectivity for almost every device.

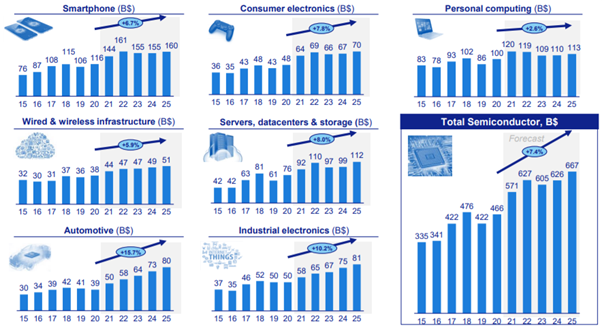

Source: UBS (Jan 22), Applied Materials (April 2021) What does this mean for the semiconductor industry?This acceleration of technological development has driven a step change in semiconductor industry growth rates, with demand rising from a historical growth rate of 3-5% p.a. to an industry forecast to grow at 6-8% p.a. out to 2030, taking total industry revenue beyond $1bn. Where demand used to rise and fall with smartphone and PC demand, there are now much broader demand drivers, with particular areas of strength expected across autos, industrials and datacentres.

Source: ASML Investor Day (Sept 21), Gartner How do we invest in this opportunity?There are many ways to invest along the chain in semiconductors. From the equipment manufacturers (ASML, Lam Research, Applied Materials, ASMI) to the main manufacturers (TSMC, Samsung, Global Foundries, Intel) to the semiconductor companies exposed to different elements of end demand spanning data centre (Nvidia, AMD, Marvell), auto (ONsemi, IFX, Texas Instruments) and memory (Micron, Samsung, Hynix) to name just a few. Each discrete exposure brings with it a nuance to overall semiconductor cyclicality and underlying demand strength. Our goal is to balance end market demand strength, company positions and financial return metrics with a degree of resilience in the face of an ever present (and sometime violent) semiconductor cycle. Among the swathe of opportunities, our preference currently lies with:

Life in 2040?The changes to tech have been stunning in the past 20 years and it is difficult to imagine what the next 20 years will bring. But one thing we do know is that compute will advance, and semiconductors will be the key linchpin in assisting this drive forward. As such the future looks bright and the return profile compelling for those that can carve out a market position exposed to these key tech growth trends. Author: Trent Masters, Global Portfolio Manager This information is for adviser & wholesale investors only |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Sustainable Share Fund |

