NEWS

29 Aug 2022 - Global equities strengthen

|

Global equities strengthen Glenmore Asset Management August 2022 After a very challenging finish to FY22, July was a strong month for equities globally. In the US, the S&P 500 rose +9.1%, the Nasdaq was up +12.4%, whilst in the UK, the FTSE was more muted, rising +3.5%. Domestically, the ASX All Ordinaries Accumulation Index rose +6.3%. The top performing sectors on the ASX were technology (assisted by falling bond yields), whilst resources were the worst performer, driven by weaker commodity prices. Unsurprisingly, small caps outperformed large caps as investor risk appetite materially improved. In our view the key driver of the rally in July was investor expectations around inflation (and hence interest rate hikes) beginning to moderate as commodity prices eased, and with central banks now well underway with raising rates, investors potentially can see some light at the end of the tunnel with regards to the current restrictive monetary policy. During the month, the Federal Reserve (US central bank) increased the Fed Funds Rate by 75 basis points (bp) to a range of 2.25% - 2.50%, whilst the RBA increased the cash rate by 50bp to 1.35%. Whilst these are quite material increases, they were largely expected by investors, with consensus that there will be more such hikes over the course of 2022. Commodity prices were broadly weaker in July, driven by fears around an economic slowdown, particularly in China. Iron ore, crude oil and copper all fell -4%, whilst gold declined -2%. Thermal coal outperformed, rising +6%. In the bond market, notably the key US 10 year bond yield fell -36 basis points (bp) to close at 2.70%, whilst the Australian 10 year bond yield fell 60 bp to close at 3.1%. The movements of both in July were a function of some early signs that inflationary pressures have started to ease. Some key themes we will be monitoring are cost pressures and how companies are dealing with them, as well as any impact on demand and/or revenue from recent central bank interest rate increases. As has been the case in the previous years, we are optimistic that reporting season can provide some excellent new investment ideas. Funds operated by this manager: |

29 Aug 2022 - 'Small Talk' - Where have all the IPOs gone?

|

'Small Talk' - Where have all the IPOs gone? Equitable Investors August 2022 In this Small Talk update, we show a chart which highlights IPO activity...or lack of it. IPOs in Australasia are down 88% so far in calendar 2022, relative to the same point in time in 2021, as measured in US dollars raised. That's slightly worse than the global decline of 74%, as per data from Dealogic. The ASX's current list of upcoming IPOs features 10 with an expected listing date, of which only one is not a miner/explorer. Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Nothing in this blog constitutes investment advice - or advice in any other field. Neither the information, commentary or any opinion contained in this blog constitutes a solicitation or offer by Equitable Investors Pty Ltd (Equitable Investors) or its affiliates to buy or sell any securities or other financial instruments. Nor shall any such security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. The content of this blog should not be relied upon in making investment decisions.Any decisions based on information contained on this blog are the sole responsibility of the visitor. In exchange for using this blog, the visitor agree to indemnify Equitable Investors and hold Equitable Investors, its officers, directors, employees, affiliates, agents, licensors and suppliers harmless against any and all claims, losses, liability, costs and expenses (including but not limited to legal fees) arising from your use of this blog, from your violation of these Terms or from any decisions that the visitor makes based on such information. This blog is for information purposes only and is not intended to be relied upon as a forecast, research or investment advice. The information on this blog does not constitute a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Although this material is based upon information that Equitable Investors considers reliable and endeavours to keep current, Equitable Investors does not assure that this material is accurate, current or complete, and it should not be relied upon as such. Any opinions expressed on this blog may change as subsequent conditions vary. Equitable Investors does not warrant, either expressly or implied, the accuracy or completeness of the information, text, graphics, links or other items contained on this blog and does not warrant that the functions contained in this blog will be uninterrupted or error-free, that defects will be corrected, or that the blog will be free of viruses or other harmful components.Equitable Investors expressly disclaims all liability for errors and omissions in the materials on this blog and for the use or interpretation by others of information contained on the blog |

