NEWS

20 Jul 2022 - Performance Report: 4D Global Infrastructure Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The fund is managed as a single portfolio including regulated utilities in gas, electricity and water, transport infrastructure such as airports, ports, road and rail, as well as communication assets such as the towers and satellite sectors. The portfolio is intended to have exposure to both developed and emerging market opportunities, with country risk assessed internally before any investment is considered. The maximum absolute position of an individual stock is 7% of the fund. |

| Manager Comments | The 4D Global Infrastructure Fund has a track record of 6 years and 4 months and has outperformed the S&P Global Infrastructure TR (AUD) Index since inception in March 2016, providing investors with an annualised return of 8.79% compared with the index's return of 8.54% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 6 years and 4 months since its inception. Over the past 12 months, the fund's largest drawdown was -5.83% vs the index's -3.91%, and since inception in March 2016 the fund's largest drawdown was -19.77% vs the index's maximum drawdown over the same period of -24.67%. The fund's maximum drawdown began in February 2020 and lasted 2 years and 2 months, reaching its lowest point during September 2020. The fund had completely recovered its losses by April 2022. The Manager has delivered these returns with 0.36% less volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.69 since inception. The fund has provided positive monthly returns 96% of the time in rising markets and 13% of the time during periods of market decline, contributing to an up-capture ratio since inception of 100% and a down-capture ratio of 98%. |

| More Information |

20 Jul 2022 - The nature of a commodity boom

|

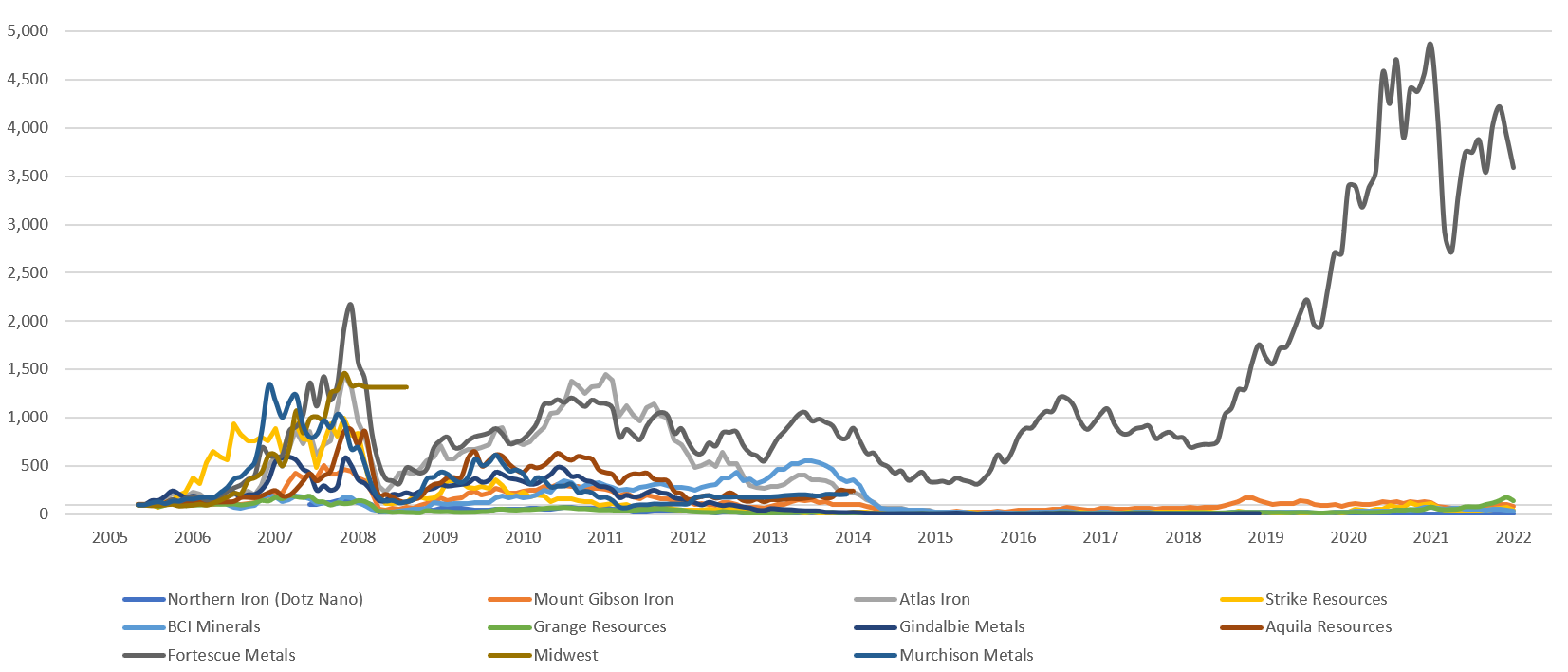

The nature of a commodity boom Eiger Capital July 2022 Speculation in commodity prices and the wave of hype that comes with it is not a new concept. Over the past few hundred years, there are many accounts of the rise and fall of a commodity's price fuelled by speculation and the promise of great profits in short-term trading. Eiger has a team favourite - Tulip Mania. We see this recurring pattern of market behaviour and have used it as a reminder as we follow the current market. Over the last 12 months, we have seen a huge rise in lithium and rare earth prices (which we categorise as advanced materials) following increasing demand for renewables and electric vehicles. We see clear parallels between the market now and the market for iron ore in 2006-2008 as China embarked on massive infrastructure spending. Let's set the scene for our comparison in the early 1630s when conditions in the Dutch republic were prosperous and increasing commercial optimism drove significant economic growth. The price of a single bulb for a desirable Tulip variety could cost the equivalent of a small townhouse in Amsterdam. By the mid-1630s, a strong market for Tulip trade existed within the Dutch Republic on news of rising demand and prices for Tulips in Paris. During late 1636 and early 1637, before planted Tulip bulbs had begun to sprout for spring, prices of Tulips of all varieties began to soar. First, the rarest, most sought-after varieties promising the greatest bloom climbed, but varieties of all shapes, sizes, and quality followed soon after. A Gouda bulb climbed from 20 to 225 guilders, the Generalissimo variety from 95 to 900, and the Yellow Croenen from 20 to 1200 in just a few weeks - the equivalent of 1 month's wage up to 5 years' wage. Credit agreements were formed for delivery of the yet to emerge blooms based merely on the prospective bloom of a bulb of a given size, weight and variety. On 3 February 1637 as spring neared, the Tulip market collapsed suddenly and agreements were torn up. In the years following Tulip Mania, prices of the most desirable varieties eventually returned to their pre-mania levels whilst lower quality, unknown and undesirable varieties never recovered. Those awaiting a healthy payment in the spring of 1637 were left empty-handed. We can't help but take some insight from Tulip Mania and the years that followed. And then the shift to iron ore…Are there parallels with iron ore from 2006 through to 2008? As the world economy continued to recover and grow after a significant disruption in the early 2000s, China began to emerge with significant expansion and an insatiable demand for iron ore to fuel a growing steel industry. Demand continued, main Australian players BHP (ASX: BHP) and Rio Tinto (ASX: RIO) were unable to meet demand, iron ore prices climbed, and new iron ore projects began to surface as they became economically feasible. Of these prospective projects, Fortescue Metals (ASX: FMG) is one that stood out due to its relative simplicity, infrastructure, sheer scale and cost-effectiveness. In 2008 the global financial crisis hit creating significant headwinds and undermining the stability of lenders and the availability of credit. Speculator confidence fell, as did equity prices and therefore miners' ability to raise capital through equity. Only those with strong, pre-existing backing were able to secure the necessary funding to continue their projects. With demand continuing to exceed supply Fortescue was able to complete its project and go on to profit immensely. The timing was everything. As you will see charted below, most projects, however, did not fare so well… Iron Ore (indexed from 1st January 2006)

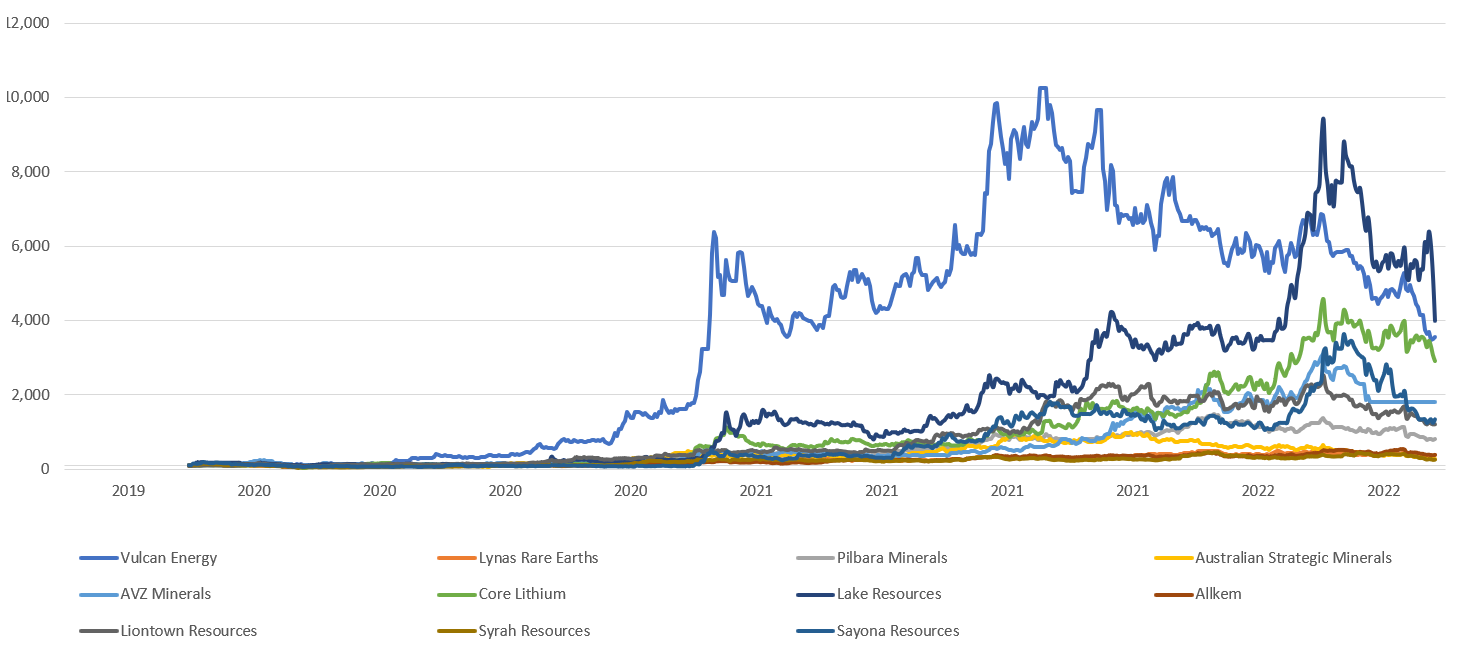

"They have dreamed out their dreams, and awaking have found nothing in their hands" Using January 2006 as an index base of 100, our iron ore aggregate of 11 stocks grows to a peak of 902 (average indexed value of all 11 stocks) by the end of May 2008. Murchison hit an indexed peak of 1340, Atlas 1457, and Fortescue 2167. During mid to late 2008 when the GFC hit, equity markets declined significantly, and debt markets froze. All these companies were in the early stages of their development. Even Fortescue which was in production by now fell using this index to a value of around 350. This still represents a more than 200% return for investors from the start of 2006 but also an 85% decline in 6 months. The timing of the takeout of Midwest could not have been better for Midwest shareholders. In late 2008 China implemented a massive infrastructure program to boost the economy in the wake of the GFC. This lifted our index to around 430 by the middle of 2011. The Atlas Iron share price also lifted significantly during this period. However, we remember well the differences between Fortescue and Atlas during this period. Atlas continued to contract mine the Wodgina iron ore deposit and truck ore to Port Hedland. The Wodgina deposit was never large nor high quality. The company was, however, able to generate significant short term cashflow by taking over the road, camp, and electricity infrastructure from the mothballed Wodgina tantalum mine and avoid heavy investment. Port facilities were also rented. Atlas was never able to repeat this outcome at another location. Infrastructure investment to lower operating costs was never forthcoming. Atlas was ultimately purchased by Hancock Prospecting in 2018 for approximately 1/100 of the peak share price (adjusted for share issues). Atlas, we believe, is a metaphor for the emerging iron ore sector from 2004 onward. Fortescue achieved profitable production with infrastructure and scale, paid down debt, and was then sustainably profitable enough to keep re-investing. It raised significant amounts of capital very early in the China boom when the markets were willing to provide it. Fortescue also got a large amount of infrastructure built before costs in Western Australia rocketed upward in the face of massive LNG investment post-GFC. Atlas and its peers could only make a profit when prices are high. They never managed to thread the needle to achieve lower costs and sustainable cash flow at scale. Fortescue was completely different. It had invested heavily in its own rail and port infrastructure and achieved significant economies of scale by investing the windfall profits it made during this period. It achieved scale economies that have stood the test of time and enabled it to generate the required cash flow to expand infrastructure and the number of mining provinces. It was also able to generate the required profits and free cash flows that allowed it to replace its initial contracted-out mining and crushing operations with its own mining truck fleet and crushing facilities. It now had the freedom to use its strong free cash flow to invest in further capital facilities that lowered its unit operating costs. Ultimately iron ore prices fell from their peaks and all the prospective (i.e. higher unit cost) junior miners either failed or returned to being producers at small volumes with barely sustainable profits. As the chart below highlights, they have all basically disappeared whilst Fortescue now has a market capitalisation of over $50bn. Global Iron ore supply, which was dominated by 3 very large producers prior to the China-led demand boom of 2006 onward, is now dominated by 4 including Fortescue. "A rising tide floats all ships, even the most unseaworthy" ...And finally to advanced materials.During 2021 and the first half of 2022 we have seen a significant rise and fall in the share price of companies with advanced materials mining projects. Early this year there was a sudden surge in the prices of several Australian listed companies that claim 'tier one' or 'world class' opportunities in the advanced materials mining space. This surge has also been associated with many of these companies being included in the S&P ASX 200 index for the first time. Most of these companies, however, have yet to mine a single ton of ore. Ironically it is these companies that have surged the most. EV manufacturers Tesla and Ford have recently engaged prospective lithium projects directly to set up off-take agreements in the hope of securing potential new supply before competitors - others are starting to follow their lead. When considering a potential investment in an advanced materials company, during the current boom we look for, among other factors, one key feature - whether the company is currently mining and processing ore. Like Fortescue in 2008, the heightened interest in advanced materials is now 3-4 years old. The boom is well underway. In the chart on page 5, of the 11 companies we've used, there are only 3 companies that mine, process ore and generate sales (Pilbara, Allkem and Lynas). The rest of the group claims to be at best 1-2 years away from producing any material from a variety of methods such as evaporation of lithium salts from ponds, rare earths as a by-product of mineral sands processing, open-pit mining, underground mining, and even processing of mud containing lithium. Each method has its own benefits and challenges impacting cost, reliability, and scalability. Post-concentration processing of rare earths in particular is very complex. Many projects are in politically very unstable jurisdictions and could face significant environmental, and modern slavery scrutiny from prospective clients. Large auto manufacturers are very protective of their brands and will not want child labour contributing to a hundred-thousand-dollar car. Irrespective of the method, most of the 11 companies are faced with the challenge of pre-production projects to commission infrastructure that will facilitate production. Under normal conditions, commissioning scalable operations is no easy feat and in our experience is rarely completed on budget or on time. In 2022, many companies are faced with labour shortages compounded by disrupted supply chains causing materials shortages and cost inflation. In a June 2022 update from Dacian Gold, we learned that their operating costs had increased 50% in the preceding months, a figure echoed by other gold producers, St Barbara and Evolution Mining. St Barbara highlighted that this issue is not just limited to Western Australia. Ignoring the challenge of securing necessary labour to carry out these projects, and the difficulty in securing materials and equipment, a 50% increase in costs is a significant challenge to proposed project plans and feasibility studies. In the current environment of cost inflation, subdued capital market conditions, and increasing interest rates, obtaining additional funding to meet project targets is likely to be increasingly difficult. These companies must endure winter before they can harvest in spring. We believe that conditions have now replicated the LNG and iron ore investment boom of 2006-2014; Woodside's Gorgon project was never supposed to cost US$40bn and Western Australia lollypop workers were not expected to receive multi-hundred thousand dollar pay packets. With a growing demand for renewable energy generation and storage, and electrified transport, demand for advanced materials has been increasing rapidly. A 3MW wind turbine (key to the renewable energy transition) requires roughly 2 tonnes of rare earth minerals for permanent magnets. In 2021, roughly 31,000 wind turbines were added (~94GW of energy generation) and this figure continues to accelerate. EVs are being ordered at an accelerating rate and require the same rare earth minerals and a significant portion of the global lithium supply. There is a significant deficit in the supply of these materials which is forecast to continue beyond 2030 according to recent research by Macquarie. We see this as a similar mix of factors and positive forecasts to the iron ore market 15 years ago. Yet most companies have disappeared! Despite significant optimism, the price of advanced materials and the enthusiasm of the equity market will likely go through cycles between now and 2030 making the funding and commissioning of new very long-term projects very difficult. The seaborne trade of iron ore is significantly bigger than it was 15 years ago, yet prices and trading conditions have varied significantly over this period. Almost all prospective iron ore hopefuls have gone. These high prices and strong outlook will also attract management and companies more interested in mining the share market as opposed to the ore market. It is often very difficult to know who-is-who before it is too late. Like Fortescue from 2008 onward we believe that 2 companies, Lynas Rare Earths and Pilbara Minerals in the advanced materials space in Australia have "threaded the needle" and have achieved a low unit cost, profitable, scalable position in rare earths and lithium respectively. Both are now generating significant cashflow and can fund ongoing refinements and growth in their operations. Lynas is funding a range of expansion projects in Australia and the US (with significant help from the US Government). Pilbara has just announced a new range of expansion plans including a plan to deploy some of their strong current free cashflow and replace their contracted-out mining and crushing operations with their own mining and crushing fleet. Sound familiar? Just like Atlas discovered, if you outsource all these processes, you are unlikely to make a profitable margin unless prices happen to remain very high after operations commence. We see unfinished projects as now having significant downside from cost overruns and delays in achieving production. We would also note that while we don't regard rare earth and lithium as "bulks" in the iron ore and coal sense and therefore don't require the same scale of rail and port infrastructure, they do present their own unique challenges. Rare Earths are very complex to separate. For example, the Lynas rare earths separation plant in Malaysia has 913 separate solvent extraction processes compared to a typical gold company that has 30-40. Hard rock lithium mining also has its share of difficulties. For one, a particularly hard ore body has its crushing and processing challenges. This is part of the reason why Pilbara chose to use a specialist contract crushing service provider to help derisk the initial commissioning of their new mine in 2018/19. Onsite lithium concentration is more difficult than drill, blast, and ship of iron ore. In most equity market and management presentations, the working capital required when mining commences is materially underestimated. Maintaining a workforce often for over a year whilst encountering operational issues and delivering poor-quality initial products is very expensive and consumes cash. Remember during this period any sales are likely to receive significant penalties for off-spec product. Our advanced materials chart below starts on January 1st, 2020 at a base of 100 and the aggregate of 11 companies hits 2599 at the end of March 2022. We note that this rally covers 821 days before peaking and the length of the rally for iron ore was roughly 880 days to the peak. Advanced Materials (Indexed January 1st 2020)

We see peak indexed values in March 2022 of 3500, 4000, 6000, and even over 9000 for individual companies. We would like to highlight the producing companies, Lynas, Pilbara, and Allkem are hidden as relatively flat lines at the base of the chart. From the late March peak, the advanced materials aggregate is down 40%. Lake resources is the worst hit with a 60% fall. We have used project risk as a key factor in selecting our lithium and rare earths investments. Pilbara Minerals and Lynas Rare Earths remain two of the most attractive options given their proven track record of profitable mining, processing and delivering ore in environments of far lower commodity prices. We see unfinished projects as adding significant downside risk to potential investments and employ lessons learned from iron ore companies 15 years ago. In line with Eiger's focus on companies' ability to generate long-term return, we value companies with proven track records of production as most likely to survive a difficult period and deliver returns. Author: Stephen Wood, Principal and Portfolio Manager, Nick Bucher, Analyst Funds operated by this manager: |

20 Jul 2022 - Uncovering value amid the market sell off

|

Uncovering value amid the market sell off Antipodes Partners Limited June 2022 Tech stocks have borne the brunt of the recent sell off in equity markets and with the Nasdaq firmly in bear market territory, it is unprofitable tech stocks that have been hit the hardest - down almost 60% this year. But amid these sell offs, there can be category leaders that fall to attractive valuations, relative to their long-term growth profile. Seagate Technology (NASDAQ: STX) is an example of this today. It's a beneficiary on the ongoing trend around data moving to the cloud as our lives become increasingly connected, and it's priced at just 8x next year's earnings. In this episode, Alison Savas hosts a deep dive into the company. Part one (2:20): Alison interviews Seagate Technology Executive Vice President and CFO, Gianluca Romano. |

|

Funds operated by this manager: Antipodes Asia Fund, Antipodes Global Fund, Antipodes Global Fund - Long Only (Class I) |

19 Jul 2022 - Performance Report: Quay Global Real Estate Fund (Unhedged)

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund will invest in a number of global listed real estate companies, groups or funds. The investment strategy is to make investments in real estate securities at a price that will deliver a real, after inflation, total return of 5% per annum (before costs and fees), inclusive of distributions over a longer-term period. The Investment Strategy is indifferent to the constraints of any index benchmarks and is relatively concentrated in its number of investments. The Fund is expected to own between 20 and 40 securities, and from time to time up to 20% of the portfolio maybe invested in cash. The Fund is $A un-hedged. |

| Manager Comments | The Quay Global Real Estate Fund (Unhedged) has a track record of 6 years and 6 months and has outperformed the BBAREIT Index since inception in January 2016, providing investors with an annualised return of 6.77% compared with the index's return of 6.17% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 6 years and 6 months since its inception. Over the past 12 months, the fund's largest drawdown was -17.02% vs the index's -12.08%, and since inception in January 2016 the fund's largest drawdown was -19.68% vs the index's maximum drawdown over the same period of -23.56%. The fund's maximum drawdown began in February 2020 and lasted 1 year and 4 months, reaching its lowest point during September 2020. The fund had completely recovered its losses by June 2021. The Manager has delivered these returns with 0.83% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.52 since inception. The fund has provided positive monthly returns 71% of the time in rising markets and 34% of the time during periods of market decline, contributing to an up-capture ratio since inception of 63% and a down-capture ratio of 66%. |

| More Information |

19 Jul 2022 - Performance Report: Cyan C3G Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Cyan C3G Fund is based on the investment philosophy which can be defined as a comprehensive, clear and considered process focused on delivering growth. These are identified through stringent filter criteria and a rigorous research process. The Manager uses a proprietary stock filter in order to eliminate a large proportion of investments due to both internal characteristics (such as gearing levels or cash flow) and external characteristics (such as exposure to commodity prices or customer concentration). Typically, the Fund looks for businesses that fit one or more of the following criteria: a) under researched, b) fundamentally undervalued, c) have a catalyst for re-rating. The Manager seeks to achieve this investment outcome by actively managing a portfolio of Australian listed securities. When the opportunity to invest in suitable securities cannot be found, the manager may reduce the level of equities exposure and accumulate a defensive cash position. Whilst it is the company's intention, there is no guarantee that any distributions or returns will be declared, or that if declared, the amount of any returns will remain constant or increase over time. The Fund does not invest in derivatives and does not use debt to leverage performance. However, companies in which the Fund invests may be leveraged. |

| Manager Comments | On a calendar year basis, the fund has only experienced a negative annual return once in the 7 years and 11 months since its inception. Over the past 12 months, the fund's largest drawdown was -25.47% vs the index's -23.88%, and since inception in August 2014 the fund's largest drawdown was -36.45% vs the index's maximum drawdown over the same period of -29.12%. The fund's maximum drawdown began in October 2019 and lasted 1 year and 4 months, reaching its lowest point during March 2020. The fund had completely recovered its losses by February 2021. The Manager has delivered these returns with 1.08% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.58 since inception. The fund has provided positive monthly returns 86% of the time in rising markets and 38% of the time during periods of market decline, contributing to an up-capture ratio since inception of 64% and a down-capture ratio of 65%. |

| More Information |

19 Jul 2022 - 'Small Talk' - cold, hard data on FY22

|

'Small Talk' - cold, hard data on FY22 Equitable Investors July 2022 We thought we would review the cold, hard data on the financial year 2022 that came to an end on June 30. The data tables paint a clear picture: companies priced on high multiples coming into the year faced a sobering reassessment of their valuations, as did unprofitable businesses; the only safe haven was the energy/commodities complex; small stocks were shunned by nervous investors, and the tech sector was particularly under pressure. The difference between high EV/EBITDA and low EV/EBITDA stocks in our "FIT" universe was the most stark - an 18% differential in price returns (where we split stocks into three baskets - low, middle and high). Five of the worst six performed stocks were in the Buy Now Pay Later (BNPL) space, led by merger partners Sezzle (SZL) and Zip Co (Z1P) in first and third. The best returns came from an eclectic mix: heart device company Anteris (AVR) and heavy equipment maintenance business Mader Group (MAD). Some of the less obvious takeaways from our "FIT" universe were that: it was not the case that the "dogs" of the prior year were the place to be - the "middle-of-the-road" stocks from FY21 held up best in FY22; and companies with market caps between $750m and $2 billion suffered notably worse declines than those capped under $100m. The wash-up from FY22 is that we are now seeing more attractive valuations AND the recapitalisation opportunities we have been highlighting are beginning to flow. For bottom-up investors like Equitable Investors, we believe the opportunity set will be as rich as it has been in many years and we are keen to engage with investors who want to be part of this "recap" opportunity through Dragonfly Fund.

Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Nothing in this blog constitutes investment advice - or advice in any other field. Neither the information, commentary or any opinion contained in this blog constitutes a solicitation or offer by Equitable Investors Pty Ltd (Equitable Investors) or its affiliates to buy or sell any securities or other financial instruments. Nor shall any such security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. The content of this blog should not be relied upon in making investment decisions.Any decisions based on information contained on this blog are the sole responsibility of the visitor. In exchange for using this blog, the visitor agree to indemnify Equitable Investors and hold Equitable Investors, its officers, directors, employees, affiliates, agents, licensors and suppliers harmless against any and all claims, losses, liability, costs and expenses (including but not limited to legal fees) arising from your use of this blog, from your violation of these Terms or from any decisions that the visitor makes based on such information. This blog is for information purposes only and is not intended to be relied upon as a forecast, research or investment advice. The information on this blog does not constitute a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Although this material is based upon information that Equitable Investors considers reliable and endeavours to keep current, Equitable Investors does not assure that this material is accurate, current or complete, and it should not be relied upon as such. Any opinions expressed on this blog may change as subsequent conditions vary. Equitable Investors does not warrant, either expressly or implied, the accuracy or completeness of the information, text, graphics, links or other items contained on this blog and does not warrant that the functions contained in this blog will be uninterrupted or error-free, that defects will be corrected, or that the blog will be free of viruses or other harmful components.Equitable Investors expressly disclaims all liability for errors and omissions in the materials on this blog and for the use or interpretation by others of information contained on the blog |

18 Jul 2022 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

||||||||||||||||||

| Ausbil Active Sustainable Equity Fund | ||||||||||||||||||

|

||||||||||||||||||

|

Ausbil Active Dividend Income Fund |

||||||||||||||||||

|

||||||||||||||||||

|

Ausbil Australian Concentrated Equity Fund |

||||||||||||||||||

|

||||||||||||||||||

|

Ausbil Australian SmallCap Fund |

||||||||||||||||||

|

||||||||||||||||||

| View Profile | ||||||||||||||||||

|

Ausbil Global Essential Infrastructure Fund (Unhedged) |

||||||||||||||||||

|

||||||||||||||||||

| View Profile | ||||||||||||||||||

|

Ausbil Global Resources Fund |

||||||||||||||||||

|

||||||||||||||||||

| View Profile | ||||||||||||||||||

|

Ausbil Long Short Focus Fund |

||||||||||||||||||

|

||||||||||||||||||

| View Profile | ||||||||||||||||||

|

MacKay Shields Multi-Sector Bond Fund |

||||||||||||||||||

|

||||||||||||||||||

| View Profile | ||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||

|

Subscribe for full access to these funds and over 650 others |

18 Jul 2022 - Manager Insights | Cyan Investment Management

|

|

||

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Dean Fergie, Director & Portfolio Manager at Cyan Investment Management. The Cyan C3G Fund has a track record of 7 years and 11 months and has outperformed the ASX Small Ordinaries Total Return Index since inception in August 2014, providing investors with an annualised return of 10.52% compared with the index's return of 5.26% over the same period.

|

18 Jul 2022 - Compelling Opportunity for Investors: Improving Convexity, Yet Benign Default Risk

|

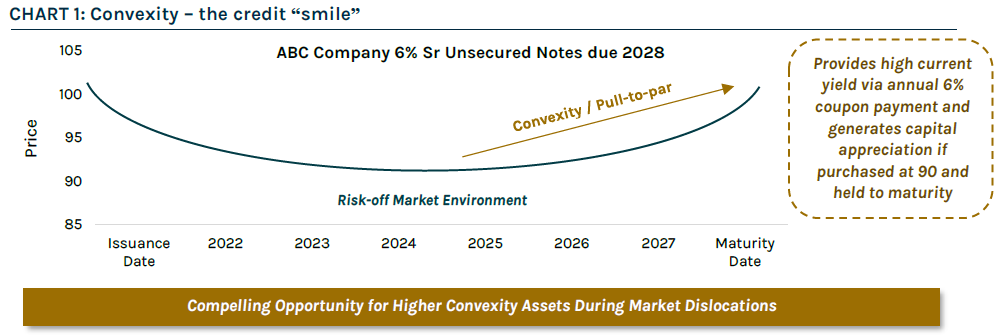

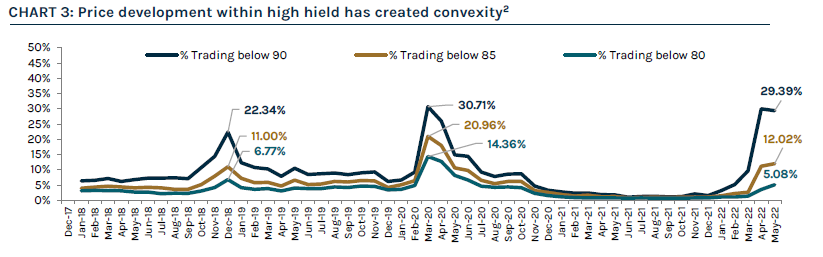

Compelling Opportunity for Investors: Improving Convexity, Yet Benign Default Risk (Adviser & Wholesale Investors Only) Ares Australia Management 28 June 2022 What is Convexity & Why Is It Important? When credit instruments sell off, market participants will often talk about convexity being back. So, what is it?

During a risk-off environment, the price of a credit instrument typically drops below its nominal value (also referred to as "face" or "par" value) due to perceived increased default risk. As illustrated by the example in Chart 1 below, there is a compelling investment opportunity when a bond trades at a discount to its nominal value - assuming the bond does not default, a bond's price will benefit from a natural "pull" to the nominal value as it approaches maturity. This movement is referred to as "pull-to-par". Typically, bonds and loans that trade at a discount have positive convexity, offering investors enhanced yield and capital appreciation potential without taking excess risk.

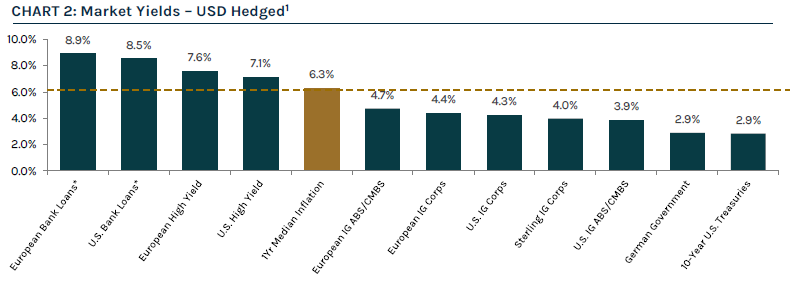

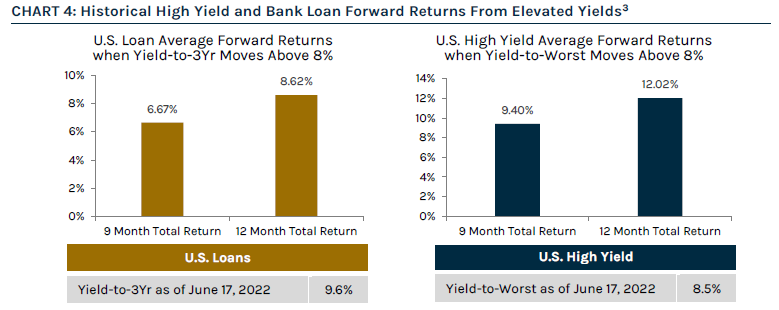

Market Opportunity - Convexity & Higher Yields Calendar year 2022 has presented significant turmoil for global financial markets amid a risk-off environment and sustained macro uncertainty. Global inflationary pressures continue to persist, including the ongoing war in Ukraine, slowing growth, higher energy prices and supply-chain disruptions. Central banks face substantial challenges as they look to combat elevated inflation with interest rate hikes, but without triggering a recession. Against the backdrop of wider spreads and the sell-off in rates over the past few months, fixed income yields have reset to higher levels, presenting an attractive opportunity for yield-focused investors. Global leveraged credit assets are providing a meaningful pickup in real yields when compared to traditional fixed income markets, as illustrated in Chart 2. Higher yields and a decline in asset prices have introduced greater upside convexity in leveraged credit This combination of higher yields and cheaper prices in an environment where bouts of volatility have become shorter and more frequent, is presenting alpha generating opportunities for active managers. History suggests investing in periods of dislocation, when yields reach current levels, provides attractive forward returns in the high yield bond and bank loan markets.

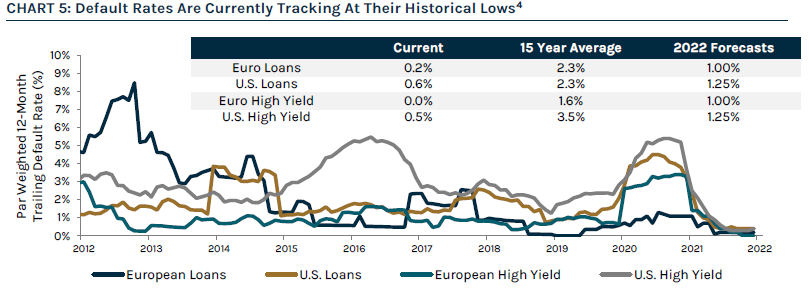

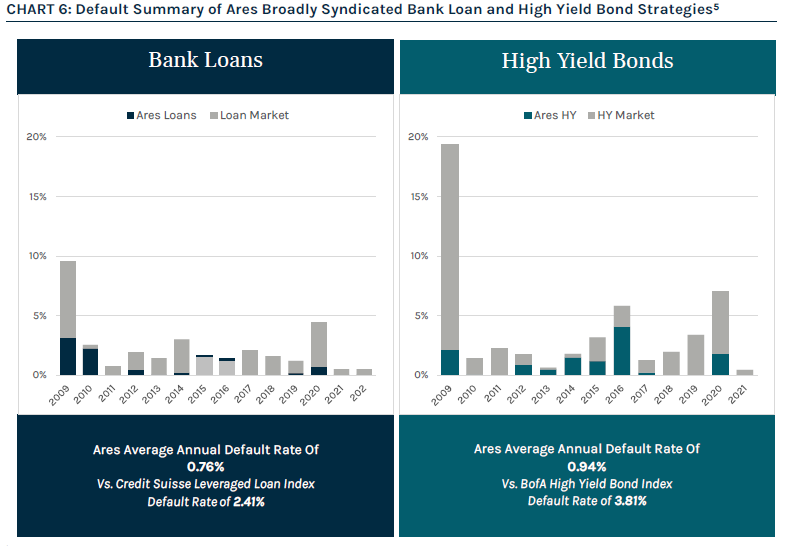

Market Outlook Looking forward, we expect volatility to persist with the potential for asset coverage leakage and an uneven recovery across markets. We believe credit spreads are currently at levels that represent attractive entry points, but tail risks have increased, and we anticipate elevated credit dispersion as well as rising idiosyncratic credit events driven by a host of conflicting themes. We believe Ares is well positioned to provide superior credit selection and vigilant risk management in today's volatile market due to our disciplined investment process that focuses on capital preservation, predicated on bottom-up fundamental research with the goal of minimizing default risk by identifying and avoiding marginal quality credit. This core tenet of Ares' investment philosophy has resulted in significantly lower defaults in its bank loan and high yield bond strategies, particularly in periods of dislocation. In summary, as investors are faced with rising rates and elevated inflation, many may struggle to determine how best to position their credit exposure in an effort to maximize yield and mitigate risk. At Ares, our differentiated approach to capitalizing on the best risk-adjusted return opportunities across the investable universe is rooted in the scale and integration of our Global Liquid and Alternative Credit strategies, which allows us to fully leverage extensive research and origination capabilities, proprietary technologies and longstanding relationships. Written By Teiki Benveniste, Head of Ares Australia Management |

|

Funds operated by this manager: Ares Diversified Credit Fund, Ares Global Credit Income Fund |

15 Jul 2022 - Hedge Clippings |15 July 2022

|

|

|

|

Hedge Clippings | Friday, 15 July 2022 Australian unemployment at 3.5% - the lowest since 1974. US consumer inflation at 9.1% year on year - the highest since 1981. Chinese GDP growth -2.6% for the quarter. Canadian interest rates up by 1%. A resurgence of COVID, with over 47,000 cases in the last 24 hours, and over 300,000 active cases at a time when half the population of NSW have been staying indoors due to yet more rain. News & Insights New Funds on FundMonitors.com Cyan Investment Management | Manager Insights Video 'Small Talk' - cold, hard data on FY22 | Equitable Investors Enduring the downturn | Cyan Investment Management |

|

|

June 2022 Performance News Bennelong Twenty20 Australian Equities Fund Quay Global Real Estate Fund (Unhedged) |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|