31 Mar 2022 - The headwinds facing Autosports Group

|

The headwinds facing Autosports Group Montgomery Investment Management March 2022 To understand the challenges facing the automotive sales industry, it is often helpful to examine a particular company, as Roger Montgomery did earlier this month. Autosports Group (ASX:ASG) operates car sales outlets in Sydney, Melbourne, Brisbane and the Gold Coast. Its share price has been on a rollercoaster ride since floating in 2016 and currently sits below the $2.40 listing price. ASG is profitable and reasonably priced, but investors should be mindful of the threats facing its business model. Established in 2006, Autosports Group owns and operates 40 retail businesses, including 23 luxury and prestige motor vehicle dealerships, two used wholesale motor vehicle dealerships and two specialised collision repair facilities in Sydney, Brisbane, the Gold Coast and Melbourne. Autosports Group represents Original Equipment Manufacturer (OEM) brands including Alpina, Aston Martin, Audi, Bentley, BMW, Jaguar, Lamborghini, Land Rover, Maserati, McLaren Mercedes Benz, Mini, Rolls-Royce, Volkswagen and Volvo. ASG offers new and used vehicles, finance and insurance, and back-end parts and servicing, including collision repair. Currently, car dealers are operating amid a veritable storm. Deliveries of new vehicles are hampered by a semiconductor chip shortage and the shuttering of manufacturing facilities due to COVID-19 associated isolation requirements. Booming demand for vehicles however is undiminished, thanks to consumers unable to travel, and flush with cash (e.g., a booming construction sector lining the pockets of builders and tradies). The eroded appeal of public transport is also driving demand for private transport. Unable to purchase a new car, buyers have turned to the used market where prices for many used vehicles have risen beyond their original purchase price of several years ago. The agency threat Meanwhile, in the background, the ever-present threat of OEMs moving to an Agency Model (Mercedes AG have already announced the change and are in court with dealers fighting for $650 million compensation) poses a revenue hazard to dealership revenues, putting investors on edge. Under the current dealership model, a brand retailer buys a vehicle from the OEM as inventory at a wholesale price. Typically the vehicle is only paid for by the dealer when it is sold. A margin for the dealer to cover costs is added and the salesperson then negotiates a transaction price with a customer. OEMs including Mercedes and Honda have expressed frustration with the traditional dealership/OEM relationship because dealer promotions including special offers, run-out deals, discounts and end-of-the-month sales all lower resale values and accelerates depreciation rates. But it hasn't all been the dealers' fault. Dealers note they have had to pay for manufacturer 'mistakes', overproduction on their floor plan charges, incorrect build combinations and obsolescence. This is the reason for the "race to the bottom" on new-vehicle margins. Under the Agency Model, dealers are paid a fee for a vehicle sale. For Honda dealers in NZ, this ranges from four per cent to seven per cent depending on meeting sales targets and customer satisfaction scores. Elsewhere, the customer places their order directly with the OEM and nominates a preferred delivery dealer. The price and dealership mark-up or commission is set by the OEM. The positive spin put on the agency model by OEMs says dealers aren't limited to selling just the cars allocated to them. They are free to sell any vehicle model in the brand's stable on order nationally. Dealers have access with access to the full range without incurring floorplan costs. The OEM owns all demonstration stock at the dealerships and all the new-car stock. New vehicles are held for sale at a national distribution centre and sales are made directly to the customer. The dealer therefore no longer finances an inventory of vehicles for sale, and all floorplan or finance costs are borne by the OEM. In Volkswagen's electric vehicle agency model in Europe, the dealer is offered a lease program for demos and loan vehicles. Across the globe, the use of agency models is more widespread. Mercedes-Benz has already introduced agency models in South Africa, Austria, Sweden and it will transition to one in Germany as well. Volkswagen is rolling it out for selling electric vehicles in Europe and Honda has been running the model in NZ since 2000. Back to ASG Navigating this tumult is a challenge attested to by a 30 per cent decline in ASG's share price since its high of $2.74 last June. Autosports Group reported its first half FY22 results recently noting the solid margins of the previous financial year continued, driving profit before tax to beat some estimates by more than 10 per cent. The company however reported revenue of A$911 million, which grew 0.8 per cent year-on-year (yoy) but missed consensus estimates for $1 billion. Revenue was down four per cent when adjusted for acquisitions, which contributed $44 million. EBITDA grew 27 per cent yoy to $48.6 million, beating some estimates by 10 per cent. Adjusted profit before tax of $39.2 million was up 35 per cent on the previous corresponding period and beat consensus estimates for $33.8 million by 16 per cent. Revenue for the sale of new vehicles was unchanged on the same period a year ago at $564 million, thanks to an inability to obtain sufficient stock. A combination of strong demand, and that inability to deliver new cars, has also resulted in the company's new vehicle order book doubling from a year ago. New orders written in the first half exceeded deliveries by 22 per cent. Over in the used car department, vehicle revenue of $209 million was also flat yoy but strong growth in the final quarter of the calendar year was implied by the fact the first quarter was down 12 per cent yoy due to lockdowns. The services department generated $59 million in revenue, which was nine per cent higher than the previous corresponding period and parts generated $60 million of revenue up 13 per cent yoy. The growth in profit, which exceeded revenue growth, was the result of higher selling prices (on less stock) and therefore improved margins. Gross margins of 19.2 per cent was an improvement on the 17.8 per cent generated in in the second half of FY21. The company's outlook remains clouded by a comprehensive lack of clarity about when deliveries will return to normal. Supply constraints are expected to last the remainder of the calendar year at least. Demand should therefore continue to exceed supply. The Used vehicle, Service and Parts divisions are expected to generate revenue growth of between six and ten per cent. Longer term the business model remains under the cloud of threats from OEMs moving to an agency selling model. Author: Roger Montgomery, Chairman and Chief Investment Officer Funds operated by this manager: Montgomery (Private) Fund, Montgomery Small Companies Fund, The Montgomery Fund |

