NEWS

15 Jul 2022 - Performance Report: Bennelong Australian Equities Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | |

| Manager Comments | The Bennelong Australian Equities Fund has a track record of 13 years and 5 months and has outperformed the ASX 200 Total Return Index since inception in February 2009, providing investors with an annualised return of 11.96% compared with the index's return of 9.27% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 13 years and 5 months since its inception. Over the past 12 months, the fund's largest drawdown was -29.92% vs the index's -11.9%, and since inception in February 2009 the fund's largest drawdown was -29.92% vs the index's maximum drawdown over the same period of -26.75%. The fund's maximum drawdown began in December 2021 and has lasted 6 months, reaching its lowest point during June 2022. During this period, the index's maximum drawdown was -11.9%. The Manager has delivered these returns with 1.39% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.69 since inception. The fund has provided positive monthly returns 91% of the time in rising markets and 17% of the time during periods of market decline, contributing to an up-capture ratio since inception of 129% and a down-capture ratio of 99%. |

| More Information |

15 Jul 2022 - Performance Report: Insync Global Quality Equity Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Insync invests in a concentrated portfolio of high quality companies that possess long 'runways' of future growth benefitting from Megatrends. Megatrends are multiyear structural and disruptive changes that transform the way we live our daily lives and result from a convergence of different underlying trends including innovation, politics, demographics, social attitudes and lifestyles. They provide important tailwinds to individual stocks and sectors, that reside within them. Insync believe this delivers exponential earnings growth ahead of market expectations. Insync screens the universe of 40,000 listed global companies to just 150 that it views as superior. This includes profitability, balance sheet performance, shareholder focus and valuations. 20-40 companies are then chosen for the portfolio. These reflect the best outcomes from further analysis using a proprietary DCF valuation, implied growth modelling, and free cash flow yield; alongside management, competitor, and industry scrutiny. The Fund may hold some cash (maximum of 5%), derivatives, currency contracts for hedging purposes, and American and/or Global Depository Receipts. It is however, for all intents and purposes, a 'long-only' fund, remaining fully invested irrespective of market cycles. |

| Manager Comments | The Insync Global Quality Equity Fund has a track record of 12 years and 9 months and has outperformed the Global Equity Index since inception in October 2009, providing investors with an annualised return of 11.47% compared with the index's return of 10.24% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 12 years and 9 months since its inception. Over the past 12 months, the fund's largest drawdown was -27.21% vs the index's -15.77%, and since inception in October 2009 the fund's largest drawdown was -27.21% vs the index's maximum drawdown over the same period of -15.77%. The fund's maximum drawdown began in January 2022 and has lasted 5 months, reaching its lowest point during June 2022. The Manager has delivered these returns with 1.47% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.81 since inception. The fund has provided positive monthly returns 82% of the time in rising markets and 20% of the time during periods of market decline, contributing to an up-capture ratio since inception of 83% and a down-capture ratio of 87%. |

| More Information |

15 Jul 2022 - Mind the gap - Hedging tails to provide liquidity in times of stress

|

Mind the gap - Hedging tails to provide liquidity in times of stress (Adviser & wholesale investors only) CIP Asset Management July 2022 Including tail hedging in a portfolio can have the following benefits:

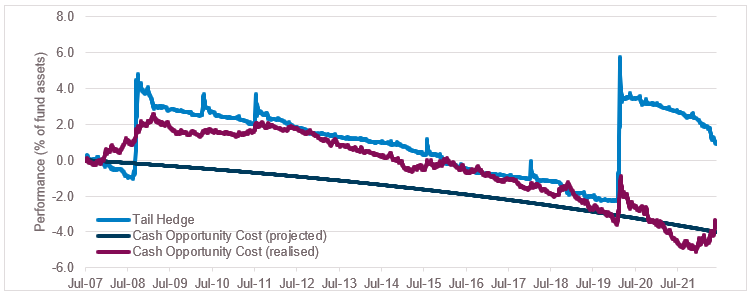

Point 3 may be of particular interest to Australian super funds where, for example, FX hedges can incur large mark-to-market losses during times of market stress. For example, the latest Quarterly Superannuation Statistics published by APRA (March 2022) show the industry currently has $322bn of FX hedges. During the financial crisis AUD dropped 37.6%, which would have led to FX hedge losses of -$121bn based on current exposures at a time the overall portfolio was down -26% (-$577bn in today's terms), and a COVID scenario would result in FX losses of around -$58bn at a time overall assets were down -$466bn. Investors use a variety of approaches to try and mitigate losses in their portfolios, including diversification, market timing, and explicit hedging. While we agree all three approaches have a place in managing portfolios, hedging is by far the most reliable way to mitigate losses during times of market stress. It (almost) goes without saying that even investors who successfully add long-term alpha for their clients via market timing cannot always predict market drawdowns, and one only needs to look at recent market moves to see the pitfalls of relying too heavily on diversification (eg simultaneous sell-off in equities and fixed income with ACWI -18.9% and Global Agg -14.5% YTD on a total return basis). Because it is reliable, hedging can be an important tool in building resilient long-term portfolios. However, that reliability comes at a cost, and because true market stress events are few and far between, we often find that the costs of hedging are more visible to investors than the benefits. Since most investors are not particularly concerned by small drawdowns, the cost of hedging can be reduced by focusing only on larger, less-frequent drawdowns. Specifically, tail hedging allows investors to hedge against only the most extreme outcomes that can inflict long-lasting damage on even the most diversified portfolios. It's worth reiterating that because tail hedging, by design, is only expected to 'work' in the most extreme circumstances, investors can expect to see (modest) losses in tail hedges far more frequently than they will see gains. However, it is the timing and magnitude of the gains that is important. A robust tail hedging program will provide investors with large gains when other parts of the portfolio are experiencing very large drawdowns. And that knowledge may also allow investors to adopt a barbell approach and take higher risk, and earn higher returns, elsewhere in the portfolio. One final point: to be reliable, a tail hedge needs to be "always on" since the whole point of hedging is that we can't always predict a drawdown. In this regard, systematic option strategies can be particularly useful. In addition to the FX exposures outlined previously, an additional liquidity drain may come in the form of capital calls on private equity commitments. The super industry currently has approximately $106bn exposure to private equity. Some basic assumptions (1) lead to a rough estimate of $11bn liquidity required in a crisis year. Further liquidity needs might reasonably be expected to arise from such things as capital raising (eg rights issues) from portfolio companies, investment opportunities in real estate, infrastructure etc arising from market and/or funding stress. The main point is that super funds can expect to have high liquidity obligations that are required (or desired) to be met during times of market turmoil, on our calculations as much as 6% of fund assets, and possibly much more. A super fund could budget for this by setting aside some amount to be held in low risk, highly liquid instruments such as cash, ready to be deployed in times of stress. However, such an approach has an opportunity cost because the return on cash is much lower than the return on the rest of the portfolio. Using the past 15y years as a rough guide, a cash investment would have returned 2.6%p.a. vs approximately 5%p.a. for a typical balanced super portfolio. The last 10y would have been an even larger difference (1.5% vs 8%). The chart below shows the performance of a systematic tail hedge strategy(2) (light blue line) compared to the realised opportunity cost of holding an additional 6% of fund assets in cash (purple line) and the projected constant opportunity cost of holding cash (dark blue line).

Figure 1: Tail hedge strategy vs opportunity cost of holding cash. The chart shows the long-term performance impact of running a tail hedge strategy can be substantially less than holding additional cash in the portfolio. The mark-to-market of the tail hedging program would need to be met over time, but the chart shows that the realised negative performance during "normal" periods is no more than the drag on performance from holding excess cash, and during stress periods the tail hedging realises large gains which can be used to meet any liquidity requirements. For the specific objective of providing liquidity during a crisis, we find an effective tail hedging program to be a more efficient approach despite the perceived "cost" of hedging. 1 10y fund life, 5y investment phase with capital called evenly, investment realisations of zero in a market crisis. 2 The example strategy is a SPX 3m 1×4 20d/5d put spread rolled monthly. |

|

Funds operated by this manager: |

14 Jul 2022 - Performance Report: Insync Global Capital Aware Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Insync invests in a concentrated portfolio of high quality companies that possess long 'runways' of future growth benefitting from Megatrends. Megatrends are multiyear structural and disruptive changes that transform the way we live our daily lives and result from a convergence of different underlying trends including innovation, politics, demographics, social attitudes and lifestyles. They provide important tailwinds to individual stocks and sectors, that reside within them. Insync believe this delivers exponential earnings growth ahead of market expectations. The fund uses Put Options to help buffer the depth and duration that sharp, severe negative market impacts would otherwide have on the value of the fund during these events. Insync screens the universe of 40,000 listed global companies to just 150 that it views as superior. This includes profitability, balance sheet performance, shareholder focus and valuations. 20-40 companies are then chosen for the portfolio. These reflect the best outcomes from further analysis using a proprietary DCF valuation, implied growth modelling, and free cash flow yield; alongside management, competitor, and industry scrutiny. The Fund may hold some cash (maximum of 5%), derivatives, currency contracts for hedging purposes, and American and/or Global Depository Receipts. It is however, for all intents and purposes, a 'long-only' fund, remaining fully invested irrespective of market cycles. |

| Manager Comments | The Insync Global Capital Aware Fund has a track record of 12 years and 9 months and has underperformed the Global Equity Index since inception in October 2009, providing investors with an annualised return of 9.59% compared with the index's return of 10.24% over the same period. On a calendar year basis, the fund has experienced a negative annual return on 2 occasions in the 12 years and 9 months since its inception. Over the past 12 months, the fund's largest drawdown was -27.39% vs the index's -15.77%, and since inception in October 2009 the fund's largest drawdown was -27.39% vs the index's maximum drawdown over the same period of -15.77%. The fund's maximum drawdown began in January 2022 and has lasted 5 months, reaching its lowest point during June 2022. The Manager has delivered these returns with 0.83% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.69 since inception. The fund has provided positive monthly returns 81% of the time in rising markets and 22% of the time during periods of market decline, contributing to an up-capture ratio since inception of 59% and a down-capture ratio of 82%. |

| More Information |

14 Jul 2022 - Be an investor not a speculator

|

Be an investor not a speculator Claremont Global June 2022 The current market sell-off has many market participants running for cover and waiting till the "uncertainty clears." Issues concerning the market are well-known - central bank tightening, high inflation, the Ukraine conflict, supply chain shortages and increasing concerns of a recession in 2023. And in current markets, I am reminded of the timeless words of Benjamin Graham (the father of security analysis and Warren Buffet's mentor) who made the clear distinction between investment and speculation. In his seminal work "The Intelligent Investor" on the very first page he makes the following observation:

Defining an adequate returnWhen reading this quote the key word is adequate. Note that Graham makes no mention of market timing or predicting a bottom - a practice much loved by sell-side strategists. So what is considered an adequate return? Over the 100 years to December the S&P 500 has given an annual return of 8% p.a. Equity returns are simply a function of:

The S&P 500 path to adequateLet's break down these constituents: Earnings growth: looking at 2007 as our starting base (i.e. peak of that cycle) and using consensus earnings in FY22 - earnings per share (EPS) growth was on average close to 6 per cent per annum over the 15-year period. We think this number is a reasonable proxy of our long-term estimate for future earnings growth. Dividends: the current dividend yield is 1.6 per cent. PE expansion/compression: this is the hardest to forecast and requires an accurate forecast of future investor psychology and interest rates. Over the last 15 years the market multiple has averaged 16 times and the current multiple is 17.4x. Assuming a reversion to 16x over 10 years would detract 0.8% p.a. from an investor's return.

Source: FactSet If we add these three constituents together it leads to a return of 6.8% per cent - somewhat short of the long-term equity return of 8 per cent. And while this may not be quite "adequate", it is still a reasonable return compared to what's currently on offer in a savings account - although hopefully news here is improving and central bankers will offer some comfort to hard-pressed pensioners! This assumes one invests in the market through an index fund, where for the purposes of this article I have ignored passive fees. And as an active manager trying to beat the market - we have always targeted a long-term return of 8-12 per cent per annum. This is why last year we were cautioning clients that we expected future returns to be at the bottom end of our targeted range, given the elevated valuation of the market. However, the recent market sell-off has us feeling far more constructive and on the front foot with clients. Let's now look at this by breaking down into the same three constituents. The Claremont path to adequateEarnings growth: we believe our companies could deliver earnings growth over the long term in the low double digits. Dividends: the current yield on the fund roughly equates to our active manager fees. PE expansion/compression: our fund holdings now trade 1 per cent below their 10-year average and 13 per cent below the five-year average. We would argue that it is not unreasonable to expect PE multiples to have a neutral impact on future returns over the long-term. So, if we put this all together - we are much more confident of hitting the right side of that 8-12 per cent per annum equation than we were a few months ago. We know we have little ability to call the bottom, however at current prices we believe we have a reasonable probability of achieving an adequate return. The art of patienceTo conclude with Ben Graham and one of my favourite quotes on market fluctuations in Chapter 8 of the Intelligent Investor:

The sell-off this year has already seen us add two companies to the portfolio - companies we have been following for years while we waited patiently for an entry point. And now with 13 names in the portfolio and a cap of 15 - we have room for two more. Whilst no one likes a falling share market, it opens up a wider opportunity set for us and the ability to acquire truly great businesses at prices that ensure a fair risk-adjusted return. We intend to do just that. Author: Bob Desmond, CFA, Head of Claremont Global & Portfolio Manager Funds operated by this manager: |

13 Jul 2022 - Performance Report: L1 Capital Long Short Fund (Monthly Class)

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | |

| Manager Comments | The L1 Capital Long Short Fund (Monthly Class) has a track record of 7 years and 10 months and has outperformed the ASX 200 Total Return Index since inception in September 2014, providing investors with an annualised return of 21.02% compared with the index's return of 6.23% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 7 years and 10 months since its inception. Over the past 12 months, the fund's largest drawdown was -13.39% vs the index's -11.9%, and since inception in September 2014 the fund's largest drawdown was -39.11% vs the index's maximum drawdown over the same period of -26.75%. The fund's maximum drawdown began in February 2018 and lasted 2 years and 9 months, reaching its lowest point during March 2020. The fund had completely recovered its losses by November 2020. The Manager has delivered these returns with 6.65% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 four times over the past five years and which currently sits at 0.96 since inception. The fund has provided positive monthly returns 79% of the time in rising markets and 64% of the time during periods of market decline, contributing to an up-capture ratio since inception of 93% and a down-capture ratio of 18%. |

| More Information |

13 Jul 2022 - Meta & the battle for digital advertising supremacy

|

Meta & the battle for digital advertising supremacy Antipodes Partners Limited June 2022 Antipodes has owned Meta (previously Facebook) since the end of 2018 and despite the recent volatility in which many sold out of the company, it remains one of our top 20 holdings. We think that even though competition for eyeballs is increasing, and will continue to increase, the digital advertising pie is growing, and Meta can continue to dominate advertising revenue over our investment horizon. Further we believe there are opportunities to increase the monetisation rate of core Facebook and Instagram. In this new podcast episode, Alison Savas is joined by Ben Legg, one of the world's leading authorities on the digital advertising industry. Ben is a former Google COO, and now helps global brands advertise on social networks. Some key points covered include:

|

|

Funds operated by this manager: Antipodes Asia Fund, Antipodes Global Fund, Antipodes Global Fund - Long Only (Class I) |

13 Jul 2022 - Super-sized rate hikes, super-sized credit risk, super-size problems. Follow the dominoes.

|

Super-sized rate hikes, super-sized credit risk, super-size problems. Follow the dominoes. Jamieson Coote Bonds June 2022

The change of policy in 2022 has set off a series of dominoes for asset markets. Government Bonds were first to fall in quarter one, with other assets also following aggressively into quarter two. Listed assets are marked to market instantly (which can often be unpleasant) whilst illiquid or private markets can hold previous asset valuation marks as there is no observable price where price discovery could occur. It is worth considering what those realisable values might be if higher quality or liquid public assets are already -10, -20, -30%? Is a credit crisis about to erupt?The dominoes of change are quickly bringing attention to credit default as it stands to reason that refinancing outstanding lowly rated corporate debt will become increasingly problematic. The Australian Government was borrowing 10-year money at 1.05% in August last year, these rates have now moved to over 4.05% today. If the Government has to pay over 4% when it used to pay a bit above 1%, then spare a thought for corporate borrowers who might have borrowed at super low rates and are now asked to refinance at Government Yield of 4% plus some large credit spread component. How long will the markets have confidence in these lowly rated corporates to refinance at such punitive interest rate levels? The danger here is that they cannot ROLL those existing borrowings forward. That means there is no further credit extended and they need to REPAY the initial borrowing amount as well. That is exactly how a credit crisis erupts.

This is the policy pivot we have written about for some time and has marked a turning point in asset performance. But how does a Central Bank do that here with inflation globally between 5 and 8 %? Central Bankers are now rapidly raising rates as fighting inflation has taken absolute priority over saving corporate zombies from bankruptcy, generating material stress in the credit complex as many investors flee the asset class. Credit risk has been spectacularly dormant as the broad decline in long term Government Bond yields since the 1980's, plus support from Central Banks, has fostered a "begin" environment for the assets class, slingshot by the massive support of flows and investor sponsorship in the ''search for yield'', under the financial repression of low interest rates. That sponsorship and flow looks likely to have ended with rates markets having a stunning sell off this year, leading most asset markets to weak performance. Many public credit assets have also underperformed - primarily from their inherent fixed income duration, rather than the material recalibration of credit (spread) risk.

The US Fed moved to 1.75% this week and suggested its next move is either 0.50% or 0.75% hike to 2.25 or 2.50% in July to continue the fight against inflation by killing demand in the economy. The forces corporate credit markets are now facingSo, the next complex issue facing markets will likely revolve around credit default and the stunning rebirth of credit risk in the corporate credit fixed income space. Credit is a high specialised market which is little understood by most investors. Credit quality, as measured by ratings agencies, ranges from the highly converted (but low yielding) AAA rated issuers, all the way through to lower CCC rated issuers classified as having substantial risk of default (known in markets as 'junk'). Due to the inherent credit risk in these lower rated securities, yields are far higher to entice investors to take on the risk of default.

Any such support for the market looks very difficult to achieve this time as Central Bankers are now rapidly raising rates to fight inflation. Would you lend money to a buy now pay later platform or a growth company with no sustainable earnings to meet debt repayments in the current environment? Thankfully for Australian investors we have very few names like this, but our corporate credit does move its sympathy with global markets which are full of such names. Rate hikes strike in an uncertain worldWith materially higher rates now priced by Government Bond markets, the economy is expected to slow rapidly as rate hikes bite, hitting the public, lowering confidence and curtailing discretionary spending. Liquidity and asset quality will become important considerations for portfolios looking to benefit from steep discounts in many quality assets. We do not expect that rates will fall back to anything like the emergency levels we have seen post pandemic, so it feels like the re-birth of credit and default risk could be with us for some time yet as we move to a structurally higher rate environment than in recent years. It is important to acknowledge that the playbook in the last few episodes of a corporate credit seizure (Central Bank rate cuts and Quantitative Easing) will not work under a higher inflation and unstable geopolitical environment. That pivot of policy simply isn't available if inflation remains above Central Bank mandate levels as we would expect for the balance of 2022 due to the global energy shock. |

|

Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged), CC Jamieson Coote Bonds Global Bond Fund (Class B - Unhedged) |

12 Jul 2022 - Performance Report: DS Capital Growth Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The investment team looks for industrial businesses that are simple to understand, generally avoiding large caps, pure mining, biotech and start-ups. They also look for: - Access to management; - Businesses with a competitive edge; - Profitable companies with good margins, organic growth prospects, strong market position and a track record of healthy dividend growth; - Sectors with structural advantage and barriers to entry; - 15% p.a. pre-tax compound return on each holding; and - A history of stable and predictable cash flows that DS Capital can understand and value. |

| Manager Comments | The DS Capital Growth Fund has a track record of 9 years and 6 months and has outperformed the ASX 200 Total Return Index since inception in January 2013, providing investors with an annualised return of 12.54% compared with the index's return of 8.06% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 9 years and 6 months since its inception. Over the past 12 months, the fund's largest drawdown was -21.05% vs the index's -11.9%, and since inception in January 2013 the fund's largest drawdown was -22.53% vs the index's maximum drawdown over the same period of -26.75%. The fund's maximum drawdown began in February 2020 and lasted 6 months, reaching its lowest point during March 2020. The fund had completely recovered its losses by August 2020. The Manager has delivered these returns with 1.91% less volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.94 since inception. The fund has provided positive monthly returns 89% of the time in rising markets and 33% of the time during periods of market decline, contributing to an up-capture ratio since inception of 66% and a down-capture ratio of 62%. |

| More Information |

12 Jul 2022 - Australian Secure Capital Fund - Market Update

|

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund June 2022 Aggregated property values across the country on a monthly basis have slowed marginally, (-0.80%). The highest performer this month was Adelaide (+1.30%), followed closely by Perth (+0.40%). Australia's property price increases experienced over the last 18 months are now well and truly past their peak rate of growth. Interestingly however unit prices are holding their value better than houses across capital cities with regional property still remaining in positive growth. The market is quickly becoming a buyers market with aggregate home sales nationally through the June quarter now 15.9% lower than a year ago. However, with housing conditions cooling, the flow of new listings to the market is slowing which along with a strong labour market should help support prices Rental markets around the country also remain extremely tight with rents and residential property yields now rising at a faster rate than housing values also providing a buffer for property investors. Ultimately however it will be interest rates which will have the largest impact on the path of housing markets.

The weighted average clearance rate across the country is lower than last year at 59.8% compared to 2021's 75.4% clearance rate (-15.60%) Other cities across the board also achieved rates marginally lower than last year, with the exception of Brisbane. Brisbane increased by +5.90% compared to the previous year, with Canberra being dropping in comparison (-29.70%) Source: CoreLogic Source: CoreLogic Quick Insights Lowered Rates & Politicised Policy A new study by the Melbourne Institute has revealed that government support programs contributed very little to the health of the housing market during the pandemic. Instead, it was the RBAs low cash rate that boosted the purchases. Buyers took advantage of relatively low servicing costs and interest rates. Housing programs typically assisted only the few who applied early. The War Room Tony Lombardo, CEO of Lendlease; Janice Lee, PwC Australia Partner; Susan Lloyd-Hurwitz, CEO of Mirvac; and Tarun Gupta, CEO of Stockland, some of the nation's most senior property leaders came together earlier this month to discuss the ongoing housing crisis. The conclusion drawn in the Channel Nine boardroom was that government policies stimulating demand can only do so much. Ultimately, it is the lack of investment in property infrastructure and overly tight zoning policies that continue to stoke unaffordability. Sydney's Stamp Duties The NSW Coalition Government announced this month its new revisions to the stamp duty. The system would allow home buyers to opt-out of paying stamp duty in favour of a $400 and 0.3% annual land tax. Some were quick to note how this might increase housing prices as the money usually spent on stamp duty would instead go into an auction bid. However, as lenders take the cost of annual tax into their loan serviceability criteria, the impact of this legislation may become negligible. Funds operated by this manager: ASCF High Yield Fund, ASCF Premium Capital Fund, ASCF Select Income Fund |