NEWS

Performance Report: Quay Global Real Estate Fund (Unhedged)

The Quay Global Real Estate Fund (Unhedged) rose by +7.49% in January, an outperformance of +2.61% compared with the FTSE EPRA/ NAREIT Developed NET TR benchmark which rose by +4.88%. Since inception in January 2016, the fund has returned...

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund rose by +7.74% in January, an outperformance of +1.51% compared with the ASX 200 Total Return benchmark which rose by +6.23%. Since inception in November 2017, the fund has returned +17.93% per annum,...

Read more...

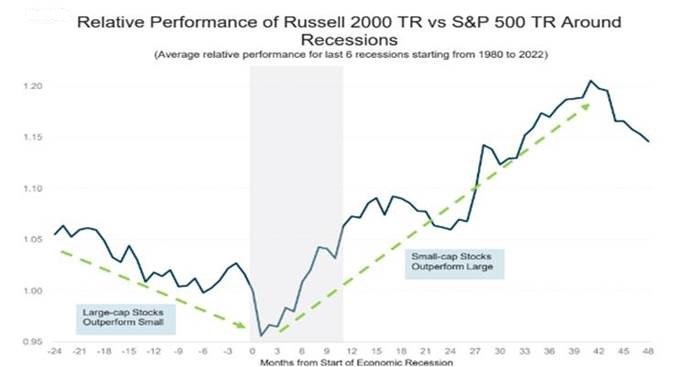

Is now a good time to start considering smaller companies?

Last year was terrible for equities. A war in Ukraine, soaring inflation, higher interest rates and weak economic growth all weighed on sentiment. Globally, both small and large caps were firmly in negative territory. Large-cap indices...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +6.78% in January, an outperformance of +0.55% compared with the ASX 200 Total Return benchmark which rose by +6.23%. Since inception in January 2013, the fund has returned +12.76% per annum, a difference...

Read more...

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund rose by +11.33% in January, an outperformance of +5.1% compared with the ASX 200 Total Return benchmark which rose by +6.23%. Since inception in February 2009, the fund has returned...

Read more...

Magellan Global Strategy Update

Magellan's Portfolio Managers Nikki Thomas, CFA and Arvid Streimann, CFA, discuss how they are viewing the current inflationary environment and chances of a recession.

Read more...

Performance Report: L1 Capital Long Short Fund (Monthly Class)

The L1 Capital Long Short Fund (Monthly Class) rose by +3.67% in January. Since inception in September 2014, the fund has returned +21.29% per annum, a difference of +13.55% relative to the ASX200 Total Return which has returned +7.74% on...

Read more...

Performance Report: Bennelong Australian Equities Fund

The Bennelong Australian Equities Fund rose by +9.96% in January, an outperformance of +3.73% compared with the ASX 200 Total Return benchmark which rose by +6.23%. Since inception in February 2009, the fund has returned +12.15% per annum,...

Read more...

Performance Report: Argonaut Natural Resources Fund

The Argonaut Natural Resources Fund rose by +9.91% in January, an outperformance of +3.68% compared with the ASX 200 Total Return benchmark which rose by +6.23%. Since inception in January 2020, the fund has returned +45.39% per annum, a...

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +0.74% in January, an outperformance of +0.09% compared with the RBA Cash Rate + 5% benchmark which rose by +0.65%. Since inception in April 2018, the fund has returned +11.27% per annum, a difference of...

Read more...