30 Mar 2022 - Performance Report: Argonaut Natural Resources Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | At times, ANRF may consider holding higher levels of cash (max 30%) if valuations are full and it is difficult to find attractive investment opportunities. The Fund does not borrow for investment or any other purposes, but it may short sell securities as part of its portfolio protection strategies. |

| Manager Comments | The Argonaut Natural Resources Fund has a track record of 2 years and 2 months and therefore comparison over all market conditions and against its peers is limited. However, the fund has outperformed the ASX 200 Total Return Index since inception in January 2020, providing investors with an annualised return of 56.23% compared with the index's return of 6.11% over the same period. On a calendar year basis, the fund hasn't experienced any negative annual returns in the 2 years and 2 months since its inception. Over the past 12 months, the fund's largest drawdown was -3.38% vs the index's -6.35%, and since inception in January 2020 the fund's largest drawdown was -14.61% vs the index's maximum drawdown over the same period of -26.75%. The fund's maximum drawdown began in February 2020 and lasted 3 months, reaching its lowest point during March 2020. The fund had completely recovered its losses by May 2020. The Manager has delivered these returns with 1.25% more volatility than the index, contributing to a Sharpe ratio for performance over the past 12 months of 3.07 and for performance since inception of 2.28. The fund has provided positive monthly returns 79% of the time in rising markets and 57% of the time during periods of market decline, contributing to an up-capture ratio since inception of 195% and a down-capture ratio of -16%. |

| More Information |

30 Mar 2022 - A tumultuous start to '22!

|

A tumultuous start to '22! Insync Fund Managers March 2022

Economy-wide events dominate the headlines Big inital swings are a typical reaction to a change in the macro-economic outlook and are not cause for us to react. This movement was primarily driven by the largest swing towards value stocks in over 20 years. As at the end of February, the 'value' style category fell -2.8% CYTD with 'growth' styles falling -12.5%, according to JP Morgan. The lesser known 'quality' style category where Insync resides is neither value nor growth, although we tend to hold stocks the market categorises as Growth. 2022 marked the 5th worst start for S&P 500 since 1927. Inflation fears have the market pricing in 5-6 interest rate rises this year, precipitating the heavy swing initially, with Ukraine's invasion by Russia creating price spikes in both energy and commodity prices as well. Markets hate uncertainty. It's no surprise then that material and energy stocks were the best performers in February (Insync has zero exposure to these sectors due to their low ROICs through the cycle). It's highly probable that the negative macro factors will slow economic growth. This in turn, will then favour a move back to profitable growth companies (rather than growth stocks overall). These are the type of stocks we hold. Thus, we liken the current portfolio to a coiled spring. When investors soon refocus on company fundamentals, the share price performance of quality businesses then rebound quickly and sharply. This usually 'surprises' commentators and investors alike. Earnings growth across the portfolio continues to compound strongly despite macro shifts, with valuations becoming more attractive.

Governance factors are why Russia and its peers don't appear with Insync Russia's invasion of Ukraine is one of the greatest tragedies of our lifetime. We have no direct exposure to Russian equities and virtually zero indirect exposure. The simple reason is that Russia is a Kleptocracy run by a ruler who has used his poitical power to systematically steal billions of dollars of its national treasure owned by its people. When there is no rule of law - and therefore no shareholder rights - valuations do not matter. The risk of near total loss of capital is too high. Companies with strong governance nearly always do the right thing and also deploy capital wisely.

Why we are confident that sustainable growth companies are poised to perform strongly Almost every big slowdown in the past has been preceded by a rise in energy prices and Federal Reserve rate hikes.Going forward then, markets will likely start shifting focus to the prospect of weaker economic growth and refocus on investing in businesses with durable, sustainable earnings growth and profitability. This economic backdrop propels precisely the kind of stocks we hold. Overlaid with identified megatrends, it enables these companies to thrive irrespective of higher rates or slower growth. Meantime, in the near term expect ongoing volatility in markets and most equity funds as well including our own.

We have often discussed the difficulty and danger of market timing. The probability of getting it right more often than wrong is extremely low. Right now, investor sentiment is very bearish with the AAII investor sentiment survey at its lowest point since April 2020. Fund managers overall reflect this view, holding the highest level of cash since the covid lows and at the bottom of the GFC.

This is why we remain fully invested when markets swing wildly as one would expect in these moments of macro-economic uncertainty. For good reason we didn't react in previous occasions such as now, and we won't in future ones either. This is also why we remain fully invested unlike many of our peers. Should timing be desired in the hope of avoiding the dips and riding the peaks, then we believe this is a decision for the investor and their adviser. We continue with our usual rifle-like approach of investing in the most profitable companies with a long runway of growth fuelled by megatrends. We refrain from trying to time these shifts, as this lowers risks and, longer term, aids returns. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund |

30 Mar 2022 - Do Multiples Matter?

|

Do Multiples Matter? Equitable Investors March 2022

Do valuation multiples matter? There's broadly two schools of thought - one that purchase price dictates your future return and the other that good companies will deliver growth in time to drive value higher, whatever the current price is. Buying a stock on low multiples is no guarantee of either future multiple expansion or earnings growth. Outside times of panic you can expect there is some logic driving the sellers of those low multiple stocks. But an excessive price today can burden a company with implied growth expectations that it just can't meet. In a different era, former dot-com darling Sun Microsystems' CEO, Scott McNealy, expressed it well:

Size is an important factor - Sun was "at scale" with >$US10 billion of dollars of annual revenue and its ability to grow into its valuation was limited. A microcap today on 10x revenue that is just beginning to penetrate its market with a competitive advantage may well be able to prove it was a bargain retrospectively. So multiples only mean something with context and analysis. Funds operated by this manager: |

29 Mar 2022 - The central bank dilemma

|

The central bank dilemma Kardinia Capital March 2022 |

|

Jerome Powell's re-election as Federal Reserve chair late last year was a relief to investors, but a few short months later his credibility is now on the line. As economists continue to argue as to whether inflation is transitory or permanent, political parties know full well that inflation is disastrous at the ballot box. The US midterms will be held in November and polling doesn't look good for the Biden administration. While the 2024 full term election is still a while away, inflation is rising. Gasoline price increases are toxic to the US voter and the prices at the pump are already at record levels, recently surpassing the 2008 spike. CPI is almost certainly going to be north of 8-9% year on year over the next few months, which is going to light a fire under the Fed. 12-month percent change in CPI for All Urban Consumers (CPI-U), Inflation is taking off, but the outlook for the global economy remains uncertain. China has just announced a GDP growth target of 5.5% this year, the lowest in more than 30 years. Russian credit has just been downgraded to junk, while global sanctions are already creating material market distortions. Meanwhile, the effects of higher oil prices are rippling across the economy. We believe those prices are here to stay, due largely to geopolitical events and ESG trends. Russia is the world's largest net exporter of oil and gas combined. According to Goldman Sachs, Russia supplies 11% of global oil consumption and 17% of global natural gas consumption (and as much as 40% of Western European consumption). However, the US has banned the import of Russian oil and gas, the UK is phasing out oil imports by the end of 2022, and the EU announced plans to cut imports of Russian gas by two thirds within a year. The world needs to replace this supply, but OPEC has already announced that it has no plans to increase production in response to the Russia/Ukraine war. US trade envoys have been dispatched to Venezuela, with suggestions that a Saudi Arabian trip is in the planning. Of course, the US has the potential to bridge some of the shortfall by ramping up its own unconventional production; however, that appears unlikely given the US administration was elected on a clean energy platform. Energy supply was already under pressure from ESG trends. In 2020, BP announced a plan to cut oil and gas production by 40% over 10 years and pivot towards renewables. Last year, Shell announced that its oil production had peaked and would fall 1-2% per annum as it targeted net zero emissions by 2050. This supply shortfall is occurring just as energy demand is returning after the COVID-induced lockdowns of the past two years. There is no easy solution. We do not believe there will be a quick end to the Russia/Ukraine conflict, meaning energy and commodities prices will remain elevated. The resources and energy sectors should generate attractive returns in 2022, with Australia in the box seat to outperform the rest of the world given its stable, resource rich environment. It's also worthwhile watching the credit and debt markets, which are so deep and more liquid that equity markets (and often equity investors) overlook the signals these markets provide. The 2yr/10yr year US yield curve is flattening, with credit markets signalling that investors are losing confidence in the economy's growth outlook. Often it can be difficult to predict the trigger for an economic downturn, but in this case it could be the Fed raising the federal funds rate itself that causes a downturn. |

