NEWS

10k Words | November 2024

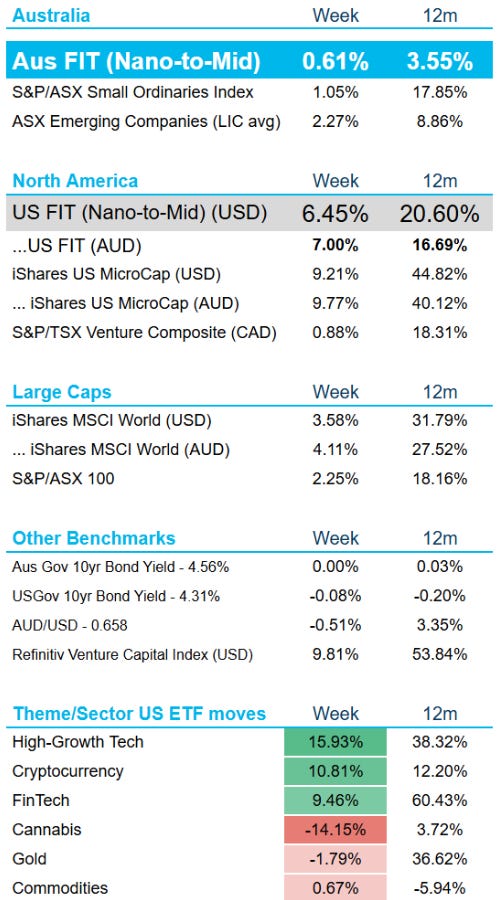

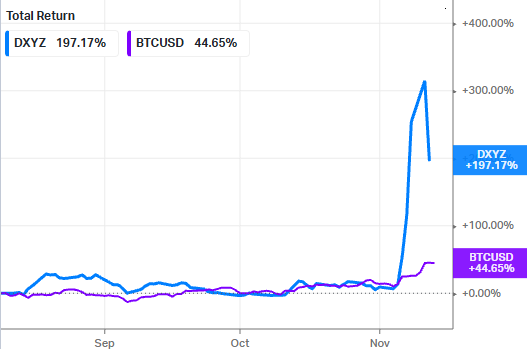

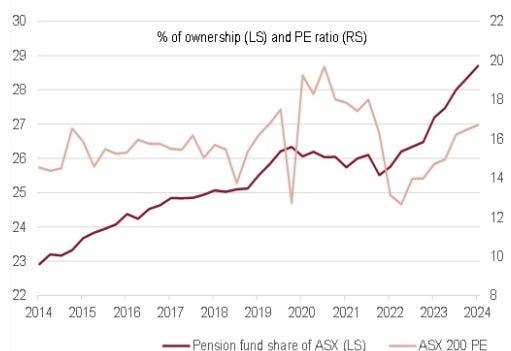

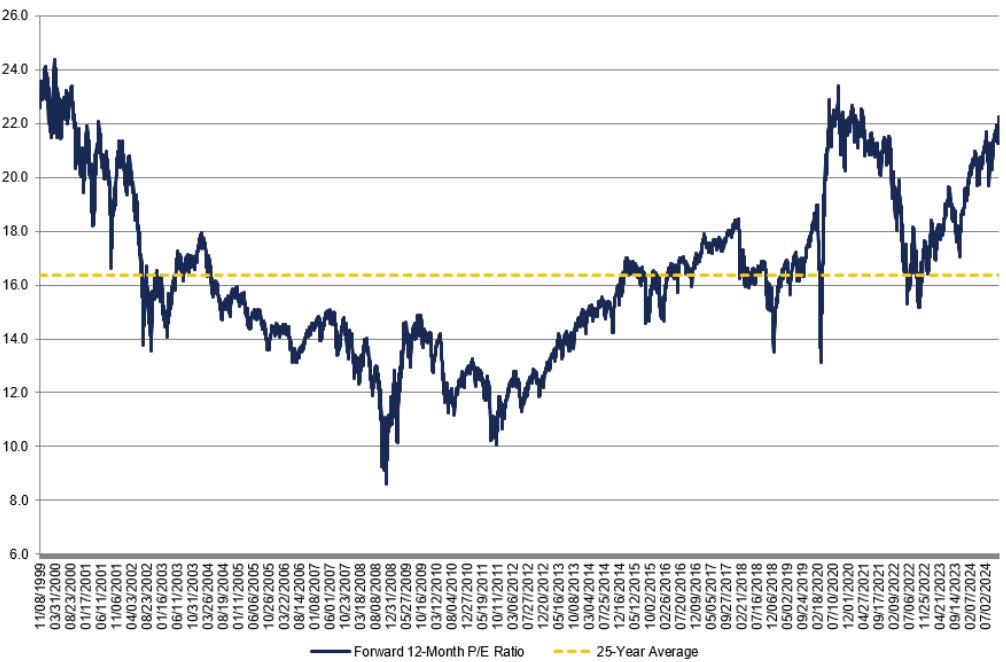

The "Trump Bump" in full effect, with bitcoin not the greatest benficiary and fund managers allocating away from equities beforehand; the "Super Bump" in Australian equities, as evident in the P/E multiple of CBA.

Read more...

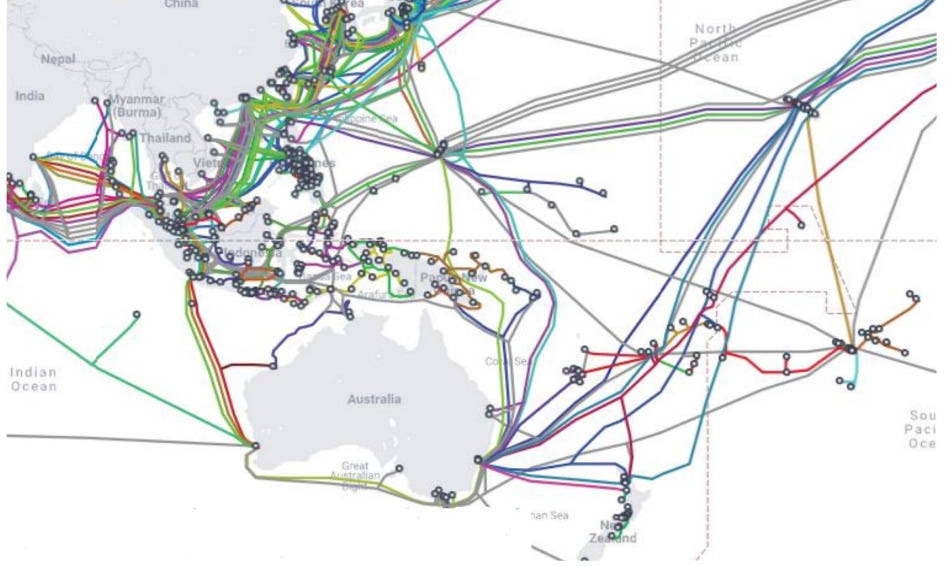

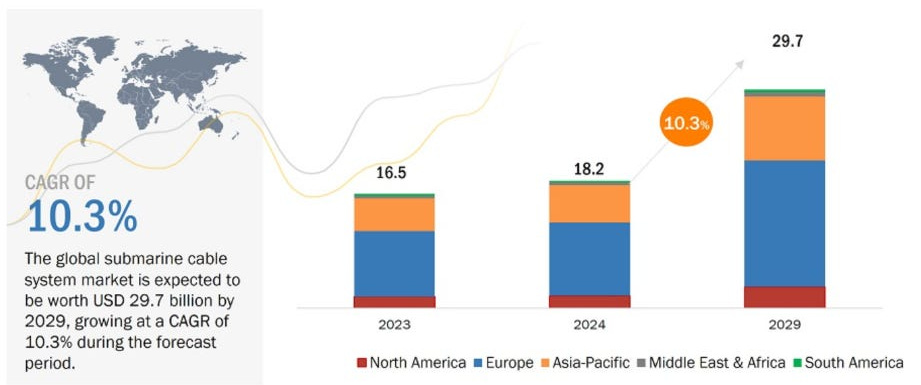

Global Matters: The data centre opportunity for infrastructure investors

In this article, Peter Aquilina (Portfolio Manager - Sustainability), summarises the challenges and opportunities that the growing data centre load demand is providing for infrastructure companies globally.

Read more...

Hedge Clippings | 22 November 2024

Following the build up, media frenzy and speculation leading to the US election, and then the surprise at Donald Trump's resounding victory (except to The Donald himself), everything has gone quiet, relatively speaking.

Read more...

Performance Report: Digital Income Fund (Digital Income Class)

The Digital Income Fund (Digital Income Class) rose by +0.26% in October, outperforming the Bloomberg AusBond Composite 0+ Yr benchmark by +2.14%. Since inception in May 2021, the fund has returned +23.09% per annum, an outperformance of...

Read more...

Performance Report: ECCM Systematic Trend Fund

The ECCM Systematic Trend Fund has risen by +19.91% over the past 12 months, outperforming the SG Trend Index by +27.09%. Since inception in January 2020, the fund has returned +15.09% per annum, an outperformance of +8.12% vs the SG Trend...

Read more...

Macro Research

Australia's monthly CPI inflation data for October is due this coming Wednesday November 27th. It is worth noting that of the four major economies that have already reported their October inflation data, inflation rates lifted in all...

Read more...

Trump wins - what does it mean for sustainability?

Green stocks wobbled as Donald Trump won the US presidential election. Here's what a second Trump term could mean for sustainability.

Read more...

Performance Report: Seed Funds Management Hybrid Income Fund

The Seed Funds Management Hybrid Income Fund rose by +0.97% in October, outperforming the Solactive Australian Hybrid Securities (Net) benchmark by +0.24%. Since inception in October 2015, the fund has returned +6.44% per annum, a...

Read more...

Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

The Skerryvore Global Emerging Markets All-Cap Equity Fund rose by +1.36% in October, outperforming the MSCI Emerging Markets (MMEF) AUD benchmark by +0.15%. Since inception in August 2021, the fund has returned +5.05% per annum, an...

Read more...

Performance Report: Bennelong Long Short Equity Fund

The Bennelong Long Short Equity Fund rose by +3.97% in October, outperforming the ASX 200 Total Return benchmark by +5.28%. Since inception in February 2002, the fund has returned +12.61% per annum, an outperformance of +4.29% relative to...

Read more...