NEWS

15 Nov 2022 - Performance Report: Insync Global Quality Equity Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Insync invests in a concentrated portfolio of high quality companies that possess long 'runways' of future growth benefitting from Megatrends. Megatrends are multiyear structural and disruptive changes that transform the way we live our daily lives and result from a convergence of different underlying trends including innovation, politics, demographics, social attitudes and lifestyles. They provide important tailwinds to individual stocks and sectors, that reside within them. Insync believe this delivers exponential earnings growth ahead of market expectations. Insync screens the universe of 40,000 listed global companies to just 150 that it views as superior. This includes profitability, balance sheet performance, shareholder focus and valuations. 20-40 companies are then chosen for the portfolio. These reflect the best outcomes from further analysis using a proprietary DCF valuation, implied growth modelling, and free cash flow yield; alongside management, competitor, and industry scrutiny. The Fund may hold some cash (maximum of 5%), derivatives, currency contracts for hedging purposes, and American and/or Global Depository Receipts. It is however, for all intents and purposes, a 'long-only' fund, remaining fully invested irrespective of market cycles. |

| Manager Comments | The Insync Global Quality Equity Fund has a track record of 13 years and 1 month and has outperformed the Global Equity Index since inception in October 2009, providing investors with an annualised return of 11.48% compared with the index's return of 10.48% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 13 years and 1 month since its inception. Over the past 12 months, the fund's largest drawdown was -28.54% vs the index's -15.77%, and since inception in October 2009 the fund's largest drawdown was -28.54% vs the index's maximum drawdown over the same period of -15.77%. The fund's maximum drawdown began in January 2022 and has so far lasted 9 months, reaching its lowest point during September 2022. The Manager has delivered these returns with 1.58% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.79 since inception. The fund has provided positive monthly returns 82% of the time in rising markets and 19% of the time during periods of market decline, contributing to an up-capture ratio since inception of 85% and a down-capture ratio of 89%. |

| More Information |

15 Nov 2022 - Magellan Global Strategy Update

|

Magellan Global Strategy Update Magellan Asset Management October 2022 |

|

Nikki Thomas, CFA, Portfolio Manager, discusses the market's reaction to the volatile macro environment, how Magellan's Global Portfolios are positioned and which quality companies are well placed to deliver growth in the years ahead. Speaker: Nikki Thomas, CFA, Portfolio Manager |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. A copy of the relevant PDS relating to a Magellan financial product or service may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to be implemented and its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

14 Nov 2022 - Performance Report: Insync Global Capital Aware Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Insync invests in a concentrated portfolio of high quality companies that possess long 'runways' of future growth benefitting from Megatrends. Megatrends are multiyear structural and disruptive changes that transform the way we live our daily lives and result from a convergence of different underlying trends including innovation, politics, demographics, social attitudes and lifestyles. They provide important tailwinds to individual stocks and sectors, that reside within them. Insync believe this delivers exponential earnings growth ahead of market expectations. The fund uses Put Options to help buffer the depth and duration that sharp, severe negative market impacts would otherwide have on the value of the fund during these events. Insync screens the universe of 40,000 listed global companies to just 150 that it views as superior. This includes profitability, balance sheet performance, shareholder focus and valuations. 20-40 companies are then chosen for the portfolio. These reflect the best outcomes from further analysis using a proprietary DCF valuation, implied growth modelling, and free cash flow yield; alongside management, competitor, and industry scrutiny. The Fund may hold some cash (maximum of 5%), derivatives, currency contracts for hedging purposes, and American and/or Global Depository Receipts. It is however, for all intents and purposes, a 'long-only' fund, remaining fully invested irrespective of market cycles. |

| Manager Comments | The Insync Global Capital Aware Fund has a track record of 13 years and 1 month and has underperformed the Global Equity Index since inception in October 2009, providing investors with an annualised return of 9.52% compared with the index's return of 10.48% over the same period. On a calendar year basis, the fund has experienced a negative annual return on 2 occasions in the 13 years and 1 month since its inception. Over the past 12 months, the fund's largest drawdown was -29.45% vs the index's -15.77%, and since inception in October 2009 the fund's largest drawdown was -29.45% vs the index's maximum drawdown over the same period of -15.77%. The fund's maximum drawdown began in January 2022 and has so far lasted 9 months, reaching its lowest point during September 2022. The Manager has delivered these returns with 0.91% more volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.67 since inception. The fund has provided positive monthly returns 81% of the time in rising markets and 21% of the time during periods of market decline, contributing to an up-capture ratio since inception of 59% and a down-capture ratio of 85%. |

| More Information |

14 Nov 2022 - Drawdowns and small stocks for God-like performance

|

Drawdowns and small stocks for God-like performance Equitable Investors October 2022 "If God is omnipotent, could he create a long-term active investment strategy fund that was so good that he could never get fired?," US-based quantitative investor and author Wesley Gray asked several years ago. Gray's data indicated that God would likely get fired - if God focused on picking investments that would deliver top decile (top 10%) returns over five years. After picking the stocks with perfect foresight and heading out fishing for five years, Gray found God's celestial clients would have endured drawdowns of as much as 76% in the interim. How many clients would have had the stomach to endure that? We semi-regularly take a look back at what the return distribution for ASX industrials has been like over a five year period. It is an exercise that provides data points and context when considering risk and return. We ran the numbers for the five years through to the end of August 2021, and found that:

Source: Equitable Investors, Sentieo Some of the names in the top decile are well known "growth" stocks like Hub24 (ASX: HUB) and Pro Medicus (ASX: PME). But there are plenty of names you may not have heard of - like IT recruitment and labour player HiTech Group (ASX: HIT) and medical diagnostic developer Proteomics (ASX: PIQ). For context, the annualised total returns for both the S&P/ASX 100 and the S&P/ASX Small Ordinaries benchmarks were both around 11% - substantially higher than the median stock in this review. The median stock would underperform indices over five years, if not for any other reason than simply because those indices would be rebalanced through the period in favour of the stocks that are performing. Consistent experienceThe distribution of returns in this period of review was similar to when we ran the same analysis back in May 2018, although in the latest numbers there is a slightly larger portion of stocks that have had negative outcomes (40% now versus 36% then). These figures are also consistent with a US analysis of the total lifetime returns for individual stocks between 1993 and 2006, where Blackstar Funds found 39% of all stocks had a negative return and around 20% were "significant" winners returning 300% or more. Source: Blackstar Funds InsightsKey insights we take out of the data presented here are that:

Author: Martin Pretty Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Nothing in this blog constitutes investment advice - or advice in any other field. Neither the information, commentary or any opinion contained in this blog constitutes a solicitation or offer by Equitable Investors Pty Ltd (Equitable Investors) or its affiliates to buy or sell any securities or other financial instruments. Nor shall any such security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. The content of this blog should not be relied upon in making investment decisions. Any decisions based on information contained on this blog are the sole responsibility of the visitor. In exchange for using this blog, the visitor agree to indemnify Equitable Investors and hold Equitable Investors, its officers, directors, employees, affiliates, agents, licensors and suppliers harmless against any and all claims, losses, liability, costs and expenses (including but not limited to legal fees) arising from your use of this blog, from your violation of these Terms or from any decisions that the visitor makes based on such information. This blog is for information purposes only and is not intended to be relied upon as a forecast, research or investment advice. The information on this blog does not constitute a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Although this material is based upon information that Equitable Investors considers reliable and endeavours to keep current, Equitable Investors does not assure that this material is accurate, current or complete, and it should not be relied upon as such. Any opinions expressed on this blog may change as subsequent conditions vary. Equitable Investors does not warrant, either expressly or implied, the accuracy or completeness of the information, text, graphics, links or other items contained on this blog and does not warrant that the functions contained in this blog will be uninterrupted or error-free, that defects will be corrected, or that the blog will be free of viruses or other harmful components. Equitable Investors expressly disclaims all liability for errors and omissions in the materials on this blog and for the use or interpretation by others of information contained on the blog |