|

Funds operated by this manager: Bennelong Kardinia Absolute Return Fund |

|

The content contained in this article represents the opinions of the author/s. The author/s may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the author/s to express their personal views on investing and for the entertainment of the reader. |

29 Mar 2022 - Portfolio positioning in a time of uncertainty

|

Portfolio positioning in a time of uncertainty Loftus Peak 21 March 2022

War in Europe. Unthinkable one month ago. War in Ukraine The unprovoked conflict in Ukraine has unleashed a human tidal wave of misery, dislocation and death, the scale of which has not been seen since World War II. A columnist for the New York Times referred to the war as "the most dangerous confrontation for the world since the Cuban missile crisis (of 1962)." Just one month ago, we wrote of the onset of higher interest rates and inflation as major factors influencing markets, having considered but not believing that Putin would be so irrational as to start a war. This is not the correct forum to deal with the human and geopolitical consequences of this, so we won't. But it is appropriate to ask: How will the war in Europe affect investors globally? The broadest economic sanctions ever enacted have resulted in the collapse of the ruble (by 50%), the delisting of Sberbank (one of Russia's largest) on some European exchanges, and a well-advanced movement by some countries to source oil and gas from places other than Russia.

Lines in Russia at ATM's for Sberbank. This is forcing up the price of energy, at the pump and the meter, which will likely drive inflation even higher than its current levels, spurring the US Federal Reserve to continue its tightening policy. But the Fed will also consider the possibility that higher energy costs could suppress demand, thus reducing the need for more serious interest rate rises - an unscripted but possible outcome. Separately, we are of the view that now that Russia is considered an unreliable energy partner for the Europeans, the impetus to de-carbonisation will accelerate. Portfolio positioning We do not know how this will end, but last month we wrote highlighting the quality of the portfolio. "Irrespective of macroeconomic conditions, this (quality) has always been an integral part of the portfolio construction process, and was a decision informed by the numerous corrections and crashes witnessed by the investment team over their lifetimes. Despite the short-term volatility and underperformance of a select few names, we believe the Fund is well positioned for a period marked by slowing economic growth and rising costs of capital because of the inherent characteristics of the big disruptive companies, which are amongst the strongest in the world. Further, earnings growth in the majority of the Fund's holdings continues to be strong, adding to the conviction we have in the long-term secular trends to which we are exposing our clients. Although the short term might remain volatile and uncertain, we believe that over the medium and long term the safest place to be is in quality companies riding secular tailwinds. Disruption no longer implies excess risk During the early days of disruption, between 1995 and 2005, there was considerable investment risk as typically the mechanism was via start-up companies, which mostly were light-on for profits, let alone cashflows and balance sheets. It was by no means clear, for example, that classified advertising would migrate on-line, that cars would go electric, movies would be shown on mobile phones or that taxi services would be replaced by Uber and the like. Investors who bought before the bursting of the 2000 bubble did not do well… for a while. But those that understood what Apple, Amazon and Google were doing on the global stage - and that part is very important - made simply stellar returns. Fast forward to today. The word disruption, for reasons related to its investment history as well as its more general meaning, still has a negative connotation. It is not unfair to prefer the safety of an 'undisrupted' world to the uncertainty that disruption implies. But it is time to move on. Some of those early-stage disruptive companies are listed in the top ten by value in the world today, including Amazon, Nvidia, and Taiwan Semiconductor Company. Properly managed, disruption no longer need equate to excessive risk. Funds operated by this manager: |

28 Mar 2022 - Manager Insights | ASCF

|

|

||

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Filippo Sciacca, Director of Investor Relations & Asset Management at ASCF. The ASCF High Yield Fund has a track record of 5 years and has outperformed the Bloomberg AusBond Composite 0+ Yr Index since inception in March 2017, providing investors with an annualised return of 8.73% compared with the index's return of 2.73% over the same period.

|

28 Mar 2022 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

||||||||||||||||||||||||||||

| Warakirri Diversified Agriculture Fund | ||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||||||

|

L1 Long Short Fund Limited (ASX: LSF) |

||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||||||

|

L1 Capital Global Opportunities Fund |

||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

| CIPAM Multi-Sector Private Lending Fund | ||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||||||||

|

Subscribe for full access to these funds and over 650 others |

||||||||||||||||||||||||||||

28 Mar 2022 - Like kites, do portfolios rise against or with the wind?

|

Like kites, do portfolios rise against or with the wind? Spatium Capital March 2022 For the runners, cyclists or outdoor sportspeople within our readership, a handful of circumstances will almost always result in a proverbial groan: headwinds. That gust of wind that makes turning that corner on the bike or spending the next half of a game with a wind impediment less enjoyable, is unfortunately a part of exercising amongst the elements. Headwinds, as it were, have become known as such a physical inconvenience that they are also a common analogy for when situations in life are met with obstacles that inhibit progress. The counter to a headwind therefore is a tailwind, where benefits and/or privileges fuel our progress, bypassing or simply overcoming the obstacles (or headwinds) that come our way. If we then take this concept and apply it to a fund manager's portfolio, how many would attribute their performance success to an investing skill or purely an outcome of a bull market? Put another way, did the manager overcome genuine obstacles (a headwind) to achieve success, or were they the beneficiary of a rising market (a tailwind)? Recent research published by social scientists Dr Gilovich and Dr Davidai in 2016 suggests that people are more likely to both recall and overweight their headwinds more poignantly than those of their tailwinds. Their theory claims that when people benefit from a tailwind, the satisfaction is adapted to quickly and is relatively short-lived, whilst a headwind's dissatisfaction is 'consumed' over a longer-period. Using the sporting analogy at the top of the above paragraph, many can relate to the internal monologue that goes on when a headwind is faced; often, longing for the tailwind. Usually, this monologue does not end until the tailwind is experienced. At which point, a brief sense of relief is felt and the team or individual go about adjusting to the new advantage. Almost without a second thought! This tendency to recount information in a way that confirms one's view (confirmation bias) that they had more obstacles than benefits has been coined by Gilovich and Davidai as the headwind-tailwind asymmetry. It is suggested that because a headwind is an obstacle that needs to be addressed, whether that be in a career, sport, relationship or an investment context, there is a greater propensity for these events to be etched into our memories. Their very existence can in fact precede critical junctures and choices in our lives. Conversely, a tailwind is a privilege that often goes unseen by its very nature of not necessitating significant effort or attention. It's harder to recount a privileged education, upbringing, career opportunities or investment successes when they were already occurring without requiring effort. At Spatium, we pride ourselves on having outperformed the benchmark (a headwind) without having a beta in excess of the benchmark, or resorting to leverage or gearing within the fund (an easy 'tailwind' during a rising market environment). Conversely, when the market winds inevitably change, Spatium has had a long-term average of losing only half as much as the benchmark. When assessing managers, portfolios, or even individual companies, one must be critical: "has this business overcome genuine headwinds, and has the strength, knowledge and processes to do so again in the future" or, "has this business simply benefitted from structural tailwinds", such as declining interest rates, or similar paradigm shifts, those of which may be unlikely to be repeated at the same amplitude (or in the case of rising interest rates, potentially work as a headwind) into the future. In aggregate, one should enjoy just as many tailwinds as headwinds over the years, with the key focus being maximising ones advantage during tailwind periods, and remaining convicted to persevering through intermittent headwinds. Author: Jesse Moores, Director |

|

Funds operated by this manager: |