NEWS

24 Mar 2025 - The future of healthcare: Trump, policy and innovation

|

The future of healthcare: Trump, policy and innovation Magellan Asset Management March 2025 |

|

Is the healthcare sector ready for transformation amidst uncertainty? Investment Analyst Wilson Nghe explores the current state of the healthcare sector, highlighting the impact of Trump's policy initiatives and the surrounding political noise. Wilson explains that increased uncertainty in the sector adds to higher volatility and regulatory risk, which is crucial in assessing the healthcare sector's outlook and risks. Despite these challenges, there are significant opportunities in healthcare innovation, with companies like Stryker at the forefront of medical technology advancements, and with the rise of GLP-1 therapy development. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Core Infrastructure Fund, Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged) Important Information: Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

21 Mar 2025 - How to Find the Best Stocks After a Market Correction

|

How to Find the Best Stocks After a Market Correction Marcus Today February 2025 |

Why Timing the Bottom is About Sentiment, Not FundamentalsIf you ever say, "I can't buy it, it's gone up 10% in a week," you will struggle as an investor. If you think, "It's up 100%, I've missed it," you doom yourself to conservatism. Chickens don't make money. You will never find a ten-bagger if you're selling at a 10% gain. Thirty-five stocks in the All Ordinaries have more than doubled in the last year, and 90 are up more than 50%. Do not sell because something has gone up--sell because it's going down. In a recovery, the stocks that rise the fastest are often the ones that fell the hardest. If the market has already started bouncing, you must buy stocks that have already gone up. Sometimes, you have to buy stocks that have gone up a lot. The Key Signs of a Market BottomNo one knows exactly when corrections will come. Those who seemed to predict them were only right in hindsight. They made noise at the right time, and then, after the fact, claimed victory. You can't predict a market bottom before it happens--but you can recognise it when it arrives. The key signs to watch for:

The best way to time a top or bottom is to read Marcus Today. Not kidding! Using Market Sentiment to Buy at the Right TimeYou Can't Predict the Bottom - But You Can React to ItDo not think you can be clever enough to predict the bottom before it happens. You can't predict the big sell-offs, just like you can't predict the exact turning point. But you can watch the signs and act decisively. The stock market has an average gain rate of 9% per year. If the market has run well beyond that pace, it becomes vulnerable. But don't act based on warning signs alone--wait until the correction begins, then react. Yes, be more alert when things get ridiculous, but still--wait for the move. When warning signs turn into a major sell-off, be ready to be decisive. Indicators That Show a Recovery is StartingThe moment to buy is not when things look cheap - it's when sentiment turns. Fundamentals won't tell you when to buy. Instead, watch for:

At extreme moments, the market lifts all boats on the way up, just as it sinks them on the way down. If you're trying to time the market, watch the herd--don't follow it. Stock Selection After a CorrectionWhat Stocks Rebound the Fastest?Catching the bottom of a correction is all about sentiment. When everyone has lost faith in the market and is doing 200 miles an hour with their hair on fire, they generally also lose sight of fundamentals. That's an opportunity. But you don't buy on the numbers--you buy on sentiment changing for the better. You need to spot that, and the way to do it is the same way you spot the top: On the balance of probabilities. If the market has fallen a lot, has a big up day or week, and the tone of the commentary is changing for the better, on the balance of probabilities, that is a bottom. Watch the herd, don't join the herd. Avoid These Stocks After a Market CrashFundamentals are useless when it comes to timing the market. It's why value investors can never time the market--a PE ratio will never tell you when to sell or buy. Sentiment watching (price watching) gives you a much better chance. At extreme moments, the market drives all--sinks all boats, lifts all boats. Focus all your attention on identifying the "Pivot Point" in the market. In corrections, the woods are on the move--forget the trees until the forest is going up again. It's no good saying "NAB is cheap" when the GFC is starting. When the market is crashing, everything will look cheap halfway through the sell-down--but you don't buy falling stocks because they're cheap. That's for Buffett quoters. You can't time the market on fundamentals. Lessons from Past Market CrashesWhat History Teaches About Buying the DipStock selection comes second to the market. In a recovery, stock selection is where you will make the most money--but not until you get the market right first. If you get that right, you'll make money in everything. Market first, stocks second. Case Study: How Stocks Recovered from the GFC and COVID CrashThe recovery will come fastest and hardest in the stocks that have suffered the most extreme sentiment swings. In a recovery, it is not the stocks with the best fundamentals that recover the best (far from it). It is the stocks that involve the most sentiment in the price--often the stocks with no fundamentals but the most growth prospects. The stocks that people made the most money in before the top, and lost the most money in during the correction. They rebound the earliest, and they rebound the most. The money is in identifying and timing the extremes of sentiment. Spend the time in cash listing the "fad" stocks you're going to buy in the recovery. It's not NAB. Final Thought: Corrections Are Your Greatest OpportunityAt the end of the day, market corrections are not a threat--they are an investor's best friend. Instead of fearing them, welcome them. They provide the chance to sell at the top and buy at the bottom. If you buy into the industry narrative that "timing the market is impossible," you'll miss some of the best opportunities of your investing life. Corrections create wealth for those who know how to take advantage of them. The only question is--will you? Author: Marcus Padley |

|

Funds operated by this manager: |

20 Mar 2025 - On the Road with Alphinity: Santos Carbon Capture and Storage Project in Moomba, South Australia

|

On the Road with Alphinity: Santos Carbon Capture and Storage Project in Moomba, South Australia Alphinity Investment Management March 2025 |