11 Nov 2022 - Hedge Clippings |11 November 2022

|

|

|

|

Hedge Clippings | Friday, 11 November 2022 Superannuation in the spotlight Australia's compulsory super system came under fire this week - or, to be more accurate the inequality of the generous taxation treatment it provides those with higher incomes and higher super balances came under attack. From small beginnings way back in the 1980s, and the love child of Paul Keating and, from memory Bill Kelty (where's Google when you need it?) "Super" has been a super success by all accounts. Unfortunately, it has been tweaked - or raided - over the years, generally by politicians and in particular treasurers who couldn't and can't help themselves, particularly when it comes to other peoples' retirement savings. Having said that, John Howard was probably an exception, looking after his "battlers" with a generous lump sum contribution, which was great as long as you were one of the battlers able to take advantage of it. The issue now appears to be that the Super pie has grown to such an extent, and which is forecast to double again in the not too distant future, that the 15% concessional tax rate on contributions, and the tax free rate when in retirement phase, is costing the budget a motza - particularly for those lucky enough, or smart with high balances. This goes against the grain normally applying to income, wealth, and tax. Normally, unless you're a Kerry Packer, the more one earns, and in many places in the world, the more one is worth, the higher your tax rate. We would hasten to add that Hedge Clippings is no expert when it comes to Super, as might be deduced from the simple explanation above. However, there are a number of arguments both ways, as well as a number of other flaws in the system which were either not recognised previously, or were possibly kicked down the road for some other government to address. The concessional tax rates applying to Super undoubtedly favour those better off, but they're not the ones to blame. The politics of envy being what they are however, it is much easier to now make the beneficiaries out to be the villains. They simply applied the rules as they stood at the time to their best advantage. There would seem to be other issues with Super at the mid to lower end of the scale as well. While accepting the argument that after 40 plus years working and contributing (even if you had no choice and it was your employer doing so) that your lump sum is "yours", surely the majority of it should be paid as a pension or annuity to ensure you don't rely on the welfare system for the remaining 20 plus years you are expected to live for? Irrespective, the stage has been set for yet another re-work of the overly complicated Super rules come next year's budget. In the meantime, we're just being softened up for it by some well placed PR. Finally we can't let the subject of politicians and Super pass without taking a swipe at their own pension arrangements down in Canberra. From memory, non contributory, and at 15% plus, with various other perks, that's inequality! Don't expect that to change in next May's budget papers! Meanwhile to markets: Cryptocurrencies were hammered further this week following the failure of FTX, a crypto exchange, reinforcing the danger not only of the coins themselves, but also the added counterparty risk in an unregulated market. And finally, US markets had their best day on record when inflation came in ahead of expectations. Or could it have been partly the expectation that Donald Trump's "Red Wave" had made not much more than a ripple? |

|

|

Webinar Recording - New Investment Opportunity & Fund Update | Collins St Asset Management 4D inflation podcast (part 1): Paul Volcker, central banks, and the UK | 4D Infrastructure October 2022 Performance News Bennelong Long Short Equity Fund Bennelong Kardinia Absolute Return Fund 4D Global Infrastructure Fund (Unhedged) Bennelong Twenty20 Australian Equities Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

11 Nov 2022 - Federal Budget October 2022-23 (For Adviser Only)

10 Nov 2022 - Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Emerging markets refers to countries that are transitioning from a low income, less developed economy towards a modern, industrial economy with a higher standard of living and greater connectivity to global markets. The strategy is index unaware (meaning that the Skerryvore team decides to invest in individual stocks based on their merit and without reference to the composition of the Benchmark) and the Fund's country and sector allocations will reflect the active bottom up investment approach of the Skerryvore team. The Fund also invests in companies that are incorporated and listed in developed market countries which have economic exposure to emerging markets. The difference in allocation against any emerging markets index can be significant. |

| Manager Comments | The Skerryvore Global Emerging Markets All-Cap Equity Fund has a track record of 1 year and 3 months and therefore comparison over all market conditions and against its peers is limited. However, the fund has underperformed the ASX 200 Total Return Index since inception in August 2021, providing investors with an annualised return of -9.5% compared with the index's return of -1.21% over the same period. Over the past 12 months, the fund's largest drawdown was -13.9% vs the index's -11.9%, and since inception in August 2021 the fund's largest drawdown was -17.45% vs the index's maximum drawdown over the same period of -11.9%. The fund's maximum drawdown began in September 2021 and has so far lasted 1 year and 1 month, reaching its lowest point during June 2022. The Manager has delivered these returns with 5.97% less volatility than the index. Since inception in August 2021 in the months where the market was negative, the fund has provided positive returns 38% of the time, contributing to a down-capture ratio since inception of 49.42%. For performance over the past 12 month, the fund's down-capture ratio is 19.68%. A down-capture ratio less than 100% indicates that, on average, the fund has outperformed in the market's negative months. |

| More Information |

10 Nov 2022 - Performance Report: 4D Global Infrastructure Fund (Unhedged)

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The fund is managed as a single portfolio including regulated utilities in gas, electricity and water, transport infrastructure such as airports, ports, road and rail, as well as communication assets such as the towers and satellite sectors. The portfolio is intended to have exposure to both developed and emerging market opportunities, with country risk assessed internally before any investment is considered. The maximum absolute position of an individual stock is 7% of the fund. |

| Manager Comments | The 4D Global Infrastructure Fund (Unhedged) has a track record of 6 years and 8 months and has underperformed the S&P Global Infrastructure TR (AUD) Index since inception in March 2016, providing investors with an annualised return of 8.24% compared with the index's return of 8.48% over the same period. On a calendar year basis, the fund has only experienced a negative annual return once in the 6 years and 8 months since its inception. Over the past 12 months, the fund's largest drawdown was -10.99% vs the index's -6.34%, and since inception in March 2016 the fund's largest drawdown was -19.77% vs the index's maximum drawdown over the same period of -24.67%. The fund's maximum drawdown began in February 2020 and lasted 2 years and 2 months, reaching its lowest point during September 2020. The fund had completely recovered its losses by April 2022. The Manager has delivered these returns with 0.26% less volatility than the index, contributing to a Sharpe ratio which has fallen below 1 five times over the past five years and which currently sits at 0.63 since inception. The fund has provided positive monthly returns 94% of the time in rising markets and 13% of the time during periods of market decline, contributing to an up-capture ratio since inception of 97% and a down-capture ratio of 99%. |

| More Information |

10 Nov 2022 - Inflation - higher for longer?

|

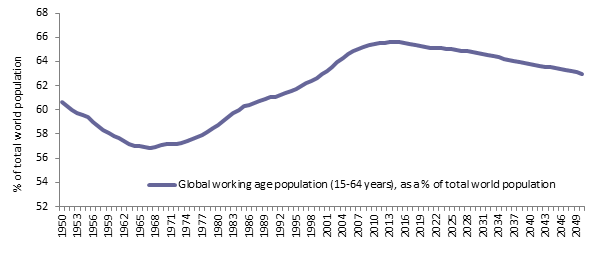

Inflation - higher for longer? abrdn October 2022 Inflation continues to be the dominant economic theme across the globe for governments, central banks and societies at large. The notion of this being a "transitory" phenomenon has been replaced by a realisation that it is much more persistent and far reaching than previously acknowledged. In turn, this has elicited aggressive tightening of monetary policy by central banks in an attempt to tame price pressures. Markets expect policymakers will be broadly successful in achieving this objective. Helpful in this respect are signs that a number of pandemic-related issues, such as supply-chain blockages and labour shortages, are beginning to ease. However, there are a variety of longer term, structural issues at play that should not be ignored as they have the potential to keep inflation elevated for a protracted period. This could further complicate the policy outlook, especially as the economic cycle looks increasingly mature. It's important to remember that the majority of these drivers were evident before policymakers rolled out Covid-induced stimulus packages. They may not be quashed by simply tightening financial conditions alone. It's therefore possible that inflation could become more ingrained globally, and while headline inflation rates may decline from their near-term highs, levels may stay elevated for longer. DeglobalisationA key facet of the mid-1980's 'Great Moderation' in inflation was increasing trade connectivity between countries and growing global interdependence. Ostensibly, developed economies benefited enormously from a liberation of the supply side. Technological advances, political reforms and economic stability allowed companies and governments to more cheaply access key inputs such as labour, raw materials and manufactured goods. In recent years, however, there's been a growing movement away from globalisation. Alarmed by China's increasing global clout, and spurred further by protectionist sentiments, the Trump administration began placing punitive tariffs on Chinese imports in 2018. President Biden has kept many of these tariffs in place. Similarly, political events such as the UK's decision to leave the EU and the embargos on Russian trade and investment are further evidence of the reversal of globalisation. At a corporate level, many firms have been moving towards shorter, more secure supply lines rather than simply the cheapest option. The pandemic exacerbated this trend. We're therefore seeing a reversal of the globalisation trend of recent decades that helped to keep input prices in check. Demographic driversInterlinked with the deglobalisation theme is the evolution of demographic factors, particularly when viewed through the prism of global supply of labour. In the late 1970s, we witnessed the beginning of an upward trend in the global working age population (those aged 15-64). This was led by the baby-boomers and medical advances. It also reflected the liberalisation of global labour markets and access to previously untapped sources of workers. The expanding supply of global labour contributed meaningfully to downward pressure on wages. However, as the chart below shows, this trend has started, and should continue to, reverse. This will potentially lead to a larger proportion of individuals who have little or no productive output but who still consume. In short, we have a situation of reduced labour supply that isn't matched by a material let up in demand. Global working age population (15-64 years), as a % of total world populationSource: UNCTAD e-handbook of Statistics 2021 Exacerbating this demographic trend has been a fall in labour participation rates in a number of developed market economies. There are various theories to explain this phenomenon. For example, large numbers of people unable to work due to 'long Covid,' early retirements and life preference changes. What matters from an inflation perspective is that reduced working age numbers, coupled with reduced participation rates, mean tighter labour markets and increased upward pressure on wages. Greenflation?An increasingly debated potential driver of structurally higher inflation is 'greenflation'. The movement towards a less carbon-intensive economy has been supported by tighter environmental regulations, as well as changing investor and corporate preferences. The result has been much reduced investment in traditional energy infrastructure in areas such as oil and gas. This is felt most acutely when exogenous strains are placed on fragile supply structures, as evidenced by the recent Ukraine conflict. More broadly, it seems unlikely that the transition towards a greener economy will be smooth. Many projects, by their very nature and scale, could take decades if not generations to execute. The implication for energy markets is that they are likely to remain volatile, with potentially increased upside risks to the inflation outlook. Putting everything togetherAlthough there will be regional and country variations, headline inflation in most developed markets appears likely to peak in late 2022 or early 2023. This will give some comfort to central bankers and government officials as it reduces the likelihood of a repeat of the early 1980s where more extreme policy measures were required to tackle excessive inflation. Still, we think inflation will remain a recurring and persistent theme, which will be a significant departure from the trend of the past four decades. With structural patterns apparently shifting, it is crucial that investors consider this evolution when constructing portfolios and recognise the value of real returns alongside nominal equivalents. Author: Adam Skerry, Head of Inflation Rate Management |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund , Aberdeen Standard Life Absolute Return Global Bond Strategies Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund

|

9 Nov 2022 - Performance Report: Airlie Australian Share Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund is long-only with a bottom-up focus. It has a concentrated portfolio of 15-35 stocks (target 25). The fund has a maximum cash holding of 10% with an aim to be fully invested. Airlie employs a prudent investment approach that identifies companies based on their financial strength, attractive durable business characteristics and the quality of their management teams. Airlie invests in these companies when their view of their fair value exceeds the prevailing market price. It is jointly managed by Matt Williams and Emma Fisher. Matt has over 25 years' investment experience and formerly held the role of Head of Equities and Portfolio Manager at Perpetual Investments. Emma has over 8 years' investment experience and has previously worked as an investment analyst within the Australian equities team at Fidelity International and, prior to that, at Nomura Securities. |

| Manager Comments | The Airlie Australian Share Fund has a track record of 4 years and 5 months and therefore comparison over all market conditions and against its peers is limited. However, the fund has outperformed the ASX 200 Total Return Index since inception in June 2018, providing investors with an annualised return of 9.72% compared with the index's return of 7.09% over the same period. On a calendar year basis, the fund hasn't experienced any negative annual returns in the 4 years and 5 months since its inception. Over the past 12 months, the fund's largest drawdown was -16.29% vs the index's -11.9%, and since inception in June 2018 the fund's largest drawdown was -23.8% vs the index's maximum drawdown over the same period of -26.75%. The fund's maximum drawdown began in February 2020 and lasted 9 months, reaching its lowest point during March 2020. The fund had completely recovered its losses by November 2020. The Manager has delivered these returns with 0.01% less volatility than the index, contributing to a Sharpe ratio which has fallen below 1 three times over the past four years and which currently sits at 0.6 since inception. The fund has provided positive monthly returns 97% of the time in rising markets and 11% of the time during periods of market decline, contributing to an up-capture ratio since inception of 111% and a down-capture ratio of 97%. |

| More Information |