NEWS

19 Apr 2022 - Performance Report: Quay Global Real Estate Fund (Unhedged)

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund will invest in a number of global listed real estate companies, groups or funds. The investment strategy is to make investments in real estate securities at a price that will deliver a real, after inflation, total return of 5% per annum (before costs and fees), inclusive of distributions over a longer-term period. The Investment Strategy is indifferent to the constraints of any index benchmarks and is relatively concentrated in its number of investments. The Fund is expected to own between 20 and 40 securities, and from time to time up to 20% of the portfolio maybe invested in cash. The Fund is $A un-hedged. |

| Manager Comments | The Quay Global Real Estate Fund (Unhedged) has a track record of 6 years and 3 months and has outperformed the BBAREIT Index since inception in January 2016, providing investors with an annualised return of 8.92% compared with the index's return of 6.6% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 6 years and 3 months since its inception. Over the past 12 months, the fund's largest drawdown was -8.2% vs the index's -11.14%, and since inception in January 2016 the fund's largest drawdown was -19.68% vs the index's maximum drawdown over the same period of -23.56%. The fund's maximum drawdown began in February 2020 and lasted 1 year and 4 months, reaching its lowest point during September 2020. The fund had completely recovered its losses by June 2021. The Manager has delivered these returns with 0.45% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 three times over the past five years and which currently sits at 0.69 since inception. The fund has provided positive monthly returns 74% of the time in rising markets and 36% of the time during periods of market decline, contributing to an up-capture ratio since inception of 70% and a down-capture ratio of 60%. |

| More Information |

19 Apr 2022 - Performance Report: 4D Global Infrastructure Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The fund is managed as a single portfolio including regulated utilities in gas, electricity and water, transport infrastructure such as airports, ports, road and rail, as well as communication assets such as the towers and satellite sectors. The portfolio is intended to have exposure to both developed and emerging market opportunities, with country risk assessed internally before any investment is considered. The maximum absolute position of an individual stock is 7% of the fund. |

| Manager Comments | The 4D Global Infrastructure Fund has a track record of 6 years and 1 month and has outperformed the S&P Global Infrastructure TR (AUD) Index since inception in March 2016, providing investors with an annualised return of 9.54% compared with the index's return of 8.87% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 6 years and 1 month since its inception. Over the past 12 months, the fund's largest drawdown was -3.9% vs the index's -0.57%, and since inception in March 2016 the fund's largest drawdown was -19.77% vs the index's maximum drawdown over the same period of -24.67%. The fund's maximum drawdown began in February 2020 and has lasted 2 years and 1 month, reaching its lowest point during September 2020. The Manager has delivered these returns with 0.52% less volatility than the index, contributing to a Sharpe ratio which has fallen below 1 three times over the past five years and which currently sits at 0.75 since inception. The fund has provided positive monthly returns 95% of the time in rising markets and 14% of the time during periods of market decline, contributing to an up-capture ratio since inception of 100% and a down-capture ratio of 96%. |

| More Information |

19 Apr 2022 - Two lessons on what to avoid in a market bubble

|

Two lessons on what to avoid in a market bubble Nikko Asset Management March 2022 Have you ever stopped to imagine what would happen if the world's central banks spent just over a decade pouring USD 25 trillion of liquidity into the economy, with more than 60% of that liquidity created in the last two years? If you are like the overwhelming majority of people, the answer is almost certainly no. The good news is you don't have to imagine as this is precisely the situation we are in today. In this article, we assess what has happened and provide some thoughts around how investors should navigate the next phase of the greatest financial experiment of all time.

USD 25 trillion is almost an unimaginable amount of money so what has happened to all of this liquidity? Well, rather inevitably, a lot of it has found its way into asset markets. The value of almost everything has gone up - considerably. From wine to whisky, growth stocks to digital gold, the returns to asset owners have been extraordinary since the depths of the financial crisis in 2009. Younger generations have gone from occupying Wall Street to trading Bitcoin on margin and buying meme stocks on trading platforms as if it were a video game. Old people "just don't get it" and lack the imagination to see just how enormous the returns will be. Make no mistake, there are many aspects of this that have the trappings of a bubble. This is nothing new. In late 1636 in the Netherlands, the Viceroy tulip bulb sold for four fat oxen, eight pigs or 12 fat sheep. As many bulbs flowered in 1637, prices crashed and by early 1638, the government decreed that tulip contracts should be annulled in return for the payment of 3.5% of the original price. There are many examples of financial speculation littered throughout history and interestingly several of these are also linked to technological innovation. Investors in railway bonds in the 19th century enabled the construction of vast networks in Europe and the US which enhanced productivity and had a huge impact on the way people lived and worked. Investors in railroads typically made little profit however, and most of the long-term gains were arguably made by the businesses and people in cities which grew up as a result of their newly connected status. The dot-com internet bubble of the late 1990s had a very similar story at its heart. Investors in the companies who built the internet networks and operated them thereafter either lost everything or made very poor long-term returns. The real beneficiaries of the networks created in the bubble were businesses like Apple, Google, Facebook, Netflix, and Amazon*, who used those networks to sell us the products and services that meant we got the most out of them. They were effectively the hotel at the end of the railway line which stood to gain the most from the passengers arriving on the newly constructed network. Is there a bubble today and if so, where is it and how can we expect things to pan out from here? The first thing that strikes us is investors' have very long-time horizons and the second is the sheer number of companies that are forecast to make significant losses for the foreseeable future. This is dangerous. The future is highly unpredictable, and far more things can happen than actually will happen. For example, if you were asked in 1969 what would be the greatest innovation in 40 years' time, you'd be forgiven for answering that humans would have colonised space and we would all be going on holiday to Mars (given Neil Armstrong had just set foot on the moon). Instead, the reality in 2009 was that the Apple iPhone was being rolled out which effectively placed the sum of all human knowledge in your pocket. We should be wary of people selling us a version of the future based on science fiction rather than practical and applicable facts.

Given the dangerous nature of these speculative businesses experiencing heavy losses and cash burn, what should we do from here? For us, understanding the drivers of cash flows and the returns on investment made by the companies we invest in is critical to the long-term health of our portfolio. By investing in businesses with strong competitive advantages who remain disciplined around capital allocation, we aim to find the next set of 'hotels at the end of the railway line' that will benefit from the new activities created by this latest bout of speculative excess. If lesson one is to avoid loss-making, cash-burning businesses chasing a pipe dream of market share, what next? In our opinion, lesson two is "beware the wolf of cyclicality wrapped up in the sheep's clothing of growth". The journey from a growth stock to a value stock can be damaging to your financial health. It strikes us that in industries such as digital advertising, investors may be mistaking a maturing industry that has seen a pull- forward of demand for one which still offers enormous secular growth. The pandemic saw an enormous amount of liquidity added to the system, and many speculative businesses received funding and/or very high valuations which they may not have otherwise. It's worth noting that a number of these new companies' costs (after generous option packages for senior staff) are spent on IT infrastructure and services, as well as digital advertising to gain market share. When you add in the pull forward of time spent at home/online for consumers in the pandemic, and inflationary pressures, it is perhaps no surprise that digital advertising in all its forms may face a more challenging outlook over the next few years. Navigating choppy watersIf we have established a few things to avoid, the obvious question remains around where are the opportunities? In our opinion, there are many businesses that have been left behind from the speculative excess of the last two years because their businesses have been negatively impacted by the pandemic which offer opportunities. In the provision of home nursing care and patient rehabilitation for example, companies such as LHC group and Encompass Health have suffered from dramatically rising costs due to a shortage of nurses exacerbated by the need for staff to quarantine following exposure to COVID-19. As the pandemic ebbs, the staffing situation is expected to normalise, and we see these companies benefitting from improving pricing as the Centers for Medicare and Medicaid Services (CMS), a US federal agency that administers the Medicare programme, has affirmed reimbursement rates which begin to take account of these near-term challenges. This should position these companies for a better 2022 while many in the digital advertising industry may face exactly the opposite scenario. Another area we feel remains underappreciated is in the provision of contract catering. Punished by stringent lockdowns and a shift away from office-based working, many of these businesses were forced to raise capital and adapt quickly to a very new reality in the pandemic. As healthcare providers, schools and universities grapple with rising costs and labour shortages, they are now outsourcing their catering operations at a record pace and the pipeline of new business for a company like Compass has never been better. Also, consumption at stadiums where the firm has many concessions is booming as people make the most of attending live sports and cultural events. These businesses are reinvesting for structural growth, but many investors perceive them to be too old hat to be interesting. 'Boring' improvements in return on capital might be just the menu item investors should choose in what may continue to be a challenging 2022. Valuation rationality and margin for safetyWe have highlighted that we have been experiencing some speculative excesses within parts of the equity markets for some time, and there have been some clear parallels to historical bubbles. Our philosophy is focused on compounding clients' capital over time rather than being a slave to the shorter-term gyrations of the market. We focus on the following:

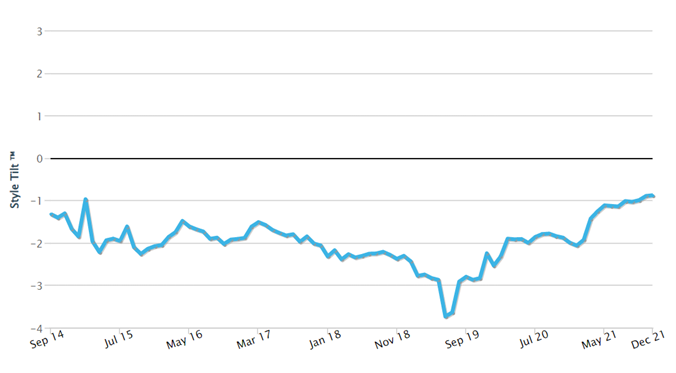

The latter point has been more relevant for portfolios in the last 12-18 months, as we have been in a period where easy monetary policy has encouraged investors to price future growth very generously. This has resulted in reductions in some holdings or a complete exit on valuation grounds, with the proceeds recycled into Future Quality companies that have better valuation support. We are comfortable paying a premium for companies that deliver better and more consistent growth, can attain, and sustain high returns on invested capital and have strong balance sheets - but that premium needs to be appropriate and fair. The following history from style analytics confirms that we have stuck to that discipline. Chart 1: Cash Flow Yield

Source: Style Analytics as at 31 December 2021

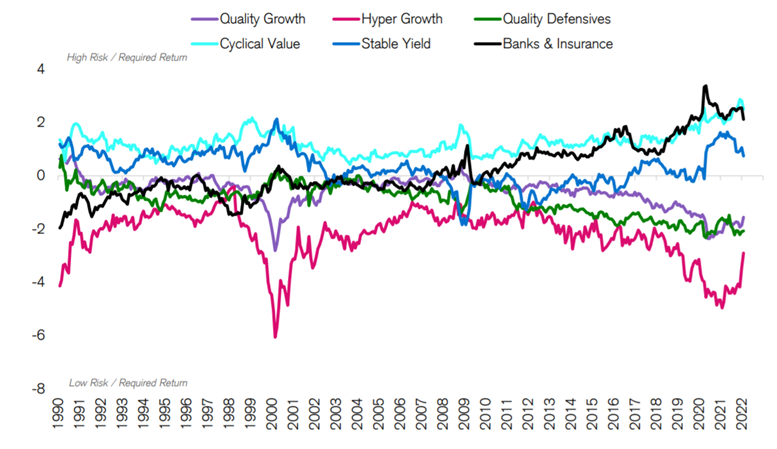

We believe we have entered an unknown period of tightening liquidity, with the evolution of supply-related inflationary inputs and central bank responses remaining the dominant drivers for returns from and within equities as an asset class. History would suggest that following an unwind from periods of excess, the prior winners typically don't regain leadership again. Given the lack of profitability of many companies that some have described as 'concept finance', this makes sense, as over the long term the delivery of cash flow and growth is the key determinant on share prices. Chart 2: Group Median Market Implied Yield (MIY) Spread vs Market

Source: Credit Suisse HOLT, Data date 2/4/2022. Universe: Top 2000 Global companies by TTM Market cap. Market Implied Yields for Financial firms on the HOLT CFROE model are trimmed by 150 bps throughout this analysis to preserve comparability.Chart 2 highlights that the growth versus value debate dominating many conversations is becoming less important for most companies. except for those with very high growth expectations. The path of future growth and profitability will likely soon start to dominate again as the driver for individual share prices once the current period of unwinding and rotation has exhausted. We believe our portfolio of Future Quality stock picks should be well placed when that time arrives. *Reference to individual stocks is for illustration purpose only and does not guarantee their continued inclusion in the strategy's portfolio, nor constitute a recommendation to buy or sell.Author: Iain Fulton (Portfolio Manager) and Will Low (Head of Global Equities), Nikko AM, Yarra Capital Management's global partner Funds operated by this manager: Nikko AM ARK Global Disruptive Innovation Fund, Nikko AM Global Share Fund, Nikko AM New Asia Fund, Disclaimer This material has been prepared by Nikko Asset Management Europe Ltd (NAM Europe) which is authorised and regulated in the United Kingdom by the FCA. This material is issued in Australia by Yara Capital Management Limited (formerly Nikko AM Limited) ABN 99 003 376 252, AFSL 237563. To the extent that any statement in this material constitutes general advice under Australian law, the advice is provided by Yarra Capital Management Limited. NAM Europe does not hold an AFS Licence. Effective 12 April 2021, Yarra Capital Management Limited became part of the Yarra Capital Management Group. The information contained in this material is of a general nature only and does not constitute personal advice, nor does it constitute an offer of any financial product. It is for the use of researchers, licensed financial advisers and their authorised representatives, and does not take into account the objectives, financial situation or needs of any individual. For this reason, you should, before acting on this material, consider the appropriateness of the material, having regard to your objectives, financial situation and needs. The information in this material has been prepared from what is considered to be reliable information, but the accuracy and integrity of the information is not guaranteed. Figures, charts, opinions and other data, including statistics, in this material are current as at the date of publication, unless stated otherwise. The graphs and figures contained in this material include either past or backdated data and make no promise of future investment returns. Past performance is not an indicator of future performance. Any economic or market forecasts are not guaranteed. Any references to particular securities or sectors are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities or sectors and no warranty or guarantee is provided. Portfolio holdings may not be representative of current or future investments. The securities discussed may not represent all of the portfolio's holdings and may represent only a small percentage of the strategy's portfolio holdings. Future portfolio holdings may not be profitable. Any mention of an investment decision is intended only to illustrate our investment approach or strategy and is not indicative of the performance of our strategy as a whole. Any such illustration is not necessarily representative of other investment decisions. Portfolio holdings may change by the time you receive this. Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold, or directly invest in the company or its securities. The information set out has been prepared in good faith and while Yarra Capital Management Limited and its related bodies corporate (together, the "Yarra Capital Management Group") reasonably believe the information and opinions to be current, accurate, or reasonably held at the time of publication, to the maximum extent permitted by law, the Yarra Capital Management Group: (a) makes no warranty as to the content's accuracy or reliability; and (b) accepts no liability for any direct or indirect loss or damage arising from any errors, omissions, or information that is not up to date. Yarra Capital Management. Copyright 2022. |

14 Apr 2022 - Hedge Clippings |14 April 2022

|

|

|

|

Hedge Clippings | Thursday, 08 April 2022

Following Anthony Albanese's clanger on Day 1 of the 2022 election campaign, former opposition leader Bill Shorten tried to pay Scott Morrison a compliment by warning his Labor colleagues that ScoMo was, or is, a formidable campaigner and not be underestimated. Bill Shorten should know. However, he either forgot or didn't want to accept responsibility for losing the 2019 election which everyone, including the polls, expected him to win. For those with short memories, or those understandably distracted by the almost biblical-like dramas of the last three years (bush fires, COVID, floods, and now war), Shorten and his then shadow treasurer, Chris Bowen came up with the dopey idea (at least going into an election) of proposing to do away with franking credits. At that time (March 2018) Hedge Clippings suggested this was a dangerous move, and became a little creative, even penning a poem, the last verse of which ran: But Willie's got his facts wrong, as pollies often do, Bowen then doubled down by suggesting that those voters (many of whom were pensioners) likely to be disadvantaged by a return to double taxation of dividend income, could vote Liberal instead. Which, as history recalls, they did! As a result, Bowen has hardly been seen since, and certainly not heard of from an economics point of view. But why would you need a former shadow treasurer when Albo, the leader of the opposition, is - or claims to be - a former economics adviser to Bob Hawke? Not being across the most basic of current economic statistics is possibly forgivable, although a clear indicator of where his interests really lie, but to follow that up with a false and easily fact checked claim, smacked of desperation. Albanese's been keen to maintain a small target heading into this election, hoping that ScoMo's missteps over the past three years will see him living the life at the Lodge and Kirribilli House after occupying the Clocktower at Sydney Uni. There's still five weeks to go, but he needs to lift his game, or Shorten's warning may prove correct. News & Insights The Rise of the Contactless Economy | Insync Fund Managers Central banks are going green to questionable avail while stirring risks | Magellan Asset Management Russia-Ukraine conflict | 4D Infrastructure |

|

|

March 2022 Performance News Insync Global Quality Equity Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

14 Apr 2022 - Performance Report: ASCF High Yield Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Does not require full valuations on loans <65% LVR. Borrowing rates are from 12% per annum on 1st mortgage loans and 16% per annum on 2nd mortgage/caveat loans. Pays investors between 5.55% - 6.25% per annum depending on their investment term. |

| Manager Comments | The ASCF High Yield Fund has a track record of 5 years and 1 month and has outperformed the Bloomberg AusBond Composite 0+ Yr Index since inception in March 2017, providing investors with an annualised return of 8.69% compared with the index's return of 1.92% over the same period. The Manager has delivered these returns with 3.73% less volatility than the index. On a calendar year basis, the fund hasn't experienced any negative annual returns in the 5 years and 1 month since its inception. Over the past 12 months, the fund hasn't had any negative monthly returns and therefore hasn't experienced a drawdown. Over the same period, the index's largest drawdown was -8.66%. Since inception in March 2017, the fund's largest drawdown was 0% vs the index's maximum drawdown over the same period of -8.94%. |

| More Information |

14 Apr 2022 - Performance Report: Bennelong Concentrated Australian Equities Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | |

| Manager Comments | The Bennelong Concentrated Australian Equities Fund has a track record of 13 years and 2 months and has outperformed the ASX 200 Total Return Index since inception in February 2009, providing investors with an annualised return of 15.71% compared with the index's return of 10.51% over the same period. On a calendar year basis, the fund has experienced a negative annual return on 2 occasions in the 13 years and 2 months since its inception. Over the past 12 months, the fund's largest drawdown was -17.98% vs the index's -6.35%, and since inception in February 2009 the fund's largest drawdown was -24.11% vs the index's maximum drawdown over the same period of -26.75%. The fund's maximum drawdown began in February 2020 and lasted 6 months, reaching its lowest point during March 2020. The fund had completely recovered its losses by August 2020. The Manager has delivered these returns with 1.69% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 four times over the past five years and which currently sits at 0.9 since inception. The fund has provided positive monthly returns 90% of the time in rising markets and 20% of the time during periods of market decline, contributing to an up-capture ratio since inception of 137% and a down-capture ratio of 93%. |

| More Information |

14 Apr 2022 - Megatrend in Focus: Enterprise Digitisation is accelerating

|

Megatrend in Focus: Enterprise Digitisation is accelerating Insync Fund Managers March 2022 Whilst we focused on this exciting megatrend and Accenture last year, things are moving even faster than forecast and so a revisit is timely. Accenture is a prime holding for this megatrend and thus remains in the Insync portfolio. In their recent earnings call, they announced a very strong demand environment. This has induced double-digit growth in all parts of their business and also across all their markets, industries and services. Many of their clients are embarking upon bold transformation programs, often spanning multiple parts of their enterprise in an accelerated time frame. Macro-economics have little impact on these companies spend on digitisation. These clients recognize the need to transform almost all of their businesses, meshing technology, data and AI and with new ways of working and delivering their product or service to market. Current market gyrations have not changed the trajectory of our identified megatrends (including this one) in the Insync portfolio. Our companies such as Accenture continue to grow profitably at multiples many times that of GDP.

Insync's intense focus on the fundamentals, investing in businesses like Accenture that are compounding their earnings at high rates, gives us confidence that the portfolio is well positioned to deliver strong returns as volatility in markets subside. Stocks held by Insync possess:

Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund |

13 Apr 2022 - Performance Report: L1 Capital Long Short Fund (Monthly Class)

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | |

| Manager Comments | The L1 Capital Long Short Fund (Monthly Class) has a track record of 7 years and 7 months and has outperformed the ASX 200 Total Return Index since inception in September 2014, providing investors with an annualised return of 23.56% compared with the index's return of 8.24% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 7 years and 7 months since its inception. Over the past 12 months, the fund's largest drawdown was -7.21% vs the index's -6.35%, and since inception in September 2014 the fund's largest drawdown was -39.11% vs the index's maximum drawdown over the same period of -26.75%. The fund's maximum drawdown began in February 2018 and lasted 2 years and 9 months, reaching its lowest point during March 2020. The fund had completely recovered its losses by November 2020. The Manager has delivered these returns with 6.47% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 two times over the past five years and which currently sits at 1.08 since inception. The fund has provided positive monthly returns 79% of the time in rising markets and 64% of the time during periods of market decline, contributing to an up-capture ratio since inception of 93% and a down-capture ratio of 3%. |

| More Information |

13 Apr 2022 - Performance Report: Cyan C3G Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Cyan C3G Fund is based on the investment philosophy which can be defined as a comprehensive, clear and considered process focused on delivering growth. These are identified through stringent filter criteria and a rigorous research process. The Manager uses a proprietary stock filter in order to eliminate a large proportion of investments due to both internal characteristics (such as gearing levels or cash flow) and external characteristics (such as exposure to commodity prices or customer concentration). Typically, the Fund looks for businesses that are one or more of: a) under researched, b) fundamentally undervalued, c) have a catalyst for re-rating. The Manager seeks to achieve this investment outcome by actively managing a portfolio of Australian listed securities. When the opportunity to invest in suitable securities cannot be found, the manager may reduce the level of equities exposure and accumulate a defensive cash position. Whilst it is the company's intention, there is no guarantee that any distributions or returns will be declared, or that if declared, the amount of any returns will remain constant or increase over time. The Fund does not invest in derivatives and does not use debt to leverage the Fund's performance. However, companies in which the Fund invests may be leveraged. |

| Manager Comments | The Cyan C3G Fund has a track record of 7 years and 8 months and has outperformed the ASX Small Ordinaries Total Return Index since inception in August 2014, providing investors with an annualised return of 12.19% compared with the index's return of 8.62% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 7 years and 8 months since its inception. Over the past 12 months, the fund's largest drawdown was -18.65% vs the index's -9.15%, and since inception in August 2014 the fund's largest drawdown was -36.45% vs the index's maximum drawdown over the same period of -29.12%. The fund's maximum drawdown began in October 2019 and lasted 1 year and 4 months, reaching its lowest point during March 2020. The fund had completely recovered its losses by February 2021. The Manager has delivered these returns with 0.18% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.71 since inception. The fund has provided positive monthly returns 86% of the time in rising markets and 39% of the time during periods of market decline, contributing to an up-capture ratio since inception of 64% and a down-capture ratio of 64%. |

| More Information |

13 Apr 2022 - Performance Report: Bennelong Kardinia Absolute Return Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | There is a slight bias to large cap stocks on the long side of the portfolio, although in a rising market the portfolio will tend to hold smaller caps, including resource stocks, more frequently. On the short side, the portfolio is particularly concentrated, with stock selection limited by both liquidity and the difficulty of borrowing stock in smaller cap companies. Short positions are only taken when there is a high conviction view on the specific stock. The Fund uses derivatives in a limited way, mainly selling short dated covered call options to generate additional income. These typically have less than 30 days to expiry, and are usually 5% to 10% out of the money. ASX SPI futures and index put options can be used to hedge the portfolio's overall net position. The Fund's discretionary investment strategy commences with a macro view of the economy and direction to establish the portfolio's desired market exposure. Following this detailed sector and company research is gathered from knowledge of the individual stocks in the Fund's universe, with widespread use of broker research. Company visits, presentations and discussions with management at CEO and CFO level are used wherever possible to assess management quality across a range of criteria. |

| Manager Comments | The Bennelong Kardinia Absolute Return Fund has a track record of 15 years and 11 months and has outperformed the ASX 200 Total Return Index since inception in May 2006, providing investors with an annualised return of 8.07% compared with the index's return of 6.72% over the same period. On a calendar year basis, the fund has experienced a negative annual return on 2 occasions in the 15 years and 11 months since its inception. Over the past 12 months, the fund's largest drawdown was -7.06% vs the index's -6.35%, and since inception in May 2006 the fund's largest drawdown was -11.71% vs the index's maximum drawdown over the same period of -47.19%. The fund's maximum drawdown began in June 2018 and lasted 2 years and 6 months, reaching its lowest point during December 2018. The fund had completely recovered its losses by December 2020. During this period, the index's maximum drawdown was -26.75%. The Manager has delivered these returns with 6.49% less volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.68 since inception. The fund has provided positive monthly returns 87% of the time in rising markets and 33% of the time during periods of market decline, contributing to an up-capture ratio since inception of 16% and a down-capture ratio of 52%. |

| More Information |