|

Towards the end of January, Jess was invited to the official opening of the Moomba Carbon Capture & Storage Project (CCS) at Santos' Moomba Gas Plant in northeastern South Australia. The project is designed to store up to 1.7 million tonnes of CO2 per year, which is equivalent to 10% of South Australia's annual CO2 emissions, and is one of the largest operational CCS projects in the world. Santos has also stated that this is one of the lowest cost CCS projects globally, with a lifecycle cost of less than US$30 per tonne of CO2. The Cooper Basin, where Moomba is located, covers 130 square kilometres and stretches 500 kilometres from east to west. The gas field is twice the size of Tasmania and the actual size of England. Out there, the operational team need to bring in or generate everything needed. They generate all the water and bring in the food needed to support 1000 people working on the fields at any one day. There are 150 separate gas fields and 1,000 producing gas wells. A group of about 80 people, including staff, project partners and other key stakeholders, flew in for the day to see the new facility and hear about the achievements of the project team. The site tour was brief, and they were only able to view it from outside the fence. Still, she gained a strong understanding of what a CCS project actually looks like. Essentially, it is a bunch of pipes and pumps in a shed, and Jess was struck by just how simple it all was. In fact, there is nothing that special at the site at all. This is not to downplay the achievement of the company in getting this project up and running, or the capital that has been spent building the pipeline infrastructure across a gas field the size of England. However, in the end, the technology and infrastructure involved are relatively simple. CO2 is captured at the Moomba gas plant and fed through dehydration units, it then goes through a four-stage modified natural gas compressor, and finally the CO2 itself is piped out to five injection wells using a mild steel pipe. First injection at Moomba started mid-2024 and, so far, the team has achieved 98% effectiveness. The main limitation is during days of extreme heat, as the processing power of the compressors needs to be reduced; other than that everything has been working as expected. From here, the focus moves to monitoring and making sure that there are no adverse impacts from injecting CO2 back into the empty gas reservoirs. At this point, there is only one other working CCS project in Australia, which is at Gorgon off the coast of Western Australia. Chevron's Gorgon CCS plant is the largest in the world with the ability to store 4 million tonnes of CO2 per year. Its plant injects the CO2 into a giant sandstone formation two kilometres under Barrow Island. Both projects have been heavily criticised by environmental groups, some investors, and some community members. CCS is still controversial. However, from what we saw during the site visit , this may well be a turning point for CCS in Australia. CCS can be quite expansive to achieve but for Moomba, a few unique attributes has kept the lifecycle cost relatively low. Firstly, CO2 separation was already taking place at the site and secondly, transportation over long distances was not needed. Unlike other developments where hundreds of kilometres of pipelines might be needed, in this case only one 50km pipeline was built. This is the first of a number of CCS projects that Santos is proposing. Although the jury is still out as to whether the economics will work as well as they do at Moomba, the outlook is positive.

|

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Global Sustainable Equity Fund, Alphinity Sustainable Share Fund This material has been prepared by Alphinity Investment Management ABN 12 140 833 709 AFSL 356 895 (Alphinity). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed. |

19 Mar 2025 - Sports Investing: A Rising Global Opportunity

|

Sports Investing: A Rising Global Opportunity Altor Capital March 2025 |

|

The world of professional sports is undergoing a seismic shift, presenting unprecedented opportunities for investors. Previously the exclusive domain of billionaires, sports franchises have emerged as a unique and rapidly growing asset class, driven by robust business models, increasing media rights valuations, and the global appeal of sports as entertainment. The Explosive Growth of Sports InvestmentsSports organisations are becoming increasingly attractive to investors due to their resilient revenue streams, monopolistic market dynamics, and cultural significance. Unlike traditional industries, professional sports have proven to be non-cyclical and resistant to economic downturns. For example, just after the 2008 financial crisis, valuations of major American sports leagues such as the NFL, NBA, MLB, and NHL dropped only 1% collectively-the sole negative year in the past two decades (*Statista). Key drivers of this growth include:

According to the Ross-Arctos Sports Franchise Index sports team valuations in the US have compounded at over 13% p.a. for over 60 years (*RASFI). Valuations from 2000 have outperformed the S&P500 by over 6x. The Media Rights Revolution: A Catalyst for Valuation GrowthThe growth in media rights deals is one of the most significant drivers of increased valuations for sports franchises. The NFL's annual media rights revenue reached US$10b in 2024, while the NBA secured an 11-year deal worth US$76 billion. This trend has propelled the average value of NBA teams to double since 2021 (*Sportico). In Australia, the sports market is following a similar trajectory. The National Basketball League (NBL), while not in the same scale as the NBA or NFL, has seen remarkable growth in fan engagement and viewership. By leveraging media rights and innovative broadcast strategies, NBL franchises have a unique opportunity to replicate the success seen in U.S. leagues. Strategic Ownership: A Key to Unlocking ValueInvestors in sports teams have historically faced challenges related to minority ownership stakes, which often come with limited control over operations. In the U.S., minority stakes have traded at discounts of 10-40%. However, as institutional demand grows, Goldman Sachs predict these discounts will diminish over the next decade. Full operational control allows owners to maximize a team's potential, optimizing revenue streams such as ticket sales, sponsorships, and merchandise. Case Studies: Evidence of Success in Sports InvestmentsSeveral recent examples highlight the transformative impact of strategic investments in sports teams:

The Rise of Women's SportsWomen's sports are experiencing explosive growth, with increasing participation rates and fan engagement. The National Women's Soccer League (NWSL) has seen a dramatic rise in viewership, leading to a media deal worth US$240 million over four years-a significant increase from its previous deal. Similarly, the WNBA's latest media rights agreement is worth a staggering US$200m per season, considerably higher than their previous US$50m per season (*The Guardian) further solidifying women's sports as a key growth segment. Speak to our team today to discover how private credit can transform your business financing. Ownership of Venues: Unlocking Additional Revenue StreamsOwning venues provides significant opportunities to generate revenue beyond sports. Many U.S. team owners utilise their stadiums to host concerts, festivals, and other entertainment events during the offseason. This model has proven highly lucrative and offers a roadmap for other markets, including Australia, to diversify income streams. Australia vs. the U.S.: Comparative Growth PotentialWhile Australia's sports market is smaller than that of the U.S., it is growing rapidly. Using basketball as an example, the NBL has benefited from increased international visibility and talent development, positioning it as the second most important basketball league in the world. The relationship between the NBL and NBA has strengthened significantly in recent years, providing a platform for growth and collaboration. The NBL has become a key developmental pathway for aspiring NBA players, with athletes like LaMelo Ball and Josh Giddey using the league as a springboard to NBA success. This connection has elevated the NBL's profile internationally, attracting talent, sponsorships, and media attention. Additionally, preseason games between NBL and NBA teams have fostered mutual recognition and enhanced fan engagement. These collaborations not only highlight the NBL's growing competitiveness but also position it as a league capable of nurturing top-tier talent. As this relationship deepens, it creates further opportunities for investors to capitalize on the NBL's rising prominence and its alignment with the NBA's global brand. In a significant step toward strengthening this connection, the NBA recently announced its return to Melbourne for two preseason games in 2025, marking another milestone in the growing relationship between Australian and U.S. basketball (*NBA) These games will provide Australian fans with firsthand exposure to NBA talent while further integrating the NBL into the global basketball ecosystem. This reinforces the investment potential in Australian basketball, as its alignment with the NBA continues to drive visibility and commercial opportunities. *statista - www.statista.com/statistics/202758/franchise-value-of-us-sports-teams/ *RASFI - michiganross.umich.edu/faculty-research/partnerships/ross-arctos-sports-franchise-index *Sportico - www.sportico.com/leagues/basketball/2024/nba-team-values-warriors-knicks-lakers-lead-1234820970/ *SBJ - www.sportsbusinessjournal.com/Articles/2024/12/02/cpkc-stadium-kc-current *The Guardian - www.theguardian.com/sport/article/2024/jul/17/wnba-revenue-set-to-surge-with-200m-a-year-broadcast-rights-deal#:~:text=The%20WNBA%27s%20current%20media%20deals,of%20the%20median%20NBA%20salary. - www.theguardian.com/sport/article/2024/jul/17/wnba-revenue-set-to-surge-with-200m-a-year-broadcast-rights-deal#:~:text=The%20WNBA%27s%20current%20media%20deals,of%20the%20median%20NBA%20salary. *ESPN- www.espn.com.au/football/story/_/id/41293395/inter-miami-made-big-bet-messi-paying-off *NBA - www.nba.com/news/nba-australia-melbourne-games |

|

Funds operated by this manager: |

18 Mar 2025 - Minksy, the X-Factor and what to watch

17 Mar 2025 - Investment Perspectives: Share based payments are an expense!

14 Mar 2025 - The infrastructure investment boom

|

The infrastructure investment boom Redwheel March 2025 |

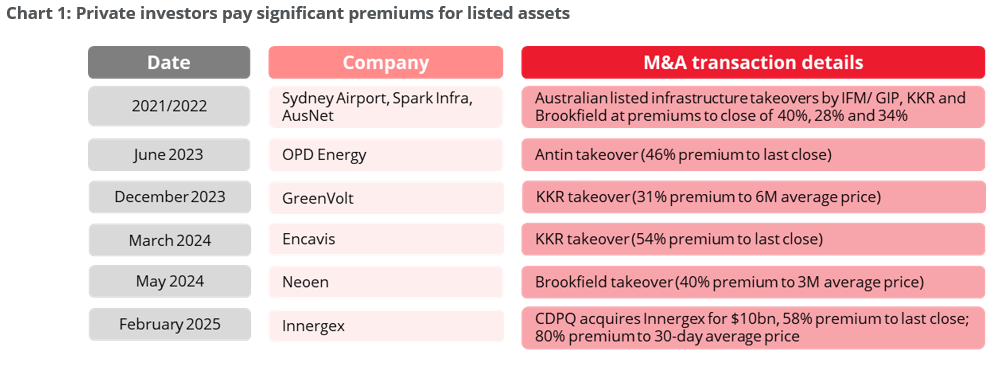

Surging infrastructure needs and private equity fundraising bodes well for listed infrastructure companiesFor years, investors have allocated to infrastructure to reap the benefits of an asset class with attractive return potential, higher yields than equity markets, defensive characteristics and inflation mitigation[1]. Today, investor interest in infrastructure is expected to grow as global electrification, digital innovations, increasing demand for energy and energy security, and the need for efficient transportation drive new development opportunities. Redwheel's Ecofin team believes in the fundamental rewards of a blended approach to investing in listed and private infrastructure. Both investments offer exposures to essential assets critical to the functioning of economies and yield steady cash flows. However, discerning investors will focus on the diversification and access to a range of sub-sectors, geographies, political systems, valuation differences, and liquidity that listed investments can also offer. Listed infrastructure is a complement and a diversifier to private infrastructure Listed infrastructure shares many of the same attractive traits as private infrastructure. Investments are underpinned by real assets with visible cash flows that should provide attractive and consistent returns with low correlations to traditional equities. Listed infrastructure also provides access to high quality assets and leadership teams globally. However, by contrast, listed infrastructure allows investors to gain full exposure immediately and offers the flexibility to adjust allocations based on risk and opportunities. Beyond this, we see four additional advantages that strengthen the case for increasing allocations to listed infrastructure: attractive relative valuation, enhanced risk diversification, a resurgence in M&A activity and greater scope for value capture. Advantage 1: Attractive valuation compared to private assets Valuations of listed infrastructure assets stand at a significant discount to their private equivalents and by historical measures, in our view. While private equity specialists have historically paid premiums to listed assets, justified to a large extent by the majority control of operations, we believe that the valuation gap has increased over the past couple of years. The table below reveals that recent take-out transactions in the space, whether for renewables assets, power & gas networks or transportation infrastructure, have averaged a c.40% premium to listed valuations. Most recently, Caisse de Depot et Placement du Quebec acquired Innergex for a 58% premium over the prevailing share price and an 80% premium to the 30-day volume weighted average price.

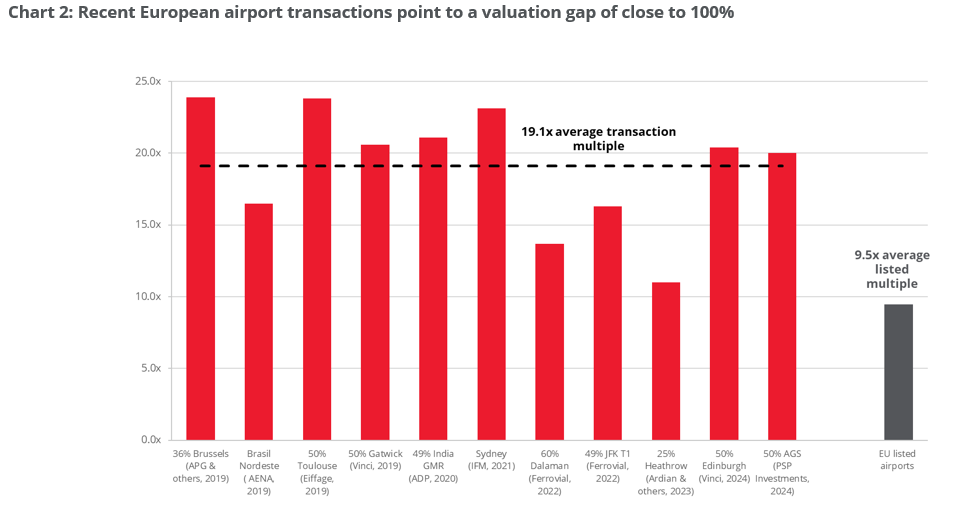

We read this situation as an illustration of the longer-term perspective of typical private equity players while listed equity investors tend to be more focused on the short-term outlook. This is a key differentiator for the analysis of infrastructure, which consists of long-duration assets and projects. The trend also reflects significant inflows into private equity infrastructure funds, generating competition to grasp scarce listed assets on relatively low valuations. A clear example of this valuation gap can be seen in recent transactions for European airport concessions. Since 2019, private M&A transactions have been concluded at valuations (EV / EBITDA) that were appreciably higher than listed assets, with individual premia on several transactions exceeding 100%. While listed airports trade at an average EV/EBITDA of 9.5x, we calculate that the average multiple paid in private transactions over the past six years has been 19.1x EV/EBITDA.