26 Aug 2022 - Hedge Clippings |26 August 2022

|

|

|

|

Hedge Clippings | Friday, 26 August 2022 Newly minted Treasurer Dr. Jim Chalmers set the proverbial cat amongst the superfund pigeons this week by proposing that an (unspecified) portion of all super balances should be invested in "national priorities" - areas like "housing and energy". To ensure his point was made, he was supported by Paul Keating, the self styled grandfather and co-creator of Australia's compulsory superannuation system. Hedge Clippings can see some merit and logic in this - in fact we have previously proposed that given super's long-term investment timeframe of up to 45 years or more, and the long-term investment needs and nature of infrastructure, the $3.4 trillion in super (forecast to grow to over $9 trillion by 2040, and $34 trillion by 2061) makes an ideal source of capital. Added to that, infrastructure as an asset has the attractive investment characteristics of steady long term income and growth, and in Australia at least, a stable political environment. Whilst slightly out of date (actually we couldn't find any date on the report, except at that stage the total in super was a mere $1.7 trillion) this report by the Financial Services Council and EY considered the issue in detail. However, the difficulty, as pointed out by a number of super funds and their trustees, is that they're responsible for returns, not national priorities such as housing and energy. This argument falls down of course when one considers the emphasis on the ESG credentials of many funds, and the fact that they're the beneficiaries of a government legislated stream of fees akin to Norman Lindsay's Magic Pudding. Chalmers will argue, with some justification, that given the government's role in supplying the pudding's recipe, plus its generous (but complex and changeable) tax concessions ingredients, that they're entitled to stipulate how and where it is invested. Up to a point Lord Copper, as Mr. Salter would say. The danger of giving politicians of the day the power to direct which "national priorities" are important is obvious. One would imagine Scomo's priorities for instance might be somewhat different to someone (probably anyone) else's. Moving on. Last week we noted that a strategy paper delivered at the Portfolio Construction Forum (PCF) by Marko Papic put forward the view that President Xi would not invade Taiwan as it would cause China itself too much damage - political, military, economic and social. One alert reader of Hedge Clippings (thank you!) pointed out that the same Marko Papic had apparently prepared a similar presentation for the February PCF, espousing the view that Putin would not invade Ukraine as it would cause Russia itself too much damage - political, military, economic and social. Needless to say, as the Russians invaded Ukraine on 24th February, and the PCF was held on the 25th, we understand there was some deft adjustment to the agenda. This time around we hope his thesis is correct, but hope, as they say, is not a reliable strategy. Which brings us to anniversaries: As above, his week the war in Ukraine passed the six month mark, when most - but particularly Putin - thought his "military exercise" would be over in weeks. Sadly, next week also brings up the 25th anniversary of the death of Diane, Princess of Wales. But on a happier note, (for those old enough to remember) August 24th was the 50th anniversary of one of the greatest rock concerts of all time - Neil Diamond's "Hot August Night" held at the Greek Theatre in Los Angeles. The resulting live recording was made into a double album running over an hour and a half. Here's a link to Crunchy Granola for old time's sake. It must be the cry of generations: Oh! for the days when music was music! News & Insights New Funds on FundMonitors.com 10k Words | Equitable Investors Tequila strategy pays off for Diageo | Magellan Asset Management Investment Perspectives: 12 charts we're thinking about right now | Quay Global Investors |

|

|

July 2022 Performance News Equitable Investors Dragonfly Fund Bennelong Kardinia Absolute Return Fund Bennelong Twenty20 Australian Equities Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

26 Aug 2022 - Could the US Supreme Court's decision against the EPA derail decarbonisation efforts?

|

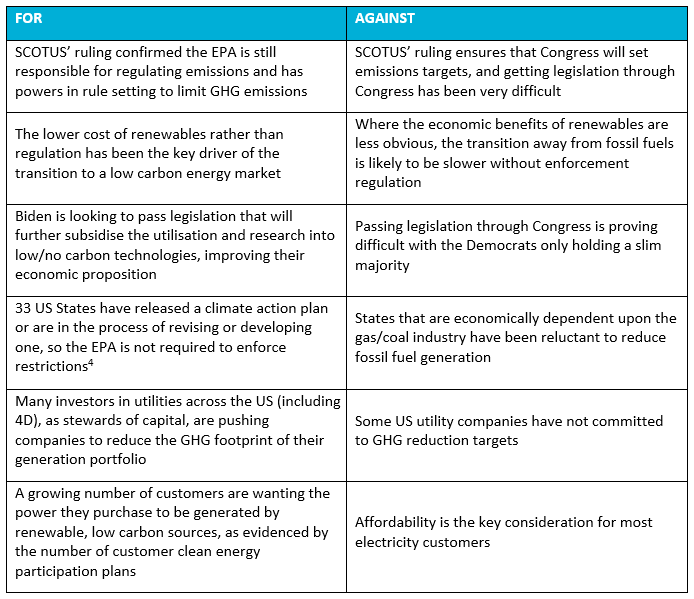

Could the US Supreme Court's decision against the EPA derail decarbonisation efforts? 4D Infrastructure August 2022 On 30 June 2022, the Supreme Court of the United States (SCOTUS) ruled in favour of West Virginia and a group of other states in their lawsuit against the Environmental Protection Agency (EPA), potentially limiting the agency's ability to enforce actions to limit greenhouse gas (GHG) emissions.

In a majority vote of 6-3, where all six conservative judges sided against the EPA, SCOTUS ruled that the agency overstepped its authority and required 'clear congressional authorisation' to enforce switching from fossil fuel generation to low/no carbon energy. Until now, the EPA had relied on powers provided under the Clean Air Act (1970) in regulating and restricting certain types and volumes of GHG emissions from fossil fuel generation facilities. In this article, we consider what this ruling means for decarbonisation efforts in the US, and for us as global infrastructure investors. Ramifications of the rulingIn its ruling, SCOTUS relied on the 'major questions' doctrine; an academic term the Court used in a ruling for the first time. The doctrine allows judges to strike down regulations or agency actions that 'address questions of vast economic or political significance' without explicit authorisation from Congress[1]. The ruling raises legal questions about the ongoing authority and powers available to the EPA in regulating emissions, and, specifically, what constitutes 'major' - in short increasing legal uncertainty[2]. Some observers have questioned whether the US' commitments to decarbonisation, and specifically the Paris Agreement, can be achieved with the current uncertainty around the EPA's ability to enforce emissions reductions. And if the US is unlikely to achieve its commitments to the Paris Agreement, does that put global efforts to achieve net-zero and limit global temperature increases to well below two degrees Celsius at risk?[3] Does this impede the US' Paris Agreement commitments?Under President Biden, the US made commitments to achieve net-zero by 2050, and reduce GHG by 50% to 52% below 2005 levels by 2030. In light of the SCOTUS ruling, arguments for and against the US' ability to achieve these targets are summarised in the table below.

4D's internal viewThere's no doubt SCOTUS' decision raises questions as to the EPA's ongoing effectiveness in enforcing emissions reductions. This could see some fossil fuel generation facilities, which would otherwise be decommissioned or retrofitted with technology to reduce emissions (such as carbon capture), continue to operate and emit GHGs for longer. This is more likely in states that are economically dependent on the fossil fuel industry. Importantly, however, the US' interim 2030 commitment under the Paris Agreement is more dependent upon the economic benefit argument in transitioning coal generation to renewables, combined with batteries and/or peaking natural gas generation. These economic benefits are supported by technological improvement in low/no carbon technologies and tax subsidies which are currently in place. Biden has communicated the ambition to improve and/or extend these subsidies as part of proposed legislation, which will improve the economics of the transition. Either on their own, or because of investor activism, most US utilities have set GHG reduction targets for 2030 that are in-line with, or more aggressive than, the US' economy wide targets. This improves our confidence that despite SCOTUS' ruling, the US can still achieve its interim commitment under the Paris Agreement. Net-zero still provides a real, long-term investment opportunityWhile the speed of ultimate decarbonisation may remain unclear, as infrastructure investors, we continue to see a real opportunity for multi-decade investment as every country moves towards a cleaner environment. At 4D, sustainability assessments have always played a key role in our investment process. As such, we continue to favour those companies that have been forward-thinking and are capitalising on the decarbonisation opportunity while generating attractive returns for investors. In the US, this includes American Electric Power and NextEra Energy; both of which are investing heavily in energy transition and will unlikely be derailed by the recent SCOTUS decision. |

|

Funds operated by this manager: 4D Global Infrastructure Fund, 4D Emerging Markets Infrastructure FundThe content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. |

25 Aug 2022 - Performance Report: Collins St Value Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The managers of the fund intend to maintain a concentrated portfolio of investments in ASX listed companies that they have investigated and consider to be undervalued. They will assess the attractiveness of potential investments using a number of common industry based measures, a proprietary in-house model and by speaking with management, industry experts and competitors. Once the managers form a view that an investment offers sufficient upside potential relative to the downside risk, the fund will seek to make an investment. If no appropriate investment can be identified the managers are prepared to hold cash and wait for the right opportunities to present themselves. |

| Manager Comments | The Collins St Value Fund has a track record of 6 years and 6 months and has outperformed the ASX 200 Total Return Index since inception in February 2016, providing investors with an annualised return of 16.78% compared with the index's return of 9.42% over the same period. On a calendar year basis, the fund hasn't experienced any negative annual returns in the 6 years and 6 months since its inception. Over the past 12 months, the fund's largest drawdown was -11.41% vs the index's -11.9%, and since inception in February 2016 the fund's largest drawdown was -27.46% vs the index's maximum drawdown over the same period of -26.75%. The fund's maximum drawdown began in February 2020 and lasted 7 months, reaching its lowest point during March 2020. The fund had completely recovered its losses by September 2020. The Manager has delivered these returns with 3.34% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 three times over the past five years and which currently sits at 0.92 since inception. The fund has provided positive monthly returns 84% of the time in rising markets and 63% of the time during periods of market decline, contributing to an up-capture ratio since inception of 79% and a down-capture ratio of 42%. |

| More Information |

25 Aug 2022 - Equities responding to a higher rate environment

|

Equities responding to a higher rate environment Eley Griffiths Group August 2022 Global equity markets (ex-China) rebounded strongly in July. The Small Ordinaries Accumulation Index rallied +11.4% over the month, a significant outperformance against large caps which gained +5.5%. There was early indication that bad news is now being discounted into stock prices. Markets pushed higher despite the US CPI report for June the highest print in 41 years, 9.1% year on year compared to the 8.8% estimate. Equities took the number in its stride failing to extinguish the "risk on" sentiment. As predicted, The Federal Reserve (Fed) raised rates by 75bp in response and whilst Fed Chair Powell's broader messaging didn't overly change, comments that the US economy may be showing signs of slowing were less hawkish than expected. The war on inflation is being won. The market responded by pricing in a lower peak Federal Funds rate and increasing the likelihood that rates may be eased in 2023 reflecting the impact higher rates will have the on real economy. Locally, the Reserve Bank of Australia delivered +50bps after the Q2 CPI came in at 6.1% YoY, the highest since 1990. Once more, equity markets responded positively to the dovish post-meeting statements, "we don't need to return inflation to target immediately… we are seeking to do this in a way in which the economy continues to grow, and unemployment remains low" (Australian Strategic Business Forum, 20 July 2022 Governor Lowe). Outside non-gold resource names and agricultural stocks, the upswing was sectorally broad based. Standing out were those most beaten-up by inflation and central bank rate hike fears, namely Information Technology (+18%) and Financials (+15%). Focus now turns to the August corporate earnings results and whether investors have been heavy handed in their treatment of stocks. The lead from the US 2Q reporting season has been adequate. Attention will be trained on the impacts of inflation on operating cost structures, a higher rate environment and the health of the consumer. Funds operated by this manager: Eley Griffiths Emerging Companies Fund, Eley Griffiths Small Companies Fund |

24 Aug 2022 - Performance Report: Equitable Investors Dragonfly Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund is an open ended, unlisted unit trust investing predominantly in ASX listed companies. Hybrid, debt & unlisted investments are also considered. The Fund is focused on investing in growing or strategic businesses and generating returns that, to the extent possible, are less dependent on the direction of the broader sharemarket. The Fund may at times change its cash weighting or utilise exchange traded products to manage market risk. Investments will primarily be made in micro-to-mid cap companies listed on the ASX. Larger listed businesses will also be considered for investment but are not expected to meet the manager's investment criteria as regularly as smaller peers. |

| Manager Comments | Equitable noted positive price action in the shares of home security tech company Scout Security (SCT) was reflective of a general bounce back for illiquid micro-caps that appeared to have suffered from tax loss selling in May and June. Marine propulsion and stabilisation systems maker Veem (VEE) was another to recover with the beginning of a new financial year. On the flip-side, Equitable's holding in NZ-listed trades app developer Geo (GEO:NZ) fell 9% in NZ dollars after cornerstone investor North Ridge Partners distributed some equity in GEO held by its Co-Investor No. 3 PIPE Fund to the underlying investors, as part of the end-of-life wind-up of that fund. Equitable see continuing opportunities both of the transactional variety (recapitalisations etc) and simply of the attractive pricing variety. They noted that while there has been a bounce back in illiquid stocks in July, that recovery hasn't been as broad-based as they might have imagined, with speculative money having another swing at questionable business models in the Buy Now Pay Later (BNPL) space and 'meme' stocks, leaving shares in a company like expense management software company 8Common (8CO) fractionally lower at the end of July than it was at the end of June. |

| More Information |

24 Aug 2022 - The outlook for equities is unclear

|

The outlook for equities is unclear Airlie Funds Management July 2022 |

|

The outlook for equities is incredibly unclear. We have talked prior that markets are at the crossroads after a +10-year bull market - inflation and interest rates are on the rise and so central banks are reversing course after a decade plus of super easy policies. The early result of this, and exacerbated by the Ukraine invasion, is a return of market volatility. After being super strong in the March quarter, even commodity prices are now weakening, putting further pressure on the Aussie market. As fabled investor Peter Lynch says - "If you can only follow one piece of data - follow the earnings...". Given profit margins overall are at record highs; stimulus is unwinding; costs pressures abound; and consumers will likely have less disposable income - then an easy bear case for the direction of earnings can be outlined. PORTFOLIO POSITIONING

As bottom-up stock-pickers, we invest on company fundamentals: seeking conservative balance sheets, businesses that generate good returns and are managed by competent people. However, from a top-down perspective we want to avoid "unintended bets"; i.e., positioning the portfolio in a way that leaves it vulnerable to certain macro events playing out. The key macro event to watch this year is inflation. There is no doubt in the near term that inflation will continue to increase: most of the companies we speak to are seeing significant input cost (and increasingly labour) inflation, and have signalled their intent to pass this on in the form of higher prices. Since we think inflation is heading up in the near-term, it's important to make sure our portfolio owns businesses with pricing power, that can protect margins and pass on higher costs to end consumers. We have analysed our portfolio through this lens and think we are well positioned. Businesses like James Hardie, Woolworths, Wesfarmers, Macquarie, the banks, Aristocrat and CSL should all benefit from (or at least not suffer from) higher inflation. The market has been quick to reprice those businesses whose valuations had benefited from the "lower-for-longer" interest rate tailwind of the last decade, chiefly high PE structural growth stories, loss-making tech companies and REITs. We believe there are additional nuances to consider. We are avoiding businesses with high ongoing capex needs, as inflation makes it more expensive to stand still, and businesses with material exposure to floating-rate debt. Meanwhile, we spend our time sifting through the wreckage of heavily sold-off companies for opportunities where good businesses have been mispriced with respect to stock selection for the portfolio, we weigh four factors when considering an investment: Financial strength: We want to own businesses with conservative levels of gearing and strong cash flows. While corporate balance sheets are in great shape across the board, with average net debt to EBITDA for ASX200 companies of 1.8x (well below the 10-year median of 2.5x), our portfolio has an average net debt to EBITDA of 0.3x. Further, 38% of our portfolio companies are in fact net cash. We believe this sets us up for strong future returns, whether through dividends, special dividends, buybacks, investment or acquisitions. Management quality: We look for alignment with shareholders, whether that be through significant management shareholdings, or appropriate long-term incentives. The ultimate model of alignment for us is owner- managed businesses, where the original founder remains in control. We believe these businesses tend to outperform over the long term, and owner-managed businesses comprise c30% of our portfolio, compared to 10% of the ASX200. Valuation: We believe the returns a business generates drive the value of the business, and seek to invest where the above factors are underappreciated in the prevailing market share price. Funds operated by this manager: Important Information: Units in the fund(s) referred to herein are issued by Magellan Asset Management Limited (ABN 31 120 593 946, AFS Licence No. 304 301) trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks.. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

23 Aug 2022 - Performance Report: Cyan C3G Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Cyan C3G Fund is based on the investment philosophy which can be defined as a comprehensive, clear and considered process focused on delivering growth. These are identified through stringent filter criteria and a rigorous research process. The Manager uses a proprietary stock filter in order to eliminate a large proportion of investments due to both internal characteristics (such as gearing levels or cash flow) and external characteristics (such as exposure to commodity prices or customer concentration). Typically, the Fund looks for businesses that fit one or more of the following criteria: a) under researched, b) fundamentally undervalued, c) have a catalyst for re-rating. The Manager seeks to achieve this investment outcome by actively managing a portfolio of Australian listed securities. When the opportunity to invest in suitable securities cannot be found, the manager may reduce the level of equities exposure and accumulate a defensive cash position. Whilst it is the company's intention, there is no guarantee that any distributions or returns will be declared, or that if declared, the amount of any returns will remain constant or increase over time. The Fund does not invest in derivatives and does not use debt to leverage performance. However, companies in which the Fund invests may be leveraged. |

| Manager Comments | The Cyan C3G Fund has a track record of 8 years and has outperformed the ASX Small Ordinaries Total Return Index since inception in August 2014, providing investors with an annualised return of 11.96% compared with the index's return of 6.64% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 8 years since its inception. Over the past 12 months, the fund's largest drawdown was -25.43% vs the index's -23.88%, and since inception in August 2014 the fund's largest drawdown was -36.45% vs the index's maximum drawdown over the same period of -29.12%. The fund's maximum drawdown began in October 2019 and lasted 1 year and 4 months, reaching its lowest point during March 2020. The fund had completely recovered its losses by February 2021. The Manager has delivered these returns with 1.03% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.64 since inception. The fund has provided positive monthly returns 86% of the time in rising markets and 38% of the time during periods of market decline, contributing to an up-capture ratio since inception of 65% and a down-capture ratio of 65%. |

| More Information |

23 Aug 2022 - Are the businesses enjoying stock price rises today also the winners of tomorrow?

|

Are the businesses enjoying stock price rises today also the winners of tomorrow? Insync Fund Managers July 2022 Lately we are all experiencing one tectonic event after the next. Foundations of the political and economic framework that have dominated much of the world since the 1980s are now being challenged; the impacts on globalisation, the questioning of the USD central role, and previously deeply embedded structural relationships in the energy markets to name a few. Our approach is far less dependent than our peers are on these issues, including inflation and interest rates. The jury is still out on whether inflation will be a temporary or a longer-term phenomenon. Covid and the tragic invasion of Ukraine have created significant commodity, energy, and labour mobility pressures. Companies that:

These are the required factors for a business to continue delivering healthy returns in real terms and are thus the same attributes Insync seeks. Most companies are not able to do this. Those companies possessing the most levers to pull going into an inflationary period are also the most likely to protect and even thrive for their investors. There will likely be tougher times ahead, quality growth investors should find themselves better positioned than most to weather the storm and come out substantially ahead. Why earnings power is crucial A shy, humble investor living on a suburban street in a small mid-western US city is often cited for his quips. "In the short-term markets are a voting machine. In the long-term it's a weighing machine" Over shorter periods sentiment in markets can shift wildly depending on the narrative of the day. This is driven by perceptions of investors trying to gauge where we are in the economic cycle, the path of inflation and interest rates, the impact of a geopolitical crisis, and what style of investing will be best equipped for the future. These are impossible to predict with any degree of certainty or to do so consistently. The one thing that is more certain over time is that in the long-term, share prices follow the consistent growth in the earnings of a business. We know that the most profitable companies remain profitable even ten years later fuelled by the enduring, large megatrends. Megatrends are so predictable you can set your watch by them. This is whether it is the rising importance of the Gen Z'ers, the acceleration in the number of people aged 70+, GDP+ growth in spending on skin and beauty, or the insatiable desire to spend on experiences. A portfolio of the most profitable companies tied to megatrends provides consistency in earnings leading to strong stock price returns. They are also mostly impervious to interest rate settings, the state of the economy or current commodity prices. 3 portfolio examples of why Earnings Growth is good for investors The evidence shows it all. Here are 3 companies in our portfolio. The coloured line in each graph is the path of earnings over the past 10 years. The white line is the share price performance. Observe the strong correlation between the earnings growth and share price performance. From time to time the two lines deviate based on an 'event', as is the case now. Obviously, present prices present an outstanding opportunity to invest.

These highly profitable businesses benefitting from Insync's identified megatrends have become even more attractive due to recent price falls. This is because their ongoing and established earnings power remains intact. Such excellent buying opportunities do not often present themselves. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |