NEWS

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund rose by +21.44% over the past 12 months. Since inception in June 2018, the fund has returned +10.44% per annum, an outperformance of +1.42% relative to the ASX 200 Total Return benchmark which has returned...

Read more...

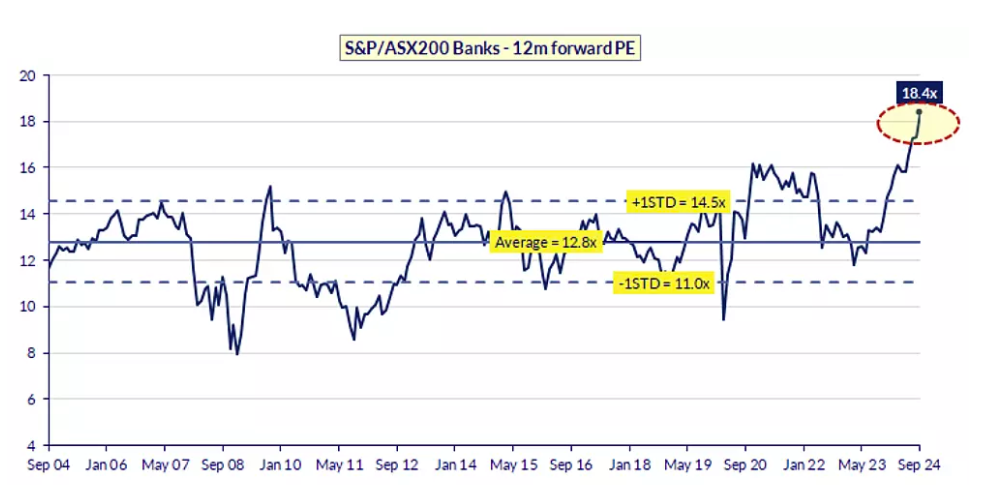

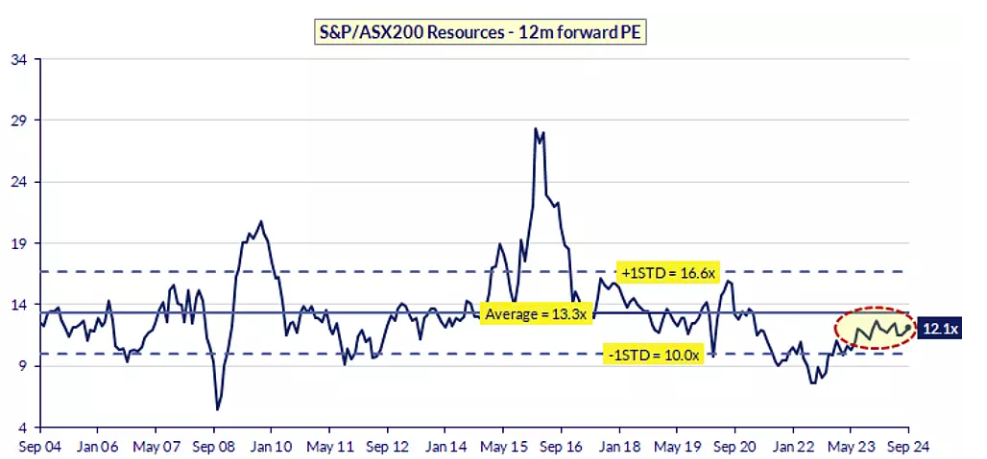

Have ASX iron ore stocks found their floor?

Recently, the People's Bank of China (PBOC) rolled out its most significant set of monetary easing policies since 2015. These measures were designed to address China's ongoing property sector challenges and provide a broader boost to...

Read more...

Performance Report: Quay Global Real Estate Fund (Unhedged)

The Quay Global Real Estate Fund (Unhedged) returned -0.91% in October. Since inception in January 2016, the fund has returned +7.44% per annum, an outperformance of +3.01% relative to the FTSE EPRA/ NAREIT Developed NET TR benchmark which...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +2.3% in October, outperforming the ASX 200 Total Return benchmark by +3.61%. Since inception in January 2013, the fund has returned +12.99% per annum, an outperformance of +3.71% relative to the...

Read more...

Green AI

AI has certainly created a buzz over the past couple of years. While a lot of attention has been focussed on Nvidia, the global poster child for the AI sector, there has been a raft of cascading effects that have trickled down to related...

Read more...

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund rose by +24.84% over the past 12 months. Since inception in February 2009, the fund has returned +13.04% per annum, an outperformance of +3.02% relative to the ASX 200 Total Return...

Read more...

Megatrends for 2025 and beyond...

Megatrends are long-term structural changes that affect the

world we live in. Importantly, they shape communities, but they

also create investment opportunities and risks.

world we live in. Importantly, they shape communities, but they

also create investment opportunities and risks.

Read more...

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) rose by +0.63% in October. Since inception in March 2016, the fund has returned +9.2% per annum, a difference of -0.35% relative to the S&P Global Infrastructure TR (AUD) benchmark which has...

Read more...

Performance Report: ASCF High Yield Fund

The ASCF High Yield Fund rose by +0.64% in October, outperforming the Bloomberg AusBond Composite 0+ Yr benchmark by +2.52%. Since inception in March 2017, the fund has returned +8.15% per annum, an outperformance of +6.61% relative to the...

Read more...

Performance Report: Bennelong Australian Equities Fund

The Bennelong Australian Equities Fund rose by +24.06% over the past 12 months. Since inception in February 2009, the fund has returned +11.74% per annum, an outperformance of +1.72% relative to the ASX 200 Total Return benchmark which...

Read more...