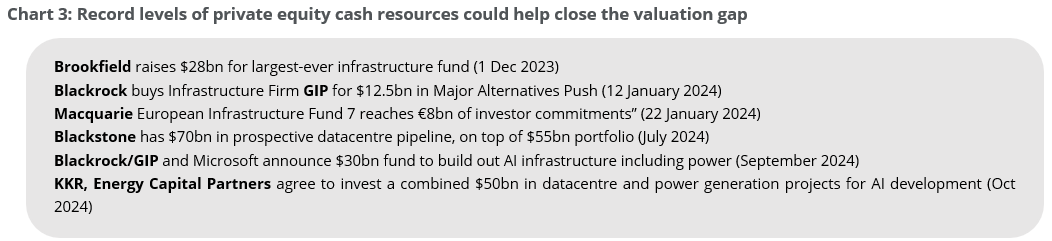

We expect this striking valuation gap to gradually reduce as private infrastructure investors put capital to work in coming years. Investors with private exposure can compound returns in the space by playing both sides of anticipated transactions as well as through rising valuations in listed assets. Over the past year, as shown in the table below, private equity majors have raised more than $100bn to invest in infrastructure. Infrastructure is seen as a portfolio diversifier away from more cyclical businesses, with growth trends underpinned by structural tailwinds in decarbonisation and electrification. The growing needs of AI-driven datacentres to secure their energy supplies fuels further growth prospects for the utilities part of the infrastructure universe. However, the opportunity is broader and more diverse than AI, encompassing the electrification of transportation through electric vehicles, the surge in cooling and heating needs globally, and reshoring initiatives for manufacturing in the US.

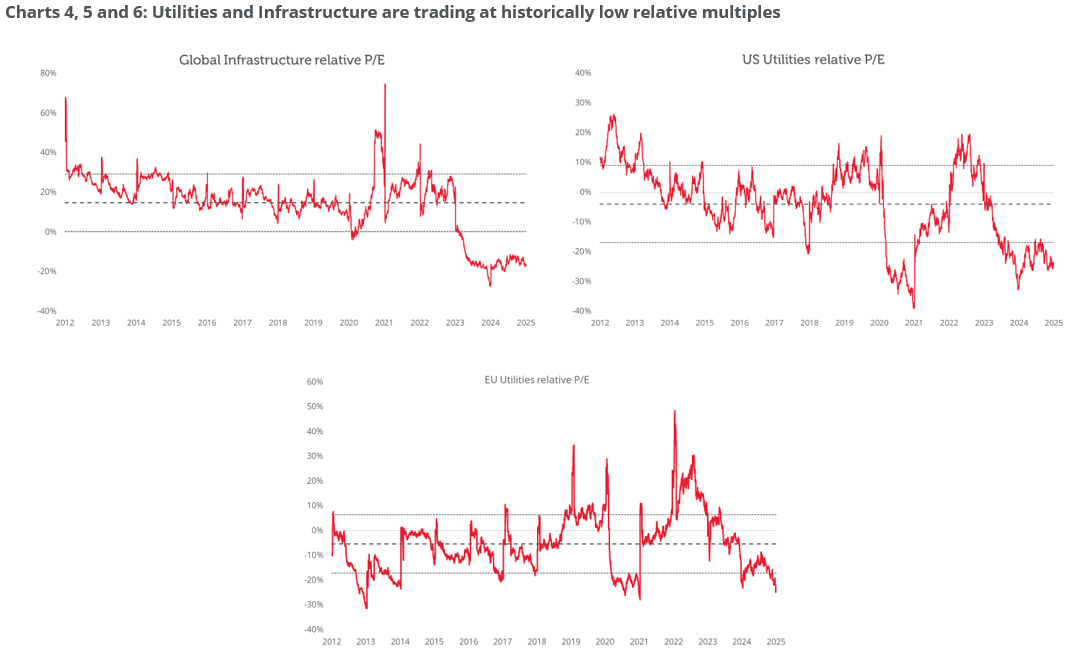

We also note that listed valuations are close to their historical lows relative to general equity indices. The charts below show that global Infrastructure companies have rarely traded at such low relative P/E multiples and Utilities, both US and European, are trading at low relative multiples as well.

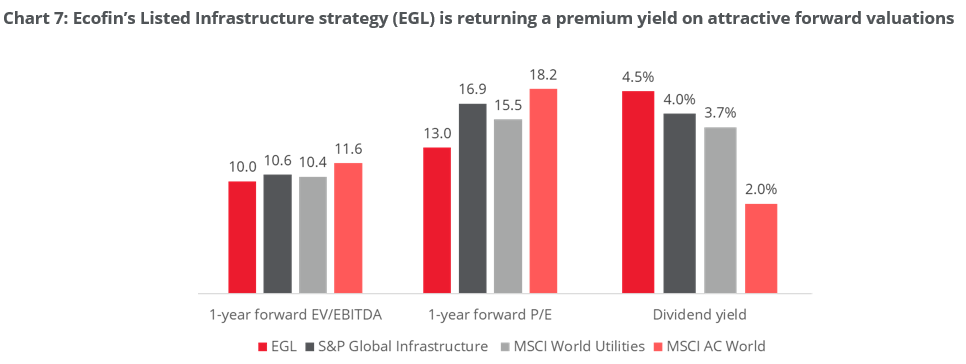

Finally, the chart below further supports our view that listed infrastructure, including Ecofin's dedicated strategy, is attractively valued relative to various market indices, yet offers a higher dividend yield.

Advantage 2: Risk diversification and financial prudence Unlike private ownership, which is typically restricted to a single asset or a small number of similar assets in single regions or countries, listed infrastructure provides the option to invest in companies whose portfolios are diversified across geographies (thereby mitigating interest rate, currency, and regulatory risk) and technologies (e.g., combining wind and solar, intermittent renewables with baseload conventional power generation, toll roads and airports etc.). Beyond portfolio diversification, we would also note a marked difference in financial leverage between public and private companies. While investors often perceive listed infrastructure as riskier than privates due to stock price volatility, the intrinsically more prudent financial structures of listed infrastructure companies - and the resulting mitigation of risk for equity holders - are often disregarded. Listed companies generally need to comply with stricter metrics for their credit ratings, and self-imposed leverage targets often fall well below the rating thresholds to provide equity investors with additional comfort. Listed companies are continually incentivised to retain attractive credit ratings (and correspondingly low financing costs) given their need to periodically refinance debt as developers - as well as owners - of infrastructure assets. Listed infrastructure groups, whether in Europe or the US, have a typical credit rating of BBB+[2].

Advantage 3: The return of big M&A? Constellation's recent acquisition of Calpine[3] (private US gas and geothermal power provider) marks a potential turning point for M&A activity in listed infrastructure. After several years of subdued deal flow, low valuations in publicly traded infrastructure assets are drawing the attention of strategic buyers. High-quality, cash-generating assets have become materially undervalued following periods of rising interest rates and political uncertainty, creating compelling acquisition opportunities. With Constellation's move serving as a strong indicator (close to $100bn combined market capitalisation post-transaction, making it one of the largest transactions in the sector in a decade), attractive pricing could drive a resurgence of big M&A deals in listed infrastructure. We think this should be a clear tailwind for listed infrastructure in 2025 and beyond. The need to reshuffle asset portfolios to adapt to the energy transition, requirements by hyperscalers to get suppliers capable of delivering large amounts of power 24/7, together with significant cash inflows into private equity infrastructure funds, bode well for future consolidation activity in the global infrastructure universe.

Advantage 4: Greater scope for alpha generation A fundamental reason why listed infrastructure could compound higher returns over time is its ability to provide exposure to the full infrastructure value chain. Listed companies typically own operating infrastructure assets and, in most cases, they develop new ones. Having exposure to greenfield projects offers listed infrastructure companies the opportunity to deliver superior returns through operational expertise and efficiencies in the development and construction phases of a project. Construction tends to be a determinant stage during which considerable value is either created or lost. Conversely, private infrastructure portfolios tend to focus on the ownership of operating (brownfield) assets, and there is potentially a more limited scope for return enhancement in the operation and maintenance of these assets.

Listed infrastructure stands out as a competitive structural growth play There is a multi-decade upswing in economic infrastructure development driven by the needs of the modern economy and decarbonisation priorities. Investors, we contest, should increasingly participate via listed securities which screen favourably on valuation and provide important attributes such as liquidity, portfolio diversification and a broad opportunity set. These features should set the scene for listed infrastructure securities to close the valuation gap with private infrastructure assets. Finally, investors will not be able to fully access this opportunity through a broad equity allocation. Listed Infrastructure (and private infrastructure) requires a dedicated allocation. Ecofin's Listed Infrastructure strategy delivers a meaningful yield pick-up over the MSCI AC World index on lower multiples - see Chart 7 - yet the portfolio represents only 1.6% of the index's market capitalisation and there is no overlap with its top 80 constituents[4]. To access the secular growth and value opportunities in listed infrastructure, investors are encouraged to seek specialised allocations. |

|

Funds operated by this manager: Redwheel China Equity Fund, Redwheel Global Emerging Markets Fund |

|

Key Information Sources: [1] Redwheel and Morningstar, February 2025 [2] Bloomberg, December 2024 [3] Reuters, January 2025 [4] Source: Bloomberg and Redwheel. EGL data as of February 2025; MSCI data as of January 2025 |

13 Mar 2025 - The state of the energy transition: Where are we now?

|

The state of the energy transition: Where are we now? Janus Henderson Investors February 2025 While the politics of climate are changing, the prevailing trends continue to reveal significant investment opportunities in the energy transition, as outlined by Tal Lomnitzer.

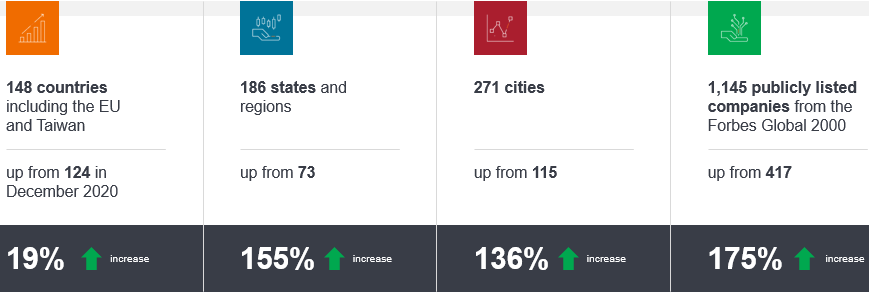

The victory of Donald Trump in the US presidential election, coupled with a lacklustre COP29 climate conference in Baku, has prompted concerns about the state of the energy transition, with some fearing progress may slow or even reverse. Such concerns are underscored by the 2024 average global temperature reaching 1.8°C above pre-industrial levels in 2024 - marking it as the first year to surpass the 1.5°C target limit. Despite rising global temperatures and the Trump administration withdrawing the US from the Paris Agreement for the second time, we still see opportunity for investors to profit from the prevailing trends underlying the energy transition. Rising corporate commitment to net zeroExhibit 1 offers a snapshot of how net zero commitments have grown over the past five years. What stands out is the notable surge in Forbes Global 2000 corporations committing to net zero over the past few years. This is significant, since these 2000 companies are responsible for approximately 20% of global embodied emissions, considering both their operations (scope 1 and 2) and supply chains (scope 3) emissions. Exhibit 1: Commitments to net zero have grown since 2020

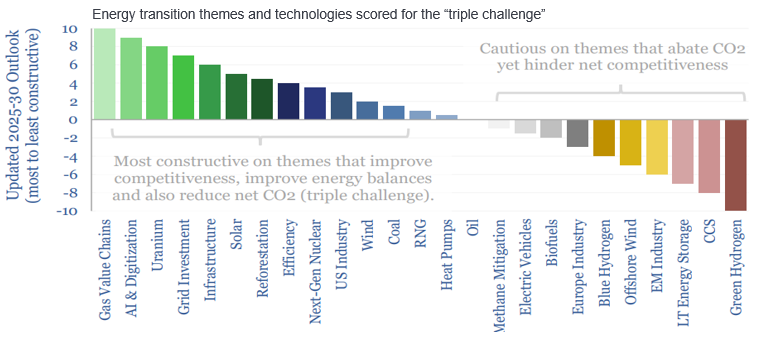

Source: Net Zero Tracker, as at September 2024. While the nature of these companies' net zero commitments varies widely, with some aiming for carbon neutrality, some for zero emissions, and others focusing on Scope 1 (direct) and 2 (indirect) emissions but not Scope 3 (value chain), the overall trend is one of growth, both in the number of commitments and the entities making them. Further, there has been a significant rise in targets enshrined in national policy in the past few years, with 88% of global emissions, 89% of the global population and 90% of global GDP covered by some form of national commitment or net zero target. The 'glass half full' perspective is a significantly higher level of ambition, but with the average global temperature in 2024 already 1.8°C above pre-industrial levels, the need for countries to address greenhouse gas (GHG) emissions faster and deeper is mounting. As it stands the race against time to net zero is arguably being lost if we want to keep below 2°C, and many entities still lack emissions reduction targets. The triple challengeWhen we examine the state of the energy transition from both a pragmatic and investment perspective, the three axes of the 'triple challenge' need to be considered. This encompasses the challenge of enhancing competitiveness by providing cheap energy, improving the energy balance by providing more energy, and simultaneously addressing the GHG emissions present in our atmosphere. A useful analysis from Thunder Said Energy (Exhibit 2) of various energy technologies and themes within the context of decarbonisation, ranks them by how much they address the triple challenge, with those on the left side improving competitiveness and those on the right side reducing competitiveness based on current economics. Exhibit 2: Triple challenge framework

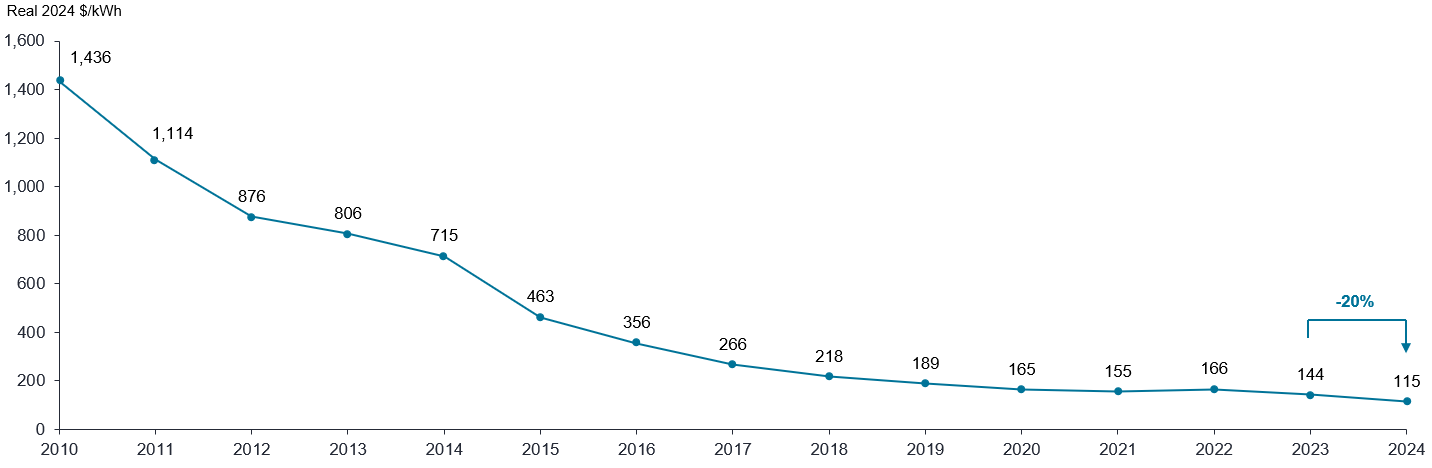

Source: Thunder Said Energy. The public statements from the Trump administration regarding renewable energy in our eyes seem less about being against decarbonisation per se and more about being pro-competitiveness. In this context, competitiveness equates to affordable energy, whereas anti-competitiveness is synonymous with expensive energy. Therefore, our investment focus favours companies that offer inexpensive energy solutions and contribute to lowering carbon emissions, such as the value chain of gas, including LNG, gas storage, and transport, along with AI, digitisation, and nuclear energy. Nuclear energy, in particular, is seen as a significant advantage for those seeking base load power with a minimal carbon footprint and self-sufficiency, especially considering that the US and Canada have abundant uranium resources or the potential for it, thus reducing dependence on potentially unfriendly suppliers such as Russia. Our investments are also directed towards grid investment, solar, energy efficiency, reforestation and other areas where we see strong returns and growth prospects that address the challenges of the energy transition. Conversely, we are currently avoiding sectors that, while potentially reducing carbon emissions, could impede competitiveness. These include green hydrogen, carbon capture storage, offshore wind, and blue hydrogen. These areas represent the more costly segments of the energy market, which we are deliberately choosing not to focus on, pivoting instead towards investments that align with improving competitiveness whilst also delivering more sustainable energy solutions. The economic case for solar energyWe were surprised to discover that during the first Trump presidency, the US experienced its fastest pace of solar installation, with Texas, an oil and gas stronghold, surpassing California in solar installations. This surge is attributed to the declining costs of solar photovoltaic (PV) systems with storage, making solar energy increasingly competitive against natural gas in the US, and even cheaper than coal-fired power in India and China on a levelised cost of energy (LCOE) basis. The reason for this cost reduction is twofold: the virtually inexhaustible nature of solar energy and the semiconductor technology it employs, which has historically seen efficiency gains and cost reductions over time. Currently, solar panels have achieved 25% efficiency in converting sunlight to electricity, a significant improvement from 5% two decades ago, with the potential to reach 50% efficiency. This improvement, alongside increased production volume, has driven down costs to approximately four to five cents per kilowatt-hour, with projections suggesting a future decrease to between one and two cents. As a result, solar energy has become the lowest-cost form of generating electrons globally. In Europe, solar production capacity is expected to triple between 2020 and 2024, outpacing both onshore and offshore wind, due to superior economics. Similarly, cost reductions are observed globally, driven by technological advancements and increased efficiency, not solely by low-cost Chinese production. The imposition of tariffs on imported solar panels could significantly benefit US solar companies that produce panels domestically by increasing their profitability due to higher margins. We anticipate further production expansion in the US as a result of these tariffs and view any additional tariffs as a highly positive development for domestic solar panel producers. Similarly domestic producers of key materials such as steel stand to benefit in a world of higher tariffs. Energy storage costs continue to fallAs utility scale solar installations increase the intermittent nature of the electricity causes power price volatility which necessitates effective energy storage solutions. The economic case for energy storage which enables energy price arbitrage becomes increasingly compelling as price volatility rises, while the costs associated with developing and deploying these technologies have significantly declined. For instance, the price of lithium-ion battery packs has plummeted from US$1,436 per kWh in 2010 to US$144 in 2023, marking a 90% decrease over approximately 13 years (Exhibit 3). Exhibit 3: Lithium-ion battery pack prices

Source: Bloomberg New Energy Finance (BNEF), as at 10 December 2024. Past performance does not predict future returns. Despite a seeming plateau in battery prices on the chart, prices continued to fall by 20% last year, with expectations for ongoing reductions. This cost reduction has catalysed a surge in battery storage installations. In 2023 alone, 60 gigawatts of energy storage were installed, enough to power 60 million homes representing a 120% increase year-on-year. Projections for 2024 estimate over 100 gigawatts of installations, with future expectations reaching up to 1 terawatt annually by 2030 and three terawatt-hours annually by 2050. By then, solar power with associated storage could contribute 43,000 terawatt-hours to the grid, driven primarily by economic feasibility rather than regulatory enforcement. Notably, in 2023, China led the world in energy storage installations, accounting for almost 50% of global capacity, with the US and the rest of the world trailing significantly. This highlights China's leadership in energy storage and underscores the need for other countries to accelerate their efforts in this domain. However, even this fast pace of energy storage deployment is arguably insufficient. To maintain alignment with the 1.5°C target, approximately 1,300 gigawatts of battery storage will be needed by 2030 according to the IEA, a goal that current estimates suggest we are unlikely to meet. Present trajectories indicate a potential global temperature increase of 2-3°C. Trump does not necessarily put a spanner in the worksWe believe that it is highly unlikely that businesses will abandon their decarbonisation efforts, as these initiatives extend beyond any single presidential term. The trend of directly sourcing clean energy is established and enduring, propelled by the economic benefits of large-scale wind and solar projects and the rising costs of grid-supplied electricity, with an added push from investments into Artificial Intelligence. Despite news of the US once again exiting the Paris Agreement and reducing subsidies, the momentum towards electrification, digitalisation, and decarbonisation is likely to continue in areas that support growth and competitiveness. As Exhibit 4 shows, clean energy capacity has grown and annual carbon emissions have fallen under both Democrat and Republican administrations in the US. Exhibit 4: US clean energy capacity vs. annual CO2 emissions

Source: ARNnet; IEA; World Economic Forum; Dean H. Barrett and Aderemi Haruna, Molecular Sciences Institute, School of Chemistry, University of the Witwatersrand; US Department of Energy; Jefferies Research, as at 30 November 2024. An increasing role for nuclear powerWe firmly believe in nuclear energy as a technology capable of providing low carbon base load power. Our current exposure to nuclear energy via uranium producers exceeds that of solar, although we plan to increase our investments in solar. However, timing is crucial, especially considering the potential negative headlines associated with solar under certain political climates. Interestingly, major corporations like Microsoft have engaged in substantial agreements with nuclear energy providers, such as the deal with Constellation Energy to restart Three Mile Island, at prices significantly higher than those of solar energy. This indicates a willingness among the world's wealthiest corporations to invest in reliable low carbon energy sources. Bottlenecks for growthFrom an investment perspective, we focus on identifying bottlenecks in energy supply chains, as these areas tend to offer excess economic returns, leading to high returns on investment and positive share price performance. One such bottleneck is the increased demand for critical metals required by nuclear and solar technologies, as well as electric vehicles, compared to traditional energy sources like coal and natural gas. This demand encompasses a variety of metals essential for the transition to green energy, including rare earth metals, zinc, graphite, nickel, lithium, and copper (Exhibit 5). Exhibit 5: Critical Minerals used in selected clean energy technologies

Source: IEA Critical Miners Report, as at December 2023. The Role of Critical Minerals in Clean Energy Transitions, IEA, Paris https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions, License: CC BY 4.0 Further, several factors contribute to the rising demand for these metals, including the shift towards de-globalisation (onshoring) and localisation of supply chains, changes in consumer behavior, increased military spending, and the expansion of data center capacity, which alone requires significant amounts of copper. However, the mining industry is likely to face challenges in meeting this demand, unless real investment increases significantly. This suggests a need for higher commodity prices to incentivise increased production. Historical data on commodity price cycles indicate potential for significant growth in the coming decades, offering an attractive investment opportunity in the resources sector. This sector not only provides diversification and inflation protection but also trades at a valuation below the historic average compared to the broader market. Navigating the complexities of the energy transitionOur responsible resources strategy focuses on the critical enablers of the energy transition, but we also have a climate transition strategy that takes a diversified approach to capitalising on these growth dynamics, focusing on green solutions, enablers of these solutions, and improvers who apply these solutions to enhance their operations. By investing in this manner, we aim to generate returns for our investors alongside a positive impact for the planet. The journey toward net zero presents a dynamic and evolving landscape filled with opportunities for investors to contribute to a sustainable future while seeking profitable returns. By understanding the complexities of the energy transition and strategically navigating its risks and opportunities, we believe that investors can position themselves to benefit from the shift toward a cleaner, more sustainable global economy and generate good returns. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund, Janus Henderson Australian Fixed Interest Fund - Institutional, Janus Henderson Cash Fund - Institutional, Janus Henderson Conservative Fixed Interest Fund, Janus Henderson Conservative Fixed Interest Fund - Institutional, Janus Henderson Diversified Credit Fund, Janus Henderson Global Equity Income Fund, Janus Henderson Global Multi-Strategy Fund, Janus Henderson Global Natural Resources Fund, Janus Henderson Tactical Income Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

12 Mar 2025 - Fun and games in macro markets

|

Fun and games in macro markets abrdn February 2025 If you were to judge the year so far by absolute yield moves, 2025 would seem quite a sedate affair. In bond markets, we're roughly where we started in terms of yields. However, scratch beneath the surface and you'll find a whole lot of headline-driven volatility. As expected, the Bank of England (BoE) and European Central Bank (ECB) cut base rates this year, while the US Federal Reserve (Fed) stayed on hold. No prizes for getting that right. But congratulations if you also had a 12-hour UK gilt mini-crisis and then an A.I.-led risk-off rally on your 2025 bingo card. One man has been playing all the cards: US President Donald Trump. He's back to what he does best - driving the narrative. In a blizzard of executive orders, policy hints, and off-the-cuff comments, Trump has covered an array of topics in just a few weeks. The two subjects that have markets most captivated? Tariffs and Ukraine. Tariffs started off slow with Colombia in the firing line, before Mexico and Canada came hurtling into view. After giving the US's closest trading partners a one-month stay of execution, Trump moved onto a sector-specific approach targeting aluminium and steel. We've since moved onto 'reciprocal tariffs' but will have to wait until April to learn the rules of that particular Trump tariff game. What is clear is that Trump hasn't changed from his first term. He likes to play games with his rivals. However, what's less clear is how Trump solves his own US economic puzzle. It won't be easy. US - Rubik's CubeTrump's economic strategy is a lot like a Rubik's Cube. The goal of the Hungarian 3D puzzle is to align all the blocks so that each side shows the same colour. The tricky part is that each layer turns independently, so focusing on one side can throw the others out of whack. Trump's goal is to 'Make America Great Again' and oversee a thriving US economy as he heads into the 2026 mid-term elections. To achieve this, inflation needs to be under control. This was the key problem for President Biden, who saw US growth and job creation accelerate but prices outpace wages. Inflation peaked at 9.1% in the summer of 2022. Trump has two years to make the average American feel richer. Back to the Rubik's Cube. To prioritise American jobs for American people, Trump is applying tariffs and slashing immigration. That's one side of his policy cube looking complete. However, these polices, combined with mooted tax cuts, are potentially inflationary - pushing the other side of the cube out of line. Price pressures are not like they were during Trump's first term. The most recent Consumer Price Index read 3% year on year, and consumers still feel the pinch of much higher price levels. It wouldn't take much for inflation to move back into uncomfortable territory. The prospect of rate hikes would move yet another side of the Trump Rubik's Cube in the wrong direction. Keeping inflation in check is possible. Trump wants to pursue lower energy prices and, with Elon Musk's help, drastically cut government spending. But again, how will aggressive government spending cuts affect the growth side of the cube? We'll watch the data with interest. On the tariff front, we should hear what 'reciprocal tariffs' look like at the start of April. On tax cuts, we await more details and substance. Research shows that any Rubik's Cube can be solved in 20 moves. We think it will take a lot more than this to complete Trump's economic puzzle. US yields have the potential to head higher as a result. UK - dodging snakes and climbing laddersThe UK faces a game of snakes and ladders. The ultimate prize is lower interest rates. The BoE cut rates in February with the message of 'gradual and careful'. Inflation is likely to move higher in 2025, but the BoE seems comfortable with its long-term forecasts. The Bank believes any near-term rise in inflation will be temporary and that it can continue to cut base rates. The BoE's first possible ladder up the board is the continued loosening of the labour market. Most indicators show the jobs markets rapidly cooling. This will embolden the BoE to speed up rate cuts when this feeds through to the official wage data. A smaller ladder comes in March: we might see more aggressive government spending cuts if the Office of Budget Responsibility review shows Chancellor Reeves is close to breaking her own fiscal rules. Reduced government outlays would likely to inhibit growth and increase the probability of cuts. The largest, fiercest snake is inflation. Increases to the national living wage and national insurance contributions kick in from April. There's a risk many firms will pass these costs onto consumers. The BoE expects only a modest price increase as a result, yet there's still scope for an inflationary surprise. The way these policy changes feed through to the real world will determine how quickly the BoE can get to the top of the snakes and ladders board. Our view for some time has been that the BoE gets there quicker than the market expects. We think labour market weakening will outweigh the risk of inflation. We are, as a result, happy to remain long gilts. Europe - GAAAAAMBLE?!Europe, and Germany in particular, face a classic gameshow dilemma: stick with what they've won or gamble for the star prize and risk walking away with nothing? Cue the slick gameshow host turning to the crowd for advice. In Europe, the answer is gaaaamble. Former ECB Chairman Mario Draghi's recent report argued for further European investment. French President Macron said that Europe cannot remain herbivores (see our last article Fixed income: Eat meat or die...). As we write, the new Trump administration is making it abundantly clear that Europe needs to step up, particularly in defence spending. The German election might offer the opportunity for one of Europe's core economies to reset its relationship with borrowing. This would have far reaching implications for the Eurozone's future direction. From an investment perspective, we think it's inevitable that Europe will start spending, despite the previous efforts at fiscal restraint. Leading figures in the European establishment have even called for some relaxation of fiscal rules via exceptions for defence spending. This will be uncomfortable for the likes of Italy and France with their high debt-to-GDP ratios. For Germany, this could mean a new government revisiting the 'debt brake'. The ECB might prefer that Europe plays it safe. With an unclear outlook and a challenging balance between growth and inflation, the ECB is noticeably hesitant. It may well signal a slowing of rate cuts. For these reasons, we think European yields can head higher, with a bias for the yield curve to steepen. Playing the game in today's marketsMarkets are so far brushing off the policy noise. We'll need details before yields start to move in either direction on a sustained basis. For now, we expect key participants to continue playing without fully revealing their hand. In this environment, investors can see the value in actively managed funds. Making the most of short-term mispricing and careful position management offers plenty of opportunities for the nimble active investment manager. Like all games: you have to be in it to potentially win it. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund, abrdn Emerging Opportunities Fund, abrdn Global Corporate Bond Fund (Class A), abrdn International Equity Fund, abrdn Multi-Asset Income Fund, abrdn Multi-Asset Real Return Fund, abrdn Sustainable International Equities Fund |

11 Mar 2025 - DeepSeek R-1: A Game-Changer?

|

DeepSeek R-1: A Game-Changer? Insync Fund Managers February 2025 Relatively unknown Chinese Quant Fund Manager - High Flyer Capital Management's chatbot, DeepSeek, has shaken the AI industry with its new reasoning model, R-1. This open-source breakthrough delivers ChatGPT-level performance at a purported 90% lower cost, using far fewer and less powerful GPUs. The Impact: A fundamental shift in AI economics--lowering costs, reducing hardware dependency, and making AI more accessible to new entrants. Investors took note, with at one stage $1.2 trillion wiped off U.S. markets, led by Nvidia's sharp decline. Why This Matters: Historically, AI has been dominated by capital-intensive models requiring massive computational power. DeepSeek's efficiency-driven approach challenges this, showing that AI can be developed at a lower cost and lower energy consumption. This opens the market to smaller players, accelerates innovation, and could curb the dominance of AI giants like OpenAI, Google, and Meta. Three large investment implications arise; Big Tech's AI Moat Narrows. Open-source models threaten pricing power and market dominance. AI Costs Plummet & Adoption Accelerates. Expect new applications and broader AI integration. Capex Strategy Shift. Firms like Meta and Microsoft will likely double down on efficiency, and may scale back on AI investments. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |